While Saregama exited this deal, it signed on with Google’s YouTube Shorts, a service similar to Instagram Reels. It announced this deal on Tuesday, leading to a 5% increase in its stock price. The company has not previously announced the termination of its deal with Meta.

Can you share any source stating “the deal termination with Meta”.?

10 Likes

Seems true. Couldn’t able to find songs of Saregama on Instagram. This is surprising giving the fact meta is pushing a lot for reels lately and this expense (I’m assuming) must be very small compare to total expense of meta. May be Meta’s analysis doesn’t have shown much value coming from saregama’s songs.

Not sure if youtube shorts will be able to replace insta reel’s volume. Insta is mostly entertainment / casual platform, Youtube is more like edu / professional content type (May be that’s just the way just I see it currently).

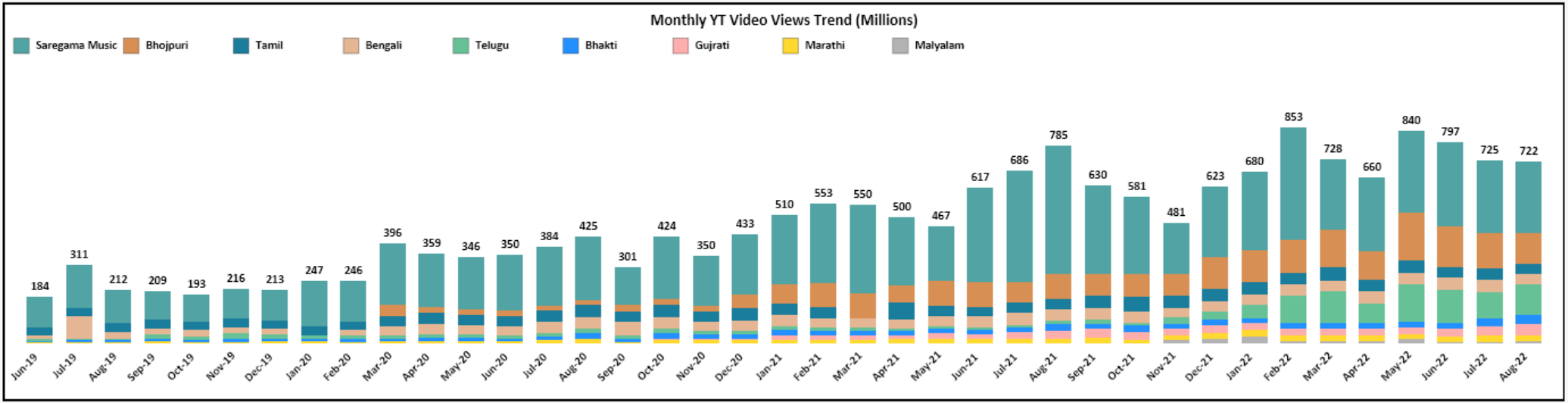

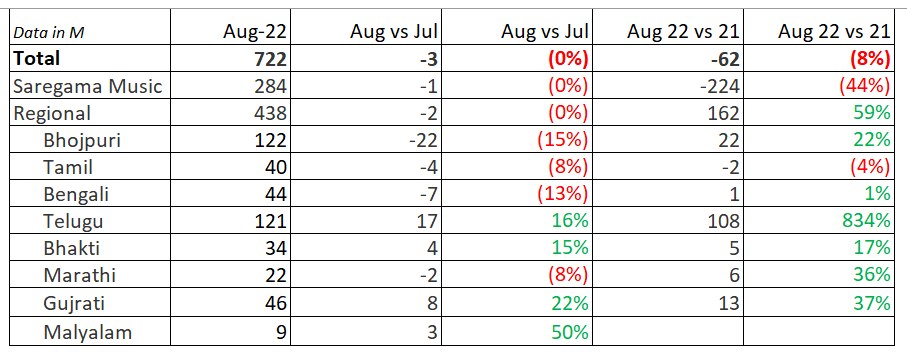

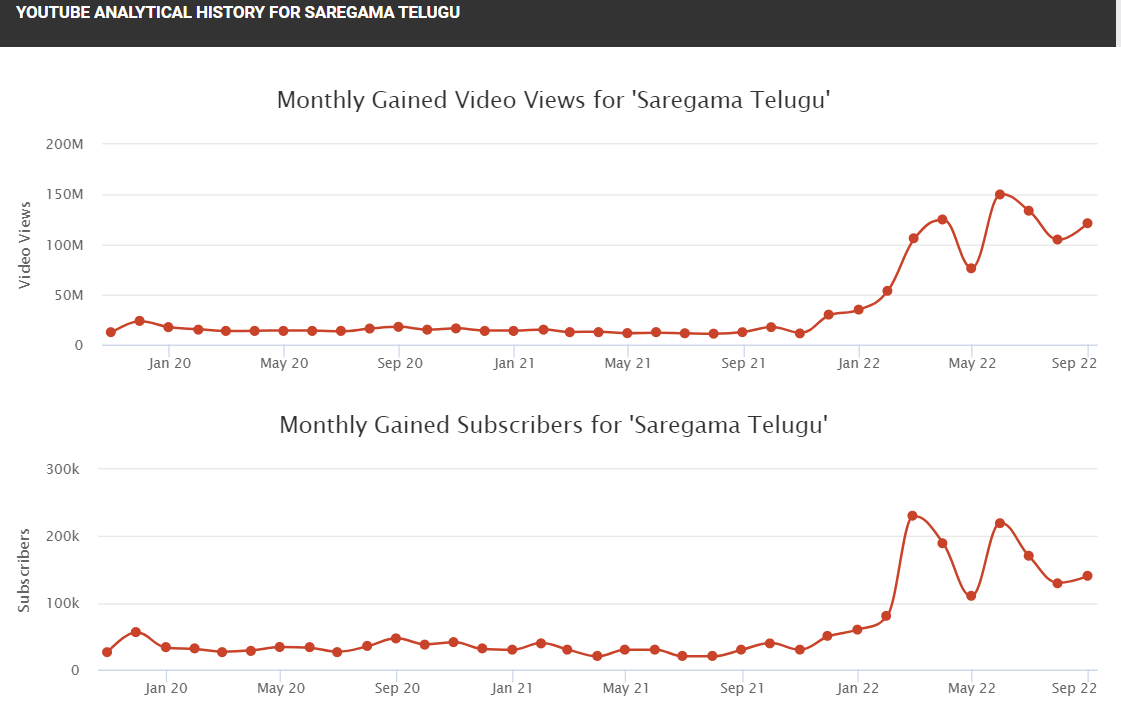

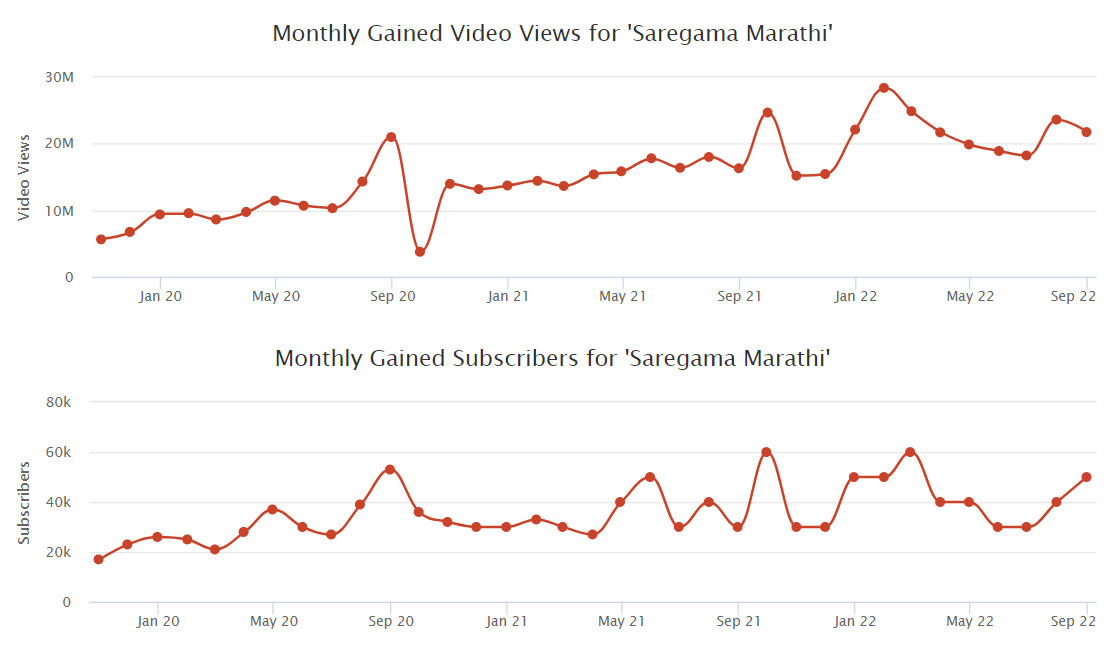

Btw, Adding data points for Aug You-tube View Trends…

/Source: Social Blade

- Video views stagnant (slight decline) over last 3 months.

- Regional channels are driving the growth in video views while decline in views on main channel.

2 Likes

As we know, short format deals are fixed. So regardless of volume, saregama looses fixed amount. Negotiation seems failed, as saregama must asked for higher amount due to increased use of catalogue, however meta may not want to increase.

Saregama had such deal problem with spotify and resolved later.

In Tips concall it was mentioned that no music label will be available on ALL platforms. There is always one or more missing in a platform.

I believe saregama (vikram) want to send message that they are not at mercey of a particular platform.

Disclosure: Invested in saregama not in Tips.

6 Likes

https://twitter.com/blitzkreigm/status/1567087449368854533

SAREGAMA gets into Feature Phones with Pre-Loaded Songs as its USP. Priced at Rs 2490 and Rs 1990 for 2 screen sizes, it has 1500 pre-loaded Hindi songs, with additional 2GB space for other personal media.

3 Likes

This is not a good capital allocation at all.

9 Likes

Gaana moves to subscription only model as acquisition talks with Airtel fall through.

Fighting to survive, Tencent-backed music app Gaana turns to subscriptions | Business Standard News.

Streaming company economics and business model sustainability is an underrated risk for IP holders. Over time, IP holders may have to settle for better terms with streaming providers for the sustainability of the ecosystem.

10 Likes

Many risks are actually playing out currently.

- While saregama does have minimum guarantees in place the overflow revenue is because of growth in advertising. In a recessionary setting those wil suffer specially for Europe & western world geographies. When Europe is finding it difficult to pay bills i find it hard to imagine how anyone renews their Spotify 7 or 10 € / month subscription. This is a discretionary spending

- The carvaan phone is at least a management focus misallocation; depending on the wc requirement could be a capital misallocation too (bears would be quite to judge and bulls will probably give management enough time to execute).

- Gaana going off of free is at least a buyer side consolidation and can potentially affect the competitive dynamics of the industry going forward

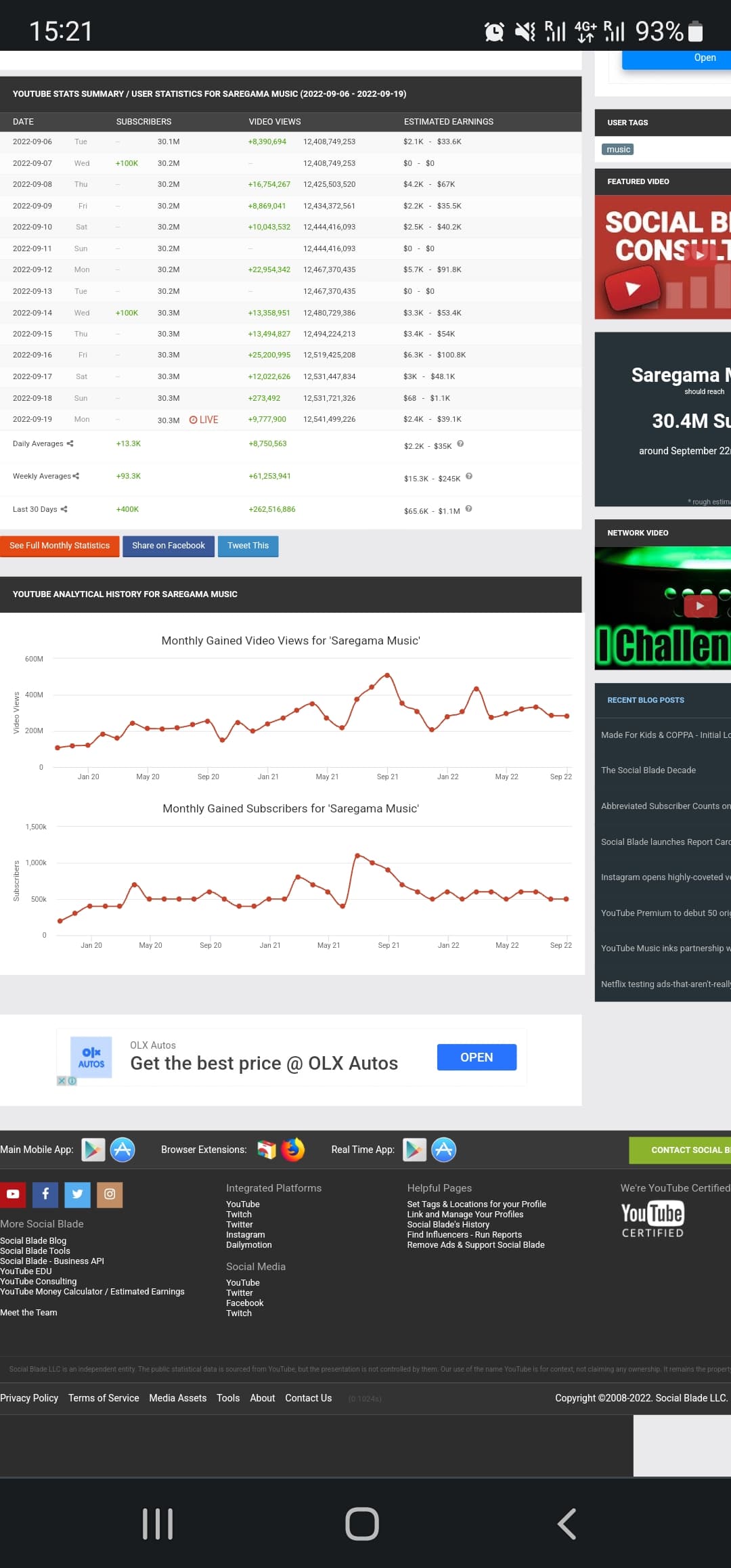

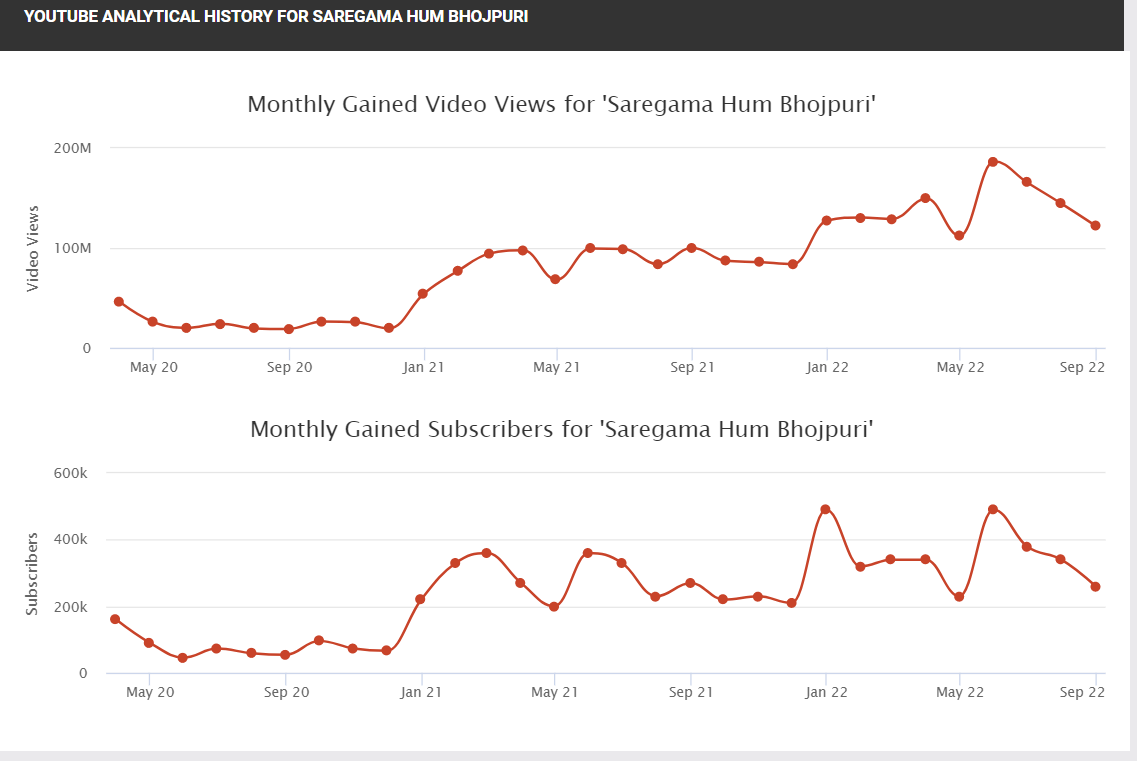

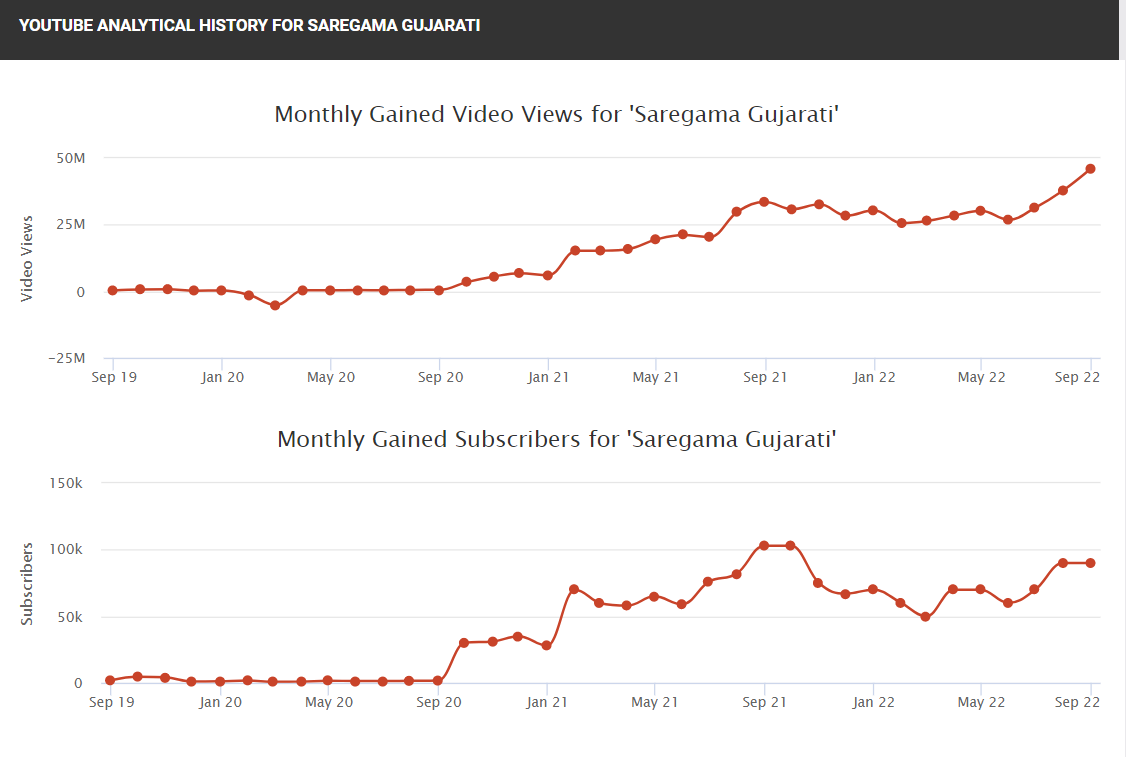

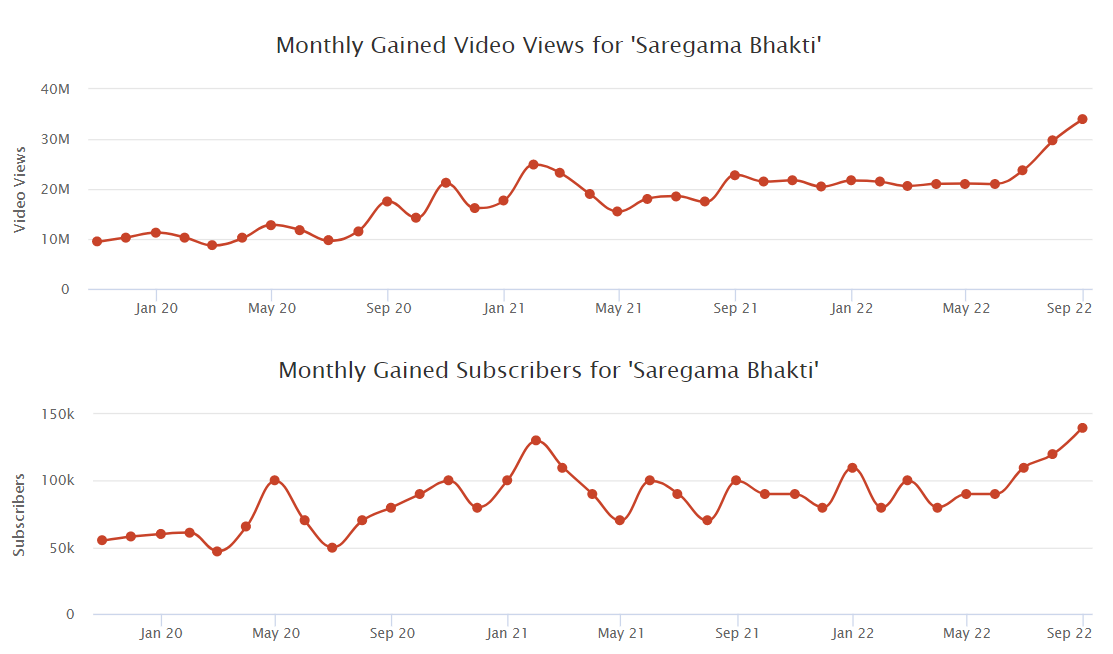

- From my calculations their streaming revenues have not been growing that fast last few quarters. Just see social blade stats for views

Alone each of those are probably things investors can ignore taken together imo they imply a real xirr risk at least in medium term of 1-2 years. I have halved my position. The supply side industry structure is still too too tooo good and thus i won’t be removing the position altogether. Let’s see how the one goes.

Disclaimer: invested, reduced position to half recent weeks.

7 Likes

Adding some data to above points. The concern pointed is valid.

| Quarter | Music Lic. Quarterly run rate | QoQ % | YoY% | YT Ads Quarterly | QoQ % | YoY% |

|---|---|---|---|---|---|---|

| Q1-FY21 | 65 | 3812 | ||||

| Q2-FY21 | 77 | 18.46% | 5037 | |||

| Q3-FY21 | 73 | -5.19% | 6885 | |||

| Q4-FY21 | 68 | -6.85% | 6005 | |||

| Q1-FY22 | 82 | 20.59% | 20.73% | 7002 | 16.60% | 45.56% |

| Q2-FY22 | 91 | 10.98% | 15.38% | 7205 | 2.90% | 30.09% |

| Q3-FY22 | 91 | 0.00% | 19.78% | 8633 | 19.82% | 20.25% |

| Q4-FY22 | 94 | 3.30% | 27.66% | 6869 | -20.43% | 12.58% |

| Q1-FY23 | 98 | 4.26% | 16.33% | 7340 | 6.86% | 4.60% |

Above is the data which has my estimates of their quarterly run rate of music licensing business, along with YT Ads revenue disclosed by Google. It does seem that quarterly run rate for Saregama is slowing down and YT Ads surely did have slowest YoY growth recent quarter, but Vikram did say that Q1 is soft quarter, so he expects higher next quarters.

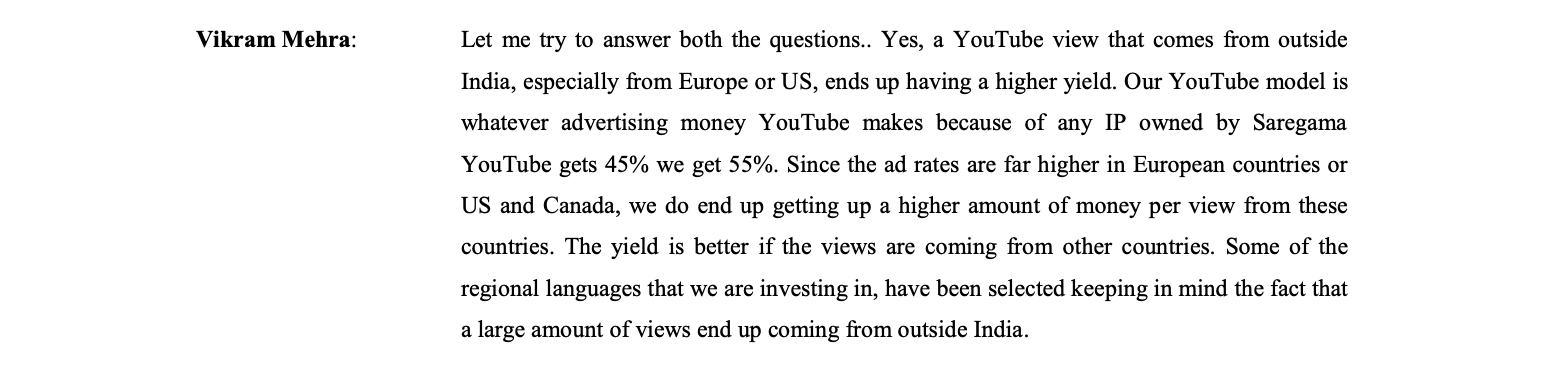

While Saregama does get 55% share of advertising revenue from Youtube, but we don’t know that how much of this is international revenue. This international revenue has higher yields.

Since we dont know the distribution of minimum guarantee revenue from streaming apps, advertising revenue from YT (domestic + international), paid subscription revenues, it is hard to know exact quantum of impact. But there will be some impact, how much material only future can tell.

Eventually, 2-3 quarters, the numbers can look below expectations, but this is where tough part for all of us begins, leaving easy money behind, I guess - Wait for headwinds to pass or sell, no one can give right answer atm. ![]()

Disc. Invested, no transactions in last 30 days because I think below picture (yearly revenues) is more likely the direction.

| Music Licensing | |

|---|---|

| FY18 | 148 |

| FY19 | 194 |

| FY20 | 238 |

| FY21 | 283 |

| FY22 | 358 |

| 19.32% |

6 Likes

Agree with narratives that there might be a slowdown, but it isn’t yet showing up in data. Q1 has always been soft. Yet from Q4 (Q3&Q4 seasonally the best Q’s). The company has still grown revenues QoQ in licensing division:-

Secondly, the pre-ceding Quarter and the current Quarter has been weak in terms of launches. This becomes clearer from the fact that majority of the content that was acquired last year will get launched in H2 this year or by Q1 next FY. Here:-

Thirdly, Capital allocation. Ideally, no one likes the Carvan division, but if the product is contract manufactured and little capital is deployed. How does it matter? Wasn’t decision to Demerge the magazine biz a bigger positive here?

A Quarter or two of softness or even some consolidation in the stock is good after a huge run up we saw. Helps to build more clarity for people already holding the business.

Multiple approaches one can take here:-

-

One can act like a positional trader/investor, and re-enter when the growth journey resumes.

-

One can just sit tight, and accept such bumps of quarterly variations as a part of the journey. In India, Paid subscriptions haven’t even taken off. Find it hard to digest how a recession directly impacts. Indirectly yes, unviable businesses like Gaana might suffer. In USA, last I checked market is pretty consolidated:-

Yet, the Labels make the money and control nearly 60% of the profit pools of the industry.

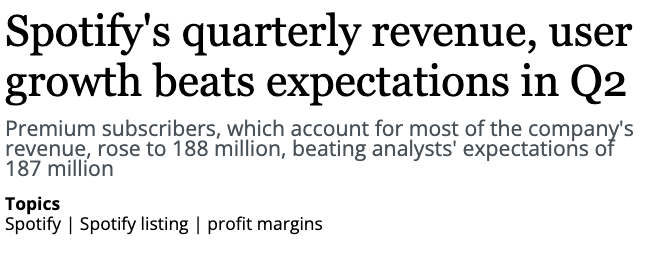

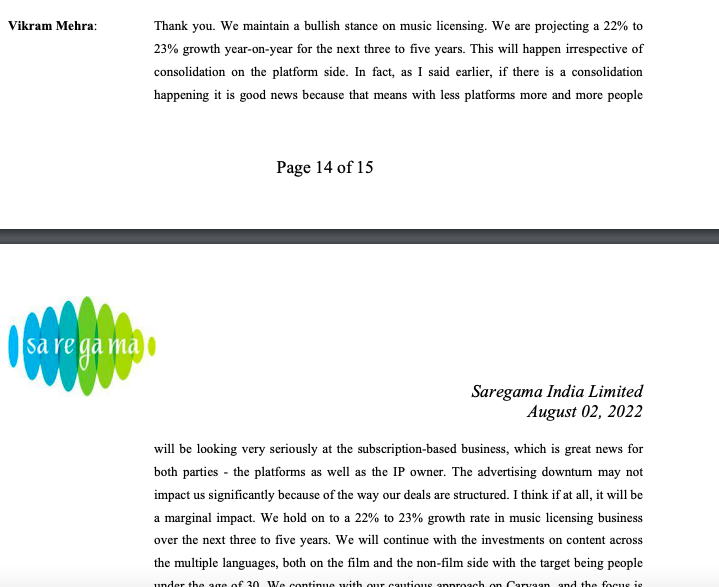

Last I checked, this Q Spotify’s revenue also grew at a very healthy clip and they ended up beating all the estimates. Here:-

What can the long term picture be here like and a counter view point to consolidation?

Disc: invested. Willing to take Quarterly bumps and not trade around too much in personal pf.

27 Likes

Thank you both for your analysis and sharing your viewpoint. The points you have raised are correct but it looks like the picture you have shared is not complete.

-

Inflation in Europe- Europe has a Per capita income of 3000-5000 euros per month, its more than what we make in India per year. So cost of spotify may be 10 times more in Europe but it is less than India as a % of monthly income.

And while it is true that Energy bill has increased (I am paying these higher bills personally), but the increase in Energy bill is in hundreds of Euros per month. 7-10 Euros per month for a music service is not first thing that comes in mind to save money. -

Carvaan phone is definitely a misallocation, but so is Carvaan in its current radio avtaar. So nothing new unless management starts spending a lot of money & time on it. Going by Vikram’s earlier statements, I suspect mgmt will spend too much bandwidth on it. But yes, need to wait on this one for more clarity.

-

Gaana going off of free- We are talking about one player in the whole industry, it is too early to call it buyer side consolidation.

-

Views on channels- While the views have reduced on some channels, several other channels are showing very good increase as well.

At the end of it, I see that sector may go through a patch of consolidation, but I won’t call them headwinds. We may have to decide that whether we want to wait out the consolidation phase or get out now and come in later when the tailwinds come back. For some savvy investors like @sahil_vi I believe the opportunity costs are too high to wait it out ![]()

17 Likes

Serious red flag against the promoter group of saregama RP Sanjeev goenka family:

To quote from redboxindia’s twitter handle

“CENTRAL BUREAU OF INVESTIGATION (CBI) HAS REGISTERED A CASE AGAINST COMPANIES OF THE RP-SANJIV GOENKA GROUP ON CHARGES OF CORRUPTION, CHEATING AND CRIMINAL CONSPIRACY”

MQ & its perception can take a serious hit here. Have decided to sell rest of my stake as well.

https://twitter.com/REDBOXINDIA/status/1572434280684617728

Saregama investors must ask themselves to what extent their endowment bias is disabling them from processing incremental information & data.

Looking at Saregama Gujarati etc are missing forest for the trees. They are insignificant compared to saregama channel views and subscribers. Have done this exercise for exhaustively for many months

Looking at Spotifys July release is focussing on where the puck was, market rewards ability to judge where the puck will be. Of course that is a probabilistic question. Let’s see where we end up. Happy to be wrong coz it’s an epic co. Even if i am wrong in my sell decision the way I’ll evaluate myself is on what i did with that capital and the xirr it generated.

11 Likes

This is some coal block allocation issue running from 1990s on RPG group.

Even at the time of buying Saregama, everyone knew RPG group was not the cleanest. Their recent buying of IPL team was also a negative indicator. RPG Life sciences perception has not been good either. But the bet remains on the industry structure and trend, not on the group.

18 Likes

The whole monetisation of youtube shorts explained very clearly and how the creators will be rewarded. Creators will be monetized at the same rates as a youtube video!

Saregama Music is back on instagram and Facebook.

Disc: invested.

4 Likes

Can you please share the source/article?

Simply check on instagram reels- Saregama music wasn’t available between July-August. It is since yesterday, possibly indicating a new deal with Insta and FB

2 Likes

Anything happened inbetween these 2 month, why saragama’s musinc not available in the platforms ?

1 Like