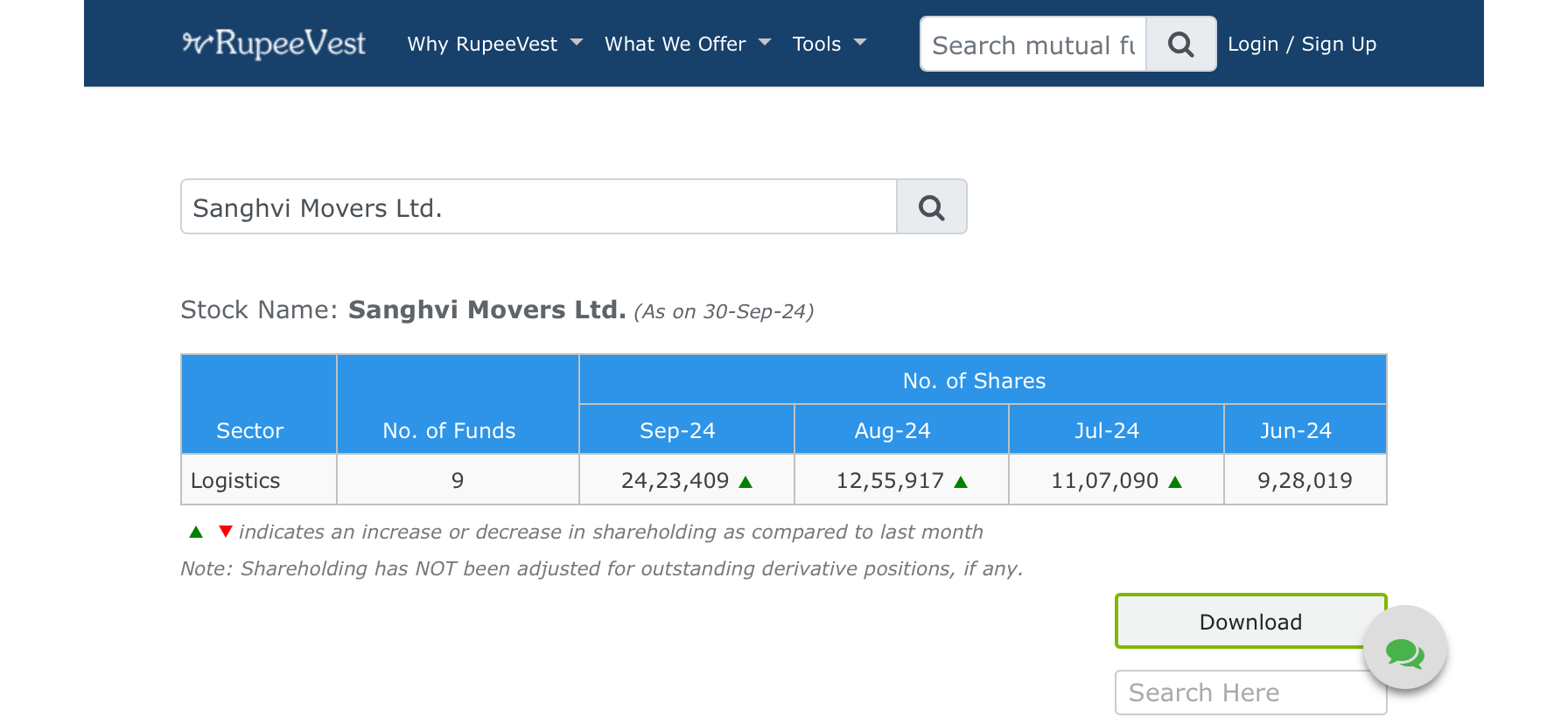

Institutional holding shows steady increase.

Update > Quantity doubling is due to stock split. Apologies for the confusion.

Institutional holding shows steady increase.

Update > Quantity doubling is due to stock split. Apologies for the confusion.

This must be due to the stock split.

record date for split - 27th sept. It fell much before that date and after that date, but did not fall on that date which usually happens in stock splits…

stock split…thats why

Any inputs on this ?

What I’m missing in sanghvi movers, why it is falling like crazy?

Reporting margin compression whereas competitors are posting better numbers

Q2 yield is higher, utilization is lower. That’s good actually.

While the results are bad, the stock is nearly 50% down so it does not warrant further fall in my opinion. Management any guided for a poor quarter

With Trump being in helm of affairs and not at all in favor of renewable energy. Shall we think all such EPC companies (involved in renewable energy sector) may face the headwinds?

Are these companies doing epc in USA?

Good point. I dont get why us policies are beating down india focussed renewable stocks. Make it make sense. Not like India will follow whatever us is doing…

Current ongoing Fall is really surprising …

Not able to find any info regarding the fall or reasons …

Even I am wondering why it fell seems some operator play to push retailer out but looking at the number it was expected as Rishi had mentioned.

Total order book for H2 crane rental is 138 cr, which is nearly equal of Q2 crane rental revenue. EPC busines has lower margin.

How are other crane companies able to get sufficient orders but not sanghvi?

But they also said in concall, 138 cr order book they have till date, there is a possibility that new order come in next 5 months, order extension with existing customer, possible over time.

Company is looking very cheap now. A more than 50% decline in spite of no new surprises and a comfortable order book. A good time to build position maybe. Management was bearish on the concall. That could be a reason. Revenues will grow but margins may contract

Not may, Margins will contract and looks like market isn’t liking that.

Margins for rental business are between 50-55% and for EPC are between 12-15%. As EPC business grows, which it is, blended margins will keep falling.

Silver lining is the EPC business will increase the ROE as the asset turnover will increase.