No Concall was conducted this time after Q3 results. But an interview with Rishi Sanghvi was there instead of it.

No Concall was conducted this time after Q3 results. But an interview with Rishi Sanghvi was there instead of it.

Thank you Mr. Wagleji for the update and valuable inputs. It’s good to see big investors like you still invested and having conviction in this company. Gives us smaller investors a lot of confidence. ![]()

![]()

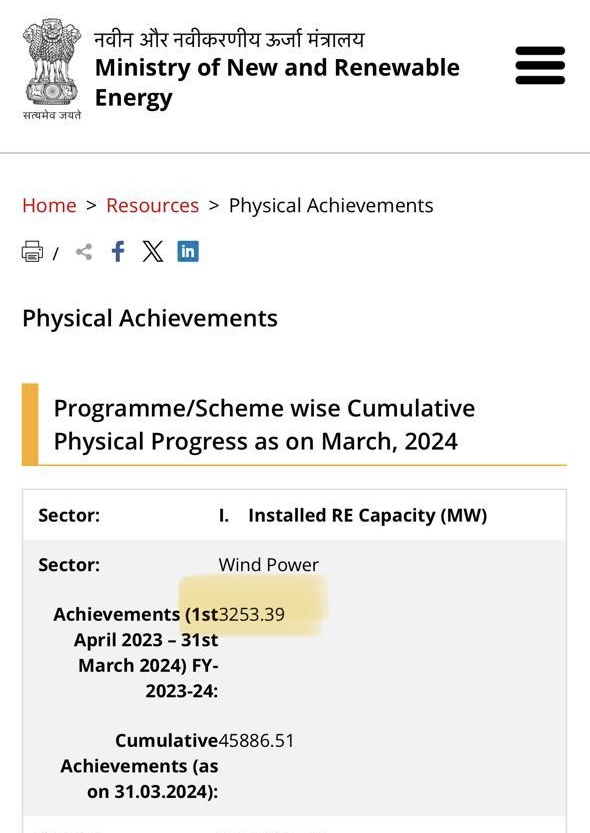

Wind installation picking up pace:

April- June : 1139;

April- July : 1306;

April- August : 1456;

April- September : 1551MW (monsoons)

April - October: 1659

April - November: 1930

April- December : 2103

April- Jan : 2336

April-Feb : 2520

April-March : 3253

Sir, which website is this?

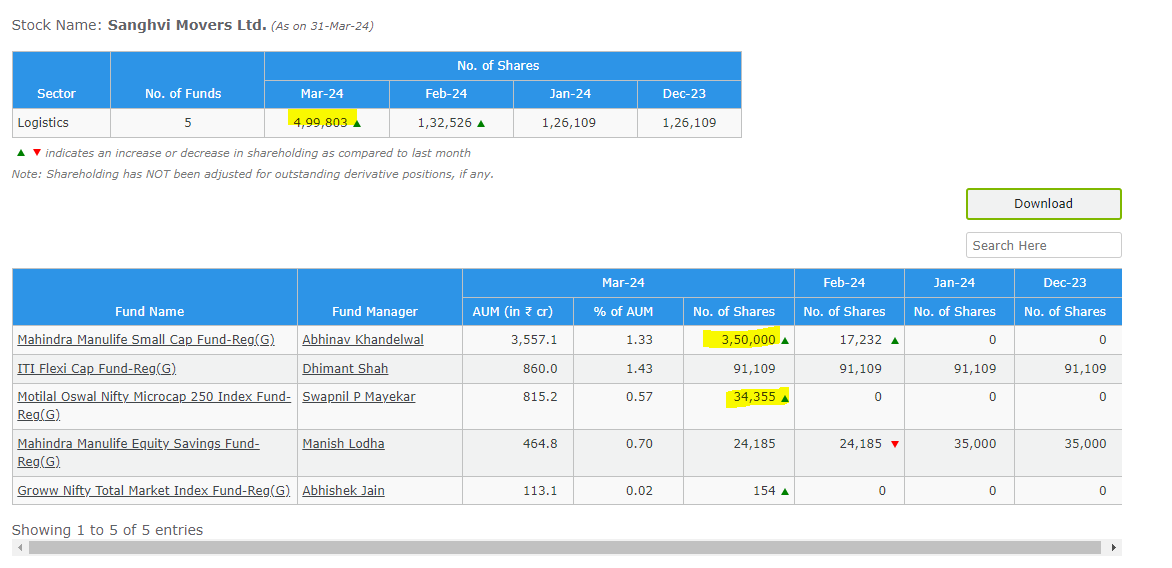

Rupeevest

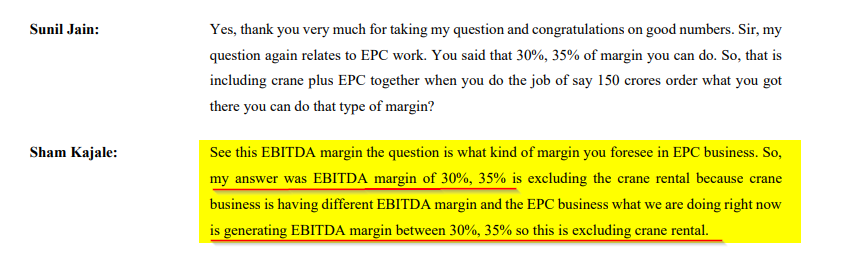

Hi Aditya Ji, Management in Q1 FY24 Concall mentioned that the EBIDTA Margins for EPC business would be in the range of 30-35 %, any specific reasons you have calculated using just 12% margins?

If we take the lower end of the mgmt’s EPC margin guidance, the FY25 Pat could be ~ 350Cr. Please share your thoughts

Yes, although i completely respect the experienced views of Mr Adityaji, even i was wondering the same. Margins in EPC could be higher as spoken by Rishiji in concall.

Awaiting your reply Mr. Aditya ji. Thank you

Generally found EPC to be a topline heavy business with slimmer margins of 12-14%.

I will be happy to be proven wrong and I hope Sanghvi Movers does earn margins that they have stated. In the meanwhile I wanted to be conservative in my estimates.

You are correct. Mr. Rishi Sanghvi himself said that EPC margins will be lower but definitely in double digits. See from 6:45.

Wind installation picking up pace:

April- June : 1139;

April- July : 1306;

April- August : 1456;

April- September : 1551MW (monsoons)

April - October: 1659

April - November: 1930

April- December : 2103

April- Jan : 2336

April-Feb : 2520

April23-March24 : 3253

1April24-30thApril: 275

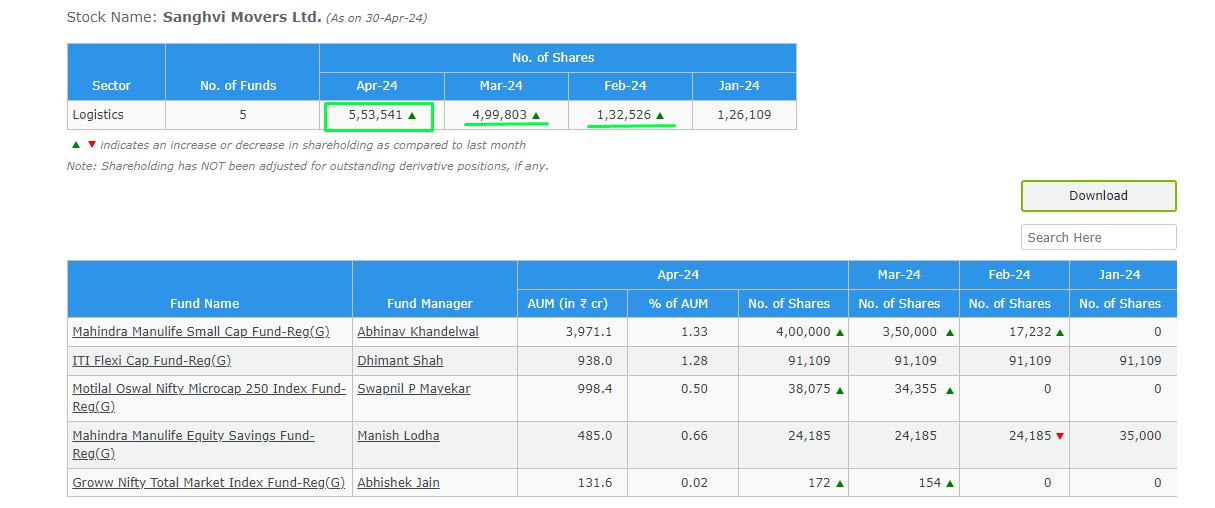

Hi,

Thanks for bringing this data in notice.

Which tool shows data in this format?

Thanks & Regards,

Sushil

This website - Stocks held by Mutual Funds | RupeeVest

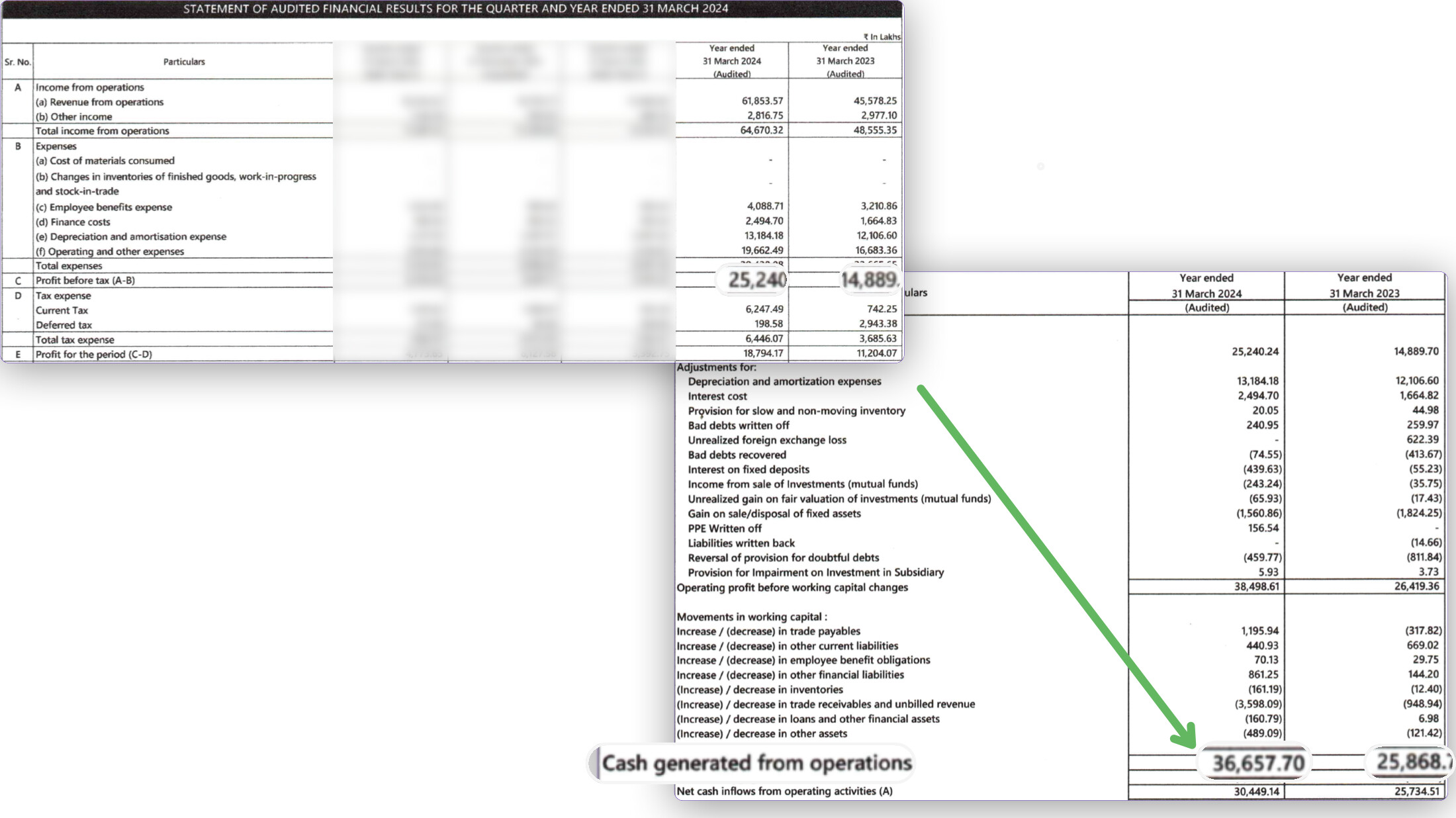

Result Published

Revenue - QoQ - Flat, YoY - +30%

EPS - QoQ -22% (negative) - YoY - +40%

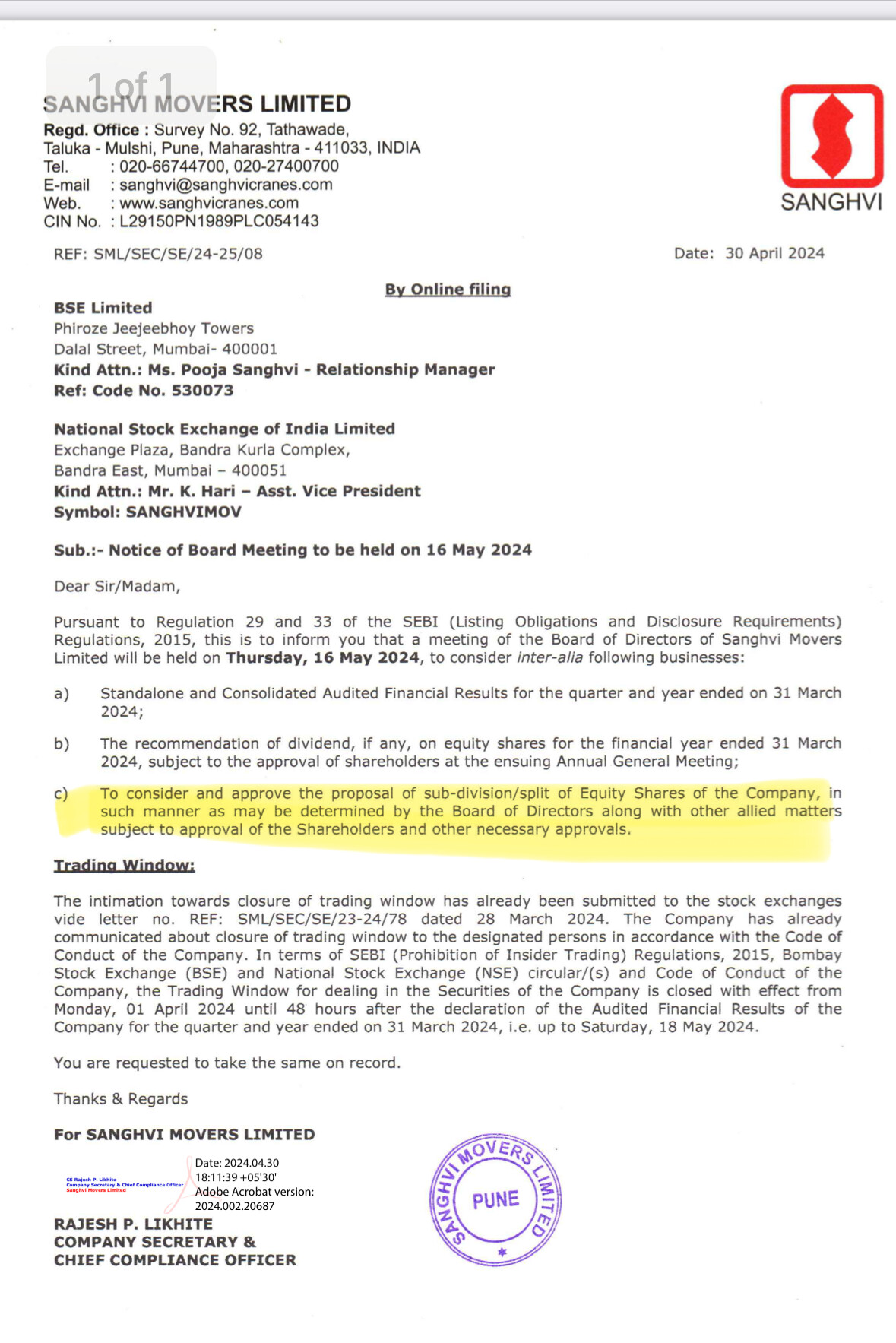

Stock Split announced - 1:1

https://www.bseindia.com/xml-data/corpfiling/AttachLive/d744c954-ac5c-4187-b010-e7055826d14a.pdf

5 Key Points from the Audited FY24 Results of Sanghvi Movers

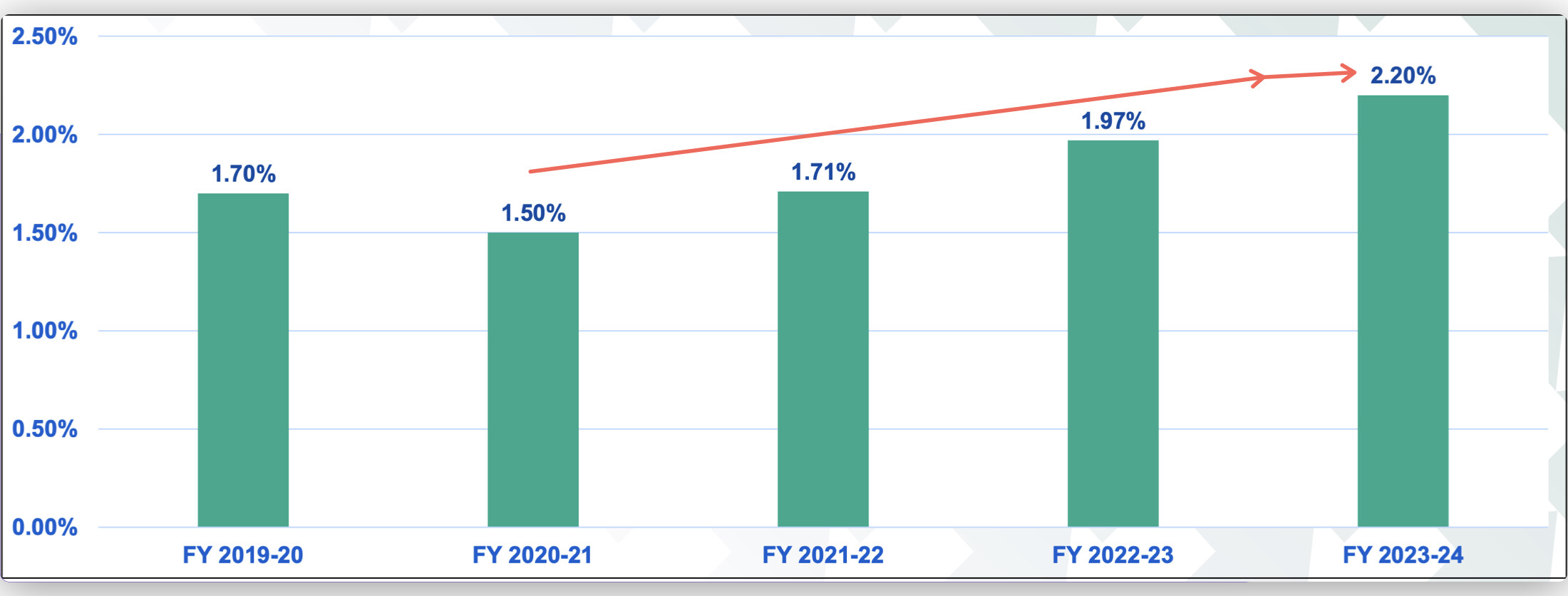

Of Course, Quarterly numbers have limitations and maybe the next quarter Will see higher yields, who knows, I don’t.

Just for newer investors : Increasing Yields boost profits disproportionally. Yields are basically pricing of the cranes, so a higher yields (rent) means higher Revenue without the higher expenses. That’s why all of yield increases flow to the bottomline. Also, the primary reason for the disproportionate growth in PAT vs Sales (talked more about below)

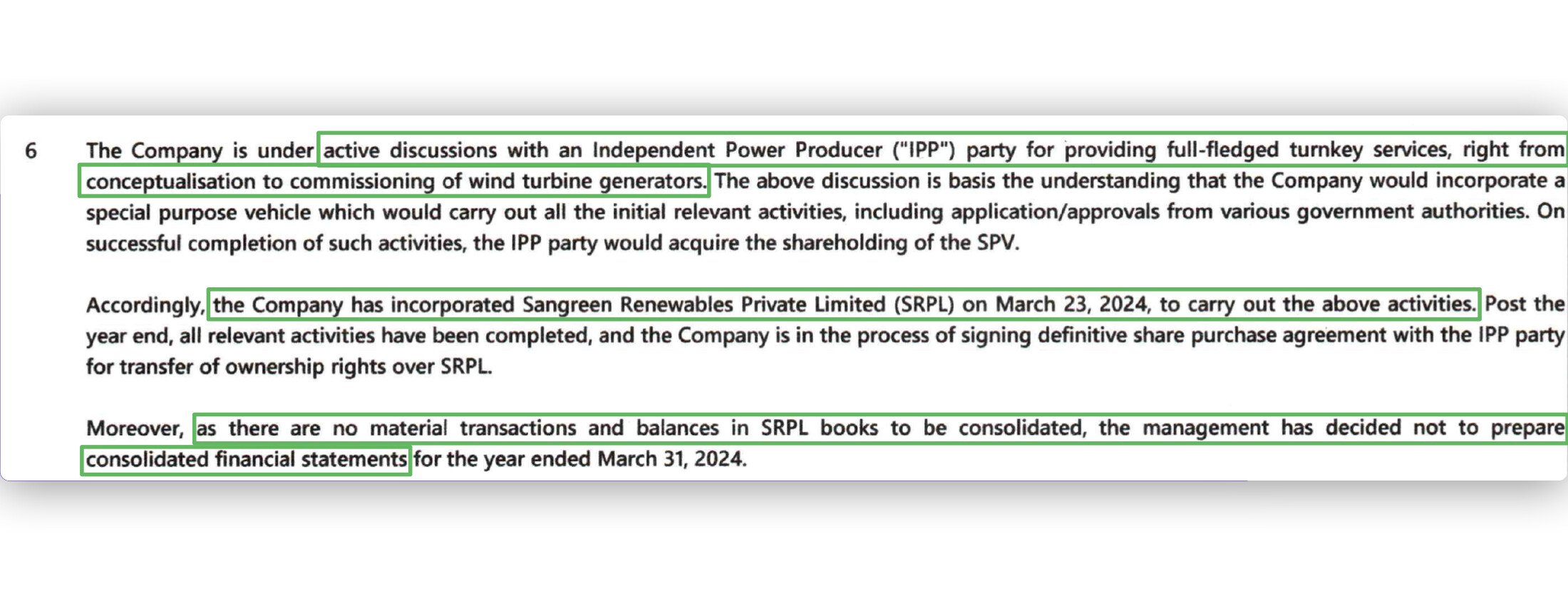

Sanghvi is taking on more risk by SPVing around. I’m guessing this is part of their EPC Order book. We don’t know how this will fare but in this quarters con-call I’m sure there will be (or should be) questions around this.

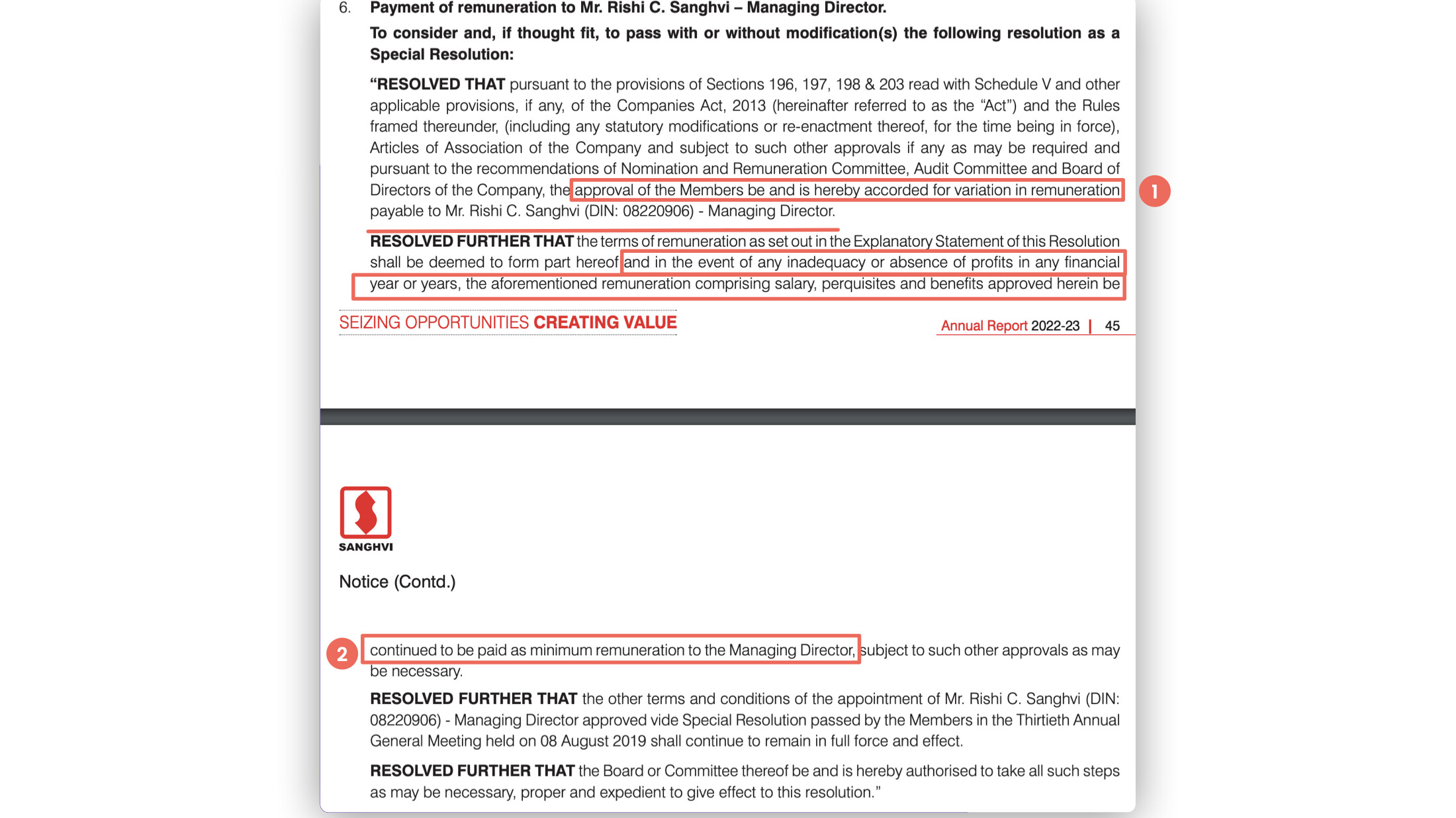

I would assign this point a very low score in terms of importance at this point. In FY23 AR, a special resolution for MD compensation was passed (need to verify), wherein (if my interpretation is correct) any “variation in remuneration” was approved. Maybe this is a business as usual type of approval but the language seems odd. Although, total compensation to MD is ~2.5-3% of PAT so not losing sleep over it.

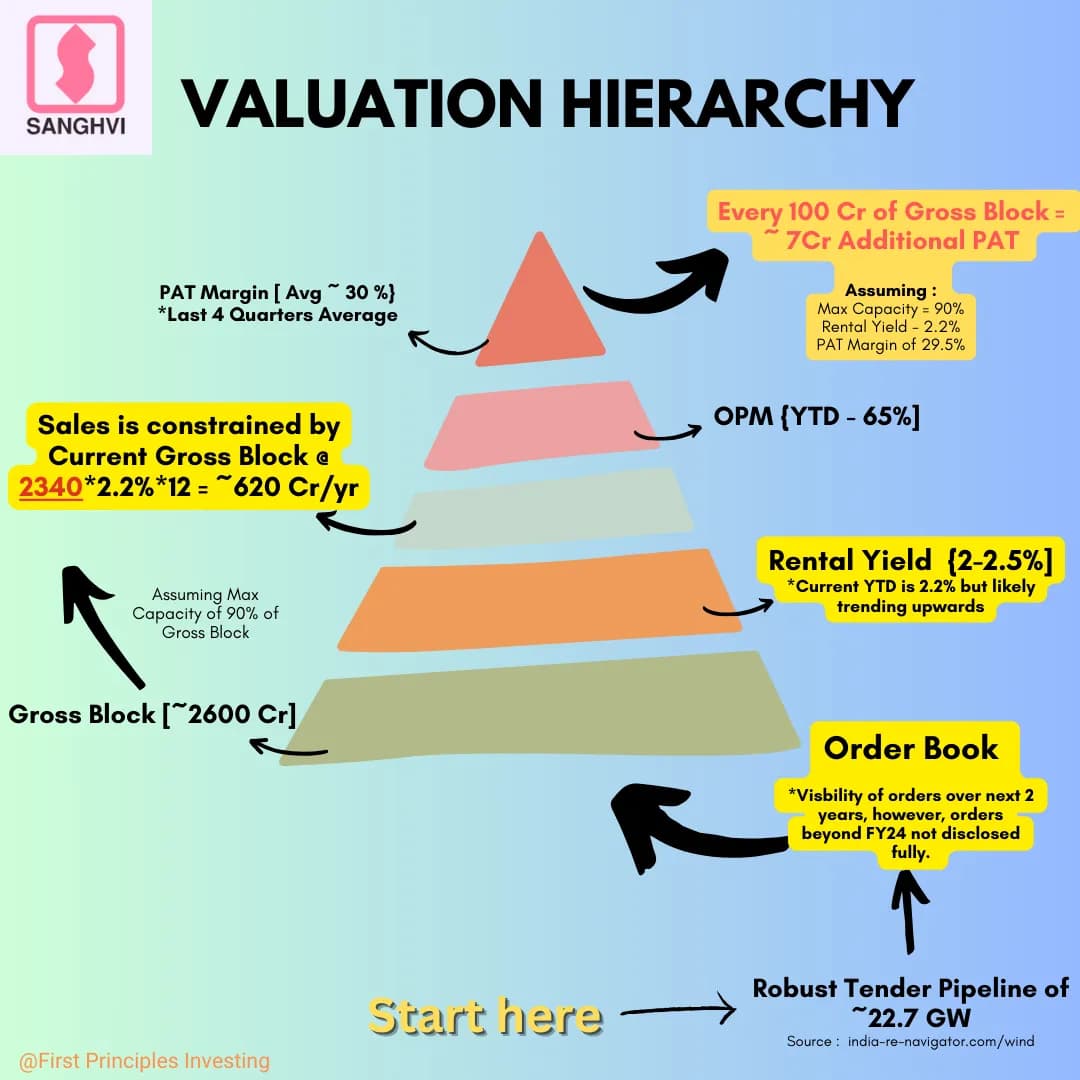

This is going to be challenging because every 100 Cr of Investments in Cranes is capable of growing PAT by ~7 Cr (check Diagram below).

so, if the co’ were to rely solely on the Crane Rental it would have to invest ~ 700 Cr. That seems unlikely.

This is why they’re also focusing on the EPC book, which doesn’t require as much capital and is incidental to its existing business. Kind of like, I have Apple orchards, might as well make Apple pie.

But we’ll see how that goes.

Hope this is somewhat useful. Thank you. Please feel free to add/change/correct.

Did you try comparing Sanghvi to ACE? or anyone following this thread?