0c348d6e-0799-4dd9-9899-a885eecab255.pdf (2.0 MB)

300 cr in sastasundar marketplace pan india expansion

700cr in sshb my guess is dividend or buyback. Listed entity might see reward of 500cr or so…

0c348d6e-0799-4dd9-9899-a885eecab255.pdf (2.0 MB)

300 cr in sastasundar marketplace pan india expansion

700cr in sshb my guess is dividend or buyback. Listed entity might see reward of 500cr or so…

Amazed to see that Sastasudar was able to unlock significant value from its subsidiary.

few observations.

On Dividend:

SML hardly has 40cr networth, considering 20% long term capital gains (inclusive of acculumated losses & indexation) tax outgo on 690cr worth stock should be close to 100cr for SSHBL. If the management decides to funnel that money back to SSVL, then there will be taxes on the dividend- this should put the new cash to listed entity after adjusting for mitshibushi stake & 25% tax is at (690-100)(75%)(75%) ~ 330Cr. i.e 20% of current market cap.

That said, i think money will be retained within SSHBL for the working capital purposes ( in anticipation of massive growth)

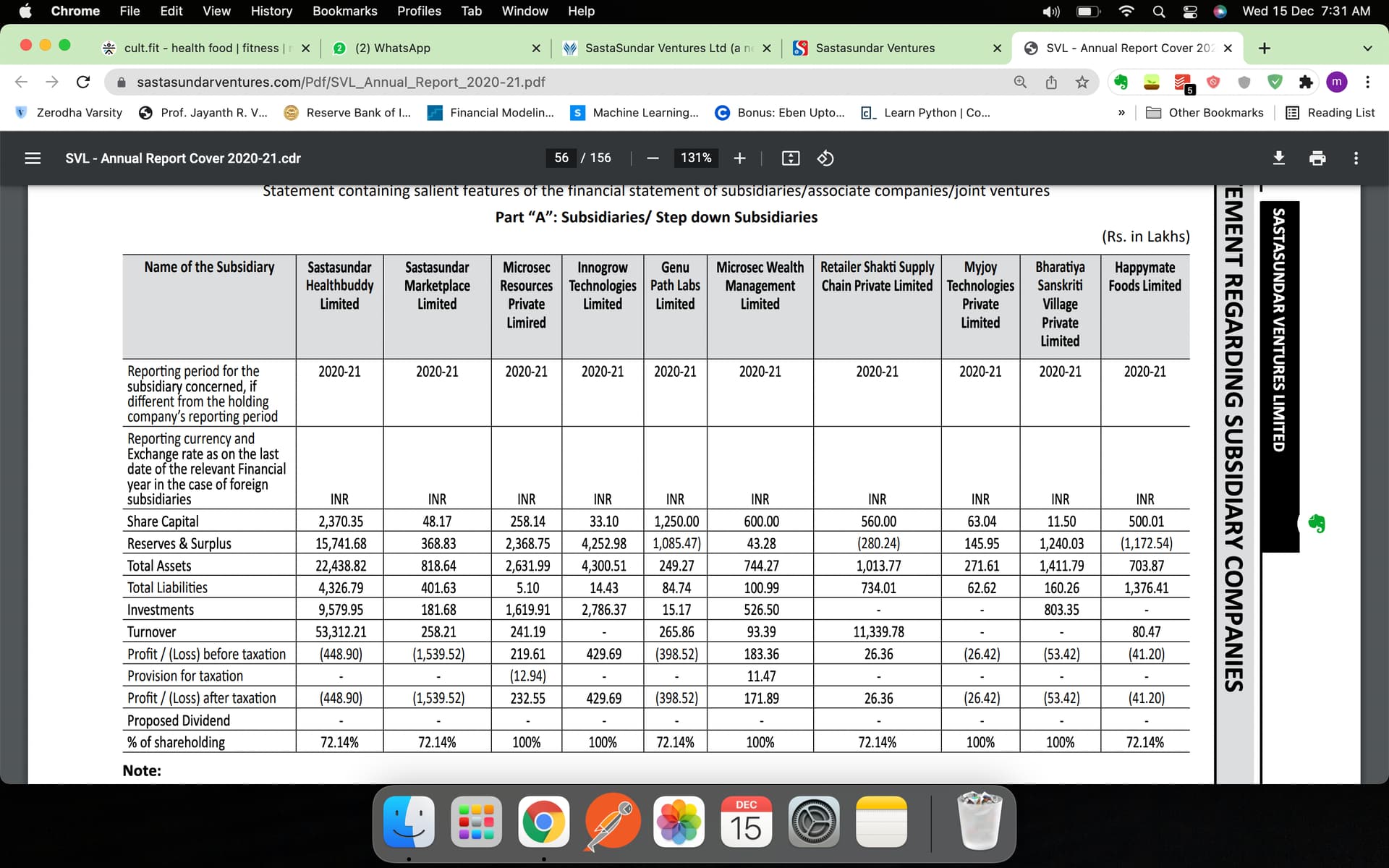

Subsidiary financials:

Company Narrative:

The most important aspect of the arrangement is- Sastasundar’s story has changed from being a B2C E-pharma player to a B2B Pharma supply chain & Distribution player with a very very strong strategic partner(FK).

– Problem with this narrative is

This brings us to the point on how to value such B2B pharma supply chain business- Views invited.

There are more tax efficient ways to do the dividend. For example, they can merge SSHB with SSV They have also indicated about this corporate structure simplification in the slide deck.

Nonetheless, huge value unlock for shareholders. I think it’ll be super weird if they retain 700odd cr in a business which does almost no turnover. I am expecting a significant buyback or dividend after retailing capital for Genu?RS expansion.

Disc: INvested, biased

If you buy Sasta Sundar Venture you have only 72% X 24.9% stake in the part you are interested in, which is a piddly = 17.9% sake in sastasundar.com. Dont see the point in this unless you can explain.

Please correct me if I am mistaken

Worst case if online sales of meds is stopped by government, will this impact business of Ratailer Shakti ? Is retailer buying from them bcos they get to fulfill online orders of Flipkart+ ? or this business has independent merits over other wholesellers ? If anyone has studied this , pls share. thank you

Some key observations since the Flipkart Deal and why I feel the company deserves to be looked at again now:

Revenue for FY 23 : 1036 Cr up 67% YOY with latest Quarters showing much higher % growth YOY and QOQ. Company is on a run rate of 1200 Cr+ FY 24 without opening any new Warehouses.

Company has a total plan of building 20 Warehouses and has opened 7(4 last FY).

Since the B2C biz is now an Associate Company the GMs and the EBITDA margins are in much better shape although EBITDA is still negative. Wholesale biz are a function of Volumes and Operating leverage would play out with more Warehouses and lower discounts(more on this later).

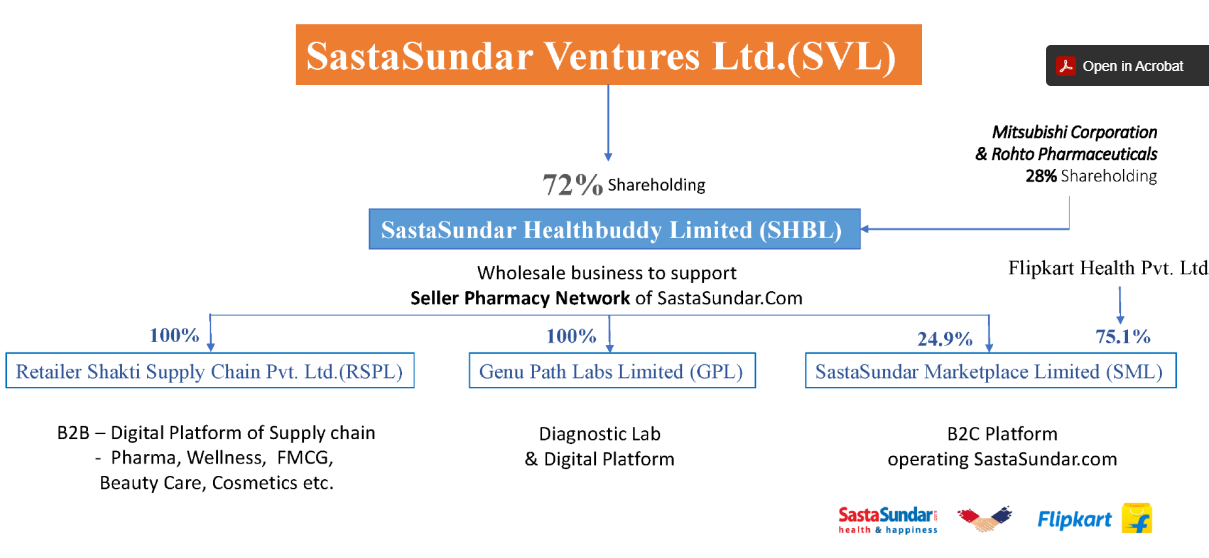

Flipkart Health+:

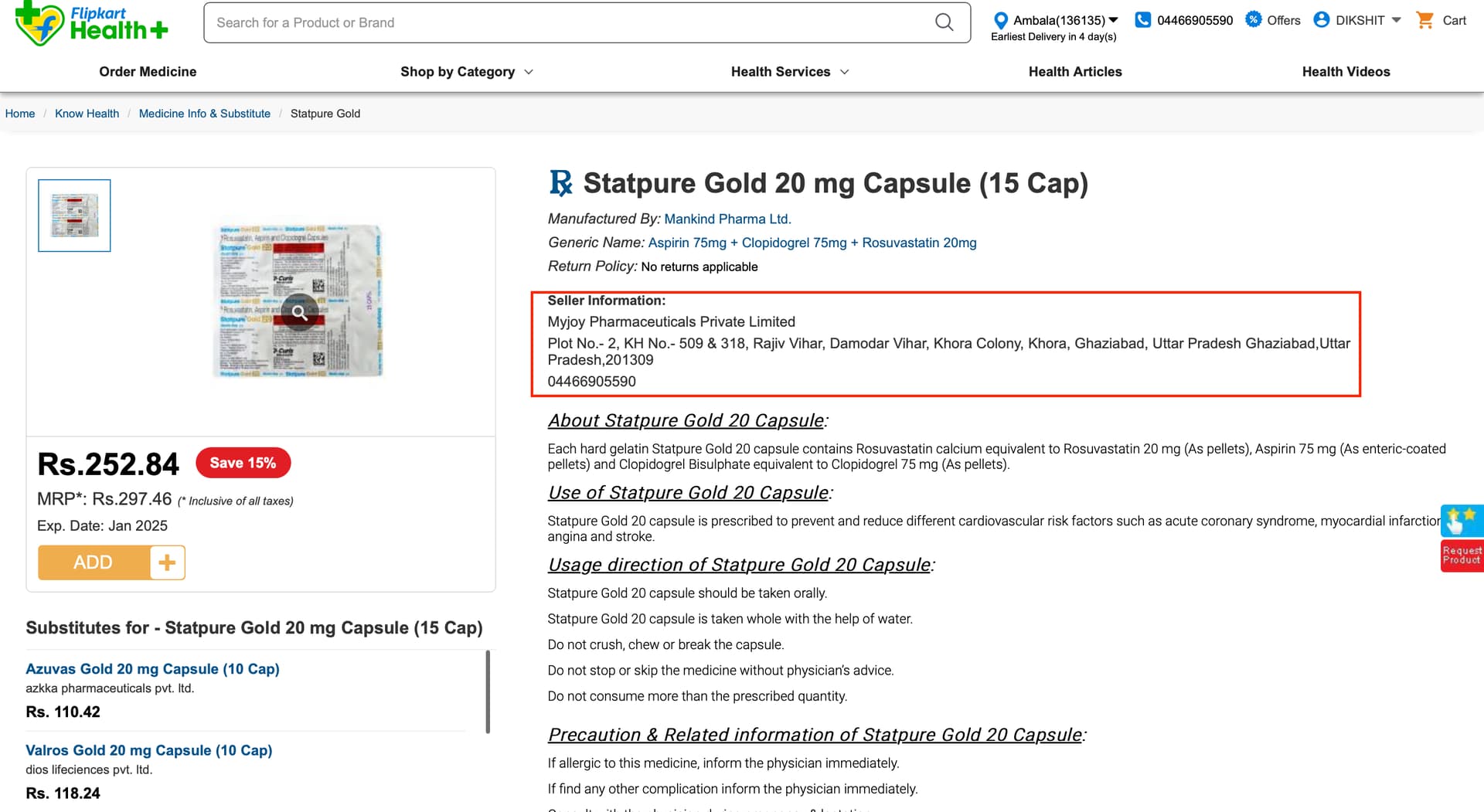

The Company has a double growth engine since the Flipkart deal in my opinion. For most medicines being sold on Health+ platform Myjoy Pharmaceuticals is the Seller which is a Subsidiary of SVL.

The Wholesale platform(Retailer Shakti) buys medicines in Bulk directly from Pharma Companies and then further sells the medicines on B2C platform via Myjoy thus pocketing the margins at both levels and enjoying the growth, fulfilment, reach & customer trust capabilities of the Flipkart brand ex the Platform Cost that Flipkart would be charging them. This could be a big enabler in their 97% YOY growth in Q4 FY23 other than the growth from the B2B retailer platform. Labs biz is most likely not this huge for them.

Yet to verify this with complete certainty as financials for the subsidiaries for FY23 aren’t updated on the website yet.

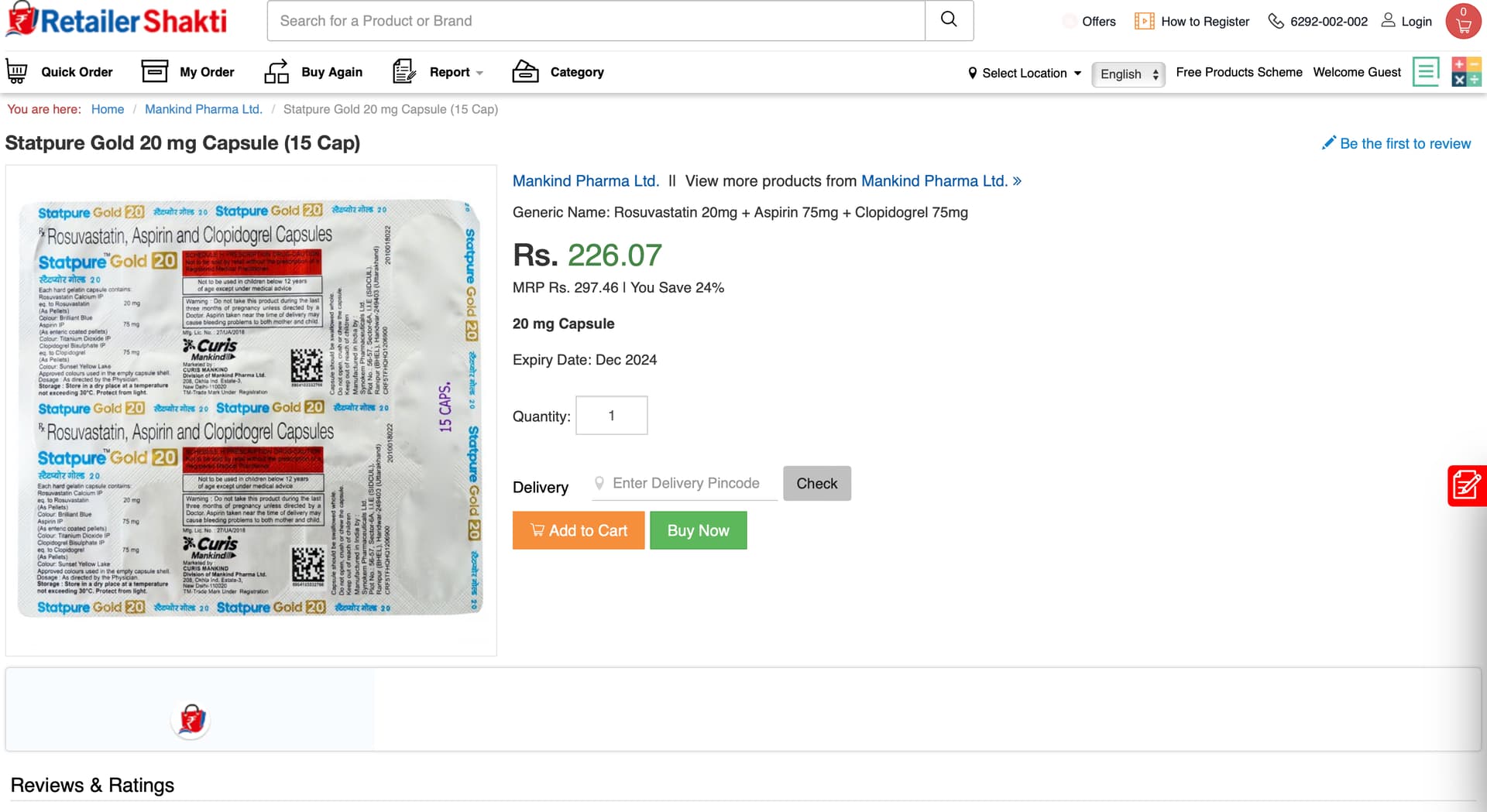

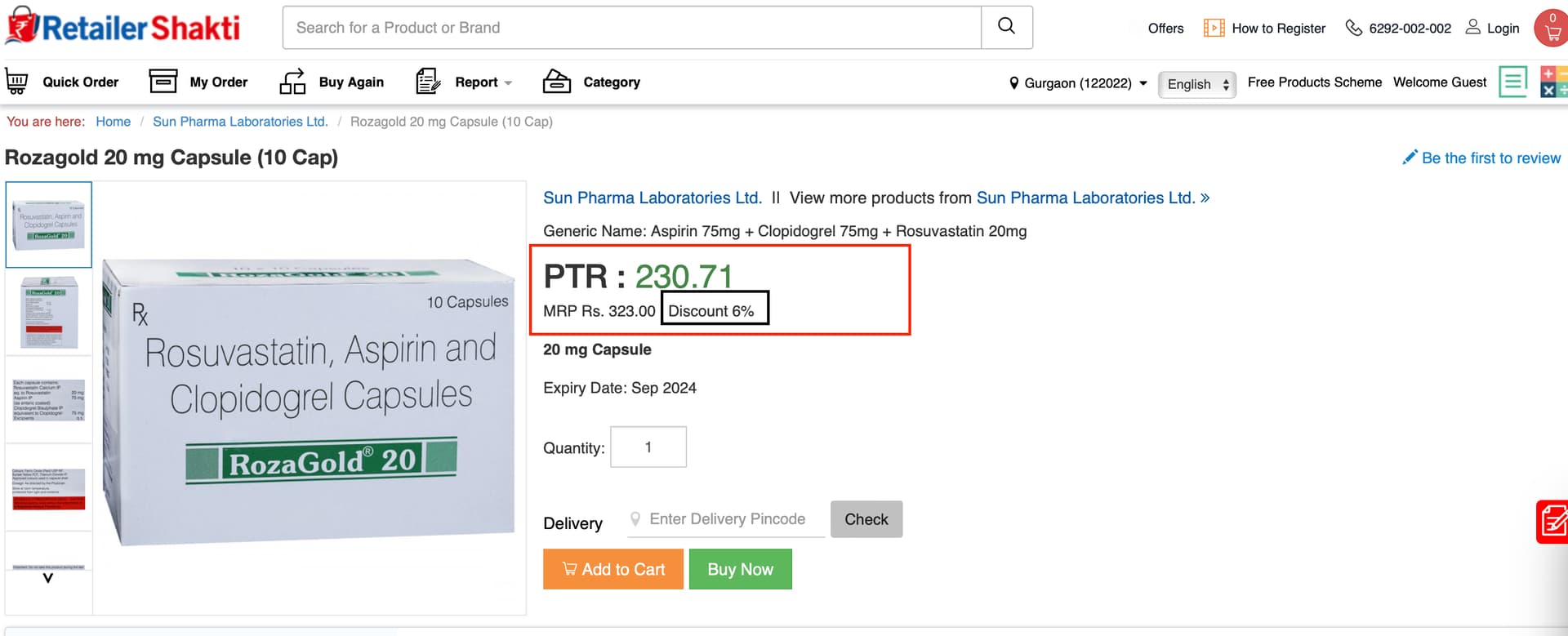

The price for the same medicine on the Wholesale platform is attached below and the margin difference for Myjoy comes to around ~ 11.5% ex Platform fees of Flipkart. This is also ex the margin of their Wholesale biz. For FY22 their Wholesale Biz did 4% GM, impact of any Operating leverage playing out has to be seen for FY 23. Myjoy had no sales in FY22.

Retailer Shakti B2B Retailer:

A simple google research reveals no large Competitor in the B2B Medicine space and seems like the initial mover will have the biggest market share since the entire country is up for taking. Sastasundar is already the biggest Pharma distributor in West Bengal with a 7% market share. They’re yet to open 13 more Warehouses in India.

The mobile web UI for Health+ is also much cleaner now than before and most likely Flipkart will revamp the Desktop web in sometime as well.

SEO is a key area where the Health+ platform lags with most search results from Health+ on Page 2 of Google search. The reason I’m highlighting Health+ isn’t from a 25% stake view point but from the Customer growth leading to growth in the Wholesale Procurement business and the combined leverage thereof including the growth in the Retailer B2B business.

Company still has a comfortable Cash position of ~ 700 Cr including Minority share which is going to be reverse merged soon and will simplify the Corporate structure.

At a P/BV ~ 1 pre/post proposed restructuring and a cash position of 0.6 BV including a 25% stake in Flipkart Health+ demands a relook given the huge market opportunity but comes with a big regulatory risk.

Yet to do a thorough valuation, will post once done.

Risks:

Pending Government regulation on e-sale of drugs - India's latest draft bill proposes strict curbs on online sale of drugs, dealing a major blow to e-pharmacies

The nature of their agreement with the B2C platform is still unclear. Flipkart onboarding multiple vendors is also a risk. I’ve asked the Investor relations for more clarity on their relationship with Flipkart and any exclusive agreements.

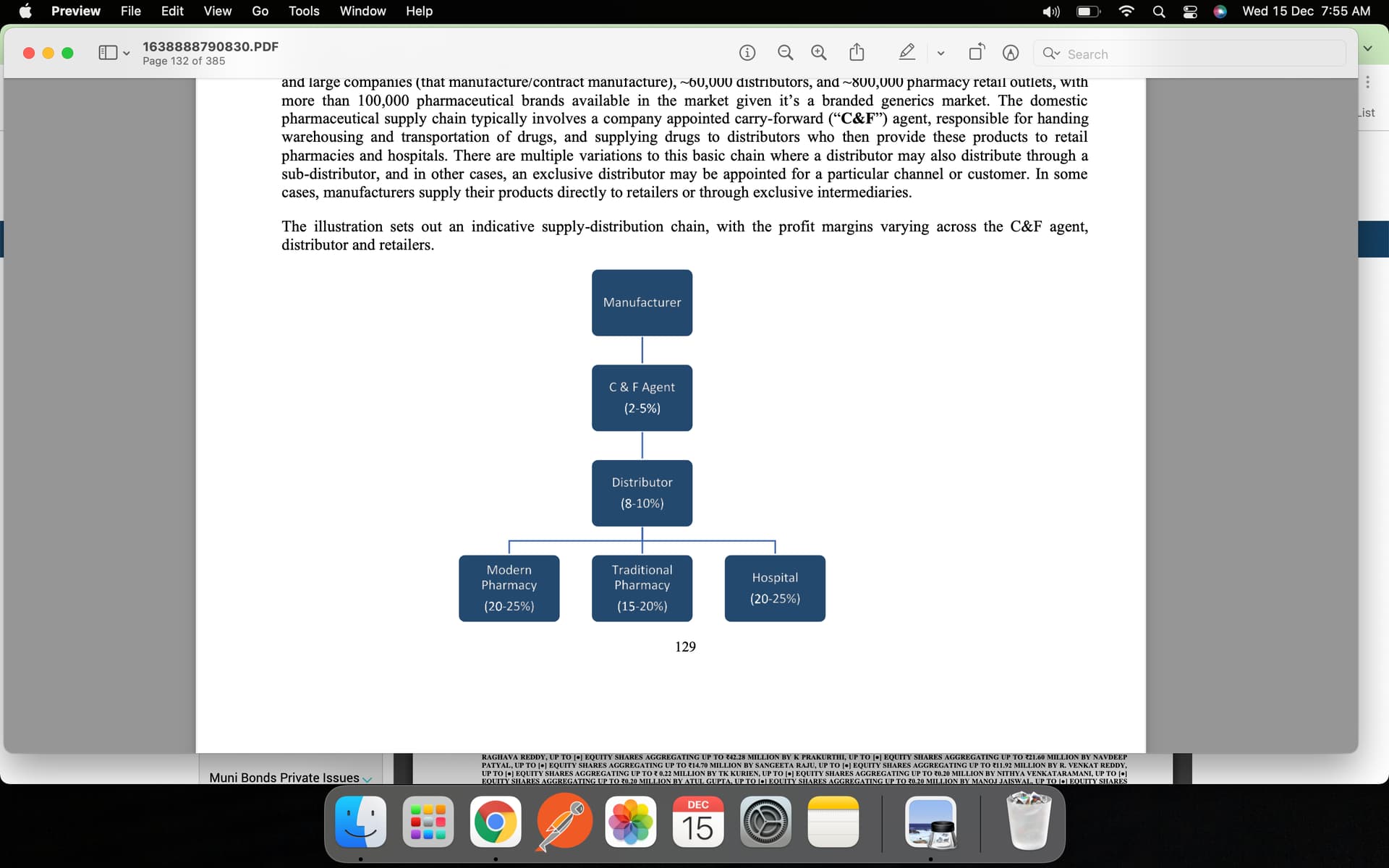

Some data on Physical Pharmacists and their relationship with their Distributors & Economics:

PTR: The price at which retailer will purchase goods from stockist or distributors is a standard Industry term. Retailers are given a discount over and above this PTR which ranges from 3-6%, the one I interacted with was a medium size Retailer and his discount ranged from 3-5%. The distributor also provides a 7-15 day credit period to the Retailer.

We compared the discount of over 20 leading branded medicines on RetailerShakti over his prevailing discount and found that RetailerShakti had most medicines on a 6% Discount, leading to total discount to the Retailer over MRP in the range of 23-24%. His distributors would offer him discount in the range of 3-5% over PTR and his total discount over MRP was 21-23%.

He seemed fine with the idea of no credit and a higher discount but had concerns over Expiry replacement, need to see how this is being handled in WB by the Company.

Then we went on to compare drug data for Generic medicines from Cipla GD, Ranbaxy GD(Generic Division) - RetailerShakti couldn’t match the discounts for most medicines that were sought after as substitutes by the larger segment of our population. For some drugs it seemed like the data on the platform wasn’t updated or a standard format was used for discounts because the difference between discounts was even north of 50% on MRP for some leading drugs from Cipla GD and Ranbaxy GD.

The Generic segment forms more than 50% of the sales of the said Retailer and higher margin here is important to him because there is no Expiry Replacement for these meds. Also their margins in this segment are more than 40% in some cases so that automatically takes care of any Inventory losses.

We couldn’t find any data on sleep inducing/related drugs and most of the industry is now not selling them online fearing Regulatory repercussions after the clarification sought from them in February.

Waiting for the results next week

Any inputs on how the new drugs and cosmetics bill 2023 going to impact the Epharmacies?

I don’t think there operations would be completely halted but some drugs mainly sleep inducing and similar classifications which are prone to misuse would definitely not be allowed on the platforms.

Steep discounts also might go away which would at least give some relief to the Drug & Chemists Association and the lobbying intensity might slow down.

Online consultations are actually most probable to exploitation and should be strictly regulated. This will turn out to be a boon for the Industry in the bigger picture.

The company came out with better than expected results, wasn’t expecting this large GM improvement this soon in the business.

QoQ the revenue is up 6%, GMs moved from 7.6% to 10.6%. The company could be sitting on Inventory gains so I wouldn’t extrapolate the margins this soon for the coming quarters - very good if the margins continue in the same trajectory.

Healthcare business is now in black ex the Health+ Associate loss.

Company in the current presentation has published breakup of its revenue across multiple healthcare divisions, highlights from today’s concall:

This business will largely become cash flow positive in a year as per management guidance.

This business turned EBITDA & PBT +ve this Quarter because discounts across e-pharmacies are reducing thus in turn they reduce their offered discounts to customers.

Retailer Shakti B2B - This business continued its growth momentum both QoQ(34%) and YoY. This will require second leg of investment, will become cash flow positive in 2-3 years time.

Genu Path B2C Wellness & Diagnostics Vertical - This is a very small business for them currently but in a very nascent stage but the company is investing in this vertical. I doubt the end economics and market competition in this business, need to see what management sees in this business. This will largely be a cash burn for them.

Other Data points:

The Myjoy Subsidiary doesn’t have a definite agreement with Health+, ordered in Gurgaon but was delivered from a local Pharmacy even when Noida has the Myjoy Warehouse, closest vendor to Customer is being chosen and in this case it wasn’t a Health buddy. Still need more clarity on their relationship with Flipkart. Orders for Norther Haryana are being fulfilled by their Myjoy Warehouse. This was also confirmed by Management on call today that there are other wholesalers present on the Health+ platform.

Growth in HealthBuddy Supply Chain Business: Need to see if they’re expanding beyond WB or plan to and the growth rate in this business and whether the Health+ platform is open to onboarding non Health buddy retailers. This is a key risk, if the Health+ platform starts onboarding Local Retailers on mass to grow.

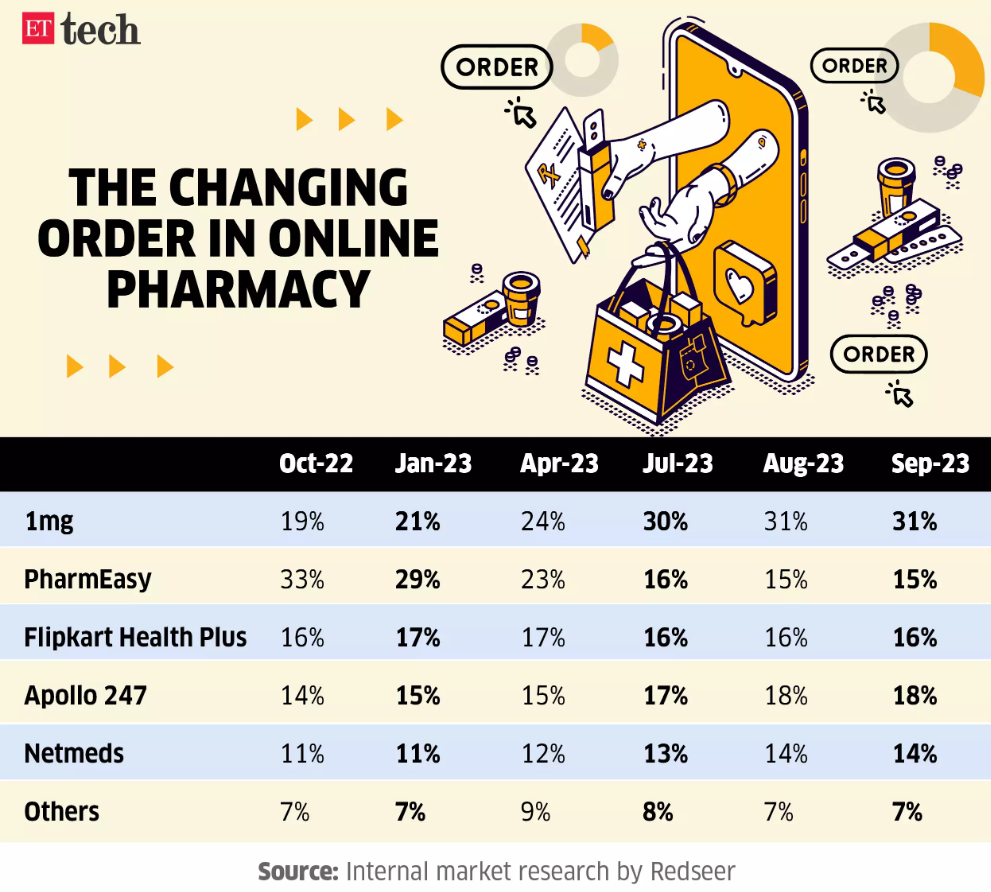

Management believes the online Cash burn discounts are soon diminishing due to dried up VC funding in this sector. PharmEasy’s recent valuation downgrade by their investors corroborates with this data point.

New Warehouses: Management had in earlier presentations talked about opening 20 new warehouses but they’re now slowing down. They’ve scrapped plans of opening new warehouses and believe that 7 is a sufficient number for them to supply pan India. Focus is on profitability for these 7 warehouses.

Consolidation in Digital Business: Management believes in the near term the growth could be low due to moving away of discounts and the real customer base sticking behind but are largely confident in long term prospects of the business. I personally believe this will be one of those Habit Forming businesses at least for Chronic Patients - Dad pings me whenever he sees medicines need to be ordered, I order it at my comfortable time and with much better pricing than Retailers. Most retailers don’t give over 10% discount but given the economics and the number of distributors substituted in the current Physical supply chain I believe 15% is a sustainable discount and will drive customer towards them. Flipkart Logistics and Brand is another key customer trust point.

Corporate structure Simplification will be likely done in a year.

Good result in Q3 2024

https://x.com/prasad_bsrk/status/1752702245328793656?s=46&t=FBaJMigqnEjzmIJQ1DviWg

Q3 FY24 Concall Notes:

RETAILER SHAKTI QUARTERLY INVOICE DATA - 11K RETAILER, 1.33L AVG QTRLY INVOICE

Q2 FY24 - 9684, 1.27L

PURE B2B BUSINESS SO GROSS MARGINS ARE LOWER BUT OPERATIONAL COSTS ARE LOWER COMPARED TO HEALTHBUDDY BIZ. IS OPERATIONALLY PROFITABLE IN CALCUTTA, NOT IN OTHER REGIONS BECAUSE TECH COSTS AND BUSINESS DEVELOPMENTS COSTS. OPERATIONAL LEVERAGE IS YET TO PLAY OUT.

E-PHARMACY BUSINESS IS FACING CONSUMER SENTIMENT ISSUE BECAUSE DISCOUNT IS MOVING AWAY SINCE BUSINESSES ARE FOCUSING ON SUSTAINABILITY AND THUS REVENUE IS TAKING HIT BECAUSE OF PEOPLE ORDERING LESS BECAUSE OF LOWER DISCOUNTS.

DIAGNOSTIC BUSINESS: THIS BUSINESS WAS STARTED FOR OUR HEALTH BUDDIES TO TAKE ADVANTAGE OF B2C PRESENCE BUT GIVEN SASTASUNDR ACCQUISITION BY HEALTH+ THEY CAN’T MOVE FORWARD WITH THIS. SO THEY’RE DESIGNING A NEW STRATEGY ON THIS FRONT. WILL HAVE SOME UPDATES FOR THE DIAGNOSTIC BUSINESS IN THE NEXT FEW MONTHS.

10% BLENDED GM NOT POSSIBLE FOR NEXT 2-3 QTRS BUT FOR A 2 YEAR HORIZON THE GM WILL BE 10%. EXPECTING INCREASE IN PROCUREMENT MARGIN BY 3-4% OVER THE LONG TERM DUE TO HIGHER VOLUME OFF-TAKE IN RETAILER SHAKTI.

EXPECT OPERATIONAL COSTS TO STABILISE AFTER THE MARCH QTR AND WILL NOT GROW AT LEVELS OF REVENUE GROWTH

APPLYING PREDECTIVE ANALYSIS TO INCREASE WALLET SHARE OF THE RETAILER BY PROVIDING THEM ADDITIONAL OFFERS RELEVANT TO THEM, PASS ON ADDITIONAL BENEFITS.

RETAILER SHAKTI BUSINESS: ORDERS ARE FULFILLED ONLY AGAINST ADVANCE PAYMENT/COD MODEL, SO NO CREDIT MODEL YET RETAILERS CONTINUE TO STICK TO THEM INSTEAD OF COMPLETE BIZ FROM UNORGANISED DISTRIBUTORS WHERE CREDIT IS PROVIDED, SO WE SEE DROPOUTS BUT RETAILERS THEN COME BACK TO US BECAUSE OF OUR TRANSPARENCY AND PRICING MODEL. LOTS OF CASES WHERE AFTER FEW MONTHS RETAILERS COME BACK. LARGE RETAILERS DO GET CREDIT FROM US WHO HAVE MULTIPLE STORES, IN DISCUSSIONS WITH FINTECHS AND BANKS FOR FINANCING CREDIT TO THE RETAILERS WHERE RISK LIES WITH THE FINANCIAL ENTITY AND NOT WITH US.

THERE IS SOME INCENTIVE RELATED TO VOLUMES FOR RETAILERS AND OFFERS QUOTED TO THEM FOR MONTHLY QUOTAS

WC TO STAY AT 10% OF REVENUE

OPERATIONAL LEVERAGE WILL PLAY OUT WITH INCREASING VOLUMES EVEN WITH SIMILAR GROSS MARGIN PROFILE

TARGETING 15K RETAILERS ON THE RS PLATFORM BY THE END OF THIS QTR.

EXISTING WAREHOUSES(7) ARE SUFFICIENT TO TAKE CARE OF GROWTH FOR NEXT 1-2 YEARS

OUR SHARE IN RETAILER’S TOTAL SUPPLY IS VERY MINISCULE ESPECIALLY FOR MOM AND POP STORES

NO PLANS FOR OUR OWN OFFLINE PRESENCE, FOCUS IS ON RETAILER SHAKTI FOR NOW

IN PROCESS FOR COSTS CUTDOWN IN THE HEALTHBUDDY SUPPLYCHAIN BUSINESS BECAUSE OF LOWER SHORT-TERM EXPECTATIONS FROM THIS BUSINESS, SO EBITDA NUMBER NEXT YEAR WILL BE DEFINITELY HIGHER

CASH IS PRESENT IN SUBSIDIARY COMPANIES AND CORPORATE SIMPLIFICATION WILL LEAD TO CASH COMING BACK TO HOLDING COMPANY ONLY THEN FURTHER INSTRUCTIONS CAN BE GIVEN ON CASH UTILISATION

There is another company recently listed as Entero Healthcare Solutions Ltd Leading Healthcare Product Disributor The company is among the top three healthcare distributors in India in terms of revenue. Please comment on this company as well. I think the business now similar to SVL.

Sastasundar parted ways with Flipkart. The old website is live again

Not sure about the shareholding pattern now. Heard about their disagreement with Flipkart few days back from the delivery person.

Yeah this is similar and leading healthcare distro

Entero acquired a pan-India supplier

Acquisitions in FY2025E: In FY2025E, Entero has completed nine acquisitions, which add collectively Rs7.5 bn in annualized revenue in FY2024, and has added new product categories like diagnostic, consumable, and equipment, medical devices, etc., and added newer geographies as well. Also, Entero has signed binding MOUs with two entities in Kerala and Haryana, which has been disclosed recently.

Thus, Entero is on course to achieve Rs10 bn of annualized revenue from inorganic forays.