Well Satia"s performance is improving because of the following reasons:

A large portion of their production is contracted out to state education boards, here the effect of raw material price change is delayed. This was actually a negative when paper prices were increasing very fast. At that time Satia’s profits were lagging its peers. Buy now this is benefitting them.

Their utilisation of PM4 is continuously increasing leading to operating leverage benefits.

They have installed new pulp machines whose benefits didn’t fully materialise in the last quarter

Could someone kindly explain how NEP would benefit the company? I realise that the company is mostly functioning at full capacity, so will NEP simply help by raising paper prices?

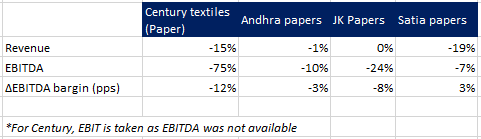

Company’s EBITDA declined by just 7% compared much higher fall in peer companies and the fall is mainly due to fall in revenue, let’s hear what management has to say on this on conference call.

Interestingly, while margins of all other company compressed, it actually increased for Satia.

Hello Fellow Investors, Can someone throw light on their Tax Rate. On the face of it they seems to be paying too little tax ( % wise).

Is there any justification which management shared OR someone has specific idea why this company is enjoying low tax rate?

Thanks!

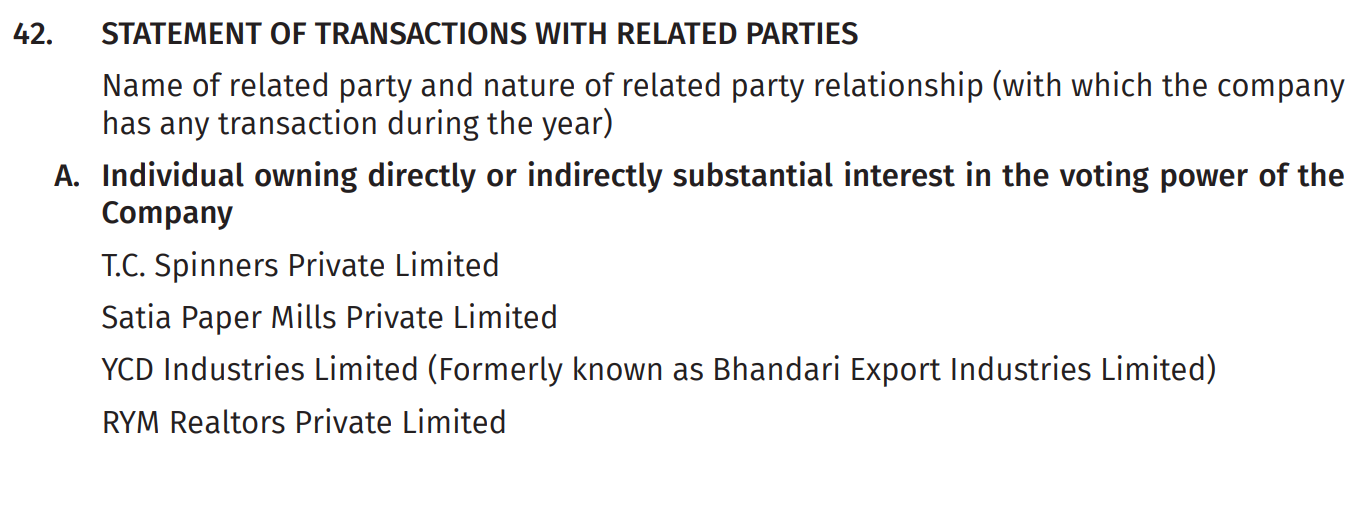

Does anyone know about the relationship between Satia Industries and Satia Paper Mills Private Limited?

From the name, it seems they do very similar business, which is a little concerning (Please correct me if I am wrong). We have seen many companies gather public funds and scale up. Once the public business is scaled up to an extent, they set up a Private business in direct competition with the Public one. The Date of Registration of Satia Industries on 26-Nov-1980 and Satia Paper Mills Private Limited on 10-Mar-2000 seems to follow this trend. (Source: Tofler)

I believe Satia Industries was called ‘Satia Paper Mills’ during incorporation. Effective 11/08/2008, roughly 8 years post incocporation of Satia Paper Mills Private Limited, the public limited company was renamed to ‘Satia Industries’. (Source: https://www.bseindia.com/downloads/ipo/20157318341IM%20PDF.pdf)

They both seem to have at least 1 common Director in Mr. Chirag Satia, who is a Promoter as well as the Executive Director of Satia Industries. (Source: Tofler)

Both companies are located in Muktsar, Punjab. (Source: Tofler)

In the Annual Report of Satia Industries, Satia Paper Mills Private Limited is listed under the header ‘Individual owning directly or indirectly substantial interest in the voting power of the Company’. But I do not see any other mention of this company elsewhere (Nothing in the Shareholding Section or Subsidiary Companies section). (Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/a424c661-edd5-4787-93fe-b084671643b6.pdf)

Other Legal information I could find in public domain about Satia Industries:

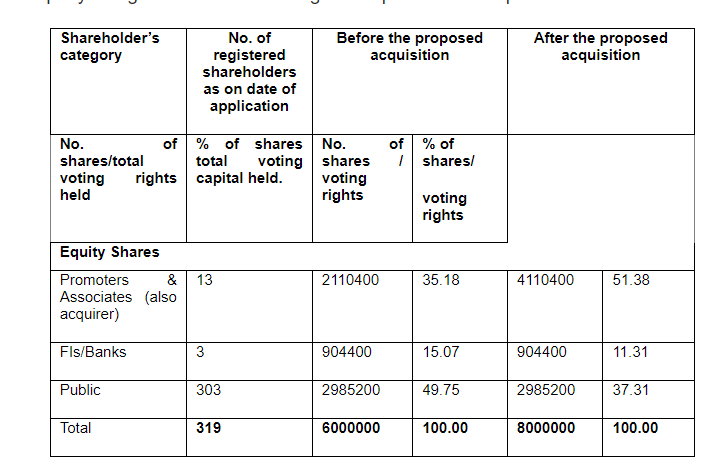

During 2005, the company was going apparently through some Debt trouble. Hence, a considerable equity induction of 22,50,000 Shares was done and the majority of it was Preferentially alloted to the Promoters at Rs. 10 per share, via which the Promoter(s) were able to up their stake in the company from 35.18% to 51.38% at the cost of equity stake dilution of FIIs, Banks and Public Shareholders (Details: https://www.sebi.gov.in/sebi_data/docfiles/15986_t.html). Presently, the Promoters put together hold 52.46% of the company as on Sep 2023)

Also back in 1997, the company made some preferential allotment of shares totalling 7,30,000 and was fined Rs. 1.5 lakhs for it by SEBI in 2009 (SEBI called it ‘unintentional non-compliance’). (Source: https://www.sebi.gov.in/sebi_data/attachdocs/1289367540098.pdf). Not sure why the fine came so late.

There was a petition filed against Satia Industries in 2019 by one Arihant Traders Private Limited. But it seems the petition was dropped in 2022 due to lack of legal representation from the Petitioner (Source: https://www.casemine.com/judgement/in/64a3ec7ccbd9ea05f1d80153).

I am trying to follow the company, and came up with all this information on my initial round of research. I would really appreciate some clarification from someone in the know or investors who have been following this company closely, especially concerning the Corporate Governance Standards of the company. Thank you.

Alternatively - if existing Shareholders are able to communicate with the Company Secretary - can you please ask them to clarify, especially:

Regarding the relationship between Satia Industries and Satia Paper Mills Private Limited.

Regarding the kind of business which Satia Paper Mills Private Limited is involved in (More relevant bit is whether they are in direct competition for any lines of products which Satia Industries produces or markets).

Paper imports are increasing at significant rate which is worrisome for paper companies. Paper manufacturing association has urged the government to keep paper and paperboard in the negative/ exclusion list, where there is no preferential treatment in terms of import tariff, while urgently reviewing existing FTAs (ASEAN, South Korea and Japan).

I think we have to wait more to emerge value in paper stocks so that margin of safety remains there. I think seshasayee paper has very good fundamentals interms of debt free status and almost 50% market cap cash is present in balance sheet. Waiting for price to come in 280-300 range for emerging substantial value in it.

Paper companies have increased the prices for writing and printing paper. The price hike of Rs 2-3 per kg is applicable from December 1. Further, by March 2024, the price will increase by another Rs 5-10 per kg.