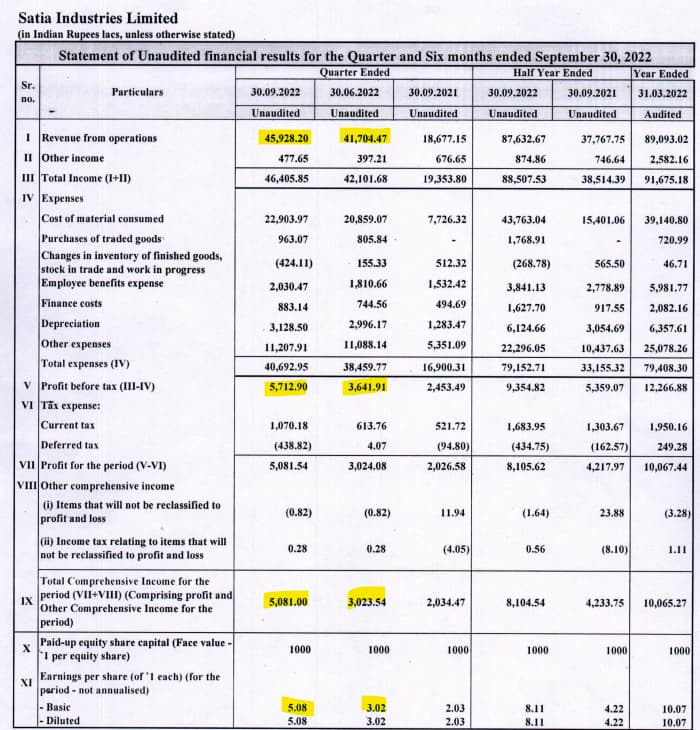

Exactly! For all the spiel around backward integration and captive power and proximity to raw material, the PAT margin disappointed me. I was expecting it to be ~10%.

Disc.: invested

Exactly! For all the spiel around backward integration and captive power and proximity to raw material, the PAT margin disappointed me. I was expecting it to be ~10%.

Disc.: invested

Results are not that bad according to me.

Eventually there new plant is operational. Their old plant was entirely backward integrated, with pulp capacity in hand. With new capacity, there are major fixed expenses to be borne by the company. This may decrease the margin. With utilization increasing operating leverage should be expected to kick in.

There is bit pressure on OPM level, which a eye raising point, however in coming quarter with increasing utilization margins should increase. While it will take time to have the integrated pulping facility for the new facility as well.

Eventually, depreciation expense has been increased 50% QoQ and 100% YoY. As utilization increases, gross margin improve (which might take a year or so considering the increasing spend on backward integration)

Other expense majorly include fuel expense, freight handling and packaging.

There is no update on the product approval from FSSAI, they said they are expecting in March quarter so far no update. And also Zume partnership looks like fizzled out.

On the paper everything looks good but when it comes to bottomline (PAT) or rewarding share holders (Dividend) not at par with JK.

There is no call this quarter ?

Company financial (Q1) looks good, order book sound too (recent NCERT order), however growth visibility is yet to be seen in investor PPT. Any info reg. comparative advantage wrt JK.

In paper sector, some stocks are hitting ATHs (those with good number) and those who have not delivered are taking a beating like Satia.

All the justification around increased depreciation etc need to be taken with a pinch of salt, as this was a cyclical upturn where numbers should have been stronger.

why would someone continue holding satia compared to a company like JK paper? - My thesis for the same was that Satia is 1/6th the size of JK - thus has a headroom for growth as well as the fact that Satia was getting into the cutlery segment in which the company had initially guided that EBITDA would be 40% ++. However now it seems that the cutlery business is on an idefinite hold and Satia is not able to maintain margins like JK.

Another thing to take into account is the boom in paper prices which is cyclical and currently, we are pretty much in the uptrend of the cycle. If Satia is not able to maintain margins right now - how will it do well when paper prices eventually come down

Even interms of valuation JK is cheaper than satia still.

Thank you @kalpesh4430 for introducing us to Satia and doing a lot of leg work. I bought around the 85-90 mark last year over a period of time. I was blown away by

When (3) above failed I started to question my thesis as this is a cyclical (whatever said, we should not confuse it with a more durable longer cycle business like HUL or Marico). I sold everything gradually between 110-120 after Q4 results. No holding now.

Any idea when they will hold the con call?

Still no news from the company regarding the con call. This is quite unusual as the company usually does com calls every quarter. Not sure how to read into this

@Investor1234 yes, this does look strange. Usually they are very proactive with setting up the investor call.

As far as I can see it , they do not do it every quarter .They do it twice a year or so …

Screener info is not correct – I have double checked that from BSE website. In CY 2021 – they did 4 concalls – notification for each was sent along with the results. Perhaps the management is busy with sth more important. I am pretty confident that they will do a concall.

I think screener scrapes some keyword like ‘Earning Call’ that’s why it didn’t scrape all four.

Disc.: invested

somewhere in q4 concall they were told they are in talk with US paper companies. US companies are planning to move some part of their requirements from china. Satia says orders from these vendors will be very big. However, they said the company will take a decision by July end. IS THIS MANAGEMENT BUSY? THEN I AM SUPER INTERESTED

Disc: Invested and positively biased for the next couple of years. However, the company’s stock return for last year was good compared to nifty and very disappointed compared to JK…

Summary of rating agency report that came out today

Thanks to @kalpesh4430

Let us not get excited about this, the opportunity size for Satia in the segment is very negligible; from the 700 ton capacity a day , the share of these molded product is max 2 tons a day ? And there is no further update on FSSAI approval (looks like they don’t see much of traction in this segment )

My 2 cents in this:

It’s very clear opportunity size for Satia is limited:

Satia doesn’t own the brand (unlike Yash Pakka), neither they have expertise/proven track record in brand building.

At the same time, jury is not out whether this Moulded cutlery business turn out to be commoditized business or branded business. If it gets developed as branded business, Yash Pakka will have first mover advantage.

FSSAI registration is not a show stopper Coming from food industry, can say with conviction that, FSSAI registration takes time, rejection rate is very low. Satia has mature leadership team to get through.

Disc. : Tracking, did scutlebutt as well. Convinced with management quality, not convinced yet with moats of the business & growth prospects.

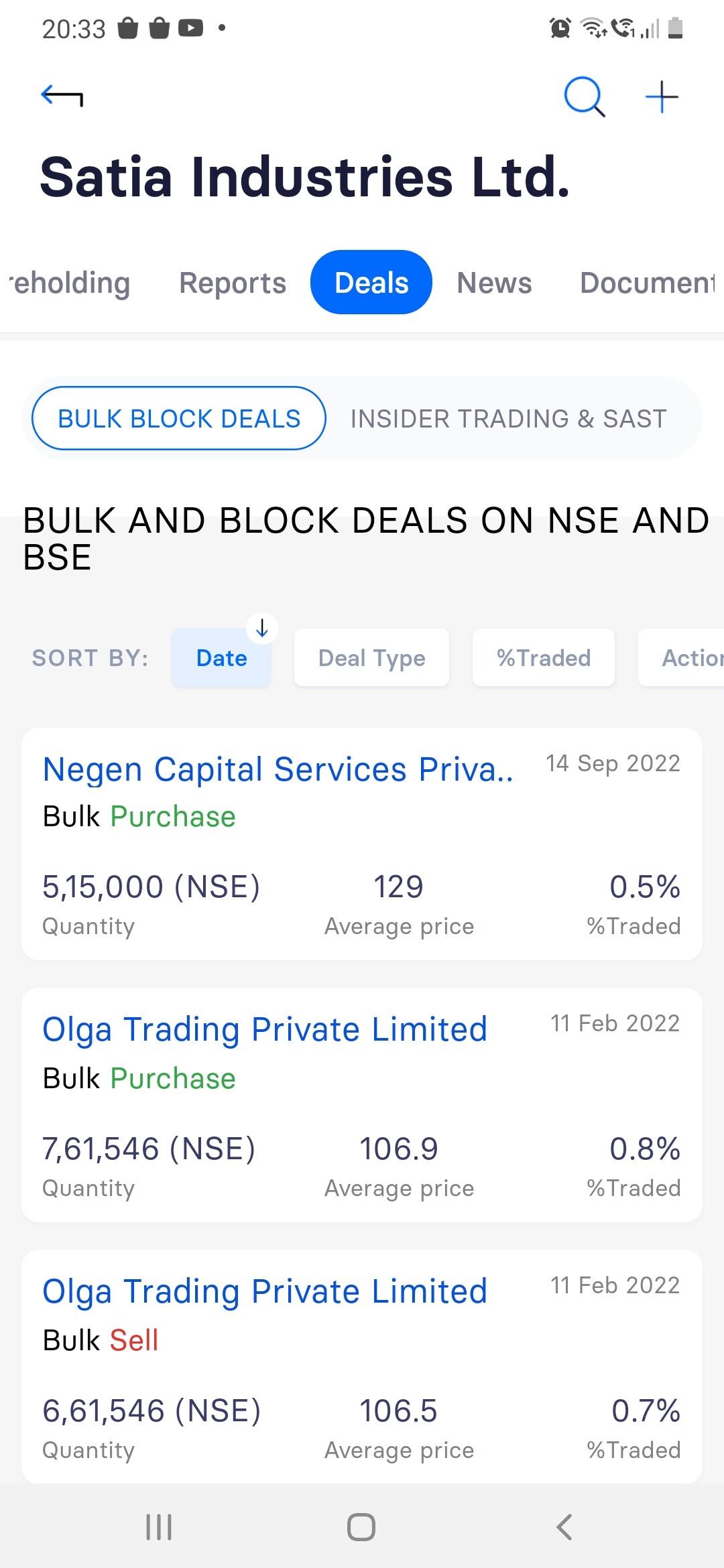

https://twitter.com/NeilBahal/status/1570039976183697408?t=kfxD5IDeCqfCQow51eE9ng&s=19

Negen Capital bought Satia today. The PMS is run by someone named Neil Bahal.

Disc.: invested

Neil bahal investment thesis about satia

1 stock idea - we haven’t had this for a while. So here goes…

Satia Industries: (Mcap 1335cr, CMP 133/share).

In short, Satia is not a Special Situation as such. It comes under the value investing category where significant Capex has just taken place and if ramp up happens as per plan, stock is available at 6.6x P/E, which is a considerable discount to historical multiples this company has got of approx 10x P/E.

(It has even seen 12-14x P/E at times in the past, but we should always conservatively take target multiples).

What I like here?

I really like that its big capex has finished already and now the ramp up should happen in the remainder of FY23. Hence, the risk is lesser in this case.

It is always a risk to buy a business when a ‘significant’ capex is just announced.

~~~

Also**, Satia is a backward integrated player which makes it a safer proposition compared to many of the listed peers who are at the mercy of ‘imports’ of raw material.**

Relying on imports can make margins unpredictable.

Hence, an integrated player like Satia offers some comfort.

~~~

In our estimates (extrapolating from official management guidance),

FY23 revenue could be 1500cr with 300cr EBITDA.

In FY24, EBITDA could increase to 400cr.

This translates into PAT in FY24 between 190-200cr.

And based on current mcap of 1335cr, stock is currently available at 6.67x P/E on FY24e.

Ps- Satia Industries is one of the rare companies which remained profitable even during the Covid pandemic which indicates a strong business and able management.

**~~~**

*Disclaimer: Negen Capital PMS owns Satia Industries. This post is our research note on Satia Ind and not investment advice. We can sell our positions at any time. We have not been paid by anyone to write this newsletter. Kindly consult your financial advisor before acting on the contents of this newsletter. The estimates mentioned could go wrong. The views could be biased.*