Hello, Sanghvi is different from Ace. Sanghvi is more of a distributor of Chinese equipment into India primarily catering to the wind sector. On the other hand, Ace has their own brand of cranes which has gained traction due to the infrastructure push. Ace is also manufacturing higher tonnage cranes now. Ace is making backhoe loaders which so far has been dominated by JCB and they intend to gain market share here. They also want to export these backhoe loaders. Also the return profile of Ace and Sanghvi is very different. Sanghvi has operated on low RoE in the past and also debt however Ace is comfortably 20%+ RoE and even higher RoCE and a net cash balance sheet.

6 Likes

Concall Highlights Q4FY24

- 334 Cr capex completed in FY24, added 34 cranes and 44 other equipment.

- Sold 32 cranes in FY24 and generated profit of 18 Cr.

- 31st Mar 25, fleet of 336 cranes ( 2490 Cr)

- 18th Apr 25, Order Book 426 Cr ( Cranes + EPC )

- Yield to be remain between 2-2.2% in FY25.

- 250-300 Cr capex for FY25 - should be done by Dec 24

- EPC revenue significant contribution for FY25 ( 200-250 Cr) , 10x of current

- Ebidta to go down by 2% for crane business.

- 82-85% capacity utilization.

- No forward guidance for sales.

- Order Book 300 Cr → 620 Cr ; 426 Cr → extrapolate

- Asset gets freed in 4 yrs, sell the asset in 40-50%.

- Capex will be funded 70% debt, 30% internals.

- Would like to keep cash on hand.

10 Likes

I read somewhere that this 250-300 Cr capex is aligned towards crane business , as Rahul pointed out that 100 Cr addition of gross block gives an additional PAT of 7 Cr than on an 300 Cr capex the PAT growth is 21 Cr . This over a base of 188 Cr - FY 24 bottomline is just 11% PAT growth - (given the utilization and yield remains at current level) in upcoming FY from the core business , EPC excluded . Can someone help me understand what am I missing out ?

1 Like

EPC guidance is 200-250 Cr, which will also contribute to the PAT plus this is order book as start of this year, company will get more orders eventually.

7 Likes

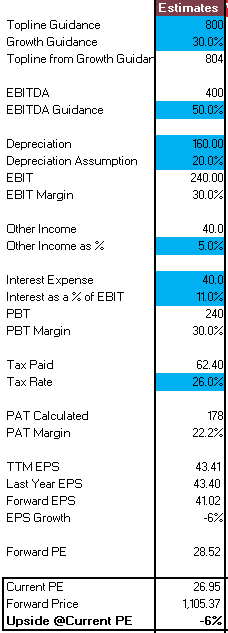

Some macro thoughts + my very basic estimation.

- EPC dhanda will lead to further margin contraction. Stocks usually get positively re-rated when two triggers happen - margin expansion + growing volumes. Given only one trigger being hit next year, I think we can expect some consolidation after the stock settles from this knee-jerk reaction we’re seeing

- First order thinking would suggest some apathy towards the minority shareholders when management hikes the incentive to 3.5%. Second order thinking would suggest them seeing higher EPS in the future in a highly cyclical business

- A very conservative estimate shows EPS decline by 6% - I don’t think it’ll be anywhere close to that - but it helps visualize some margin of safety at current PE levels. Lower tending PE re-rating will throw this out of the window

- It’ll be interesting to see interest expenses over the quarters since the co is looking to gear up

- The stock remains a broader proxy to the infra theme. The “extrapolated” topline is also very conservative - unless something in the system breaks, we should be well beyond that

9 Likes

Rishi Sanghvi Interview with NDTV Profit

-

EPC to contribute 250-300 cr Revenue. Margins of 30%. During the call yesterday Sham Kajale mentioned margins of 23% stating that they are getting premium margins because they were first movers in Wind EPC. Management expects margins to contract over the long term.

-

2 GW order backlog. Management indicating FY 25 Rev to be in the range of 850 cr+ current order book is 426 cr as on April 14th, 2024. A split between the Rental and EPC business would be helpful but management not sharing this info at the moment.

-

250-300 cr CAPEX may be revised upwards depending on demand.

-

Management commission one time due to exceptional performance in FY 24. FY 25 commission will depend on performance in FY 25. My view expect another commission in FY 25 but it’s a non issue looking at the larger picture.

10 Likes

Sir, Do you still believe these numbers are achievable post the concall and management commentary?

You had assumed a revenue of 1071 cr. However management is guiding for a revenue of 850cr+. Even in optimistic scenario, it might not cross 1000 cr.

Also management has guided for the yield to be in the range of 2 to 2.2%. Assumptions were it will go higher given the supply constraints. On top of that margin contraction because of lower margin EPC business. Would like to know your opinion and any change in the calculations if you have done them.

4 Likes

Personally expect revenues to be north of 850 cr and also expect yields to be better than 2.2% currently. Although installations need to pick up 275 MW in April was a slow start.

3 Likes

@First_Principles Very nicely captured .

I maintain my stance that the PAT of Sanghvi movers is logically and legally as per rules deflated (aggressive depreciation )

•The right way to see the valuation is Cash PAT multiple and not PE multiple .

•Even in Cash Pat Multiple the Valuation is deflated as assets are depreciated in circa 5 years or so whereas assets have life of 25/30/35/40 years .Recently they sold a crane of 1962 !!

•Hence better to calculate the life time value of these assets (2490 Cr is Gross Block ) which has huge earnings capacity !

First way (my way –crude approach) :

1.The future value of 2,490cr with a 15% annual yield (they now get 24% )over 25 years is approximately 81,574 cr

2.Present value of ₹81,574 crore after 25 years with an annual inflation rate of 6% is approximately ₹18,998 crore.

Second way (traditional way –DCF approach):

•Discounted cash flow (DCF) of an investment of 2,490 Cr with a 15% per annum discount rate over 25 years and a terminal value growth rate of 2% is approximately 17,386 Cr

Current market cap is only 5300 cr .

What can go wrong – Have taken yield at 15% which is 15/24 =63% capacity utilisation .Though currently for last 3 years its at an average of 80%+ it can be much lower than my assumption for longer period of time .Hence I can be completely wrong .

Will calculate this years (24-25) financials and share on Monday .

14 Likes

I think Sanghvi movers investor concall was not well planned, the message passed was wrongly interpreted by most.

The positives I picked up in call is

- pricing power (tagging EPC with credit period and saying would stop giving cranes )

- pay as you grow model -capex in last 3 years always increased by board -same may continue

- % mix changing for higher cranes will lead to higher yield (my guess )

- 77% of gross block is new cranes

- check past order book increase between 1 year period ,gives indication revenue would be close to 900cr

The company which will grow minimum at 25/30%+ is available at Cash Pat multiple of 14 in this bullish market

14 Likes

Your valuation calculations are really appreciable, though holding for long term, had difficulty to calculate the valuations.

1 Like

thanks for the calculations which look very logical to me. How would you consider heavy cyclicity in Wind Energy in these calculations . There could be serious slow down after 5 years which has serious impact on Cash flows of the Company for many years with cranes lying idle. (the way it happened during 2018 to 2021).

6 Likes

While I appreciate the thought process I feel discounting at 6% inflation rate makes no sense. Let me ask you a question, would you invest in equity of your expected ROI is 6%? Answer is no you can literally get more in FDs. You need to discount it either by the cost of equity (different ways to calculate) or the XIRR you aim to make on your investment and then see the PV.

Also, it is not like the 15% flows straight into bottom line, at 60% EBITDA margins, only 9% would go into bottom line excluding depreciation and interest for now.

1 Like

The business looks interesting to me but the problem I have with this business:

Let’s try and break down the unit economics of the business:

We invest 100 crore in cranes today and get delivery.

At 20% avg yield, we have a topline of 20cr. EBITDA Margins of 60% means EBITDA of 12cr. For simplicity, lets ignore other income, interest as they are not relevant here.

Assuming a 25% tax rate, we end up with approx 9cr of PAT.

If a business invests 100cr and earns 9cr, is it really a great business? Also, this excludes the REAL depreciation. Even if we assume a actual life of 40 years, implying dep of 2.5% per annum, this will give us an effective PAT of 6.5cr.

So it is not a bad business, but does it deserve high valuations? Wind EPC is one business to see how they can execute.

Note: These are all rough calculations, let me know if there are any errors here

7 Likes

Given the current demand scenario I don’t think it will be difficult for the management to get a 20-30 bps increase in monthly yield over the course of the full financial year. If they manage a 2.5% yield you get revenues of 720 cr from the crane rental business. They are being conservative in their guidance which is good. Again I could be wrong but I don’t think growth of 20-25% in the rental business is an unreasonable assumption.

2 Likes

I am quite surprised by Sanghvi Movers’ gross yield guidance of 2-2.2%. Tarachand Infra reported average gross yields of 2.85% in FY24. Tarachand has no presence in wind sector yet (They are entering in FY25) whereas about 50% of Sanghvi’s business comes from wind and wind is supposed to have very good yields across industries.

Also, while I buy their rationale of increasing management commission in a good year to compensate for bad years where management remuneration did not go up, the same could be said about dividends? From FY18-FY21 there were zero dividends. So why are they over-compensating the promoter shareholders while ignoring the minority shareholders?

This and the overall defensive tone of the call was surprising and disappointing to an extent.

Disclaimer: Invested in Tarachand. Tried a results trade in Sanghvi expecting a good set, hit my SL and exited. No reco.

12 Likes

i didnt assume 6% ,please refer valuation in point 2 ,i have used 15% for 25 years with terminal value of 2% pa ,present mkt value comes to 18998 cr !

1 Like

I appreciate your thinking .Even if we assume that each asset of 100 cr yields 9 cr pa (though added cranes doesnt increase expense proportionately ) ,the value of gross block of 2490 cr (77% new cranes ) with a 9% per annum discount rate over 40 years and a terminal value growth rate of 0% is approximately 27,244cr !!Todays market cap is 5300 cr only !

Discounting for such long period of 40 years have risk ,hence I earlier used 15% pa for 25 years and terminal value of 2% .

In good companies like say Unilever for Management Accounting, they used to work on ‘Remainder Life Replacement Value. While for financial accounting book value was taken! If one can do that ,the difference will be stark ,suggest we think like that and then let’s hear others views here .

I am only saying we think like business owners/ promoters who is increasing capacity slowly but regularly (learning from past mistake) as he cannot exit the business .We as investors have an added advantage over him .We know there is immense life time value with a huge tailwind (atleast till 2030 ) .We dont know the exact value or the exact tail wind when it can slow down ? Hence my 2 cents is :we as long term value investors see value in it ,stay invested and exit when tailwind of sector stops .

Disc: Views may be biased bcos of my holdings please do your own due diligence /scuttle butt

4 Likes

Thank you for your explanation. I have 2 major caveats to your view:

-

You are using 15% yield but that is just the revenue it generates. To calculate value, we need to see the amount of free cash flow it generates and not the revenue. As mentioned in my earlier calculations, a simplistic cash flow comes out to around 9% (this may actually go a little up or down with leverage but ignoring that for now)

-

I feel 9% discount rate is quite low. I personally will not invest in a stock if I feel it will give me an average return of 9%. Using XIRR method, i would discount at at-least 13-15% which is the minimum return I feel is worth investing for (Usually I aim for even higher but since we are talking very long term I feel 13-15% seems like a reasonable discount rate)

Note: Again my own personal rough calculations and views. Please let me know if there are any errors.

3 Likes

On your point 1 & 2

point 1)The discounted cash flow (DCF) of an investment of 100 with a 9% per annum discount rate over 40 years and a terminal value growth rate of 0% is approximately 1,103

point 2) we are valuing an assets residual value with 9% return basis (and not our return expectation ) .The way I think is Imagine buying a house which will give rent for 9% for 40 years after which the building will not last .Today that house we are buying at 1 cr ,in 40 years the rental of 9 lacs at todays price is 11 cr (hence gross block of 2490cr at todays price is 27400 cr ! ) .

What is the problem in the above view is? 40 years is too long period hence bring it down to 25 years .Lets be conservative and apply further probability to it (whatever we think ) ,still it would be higher than todays market cap .

Whats the risk ?no one can predict long term .Hence we need to keep on evaluating /calculating terminal value every 2-3 years

2 Likes