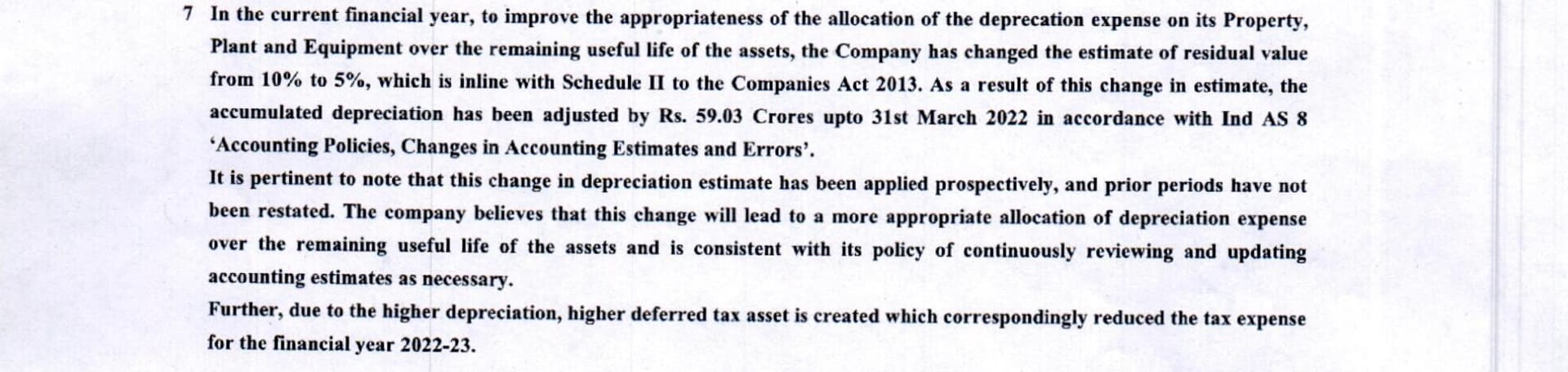

There is an excess depreciation of 59 Crores. so if we add that then PAT will be much higher than last quarter. Secondly, if you look at the balance sheet there is still a capital WIP of 137 crores. This means that one of their pulp mills is still not operational. That benefit should come in the next quarter. So, if there is a fall in the share price on Monday, I will definitely load up.

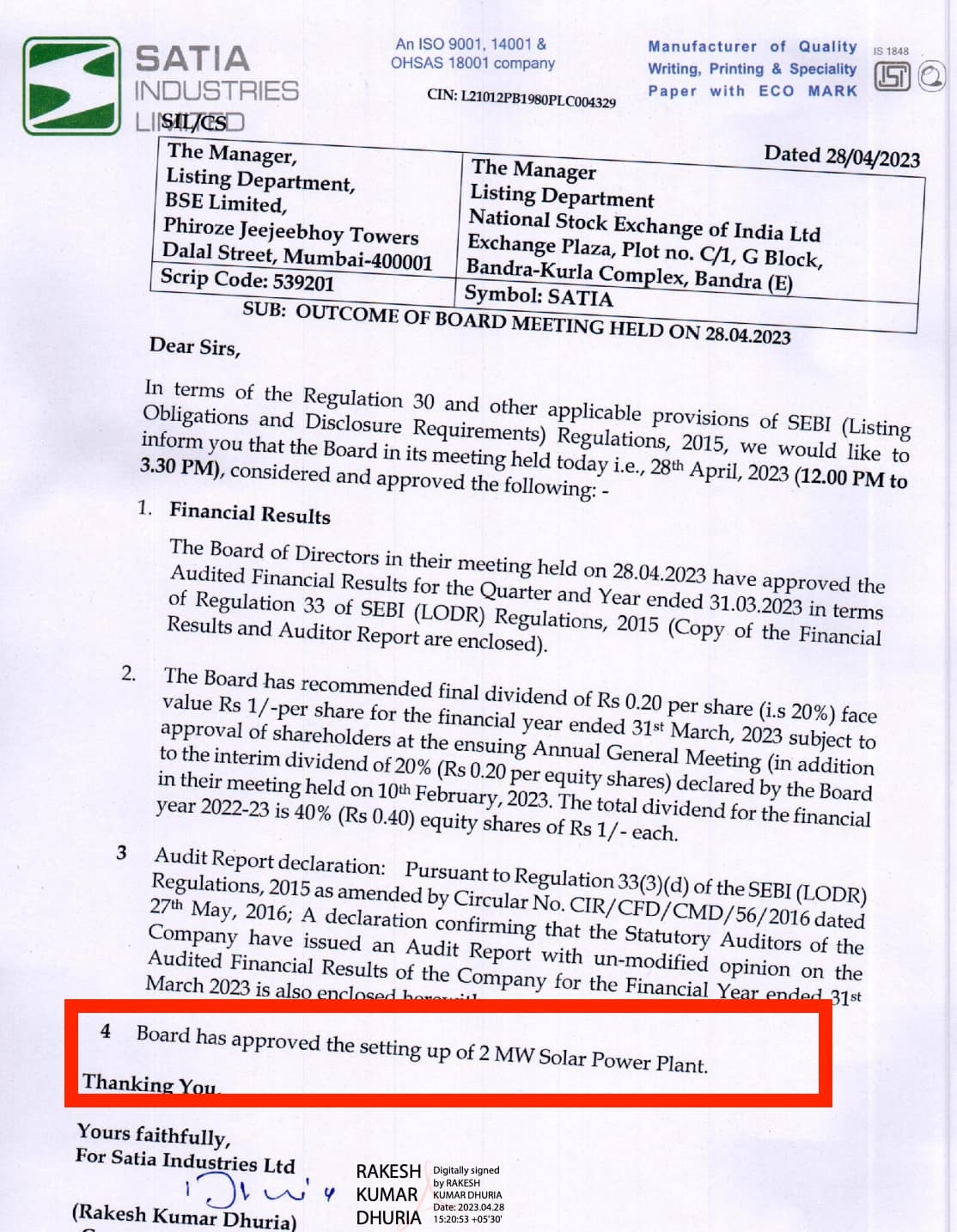

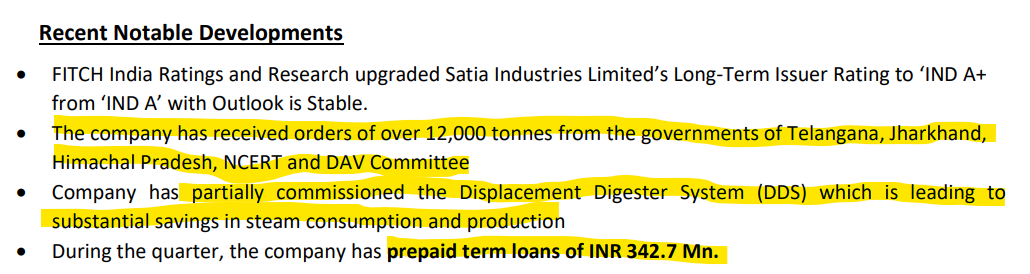

They have also announced the setting up of a 2 MW solar plant. That should lead to a decrease in their energy costs which have been a persistent pain point for the past few quarters.

Satia recently got triggered in my screener and was going through the industry dynamics and company profile. Today the FY23 result came out and I think it was good enough but stock tanked 2%. But I believe that if everything looks good but still the stock goes down then it would required further due diligence. I would be grateful if the knowledgeable members following this company can provide inputs as to why the stock price is stagnant since last year.

JK also has similar valuation then wont it make sense to invest in a larger company?

True, but energy prices and Caustic Soda prices have also fallen massively. Both of these are a very big part of the company’s costs. Caustic Soda prices have nearly halved. Additionally, their new pulp mill will be fully operational from next quarter onwards. This would end their massive capex program and free cash flow from hereon, leading to even more debt reduction.

They are also setting up a 2 MW Captive solar plant. This should aid in bringing down their power costs. Lastly, in the concall the management mentioned that they had to employ additional 500 people for the new plants and thus there was an increase in their employee costs, this is why employee cost as a % of revenue was very higher this time; this should normalize after the plants reach optimal utilization.

Paper Mills have already started to shut down even when Satia has guided for 21% margins for the year. The next wave of consolidation and market share increase coming soon.

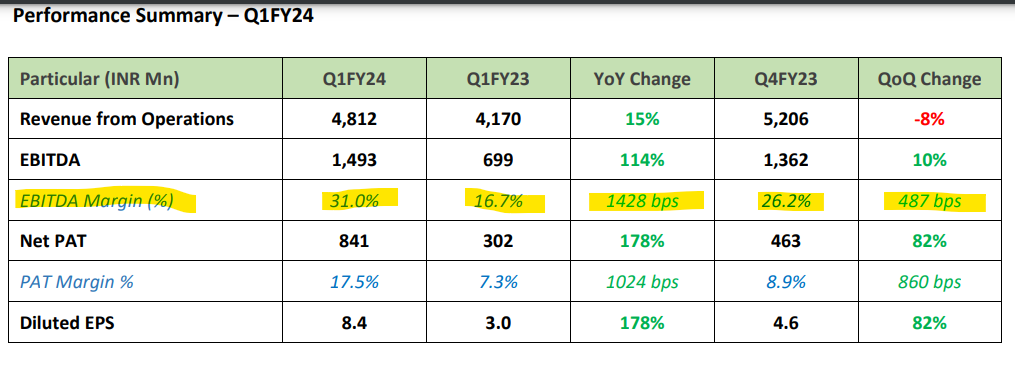

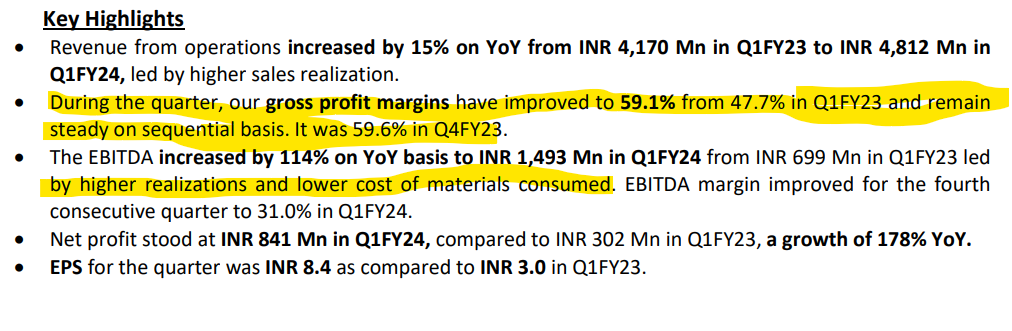

Super Improvement in Operational Efficiency. The key question in my mind is - if they will be able to maintain such operational performance in terms of gross margins - @Rafi_Syed or @kalpesh4430 can share view.

I don’t think margins of this quarter will sustain as paper prices have started to fall as per JK concall but any way Sept margins were 20% so next quarter margins should be better than that as operational efficiencies have kicked in. In March they had paid more debt hence profit looks optically low so PE is less than 5 as of now. Avg PE is 8 as per screener and as they are trying to be efficient I think next few years should see the effect and if they maintain margins market will reward them.

@Rafi_Syed@Vishal_Jajoo & Others. Thank you for details on this. I am wondering anyone has not mentioned or compared Satia Industries with comparable Kuantum Papers on this thread so far or I am missing something.

Kuantum Paper also operates from Hosiarpur, Punjab with almost same legacy since 1980. They have installed capacity of close to 2 Lakh tonnes with quarterly production of 35,000 + tonnes.

They had taken term loans for expansion started in 2019 and availed moratorium due to COVID. But they have repaid all loans ahead of schedule (details available in concall / investor presentation)

Very obvious and visible difference is in type of customers & hence may be operating margins. They boast of enjoying 500 bsp edge over peers in operating margins (which they have been able to maintain). They also reported record highest margins in Q1FY24.

Kuantum is trading at highest PE 7x compared to market leader JK Paper

The entire sector is out of fancy now , I don’t think so these guys can outperform the sector. This company is puzzle to me as well, it never participated in the last paper rally. Promoters are very conservative in nature at the same time I don’t see their willingness to share wealth with share holders, they just announced very very nominal dividend. When companies in cyclical sectores are going through up cycles, good ones always reward share holders (JK paper did buy back, not like to like comparision but check Goldiam such a small company but always reward share holders).

Satia is cheaper now compared to kauntum… i have exited kautum and entered this… writing paper sector is out of favour as the maargins look peaked out…

they have annouced 1 Rs div compared to 20 pisa in last 2 years… so there is some positive development in that value sharing regard…they added capacity…in last 2 years… i am also puzzled by its underperformance…

I am not able to understand the deviance between industry dynamics and performance of Satia and West Coast Papers. As per industry reviews in links below, there is exptected downturn in industry and mill are being shut down. Any company operating in commodity business cannot outperform industry dynamics for long. But contrary Satia/ West Coast is improving sales/financial performance (?!)