Rishi mentioned 10 to 15pct margins. And It’s not unheard of. For e.g. EMS Ltd, though in a different sector, has better EPC margins for many years. SML seems to be able to pick the orders they want, on very favorable terms.

2 Likes

Sanghvi Movers to Become a Zero Debt Company Soon, Says MD Rishi C Sanghvi in a Live Interview

8 Likes

Hi everyone,

There has been considerable reduction in wind power budget allocation. Can anyone elaborate whether:

-

Sanghvi will be affected and how significantly over the next 2-3 years?

-

They will keep growing at 30%+ EPS CAGR for comibg years due to business diversification strategies?

1 Like

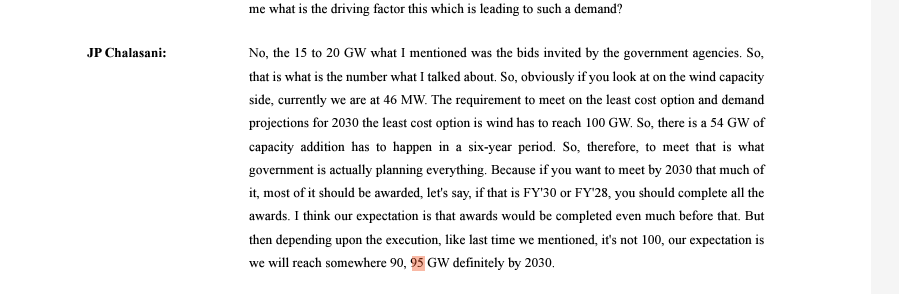

Govt prioritise Solar and Nuclear energy and not doubt about that, but 54G additional wind energy target by 2030 still intact (total 100G wind by 2030 where 46G currently installed capacity + 54G additional/new) . in Q1-FY25 earning-call Suzlon management said (refer screenshot), this 54G target is huge and we may be 5G short of target by 2030. In short, wind energy turbine suppliers and EPC players will have enough work, and the only concern is if they will be able to deliver it.

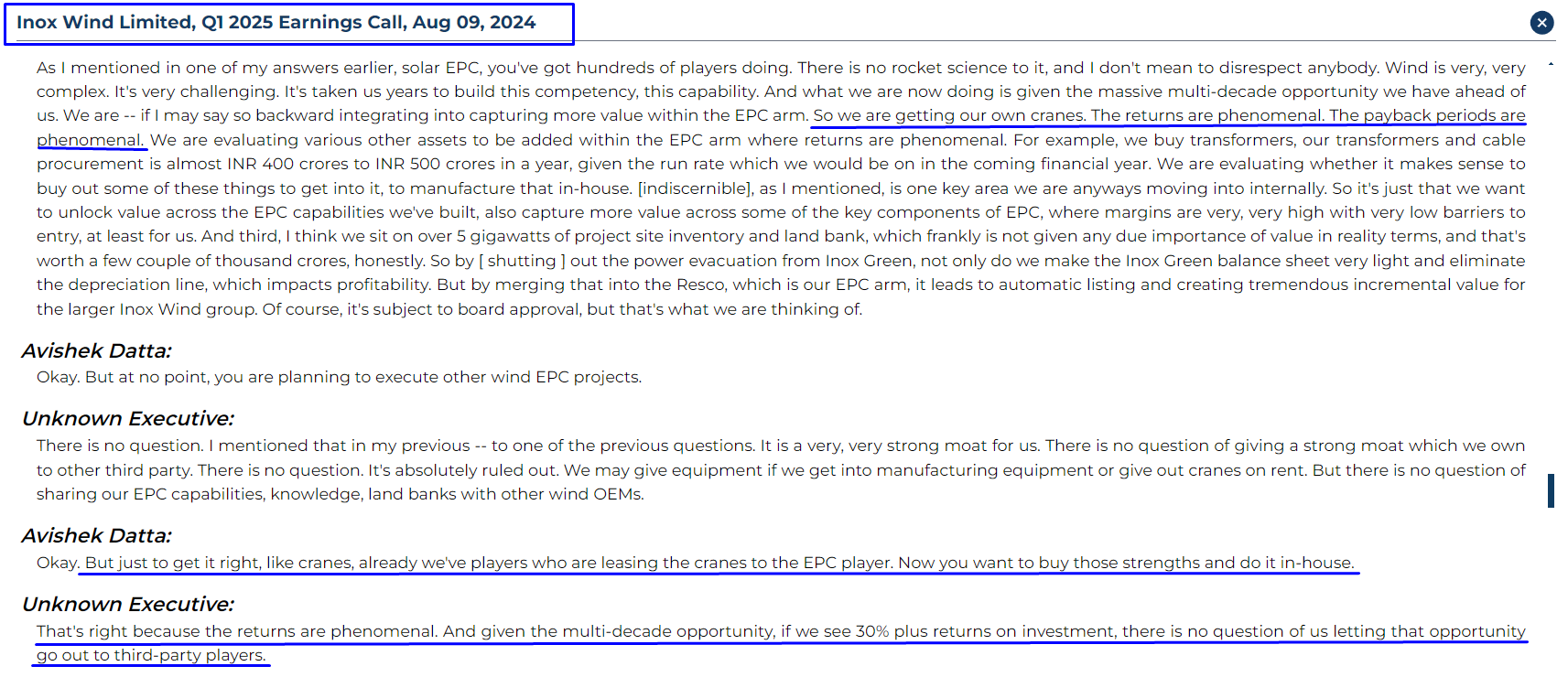

Yesterday (06-08-2024) Inox wind secured 201MW wind equipment supply from Integrum Energy, C&I order and I believe EPC work will be carried out by EPC players like Sanghvi or others

2 Likes

Q1FY25 results and Investor Presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/daa04543-547a-4b9a-accf-9dfb50e0c11f.pdf

How the mighty has fallen. Breach of the 200 Day moving average is just non negotiable, time to move on to other ideas.

1 Like

Should not you wait to hear the management side?

During the previous 2 quarters, performance did not meet expectations, leading to widespread negativity among stakeholders. Previously, the sentiment towards our company was overwhelmingly bullish. This shift in outlook suggests that the forum may be more aligned with traders’ perspectives rather than those of long-term investors.

3 Likes

Deep cyclical stock experiencing seasonality. Such a massive reaction is a bit unexpected, almost as if the market expects the beginning of a down cycle.

Looks like another bad quarter coming due to monsoons, should make this stock a value bet if prices continue to free fall. If they achieve 590 cr as per the deck, they’ll still close the year at around 18% topline growth.

The org restructuring is interesting as well.

5 Likes

Any update about the stock split company was talking about during Q4 FY24?

This fall is really baffling, have exited holdings, can’t see capital erosion. Reallocated capital.

2 Likes

When the management itself is indicating that the next quarter will also be lean, we should look for better opportunities.

2 Likes

I feel Sanghvi has become a good value buy now. You are getting the largest crane rental company in India at 3500 cr mkt cap. With 500 cr+ orders in hand and extrapolating their order book to execution in FY 24 easily 800 cr top line is doable . Yes Q2 will also be sluggish ( As we are already in August and mgmt has a fair idea ) , but looking at the bigger picture of infra growth, Sanghvi exploring adjacencies etc , I think it’s a good value buy now.

11 Likes

So this sums up for their short term performance. Any view on next year guidance? Thanks

1 Like

Friends , do you consider Sanghvi’s Management Ethical ? Does Sanghvi have a good Culture ? Are the Employees motivated ?

The contrast between the tremendous growth shown by potential clients like Inox, and the damp results and even more damp outlook given by Sanghvi could not be more ironical!**

3 Likes

Here are four important points from the conference call:

- The company’s EPC Bussiness is expected to grow by 50% year-over-year (YoY).

- The company is experiencing lower yields because they have invested in high-quality German cranes, whereas recent competitors have opted for Chinese cranes that offer higher yields but at a lower quality.

- Wind installations in Q1 reduced by 30% therefore causing less requirement of cranes in Q1.

- Multiple players tried entering into crane rental in the past like inox announced in this quarter but it has a lot of technicality which caused them to stop that vertical.

13 Likes