Please share the document this is taken from

Sasta Sundar Venture Limited

The company operates in two segments:

- B2C platform – sells medicines directly to consumers.

-

Margins are significantly higher in generics (up to 40%, typically ~30%), while in branded products margins are lower (15–20%).

-

However, at the EBITDA level, margins shrink sharply due to stiff competition from deep-pocketed players such as 1mg (Tata), Netmeds (Reliance), and PharmEasy. Discounts and logistics costs eat away a large part of profitability.

- B2B (Retail Shakti) – works as a distributor to pharma shops.

-

Margins are lower: 8–12% in branded products and 10–20% in generics.

-

Branded sales dominate, since pharmacies perceive them as higher quality, making it difficult to realise generic margins.

-

Competition is less intense than in B2C but still stiff, with players such as MedPlus Online, Netmeds Retail, regional distributors, and large multi-vertical platforms like Udaan, ShopX, IndustryBuying, Power2SME, Moglix, and Amazon Business. These compete on scale, logistics, and assortment.

-

At the EBITDA level, margins should be around 5%. The model is working-capital intensive because inventory needs to be maintained for timely delivery, and credit must be extended to pharmacies, which they already get from local distributors.

-

Management targets 5% blended EBITDA margins by FY30, most of which will likely come from B2B.

Why Focus on B2B

My focus is on the B2B segment because:

-

It already contributes more to current revenue.

-

The B2C business is unlikely to grow meaningfully given the intense competition. Flipkart’s exit is a telling sign — in this space, nobody is going to make money anytime soon.

In FY25, the B2B segment doubled its revenue and improved working capital — an encouraging sign in a segment usually very WC-heavy. But this growth may have come through discounts to pharmacies, as Sasta Sundar earns ~6.5% gross margins versus Entero Healthcare’s ~9.5%. The difference may also be scale-related. Notably, Entero’s growth has been driven by expanding working capital (large trade receivables), while Sasta Sundar seems to be incentivizing with discounts rather than credit.

Currently, the business lacks a strong competitive advantage. Scale could eventually provide one by lowering procurement costs and improving warehouse efficiency, but achieving this won’t be easy in such a competitive landscape.

Management

-

Banwari Lal Mittal appears to be an honest and high-integrity leader.

-

Evidence: he has not taken remuneration since FY23, and I couldn’t find aggressive ESOP or share warrant issuances in his favour.

Overall View

The mortality rate in B2C is very high. B2B is more stable but operates with thinner margins and meaningful competition. At present, investing here would mainly be a bet on management and confidence in their execution.

At the current market cap of ₹863 crore, my calculations imply the company would need to grow revenue at a 31% CAGR and reach 11% EBIT margins. That’s ambitious, since ~11% is what players typically achieve at the gross margin level in B2B.

1 Like

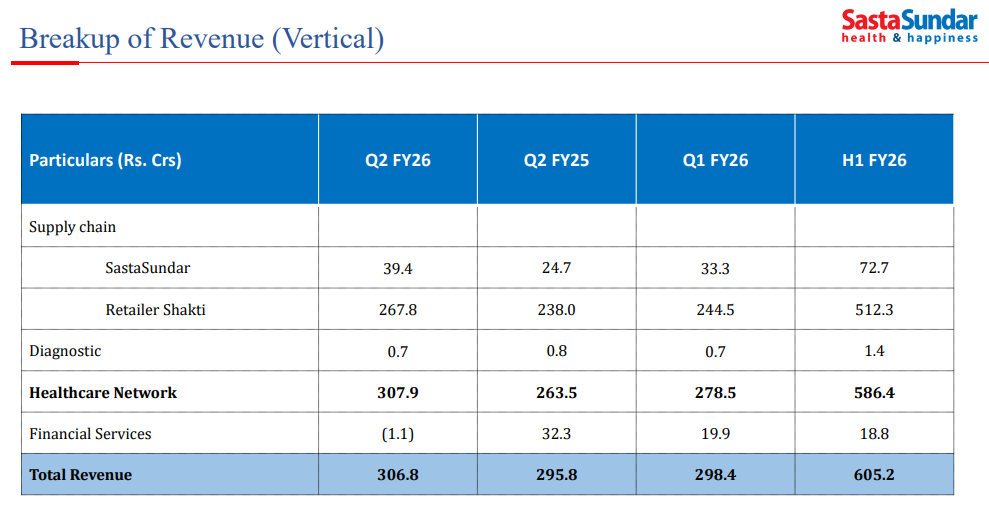

The results for Q2-FY26 have come. Although the revenue increased 16.9% YoY and 10.6% QoQ, the net profit is still in loss due to to much higher increase in employee benefit expenses. The company operates in two business segments, SastaSudar (B2C) and Retailer Shakti (B2B). The split-up in shown in following figure as per latest investor ppt of Q2-FY26.

The promoter Mr. Banwari Lal Mittal has bought the total of 90000 shares from the open market on each day of the last week (17 Nov to 21 Nov). This has increased the shareholding from 33.43% to 33.6%.

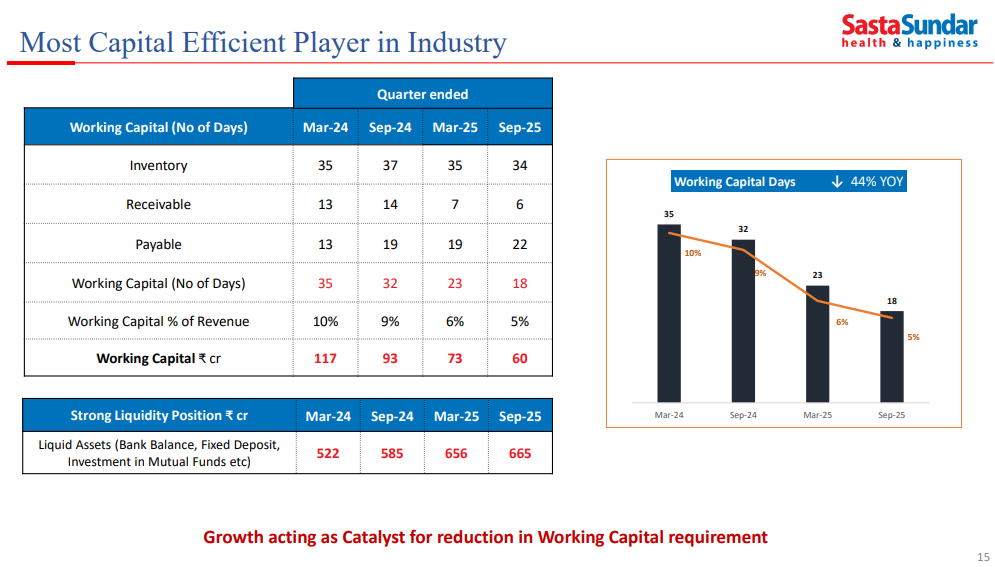

Another metric the company has shared is the working capital days, which is continuously decreasing from March 2024 onwards, as shown below. The major metric which is contributing for this reduction (apart from Payable) is the receivable days which has reduce from 13 days in March 2024 to 6 days in Sep-25.

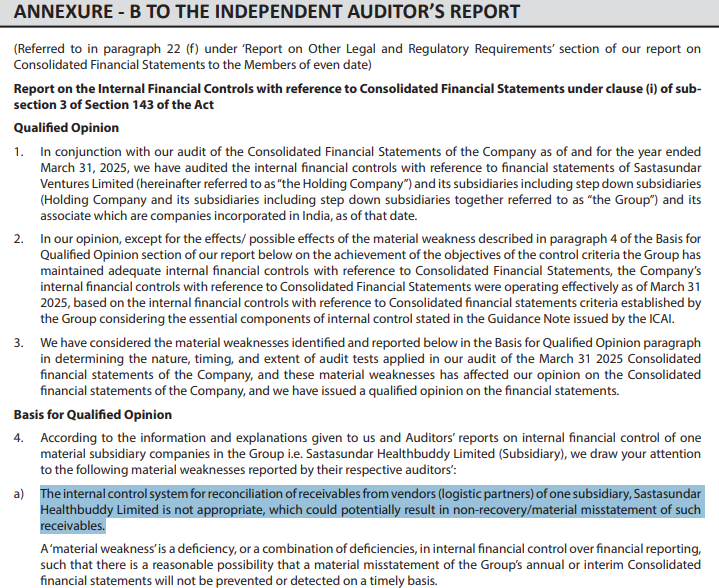

However, by going through the FY-2025 annual report, in Page-128, the independent auditor has mentioned that the internal control system for reconciliation of receivables from vendors is not appropriate in one of the subsidiary Sastasundar Healthbuddy Limited (Retailer Shakti B2B segment), as shown below. This can result in material mis-statement in such receivables.

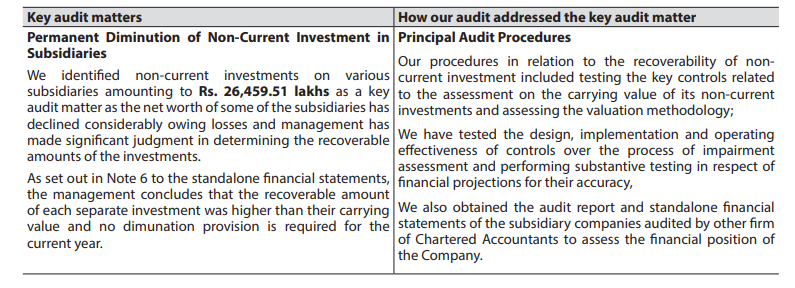

Another key audit-matter flagged by the independent auditor (Page-72 of AR FY-2025) is about the non-current investment of Rs. 264Cr in various subsidiaries in standalone Balance Sheet. The net worth of some of the subsidiaries has declined considerably owing to losses and management has made significant judgement in determining the recoverable amounts of the investments.

Request the experienced members of this forum to kindly give comments and how to look into it. Whether this can be considered as corporate governance issue or is this how business operate in other companies too?