Great results!

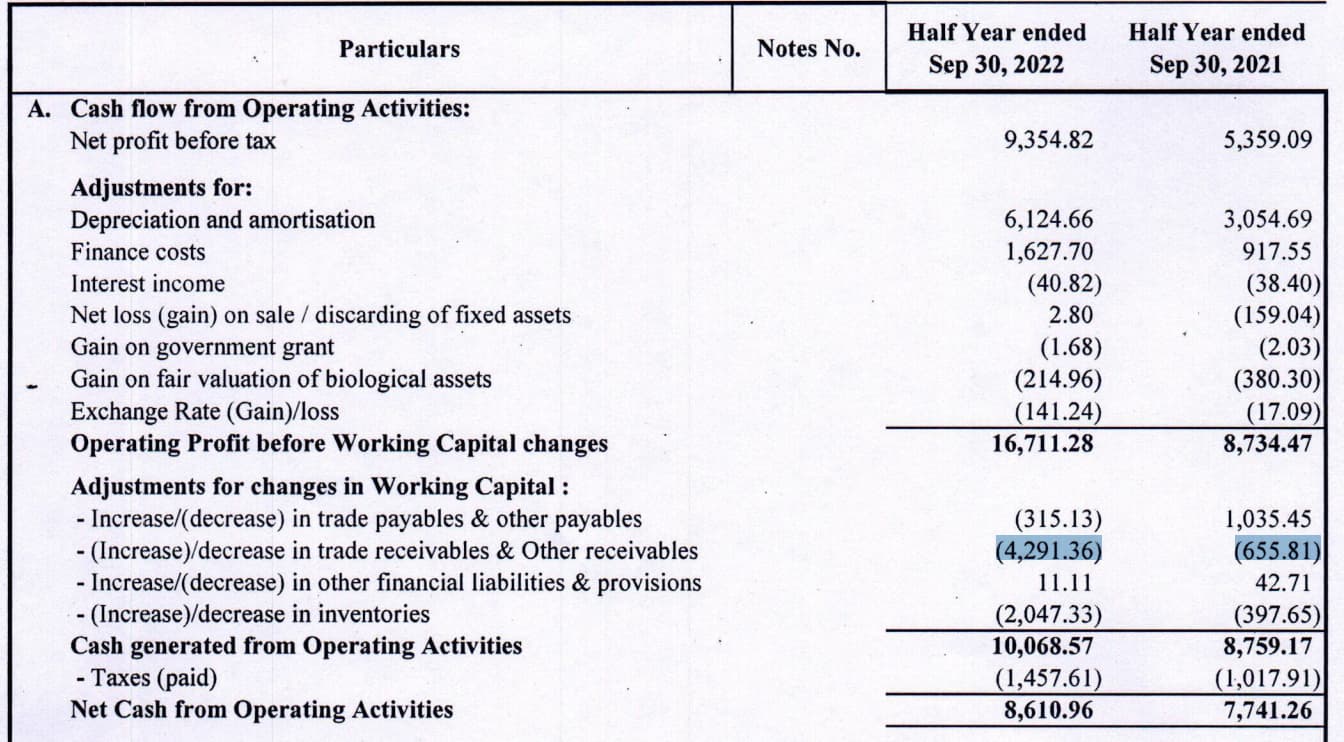

But the trade receiveable have gone up significantly in the first half…

2 Likes

Solid results…operating leverage looks to be playing out. I regrettably exited around 145 level in anticipation of another round of poor results (similar to last Q).

150 cr sales/month…Debtor days 44 days… Hence 43 Cr not seems to be a huge…

3 Likes

Super results… doubled sales and profits😊. What excited me more putting more capex into the business. WIP 137 crore.

2 Likes

Earing updates Q3

SATIA Q1 22-23 Earning updates.pdf (531.9 KB)

2 Likes

Satia Industries Ltd.

Why we like the stock?

-

Satia is one of the more efficient players in the paper industry, because of their backward integration.

-

They have 100% co-gen power facilities which lets them use electricity at cost of Rs 2-2.5 per unit against grid cost of Rs 7-8 per unit.

-

They have a caustic soda recovery plant. Paper is an industry which uses lots of caustic soda and it is very expensive at around Rs 50000 per ton. Satia has a plant that can recover 90% of the caustic soda they use in the manufacturing process. This is approximately 120-130 tons a day which comes to cost savings of about 60 lakhs a day, which means savings of 180 crores a year.

-

Satia is strategically located in Punjab which allows for easy availability of agro based raw material used to make paper. This helps them save on freight costs.

-

The agro based raw materials such as rice straw and rice husk which they use for generating power are usually burned by the farmers causing stubble burning pollution. Satia is transforming waste which would have caused pollution into something valuable. Because this is considered as green energy they earn REC certificates on this. These certificates can be traded on the energy exchanges and is an additional income for the company.

-

They have recently installed boilers in their plant which are able to use rice straw while most other players’ boilers use rice husk. For comparison, rice husk costs Rs 7000-8000 per ton, which while rice straw costs Rs 2000-4000 per ton. This allows for more cost savings

-

They have existing relationships with State Textbook corporations, and these corporations place bulk orders with Satia for paper. Because of this, we don’t see the volitility in their PAT numbers as compared to other paper players which mostly sell through the market. These relationships will be of further help to them, when the NEP is implemented and all new books have to be printed.

-

Even during peak covid period, when almost all other paper manufacturers were posting losses, they never posted a single quarter of loss. This points to an inherent strength in the business.

-

Usually in these types manufacturing companies such as paper, cement, steel, being the lowest cost and the most efficient producer is THE moat. And Satia, seems to have a deep one at that.

-

They are upgrading their wood pulping facilities from 150MT per day to 300MT per day. Once that is operational they’ll be able to make higher grade paper on their latest PM4 machine. This will lead to further margin expansion and higher profitability with operating leverage.

Risks:

- Low float

- Paper price volatility. This remains a risk even though they have proved they could remain profitable even during lockdown period which was probably the worst time for the paper industry ever, in recent decades

Disclosure: Invested from 90 levels.

19 Likes

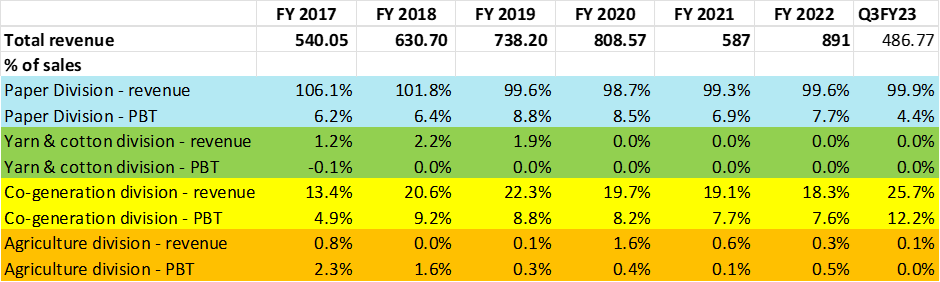

| Material Cost % | Satia Industries | 60% | 38% | 39% | 44% | 46% | 51% | 44% | 37% | 39% | 44% | 39% | 45% |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Yash Pakka | 30% | 40% | 41% | 32% | 41% | 51% | 53% | 26% | 28% | 25% | 21% | 22% |

Why there is gap in gross margin, being a BI company satia’s material cost must be at par with peer or better, any specific reason for that

1 Like

May be because of end product…Yash Pakka focus on low grammage MG industrial bleached and unbleached paper grades of between 30- 80 GSM and Specialised paper grades for rapping, packaging, interleaving for food and pharmaceutical industries, etc. Whereas Satia supplies 50% of its production to State textbook boards with the balance sold in the open market.

1 Like

When there is such huge demand for Wheat Straw, that is used as feedstock to fire the boilers why farmers burn it in the field ? Why can’t them bail up them and sell to paper industries ?

2 Likes

Overall good information covered,

Some points not covered/misinformed -

- Tie up with zume is ended and their machines being returned

- Ordered 6 new machines from indian manufacturer for cutlery segment

- Pulp mill not covered in detail

- Already started production on PM4

- PM4 efficiency will increase after pulp mill capex complete, as machine will operate with continuous pulp supply

11 Likes

Orders bagged worth 200 crores for Q423 …

e8d4ebeb-693e-4ca3-bca8-c760b1d67a41.pdf (449.7 KB)

5 Likes

Burning is easier and cheaper, costs next to nothing. And is also a source of potash - one of the three primary fertilizer.

3 Likes

To prevent over use of ground water, govt notifies official paddy plantation dates, this date depends on weather forecast of the monsoon rains, this is since stubble burning states are not ‘natural’ paddy planters. This date leaves very little time to clear and plant new crop, disturbing entire crop cycle. The rush means burning is fastest and preferred method.

Disc: studying

2 Likes

Results published…

Even though the results look good, the margins for the paper division is depressed… generation division saved the day…

1 Like

Seems like error in putting up segmental result. Might have punched paper in co-genration and vice versa

1 Like

Entire co-generation shown as inter segment revenue…

Paper division PBT is down -

possible reasons -

- It may be due to PM4 running on high cost waste paper because pulp capex is still pending.

- Paper realisation may have gone down, as all commodities are down.

Co-gen efficiency may be improved due to below,

update from company on 13-11-2021

Wood pulp digester automation is being done at a cost of ₹ 60 crores to optimize steam

consumption from present level of 1.6ton steam /ton of pulp to 0.6 ton steam/ton of pulp.

Based on the present cost of steam @ 2000/ton; it will lead to saving of minimum 300 ton steam costing ₹ 6 lacs /day and 22 cr/yr.

5 Likes

Any comments on satia’s Q4 numbers? EBITDA margins are at an all-time high but the depreciation has shit up 3x which Indo not understand.

1 Like