Yeah i phrased it poorly. But i like that the management is proactive about the whole issue. Management guided for similar numbers in H2 from crane rental… 500 cr down from 592 cr last year … but EPC could make up a part of that hopefully.

1 Like

This company is at an interesting juncture now. A lot depends on how well they execute on their plans for KSA and the GCC region. It seems like the right strategic decision as competition in the crane business starts diluting their margins there (at least in the domestic business). Their focus on IPPs and prudence in managing receivables means they are unlikely to take on government contracts which is a good thing in terms of reducing exposure to working capital risks. However, EPC is a much more difficult business and they are new to this - remains to be seen how well they are able to execute. If they execute well with reasonable margins, it can be a much bigger growth driver.

Anything positive in terms of growth in the crane rental business will be an unexpected benefit as the market seems to have discounted that fully now. Probably rightly so, given what the management said about the on-ground execution delays and funding challenges.

6 Likes

Proud to share our first-ever international project at Hanimaadhoo International Airport in Maldives.

What is this all about?

Maybe he meant this - Found this on their LinkedIn page.

3 Likes

Wow, this crashed far more than I thought. Rishi Sanghvi had indicated H2 would be challenging too, but looks like it will be worse than expected. Haven’t seen any significant news, but all renewable stocks have taken a beating. I guess given their dependency on that segment, this is collateral damage. May also reflect challenging receivables situation, who knows!

8 Likes

In the Q2FY25 concall, Sanghvi Movers mentioned signs of an economic slowdown. However, the bullish bias in me didn’t want to acknowledge it. Hindsight is always 20/20.

8 Likes

Concall tidbits

The Company proposes to do additional CAPEX of Rs. 150 crore in Q4 FY25 and

intends to process some 34 cranes ranging from 110-ton capacity to 800-ton capacity which are

brought by long term contracts from various clients.

Capacity utilization was 70% in Q3 FY25 and competitive intensity is increasing in Crane Rental space.

regarding Saudi Arabia expansion

disc: used to own, Exited at a loss during recent market conditions, tracking for now.

4 Likes

Concall summary:

Plus:

- The Capex so far in first 9 months is 115 crs, but in Q4 itself company is incurring Capex of 150 crs in core crane rental business. Company has insisted that this Capex is backed by long term orders from the customers.

- Unexecuted projects are worth 300 crores in Q4 and company is expected to cross the revenue of 800 crores in Q4. Out of that 142 crores will be in core crane rental business and the rest will be in EPC business. Considering 50% EBITDA in crane rental and 10% EBITDA in EPC business, the expected EBITDA could around 85-90 crores, which is similar to Q4 2024. These are conservative numbers.

- Cash on hand is 178 crores which is 8-9% of the market cap and they can incur the CAPEX with internal accruals.

Negatives:

- 2nd consecutive concall in which the management is giving excuse of general election and monsoon while the other competitors seem to be doing ok. Management repeated the same excuse at least 10 times during the concall.

- Reducing crane rental yield: Crane rental yield was 1.97% during Q3 FY 25 and management is expecting it to settle down at 2% in the long run. Clear indication of increasing competitive intensity in their core business as the historic yield had been in the range of 2.05 - 2.10%

- EBITDA margin in the EPC business would be just 10-12% which is far lesser than the earlier projections of around 20%. I think this has really spooked the market.

Conclusion: The core business is definitely facing the headwinds, but the management is pro-active and the capex of 150 crs in the core business in Q4 is reassuring, especially since it is backed by long term customer orders.

Top line would increase substantially in Q4, but how much of it trickles down to bottom line remains to be seen. The rerating could only happen after the bottom line also shows substantial improvements in absolute numbers (margins would naturally go down as more and more revenue share would be contributed from EPC business).

The market cap has reduced by two third in a short period of 7-8 months. Seems like all the negatives have been priced in. Any positive development on GCC business could help the stock to re-rate.

Disc: Invested and adding at current levels

8 Likes

I am a little doubtful about the 50% EBITDA they expect on crane rental. If competitive intensity is so high, logically, it has to fall further. Let’s see.

For 9M FY 25, the EBITDA for crane rental business is 56% (60% / 57% and 49% respectively in Q1, Q2 and Q3). So, 50% seems quite feasible considering the better demand projection from management. But yeah, would have to wait and see.

2 Likes

Revenue is extremely concentrated towards the Wind Energy Sector (be it crane or EPC), they better set sails and diversify to other sectors soon before the wind runs out.

3 Likes

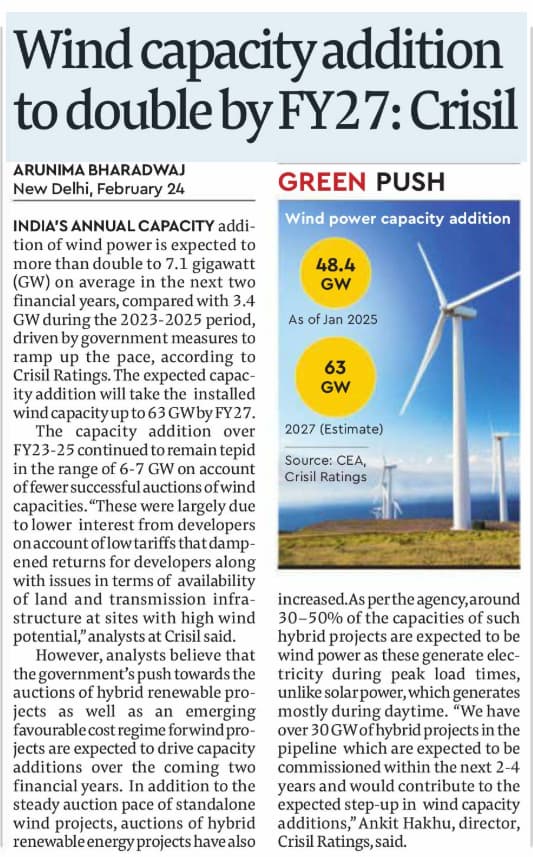

An article that warrants merit to track few data points that may have a bearing on Sanghvi’s guidance (both on crane rentals and wind EPC) going forward

The key trigger for wind energy expansion and IPPs to invest is the different tariff rates for REs. The recent budget increased allocation to the RE sector by ₹9,251 crore, bringing the total to ₹26,549 crore—a 53% increase from the previous budget but more clarity would be required on the viability gap funding (VGF) by the Govt as subsidies for Wind Energy tariffs (especially Offshore Wind) but there is not much clarity. Also, there is less clarity on the original Govt’s plan for Uniform Renewable Energy Tariff (URET) or mandating Renewable Purchase Obligation (RPO) by each state discom. The condition of many state discoms are a known factor for many years. Unless there is a clear policy and execution push, the pace of Wind Energy installation as a pie of the overall Renewable Energy may be a drag with IPPs postponing their capex and the downstream impact will be felt on Sanghvi.

Disclosure: Invested from higher levels but waiting for more clarity on execution of Wind Energy projects and plans by IPP to make a decision of adding more or exiting.

4 Likes

Sanghvi Movers: Intention to Become an EPC Player

-

Policy Shift Impact

- Transition from feed and tariff regime to reverse auction led to a decline in capacity addition.

- In FY14-15 and FY15-16, 5.5 GW was added annually; this level has not been reached since.

- Industry took a long time to adjust to this policy change.

-

OEMs’ Role Shift

- Initially, OEMs provided full product and project services, including wind farm erection.

- Over time, OEMs adopted a global operating model, focusing solely on product supply.

- This left Independent Power Producers (IPPs) to execute projects independently.

-

Challenges for IPPs

- IPPs, primarily hedge funds, pension funds, and private equity investors, lacked execution capabilities.

- Market gap emerged for reliable project execution vendors.

- The supply chain was fragmented, with small players lacking financial strength, corporate governance, and performance reliability.

-

Sanghvi Movers’ Market Opportunity

- Achieved a 15 GW erection track record.

- Present in nearly every wind farm constructed in the country.

- Strong demand from the market to provide additional services beyond turbine erection.

-

Expansion into EPC Services

- Developed capabilities across five key areas:

- Mechanical

- Electrical

- Civil

- Transportation (Surface Logistics)

- Land Approvals & Permits

- Aimed at providing a turnkey solution for the renewable wind energy sector.

- Developed capabilities across five key areas:

-

Industry Outlook & Company Positioning

- Industry is still in its early stages, with top EPC players yet to emerge.

- Some companies have gained traction, but most are still establishing execution track records.

- Sanghvi Movers is committed to only taking projects where delivery is assured.

- Confident in EPC execution, leveraging 15 GW of prior erection experience.

- Strategic approach driven by market demand and in-house capability development.

Source: Latest Concall

5 Likes

Results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/c1b09248-32fe-42b4-84dc-b3d46b4fb8bd.pdf

Nice set but could someone explain why its down despite such good numbers

Its forming a bottom.

Monthly chart: Post ~72% DD from May2024 top to Feb2025 bottom , its given a decent upmove (post multi year retest).

Weekly chart: Post Feb25 bottom, its given a ~70% upmove, most likely capturing the turn in results and markets understanding/reflecting the new business model and margin structure for the company.

Daily Chart: Gives the clearest picture. Bottom forming patterns like the inverse H&S (powerful patterns) are clearly seen. Accumulation can be seen in volume spurts and high deliveries.

It mostly wont be a V shaped recovery back to the previous ATH’s. but a slower upmove, with earnings catching up with valuations.

Post results fall was mostly expected given the previous upmove in past weeks and as per Inverse H&S pattern formation. Trading volatility most likely.

3 Likes

India just did 1 GW wind installation in April alone….whole of FY 25 was 4.1 GW.

Sanghvi guiding for 25-30% growth in topline overall.

Cranes should touch 75-80% capacity utilisation. 84% is optimal according to management.

Looking to be a strong year after a brutal FY 25.

Capex 250 cr + 100 cr in Saudi Arabia.

This is a limited summary. Management given detailed guidance in call.

9 Likes

FY25 EBITDA: 330 Cr

Therefore expected EBITDA growth for FY26 is approximately 1.6% to 14.2% over FY25

6 Likes

2 Likes