SIL is shifting its focus on short term on its current expansion. While expansion in cutlery segment will take time.

From concall, it seems that cutlery segment will only be fueled until govt impose ban on Single Use Plastic. While Zume partnership with SIL is in turbulence, as Zume has started its own production at slower space. For this SIL is looking tieng-up with other players in outside India.

Hence cutlery segment will take time in SIL probably post FY23 it will contribute significant portion. Next 2 years I expected SIL to look like

FY23: Increasing Paper utilization (60-80% utilization for new unit)

FY24: Optimum Utilization & increase in realization (by spent in backward integration); Cutlery segment to drive growth for FY25.

After going through the latest concall it seems like the management enthusiasm around cutlery/Zume tie-up has fizzled out. If they are not able to crack something big with Zume (which seems to be the case) and with so many young startups coming into the paper packaging industry don’t think this story will pan out as intially anticipated.

If not, we are just looking at a fully commoditized play in the middle of a mid-term upcycle. And to play the paper cycle it is much better to look at bigger players with better economies of scale, distribution networks and much deeper pockets. The potential upside here seems very low.

Paper cutlery was talked about with 40% EBITDA in last 2-3 conf calls, with aggressive expansion planned after learning operations from initial 2 machines. Real disappointment that management is hiding behind govt regulations (if govt is going to enforce strictly single-use plastic ban).

Mgmt also has said that the cost of these paper cutlery has (mysteriously) come down recently affecting projected profit margins.

Smaller scale suppliers with semi-automated machines are selling paper cutlery at lower prices, and hence Satia may not be able to proceed on this with such margins (20-25%) though these margins are equivalent or more than their current paper margins. I was thinking that with their backward integration and power plant Satia is uniquely positioned to be a lowest cut paper cutlery maker.

Even the paper capacity post-expansion will be at ~60% utilization this fiscal (FY23) and any more revenue/EPS growth is capped at utilizing the remaining capacity. Mgmt is NOT gung-ho about any additional paper capacity addition. Their debt/financial position to my understanding won’t support additional capacity expense for another 2-3 years atleast.

With (4) above any revenue/EPS growth is based on assuming paper prices stay at today’s elevated levels for the next FY too.

This sudden change in narrative has made it necessary to take a real hard look at mgmt’s other projections too.

It is now pretty clear Zume opportunity is just change of product mix and will not be driving revenues in a meaningful way during this FY at least

If you take the lower band of the FY23 revenue guidance then quarterly run rate should be 350 crores, this the key monitorable, to achieve this they should be selling 50,000 ton a quarter.

Any more clarity on the Zume orders or a new customer that they are referring from US or Regulatory approval for this packaging product will give more visibility to the top line

Their captive power plant is saving their bottom-line along with REC credits and 500+ acres eucalyptus plantation revenue as well.

India is a net importer of paper so I don’t see any issues on the demand side. We all continue to use ecommerce portals for our day to day needs Amazon, Nyka, Swiggy, Zomato, Paper Text Books Paper based Exams etc… We are not going to give up paper usage. There is paper everywhere in our daily life.

Let us track the story on quarterly basis and see how their capacity utilization on the newly installed machines. One encouraging thing is with these new machines their wastage in the production process is almost zero.

My problem with their Backward integrations is that although it increases their margins the RoCEs are almost the same as the industry. Instead of making ₹15 on ₹100 investment they are making ₹30 on ₹200. So although it reduces the risk of external dependencies it doesn’t make them a better business.

Absolutely agreed. I don’t forsee any growth triggers until FY25 atleast. And revenue seems capped at ₹1450cr even at full capacity utilisation if the paper realisations come back to their steady state ₹60-65k per ton levels.

Absolutely agreed with these. But historically in most of paper company all the backward integration support kicks in post 2-3 year of expansion.

Actually most of the paper companies have expanded at the same pace. They carry on debt for expansion and focus on repayment of plant for next 3-4 years. Eventually every company has to keep in mind that the industry growth is in mid single digit. Any aggressive expansion in Paper Industry can kill the company is the cycle turns. (Situation of NR Agarwal in 2013-14)

This can be true. However if company suffice its PM4 till FY24 in efficient manner, than I think its still better. As mgmt is claiming for asset turn of 1.8 till FY24. Now none of the industry player has such high asset turn. If I expect they place the asset turn at 1.5, even that is great, because with capped topline, they can expand much on their bottom-line by expanding heavily in bottom line.

While SIL has more investment on backward integration, which may turn in upward Profit Margin in comparison to industry level.

However all these theories solely depend on management action, which may result in coming quarters.

“The infrastructure for producing both biodegradable plastic straws and paper straws at scale is non-existent in India today,” said Shahrukh Khan, executive director (operations) at Dabur India Ltd., which sells Real fruit juice packs priced at Rs 10. “We would be able to cover only 10-15% of our requirement with the imported paper straws as there is a huge global demand-supply gap.”

The country currently has zero capacity to produce compostable and recyclable plastic straws, according to Praveen Aggarwal, chief executive officer at Action Alliance for Recycling Beverage Cartons, which represents beverage makers including Dabur, Parle and PepsiCo. Lack of commercially viable alternatives could lead to losses worth Rs 3,000 crore in sales for the industry, he said.

“But work is under progress to introduce bio-compostable polylactic acid or PLA straws,” Aggarwal said over the phone. “Orders for machines to manufacture such straws locally have been placed, but the production would begin at the end of this year.”

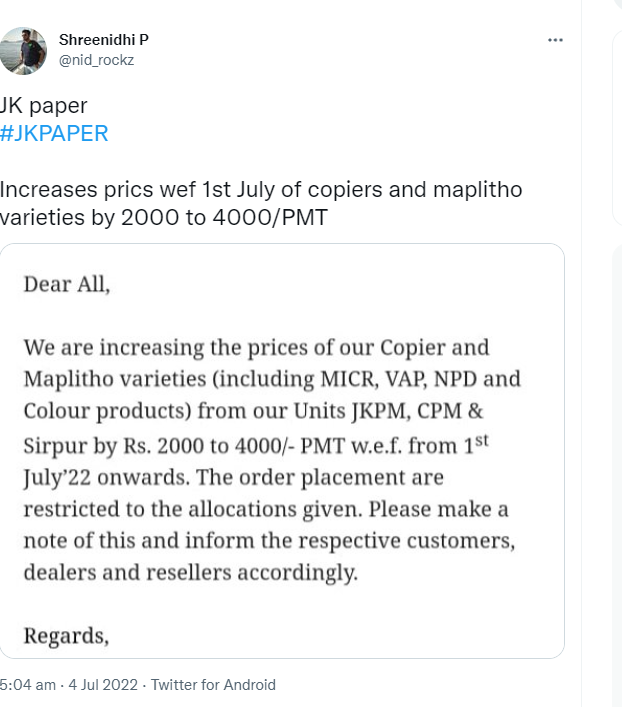

@Rafi_Syed the realization works out to be about 95K per ton which is much above the kind of #s they talked in the last concall. Any comments in that? Have there been additional price hikes recently?

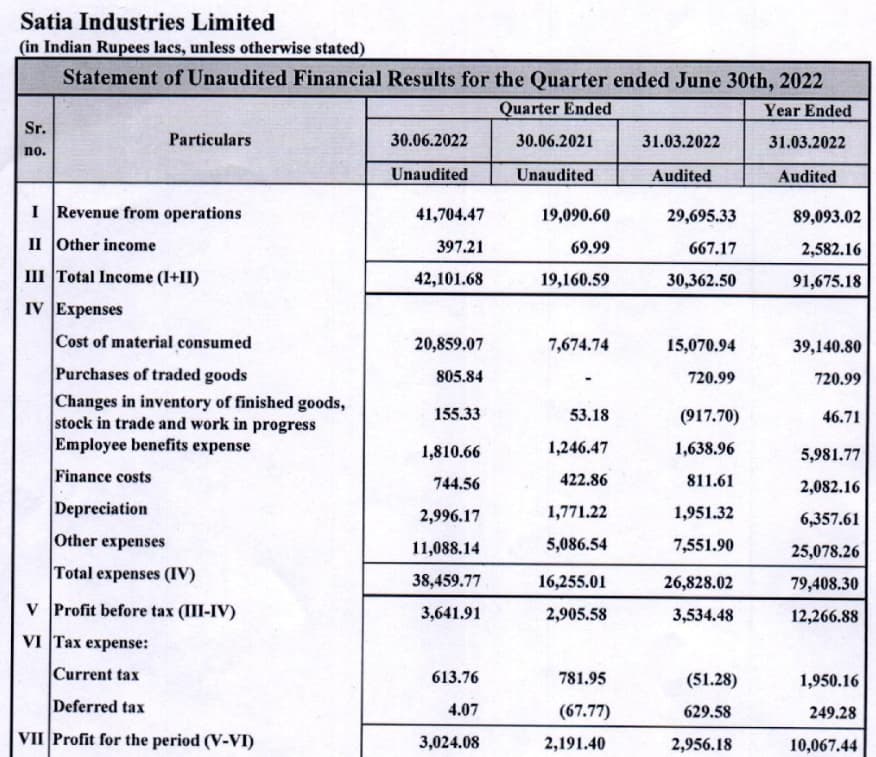

Excellent Top line growth

2)As expected margins have taken a hit -hopefully the price increase have happened in qtr2 (time lag against RM price increase )which will reflect in bottom-line going forward

There is 10 crores of extra depreciation that optically reduces the PAT . If they had depreciated same amount as the last quarter,the PAT mrgin would be around 9.8% instead of 7.5%. Its good practice to depreciate assets quickly to reduce tax outgo .

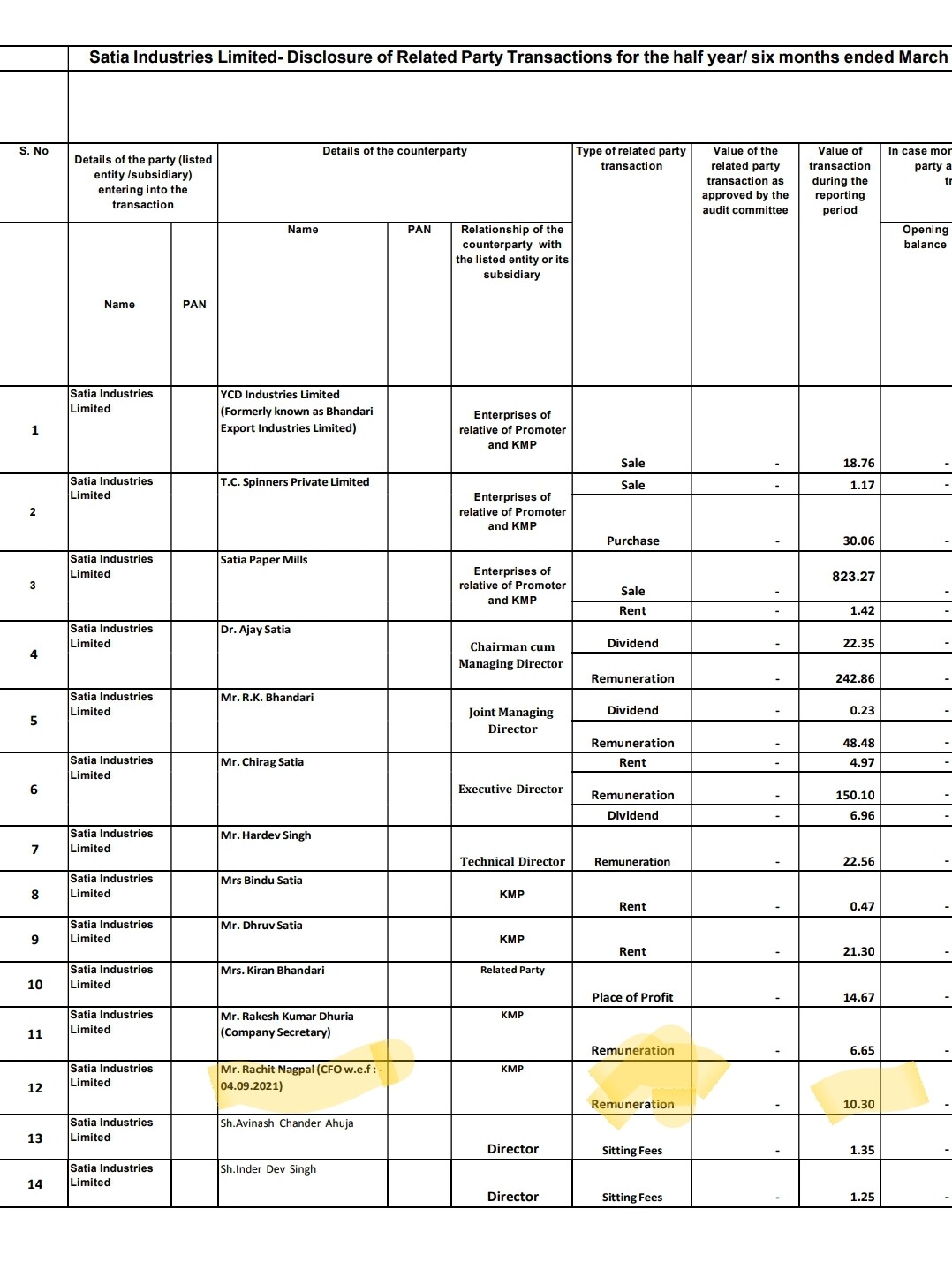

JK and Satia are not exactly comparable as Satia sells papers mostly to state boards and the contracts run for a year. So higher sales may take some quarters to percolate to bottom line . @kalpesh4430 Do you know what’s included in the “Other Expenses” ? That too has a 10 crore extra that’s not proportionate with the increase in sales .