Looks like an agreement.

1 Like

Decent quarterly results for the music business as a whole. However, starting to get concerned by the frequent tinkering with the ammortization policy of new music acquisition. Conveniently, this comes right before Saregama is likely to go into a phase of high content acquisition. Does anybody have any idea how global players ammortize rights?

The Group has a history of poor corporate governance, such accounting jugglery makes me nervous. Anybody have any thoughts?

6 Likes

Global players does it between 10-25 years as mentioned by management in concall.

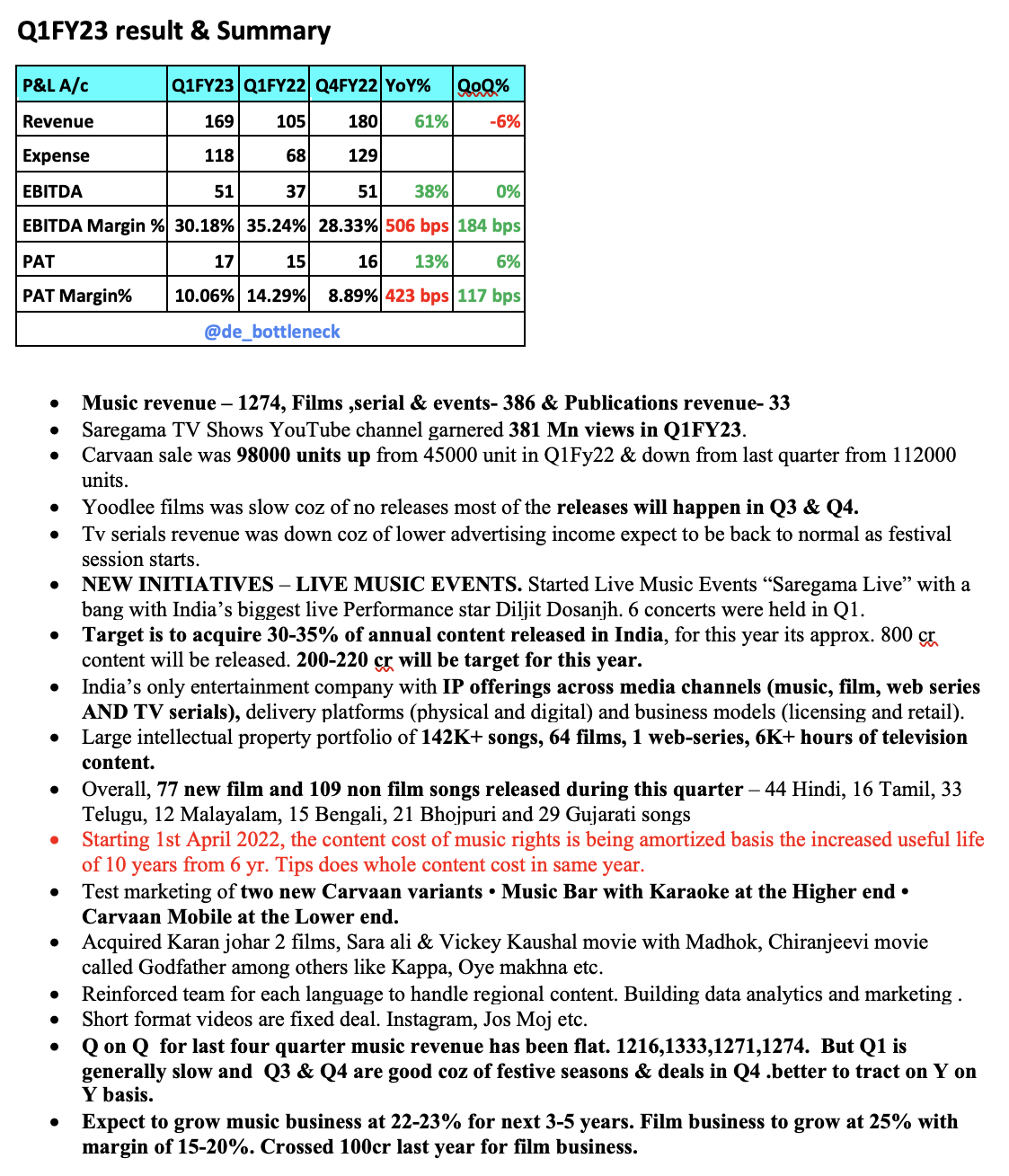

Q1FY23 Results|Strong in a seasonally weak Quarter:-

Business

-Music segment grew by 38%, which might be better than global labels and other labels in India. Q1 is generally a soft quarter.

-In terms of revenues, Q4 is the best Quarter as International Publication Revenue & Society Revenue hits in Q4. Carvan also does well due to festive season.

-Whatever Music saregama is acquiring, its impact will be visible only 12-18 months down the line. As in Bollywood, music gets sold 12-18months in Advance.

-Music Acquisition Strategy

-

Have raised 750 crores in QIP which provides us with the growth capital.

-

Only People below 30 are involved in picking the Music.

-

Every Year, content worth 800 crores is released. Saregama’s target is to capture 30-35% of the incremental content market. Thus, 240-250 crores of spending on content going forward.

-Change in Accounting related to new music acquisition

-

Music that the company acquired even in 1970s is still growing at a healthy pace. Current useful life of music is 6 years.

-

Asked E&Y, almost every other music label in the world is amortising music over 10-25 years.

-

Changing, useful life of Music from 6 years to 10 years.

-

How was it done earlier?

-If Rs100 are spent on music acquisition, Rs20 is spent towards marketing and Rs80 is spent on the Actual Music.

-Rs 20 on Marketing is written off in Year 1.

-Rs 80 is amortised this way:-

35% in Year 1.

13% in Next 5 years.

- The changes in Amortisation now?

-Rs 20 will be written off in Year 1 which is meant for marketing.

-Rs 80, 20% will be amortised in Year 1, 15% in Year 2 and 8.12% in the remaining 8 years.

Why has this been done?

-Total impact is net 1.7 crores positive this Quarter.

-Acquiring a lot of content going forward, have to prepare company for practical realities. Life of music in reality is much higher as proven by music from 1970s and 1960s still doing well.

-Unlike Global Peers, who do straight Line depreciation. Taking a more conservative approach of front loading Amortisation in earlier years.

-Did 6 successful events with Daljit this year. Business of live events should be EBITDA Positive and will contribute to topline.

-Events business is a 5-10% margin business.

-Youtube growth is coming through organic uploads on the SAREGAMA Channel. Market leader in Gujrati and Bhojpuri Music.

-How Music Licensing Revenues are earned?

A) Short Format app deal (insta reels eg) is fixed fee deal in general.

B)Variable Deal with Minimum Guarantee+Fixed fee. This will happen with Short Format when numbers become substantial. Already seeing overflows.

C)Are licensing revenues cyclical?

Licensing Revenues aren’t too much Ad dependent, as in most deals SAREGAMA earns through fixed paisa per stream. No impact of ad slowdown on Licensing business. TV Part is hurting though (but too small as a % of business).

Management

-

Company continues to guide for 22-23% growth in Music Licensing in the next 3-5 years.

-

No plans for stepping up investments in Caravan.

-

Movies & Films Business is a 15-20% Margin Business. This business is already at 100 crores and should become 150-200 crores going forward. All content related costs are written off in Year 1. 2nd round of content licensing hasn’t been factored in this business.

New Launches

-New content acquired will start getting released from Q4FY23 and FY24.

-Eg:- Karan Johar, Rocky Rani, Dharma Rola, Some Salman Khan songs in Godfather (Telugu movie) and Prithviraj Kappa etc.

-Bhojpuri, Nathunia Song by Khesari Lal crossed 150m+ views on YT in less than 3 months.

Key Risks

-

IRR on new music. Management has done well in the past, will be interesting to see going forward.

-

Investments in Carvan. Though Management categorically denies.

3. Any slowdown in category or any streaming player going bankrupt.

Disclosure:- Invested since Early 2021, and continue to believe in long term story of Saregama, along with the risks mentioned above. Not a recommendation to buy or sell. Not SEBI Registered. Looking segmentally, Music Licensing revenues have grown 3% QoQ in a seasonally weak Q.

27 Likes

- ++Streaming player getting acquired or out of business would mean that existing players would try to move towards paid streaming which is expected to be win win for labels and platforms.

3 Likes

The useful life seems to be in-line with competitors below. Plus if we look at the revenue share from songs from 1960-2000 it is currently at 57%, which would imply that 10 years is not a totally unreasonable assumption for useful life.

Hipgnosis Songs Fund

The Group amortises Catalogues over a useful life, using a straight-line method of 20 years, which is in line with industry standard.

Round Hill Music Royalty Fund

The Board has assessed the useful life of each Catalogue’s assets to be 16 years and amortises its intangibles as such;

Warner Music

Recorded music 10 years and publishing copyrights 26 years

Universal Music

The majority of the music catalogues are amortised over 20 years on a straight-line basis. Some significant catalogues can be amortized over longer period of time.

8 Likes

So as I understand the IP will owned by the artists and the creation cost also. Is it ?

on what parameters we can actually assess that the company is earning good IRR on new music and is doing prudent capital allocation on acquiring new content… would you look at traditional parameters like ROE and ROCE 2-3 years later to check how good IRR they earned 2-3 years back from that year in future? how one can assess this IRR?

1 Like

Songs reliese before movies, and get less traction initially,

whenever movies reliese, songs become more popular than earlier !!!

am I right ?

2 Likes

Nowdays what’s happening is that film makers is giving more emphasis on song. People think that if song is good then movie may be good not 100% sure. Currently only 15-30 second line of song is catching people’s eye which is called “Hook” in music. Like recently launched song kesariya by arjit, jugnu by badshah, ghungroo song of war movie and many more. Even what content creator is focusing is only on one line of song on which they will create their reels and short.

So, song which have a catchy hook also called Tiktokification will get more views by creators.

8 Likes

so till now , saregama did not get the revenues from youtube for music used in shorts?

Doesn’t seem to be the case as YT shorts have really taken off in last 6 months. Observed it first hand being the owner of a youtube channel ![]()

8 Likes

:-)… any insight on unit economics of YT shorts?

2 Likes

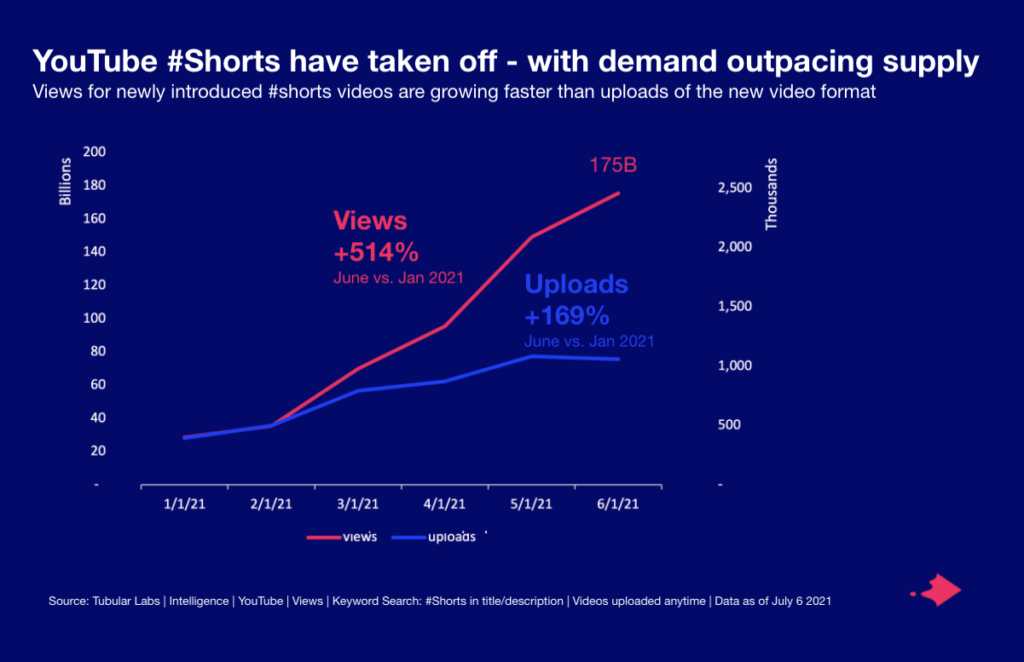

Some stats that I could find online:

-

YouTube Shorts receives 15 Billion views daily which was 3.5 billion views in 2020.

-

More than 70% of YouTube watch time is through mobile and Shorts are mostly consumed on mobile devices.

-

More than 70% of YouTube Shorts are longer than 15 seconds. Max limit for any YouTube short is 60 seconds. This average duration being 15 seconds will help music labels as nowadays only a small line of a line is becoming more and more viral (also known as the “hook” line of a song).

-

YouTube has a $100 million YouTube Shorts creator’s fund. This is a very big initiative from Google to encourage creators to get bonus monetization for creating shorts. This bonus can vary anywhere from %100 to $10,000.

10 Likes

This is great. Does anyone know how much one can earn from shorts? is it same = 10p/ song?

It was mentioned on concall, all short video apps are lump sump and there is industry agreement that when it become bit, it will be pay per stream model, so YT Short may be lump sump.

Another lever still pending is subscription model take for audio OTT.

Disclosure: Invested

2 Likes

Moreover, There seems no ad revenue shared to the content creator right now when YouTube shorts are played from ‘shorts section’ rather than going by the creator’s channel and then viewing the short content(Very less) thus ultimately will not get the share of revenue even if the creator uses Saregama’s catalogue.

So, YouTube shorts for now will remain a lumpsum deal like Meta platforms.

2 Likes