Strongly disagree,

Many companies like Suzlon and Inox wind are getting multiple orders almost every week…

And Sanghvi is the only Proxy to wind turbine set up ')

5 Likes

I think Margin will be reduced from the new segment. then question is - will growth remain same like their core crane business? what should be the expectation from investor point in terms of return CAGR?

1 Like

Sanghvi Movers has appointed Bain & Company Private

Limited as Business Strategy Consultant to explore growth opportunities and build the next chapter of

growth (Engine 2). Engine 2 is defined as businesses beyond SML’s core, including any global opportunities within the current businesses and will build on the company’s vision by leveraging core capabilities.

8 Likes

Today’s fall is because of one of the OEMs of Sanghvi Movers, Kato Works, which is into crane manufacturing(one business) is forming a joint collaboration with ACE to enter India market? What is the impact of this on Sanghvi’s business in short term and long term?

Kato works is a manufacturer and so is ACE. Sanghvi movers rent out the equipment.

It’s like Maruti Suzuki who makes car. They can’t be direct threat or competition to Ola/Uber of the world.

Actually it may not be even that much. In my limited understanding about ACE, they don’t manufacture what Sanghi rents out which is typically heavy lifting equipment. There could be little overlap in what one makes and other uses but ACE is definitely not in its main suppliers list.

12 Likes

Where was this information published that ACE is doing sort of JV with Kato?

I don’t understand all the fuss over margin dilution due to foray into EPC business which has lower margins than Crane rentals business. The following points should be taken into consideration.

- Margin expansion/contraction is not the only value driving factor in this case.

- Increase in ROE is possible with a lower margin business if additional Capex is not required (which is the case in EPC here).

- Rentals business has high margin but also has high depreciation, depreciation is not an element in EPC business.

- Ultimately PAT growth matters which may come from EPC without affecting the crane rentals business and without equity dilution.

The real issue though is the increase in the MD’s commision from 1.5% to 3.5%. I recently observed that the MD of Shakti Pump waived off his right of commission in the profit. Hopefully, Bain Capital would also advise the management in this regard as higher valuation would benefit both (Promoters and Investors).

12 Likes

I haven’t found it on NSE website but found few articles related to it including REDBOX tweet

1 Like

This has the exchange filing by ACE, seems discussions are going on, but not finalized. ACE is not a competitor to SM, since they are into manufacturing of cranes as of now.

2 Likes

1 Like

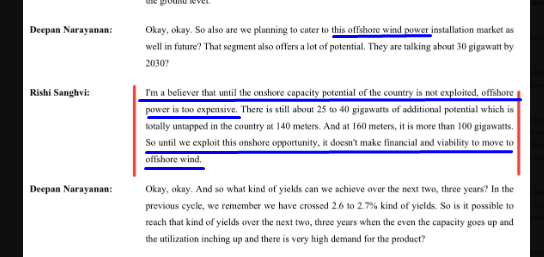

This is what Rishi said is 3Q concall about Offshore…

3 Likes

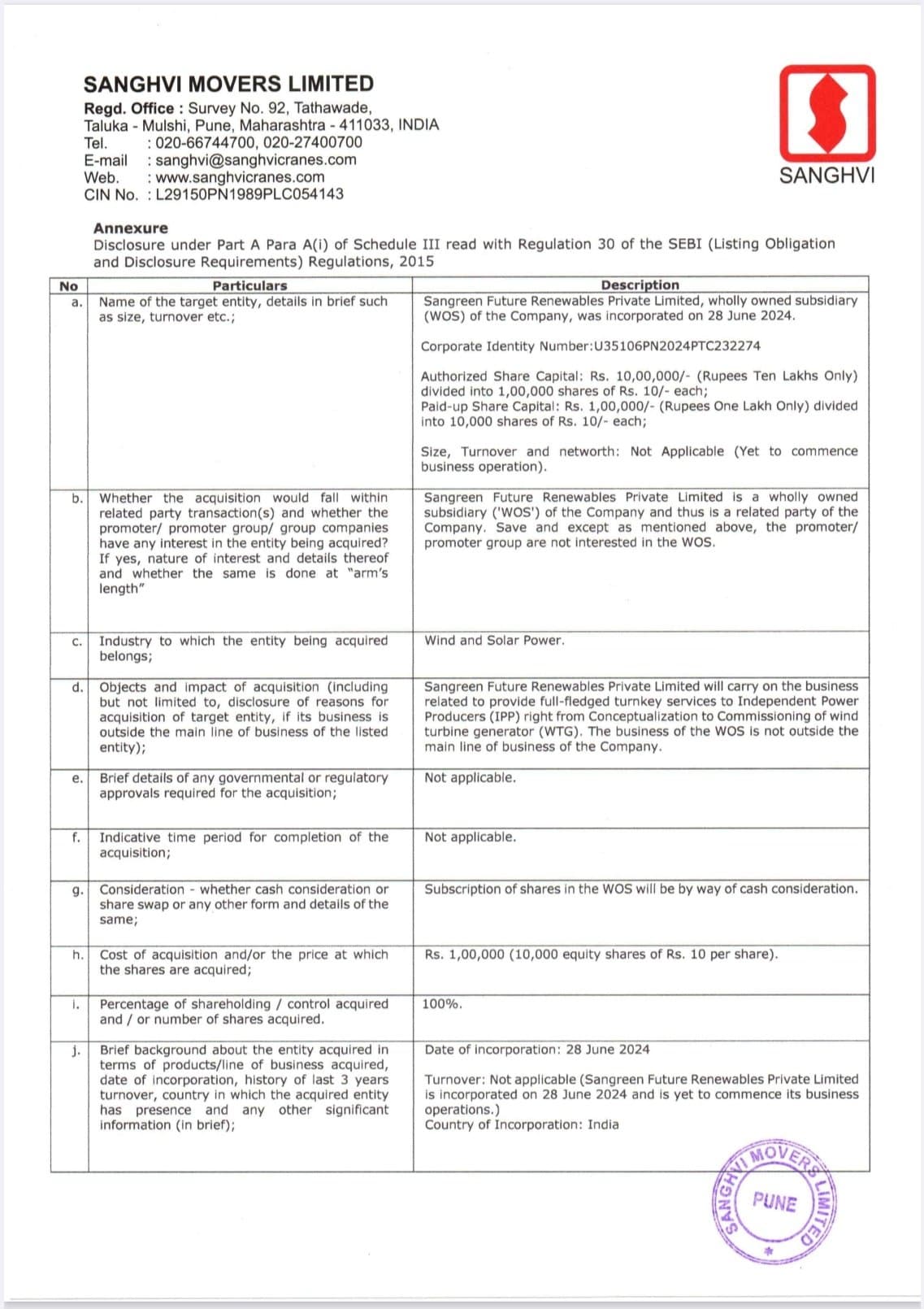

Sanghvi Movers Limited received order.

62b771f3-58f3-4396-af3d-f8de5343fe6f.pdf (712.6 KB)

3 Likes

Interview with ET NOW

-

FY 25 Rev to be between 950-1000 cr. Current Order Book 600-650 cr (all executable in FY 25).

-

60:40 split between Rental and EPC. Rental margins 60-62%, EPC to be 10-12%.

-

10 GW enquiry pipeline. Capacity Utilisation > 80% (theoretically 100%).

7 Likes

That is 400cr operating profit approx as compared to 381cr in fy24. ![]()

1 Like

that too by taking revenue and profitability, as is being guided by mgmt. for FY25. Besides, there will be capex of Rs 150-200 crores, for which they will be raising long term debt, @ around similar cost and addl depreciation cost. In all likelihood, the earnings will degrow from FY24…

4 Likes

Assuming the same NPM will remain in rental business the net profit from 600 Cr would be 600×0.3= 180 Cr and NP on EPC 400 Cr× 0.12 = 48 Cr

Total net profit in fy25 = 228 Cr. Thats 20 PE on fy25 earnings. Ignoring Capex.

I think people got injected OPM vaccine and developed a fixation around it. Ofcourse operating leverage is not in play now because of high capacity utilisation.

14 Likes

When a company like this goes under Capex, does it mean they’re spending on acquiring cranes or they’re putting up capex manufacturing?

Sanghvi mover’s Capex is to acquire/purchase Cranes.

1 Like

I don’t think they’ll make 12% PAT margins in EPC which is what you have assumed.