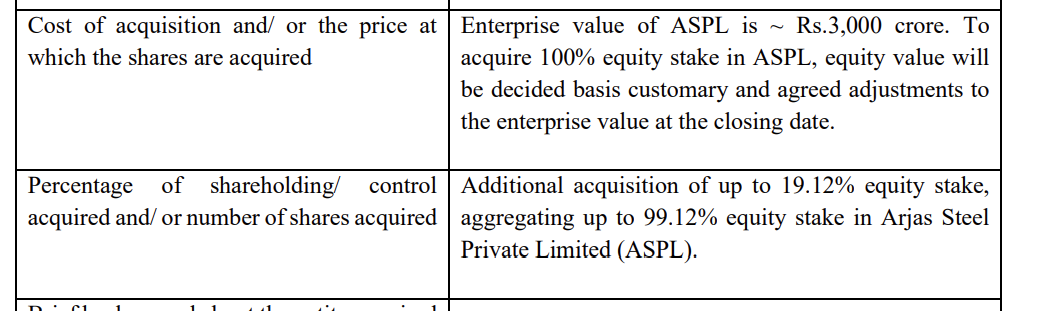

Did they randomly change to buying 100% of Arjas; instead of the 80-20 split between company and promoter?

1 Like

will proposed tax, will get implemented as it is?

or congress supportive sandur will be able to get it diluted?

and if gets implemented, Can sandur survive this abnormal tax hike?

will arjas offset the loss in operating profit due to tax?

@ayushmit what are your thoughts about this proposed tax ? Will it be a major dent on the profitability given this legislation

The Karnataka government has proposed the Karnataka (Mineral Rights and Mineral Bearing Land) Tax Bill, 2024, which aims to introduce taxes on mining operations. Here’s a summary:

Summary of the Proposed Tax:

-

Tax on Mineral Rights: The bill proposes to levy a tax on the exercise of mineral rights. The tax rates vary based on the type of mineral; for instance, iron ore, manganese, and bauxite are proposed to be taxed at ₹100 per tonne, copper ore at ₹50 per tonne, limeshell at ₹20 per tonne, and gold byproducts at ₹50 per tonne. Other unspecified minerals would be taxed at ₹40 per tonne.

-

Tax on Mineral-Bearing Land: Additionally, there’s a proposed tax on land that bears minerals, which would also contribute to the state’s revenue.

-

Revenue Expectations: The government anticipates generating approximately ₹4,207.95 crore from the mineral rights tax and an additional ₹505.9 crore from the tax on mineral-bearing land annually.

-

Impact: This taxation is expected to significantly affect companies like NMDC Ltd., Vedanta Ltd., and Sandur Manganese and Iron Ores Ltd., which operate in Karnataka. The increased cost could potentially lead to higher iron ore prices and affect profitability.

Applicability Date:

-

Retrospective Effect: The tax on mineral-bearing land can be applied retrospectively from April 1, 2005, while the tax on mineral rights is applicable from January 12, 2015.

-

Implementation: Although the bill has been tabled, the exact date for when these taxes will start being enforced post-passage is not explicitly stated, but it’s anticipated that they would commence once the bill becomes law. However, posts on X suggest an effective date of April 1, 2025, for at least some aspects of the tax, like on iron ore.

Since its applicable retrospective from 1st April’ 2005, there will be huge payout, we need to wait once its get passed and what are payout options to companies, there will be huge impact on cash flows.

Impact on Sandur

Management - no press release by management on impact of this act, what can be payout and impact on cost increase, what is %age of this cost they can pass out, final profitability impact, cash flows and impacting future strategic plans.

1 - Cash flows - we need to wait for further details of acts to come and management comments.

2- share price already dropped from 500 to 400 - 20% drop

3- company plant to move iron ore from Karnataka to Arjas plant to AP, now proposed mining tax of 1.5 times of royalty will have significant impact of cost increase, cost benefit due to acquisition will not be there.

4 - can they pass on this mining tax to their customers and what is their position on agreements with customers.

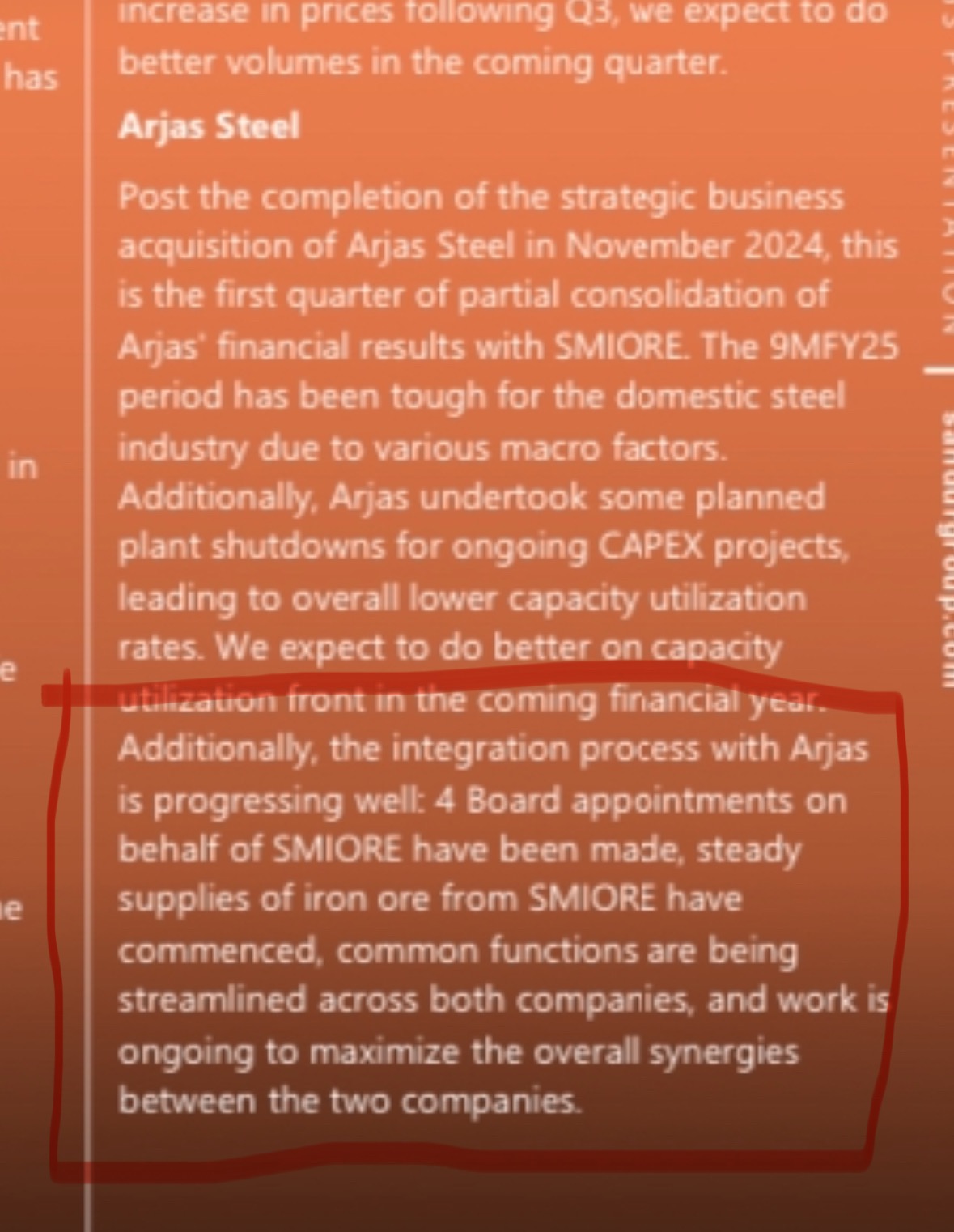

Integration with Arjas explained

Good thing Management understands what investors want to know thereby keeping things relevant.

1 Like

Last year i.e. FY 2023-24 Arjas Had TO of 2608 cr. And PAT of 32.81 cr.

Will be interesting to see how supply of RM from SANDUR to Arjas as to quantity and the price wise impacts SANDUR consolidated results in FY 2025-26.

Invested and Not an advice

As steel sector is seeing some revival overall, arjas steel will do even better from here.

And even mining sector is seeing uptick as guided by management.

Hoping for the good upmove in short to medium from this stock, as business is doing and generating good revenue and cash flow.

2 Likes

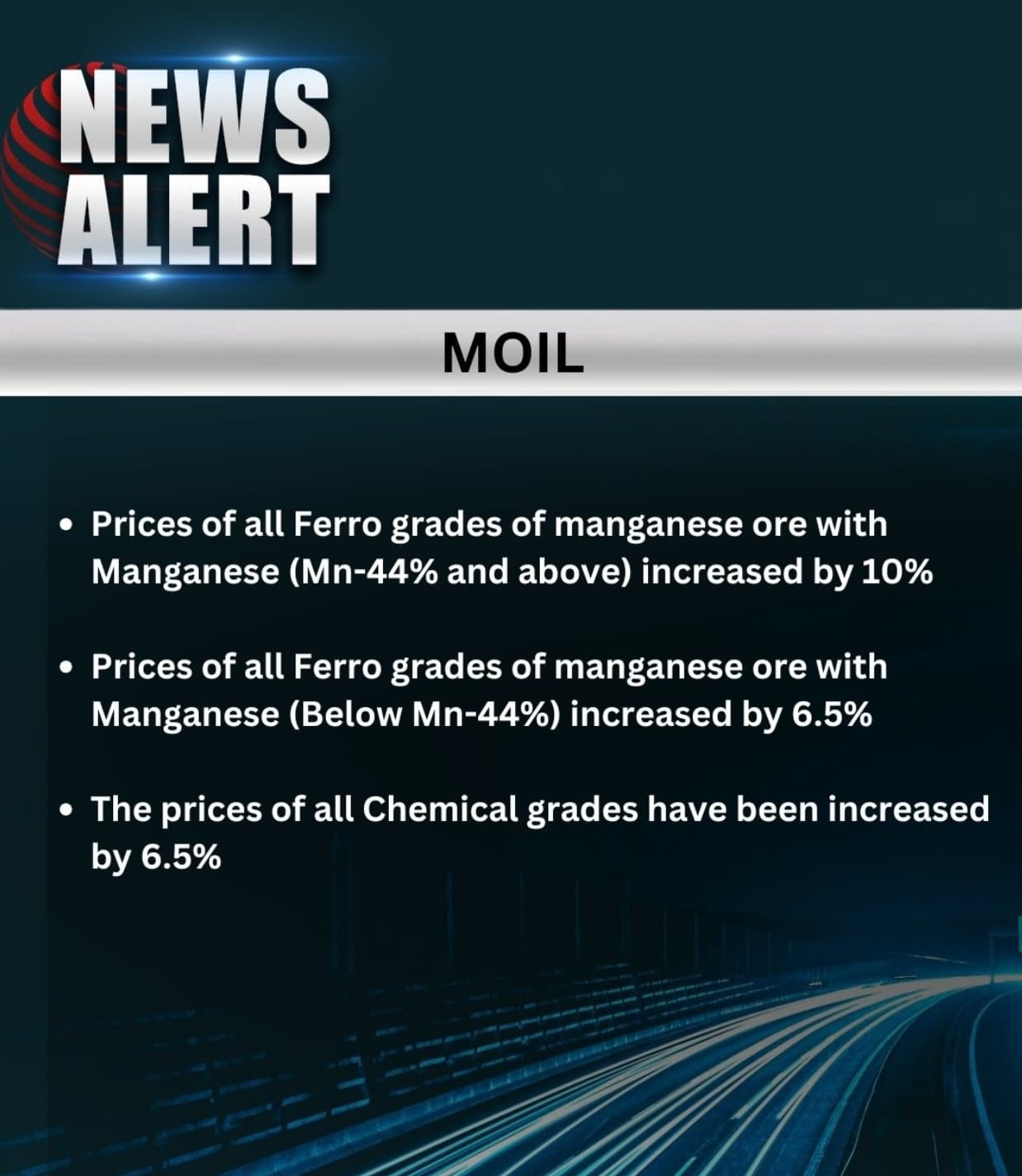

Price increase in manganese ore upto 10%.

Margin will expand further.Q4 will be Interesting watch. Full arjas steel impact plus demand picking up in mining.

3 Likes

CEO resigned, reasons not state all though seeing lot of resignations from CFOs/auditors and CEOs in bear market!

Be advised, he joined last year in August

2 Likes

Point 8 on the Notes to Account : Subsequent to the quarter and year ended 31 March 2025, the Holding Company has received Consent for Operation (CFO) frorn Karnataka State Pollution Control Board (KSPCB), Bengaluru for increase in production of Iron Ore from 3.81 Million Tonnes Per Annum (MTPA) to 4.36 MTPA. Further to the receipt of CFO, the Company has on 7 May 2025 received allocation of Maximum Permissible Annual Production (MPAP) from Monitoring Committee to operate at the enhanced levels. Considering the pro-rata allocation, the MPAP for financial year 2025-26 is 4.31 MTPA for iron ore.

Interesting comments on Investor Presentation, “We are entering FY26 on a strong footing, with all mining expansions operational from the very start of the year and the added advantage of fully consolidating Arjas Steel.

2 Likes

Does anyone have any idea why the period between 2019 and 2023 is blank in the balance sheet in the screener?

1 Like

For those years they had only Standalone statements as the existing subsidiary was merged into Sandur. But later in 2022 they set up another subsidiary, so Consolidation started again.

2 Likes

Thank you for the clarification.

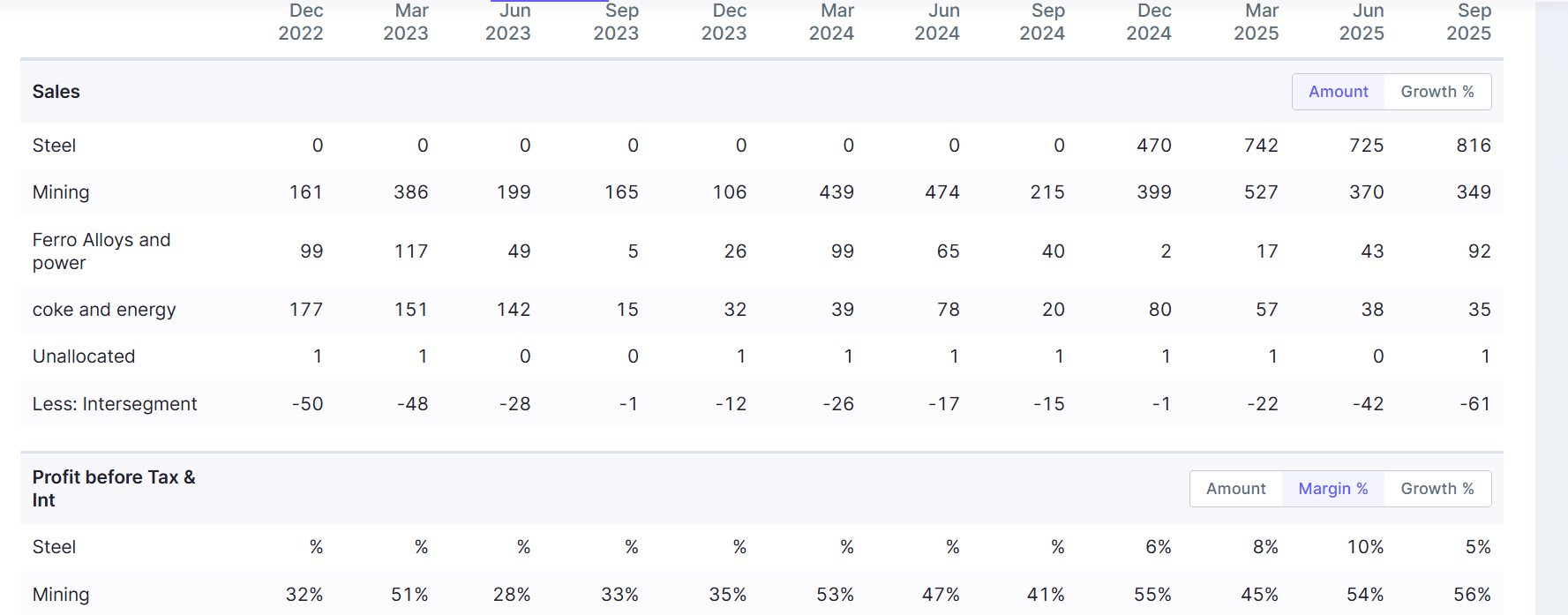

What’s the business rationale behind the Company amping Steel business when the margins on Steel business is 8%, 10%, 5% - essentially in single digits and the margins on Mining have been consistently steady and in the mid 45% to 55% range which ?

They acquired Arjas Steel and the integration and its impact is underway currently. They are supplying iron ore to Arjas (25% of Arjas needs are currently met by Sandur ores and it will increase going forward).

Sandur will transform from being a mining company into a speciality steel company. Arjas margins are likely to improve to 12 to 13% going forward due to the integration and they are also looking to increase the share of value-added products

4 Likes

As stated by @kartik_bhat above, margins will improve once integration is complete and Arjas starts using in-house inputs. Even if consolidated margins are lower, there will be absolute growth in profits, and hence EPS growth for the company.

But there is an even more important angle behind Arjas Steel acquisition.

Sandur has two mining leases, one for iron ore and one for manganese. Both the leases expire in 2033. Under the amendments made to MMDR Act in 2015, all such leases will be put up for compulsory auction through competitive bidding. There is no discretionary or automatic renewal. This means the mines will go for auction in 2033. And somebody else can bid higher and snatch away the mines from Sandur, leaving it with virtually nothing. This risks the very existence of the company, as we know it.

However, the Act also provides that if the mine is a captive mine, the lease holder has the Right of First Refusal (ROFR) if it matches the highest bid. It is therefore imperative that Sandur becomes a steel company and demonstrate that the mine is a captive mine rather than a standalone mine. It can then match the highest bidder (if someone else bids higher) and retain the mine for itself. Once it wins the bid in 2033, it will get a 50-year lease, ensuring mining rights till 2083.

28 Likes

Thankyou for the clarification

1 Like