I dont know if something is being lost in translation, but the values I get using FCF of 9% and discount rate of 14% are very different. Guess we can agree to disagree here ![]()

1 Like

Perfectly possible what you are saying as its a cyclicality sector .Hence I am saying to gaze the business /terminal value every 2/3 years .Currently the tail wind is very strong .Please go thru yesterdays attached article

5 Likes

I’m new to this so I might be wrong. Your return numbers are for a pure equity business where ROE = ROCE. Gearing will improve your FCFE and ROE numbers. Also in such a cyclical, high growth business does DCF even work? I’d only use it for strong stable businesses with no growth upsets on either side.

1 Like

Can someone throw some light on how Tara chand infra logistics has a rental yield of 2.85 compared to the market leader who has a rental yield of 2.2?

1 Like

It was a simple example. Can do this for debt also.

Suppose 100 crores of incremental debt is taken and cranes are acquired. Assuming their is no time lag in acquiring after debt is taken and they get immediate delivery for simplicity.

From that the unit economics look like:

As per previous post, 20cr revenue, 12cr EBITDA.

Interest on 100cr according to me would be 9-12cr. Being optimistic and taking 9cr.

Gives us PBT 3cr and PAT/Cash flow of 2.25cr

But if we take into account effective depreciation, assuming 40 year life, 2.5cr will be depreciation which will be more than PAT/Cash flow. This is when we assume 9% interest on debt, but in reality is likely to be more.

Note: My personal rough calculations, might be errors

1 Like

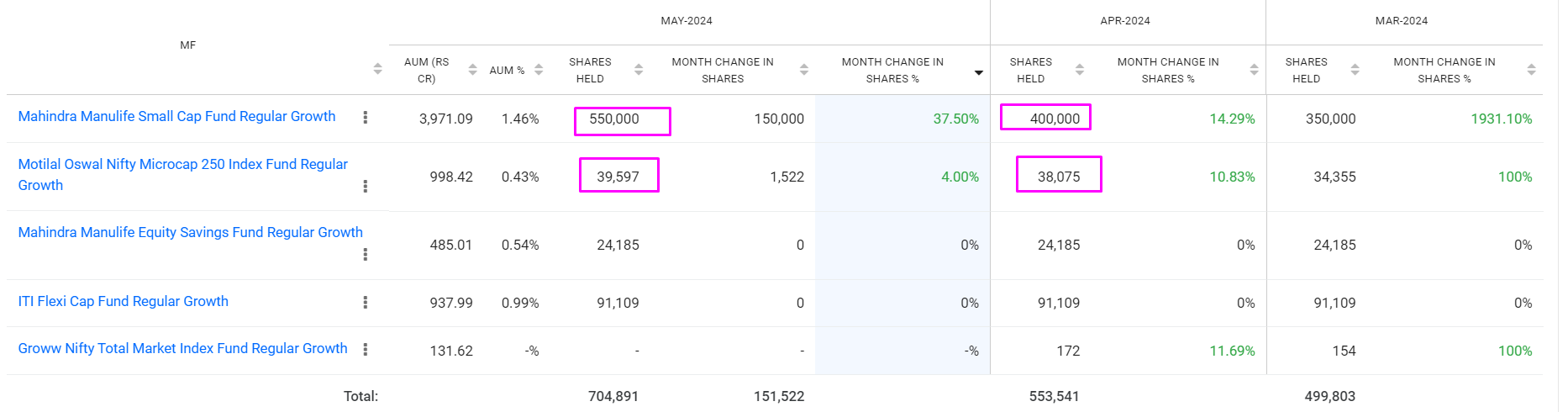

These are the turnover numbers for Sanghvi from screener -

Also, from PAT, we need to calculate Free Cash Flow to Equity, not just FCF. It’s what makes owning a bank more profitable than lending to one. When ROCE >> Cost of Debt, leveraging generates FCF towards equity since interest costs remain fixed.

2 Likes

Why use net block? Should use gross block

1 Like

Maybe because the crane assets have pretty good resale value upon liquidation and quite long working life etc.

Disc: invested

1 Like

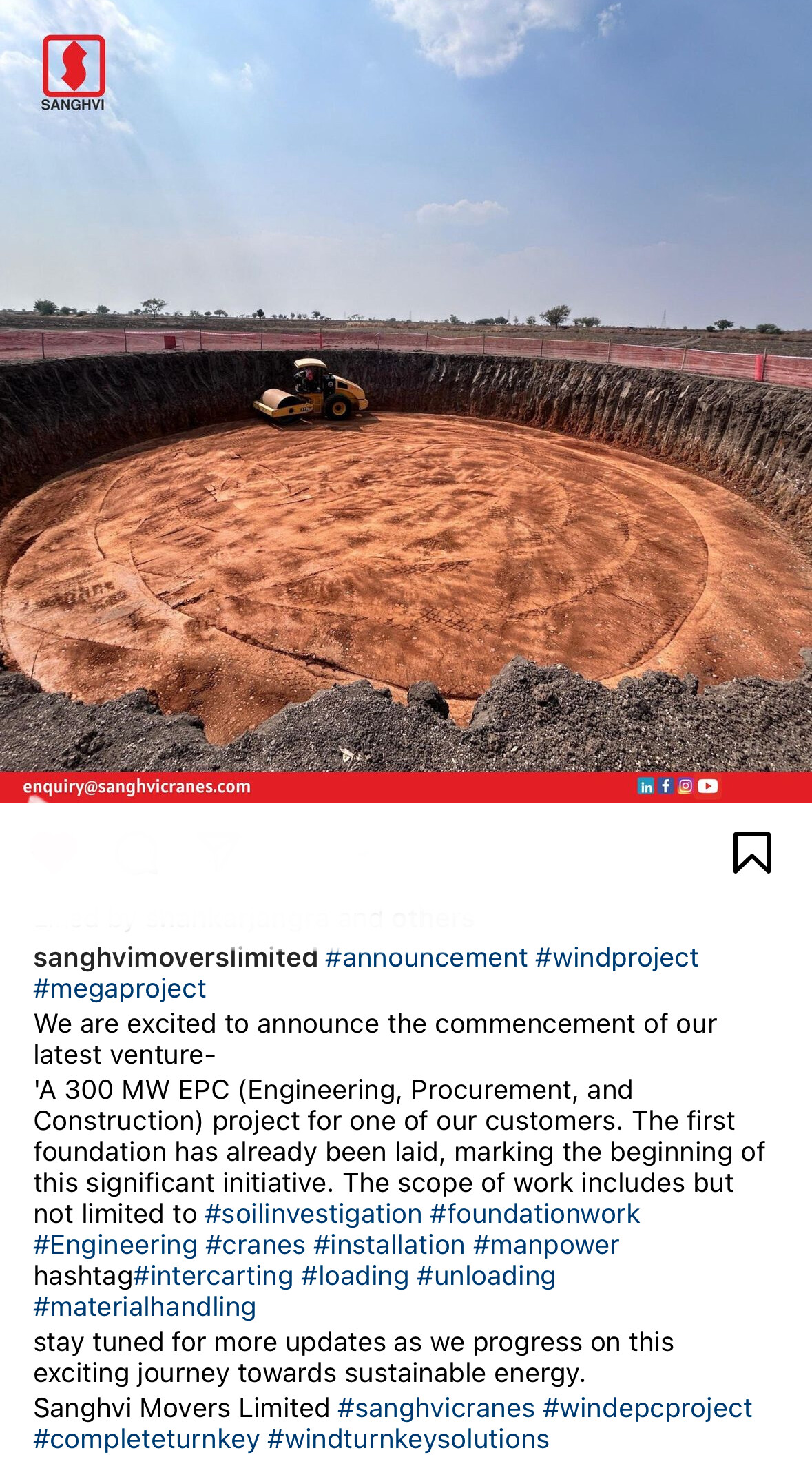

Watched the interview with NDTV Profit and read the concall transcript. While one understands that mgt does not provide forward guidance, they keep alluding that EPC will contribute to 30% of topline going forward. With Rishi Sanghvi mentioning that the EPC life cycle would take approx 2 years for completion and with a minimal base of 25cr for EPC business in FY23-24 not sure how much can one extrapolate revenue from the EPC business for FY 24-25.

Assuming continuity in govt expansion plans of renewable energy, would a conservative estimate of the crane rental business of 800 cr be reasonable and maybe a 50-100cr (better to assume the lower end) from EPC for FY24-25?. With an assumption of 20% EBITDA margins from the EPC business and a 55 to 60% EBITDA margins from the existing crane business, would be best to expect a blended EBITDA of 50% approx overall on a possible topline of 850 crores. Again, without much of forward guidance on the revenue break up, order book break up and timelines for the order book to the executed, assumptions are more speculative than with a reasonable estimate.

Disclosure: invested from lower levels.

4 Likes

If the current Government is elected back with majority then the existing power policy will continue and will get further boost up. Business model of the Company and the rgoernment policy gives clear a road ahead for for next at least 5 to 7 years. The total power demand as on date is expected to increase by at least 50% in next 8 to 10 years i.e we will have to create power infrastructure of around 50% in next 8 to 10 years (50% of what has been created during last 75 years.).

The Company will not only be beneficiary of CAPEX in power structure but also of expansion in infrastructure, mining, Cement, Iron & Steel,Power, Fertilizers, Petrochemicals & Refineries, Metros (underground as well as elevated) and Windmill sector. etc.

Largest Organised listed player in India (Sixth largest in world) with experience of 35 years and satisfactory track record of Corporate Governance.

Apart from this foray of the Company into EPC segment is a sweetner.

EPC is very risky and working capital intensive business but Company has decided to restrict its EPC business only for Wind Power and asper news article there is already dearth of EPC players in Wind segment. Further Company will be entering EPC business along with its Crane rental business which mitigates the risk overall business risk.

Company business model makes EPC asset light, low work capital requirement and faster payment mechanism.

Company has guided for 10x growth in EPC business to Rs 250 Cr with margin of around 13%.

Some highlights of Concal:

“So, we have a very healthy outlook for the EPC both on the project and wind side. And we expect our revenues contribution from the construction from the wind and project side to have a significant revenue contribution this year”

“See we already disclosed the necessary order that we already backed to the stock exchange. And based on that intimation, which is already circulated, we estimated to get a revenue of between 200 crores to 250 crores from the EPC business.”

Sham D Kajale: “See it is slightly working capital intensive business, asset light, but what is happening we are tying up this business along with the crane business and we are working, taking the orders based on the 30 days credit period. So, if there is any delay happens with respect to EPC related business, we have option to close down the crane operations. So, that is the advantage that we have so, that our working capital should not get blocked.”

Okay. So, till date whatever EPC business we have done has had a zero drawn on our working capital because we are getting paid within 30 days from our customers. So, that is a unique way in which we have approached the EPC business. Although our margin is low and it is working capital intensive, we have been able to mitigate those challenges?

Sham D Kajale: Last financial year we have paid cash credit interest of Rs.1,62,000 on a cash credit limit of 100 crores that shows how judiciously we are using our working capital limits."

Disclosure: Invested from lower levels and added during current fall. Will add more post elcetion results as that will be a critical aspect for holding stock for next 4 to 5 years

12 Likes

I think that is the difference between cashflow in hand( from operating received after all expenses Inc tax) and profit based on accrual principles (which are accounted this year,but yet to recieve,may be accounted as receivables)…Cash may be received at later stage…But profit is accounted this year

1 Like

Why this way because they make yearly or multi-year contract with suzlon kind of companies ?

Difference is due to depreciation, Saghvi movers have huge depreciation expenses. Depreciation is an accounting expense not a cash expense. So, the cash generated is far more than net profit in P&L. This is what made me invest in saghvi movers during 2019 to 2020 at an average price of 80. In P&L they are making loss but generating cash and reducing debt during that time.

Disclosures: No holding exited all at above 600 and made huge profits

8 Likes

Patience needed. It has moved 32% in YTD and 127% from last 1 year, 425% in 2 years timeframe. Wait for the needle to move if you are recent entrant.

5 Likes

I think they are moving to EPC segment then does it still make sense to freshly invest or remain invested?