My View on Sandur Manganese (Read FY17 and FY19 annual report, based on same)

1) Excellent work environment (more as subject then labour)

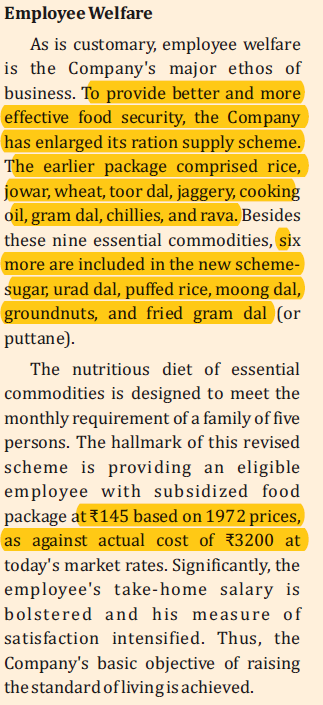

The company management has very well treated employee. The provide subsidised food to employee and never faced problem since inception as per AR. While this is good, cost of employee has large portion of subsidised food which can increase cost and reduce comepeitiveness of the company over a period.

ARFY19 Chairman speech:

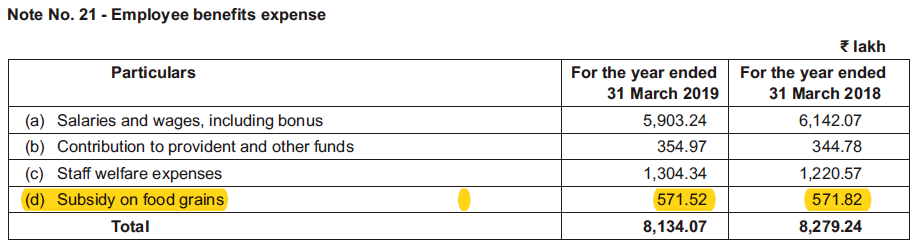

Food subsidiary expenditure increased from Rs 4.78 Cr in FY16 to Rs 5.71 Cr in FY19. During same period, employee strength increased from 1879 in FY16 (1st April 2016) to 2109 in FY19 (31 Mar 2019). Average food subsidy per employee increased from Rs 25439 in FY16 to Rs 27074 in FY19 at CAGR of 2% which is lower than inflation as well.

Secondly, in FY19, the company increased six more item to sudsidised food item as per chairman speech and and higher employee strength, but despite that total Food subsidy charge declined. Need to understand exact relationship between employee and remuneration to same by the company.

2) Significant jump on Board size and higher managerial remunerations

The company has very wide group of board of directors. Some of directors are also on board of Brigade enterpise, JSW Engery and Navbharat Venture. The company has also proactively formed Risk management committee which is necessary for only Top 100 market capitalised listed company. So the company has been proactive and having good corporate governence. On Page 61 of AR FY19, the company has provided skill set and industry specialisation of board member which I have seen first time in investment journey.

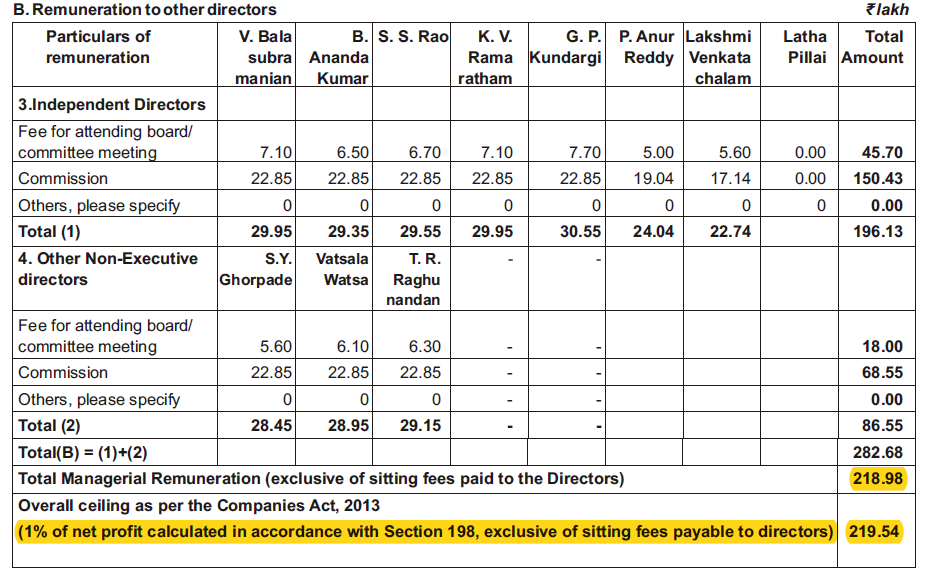

However, that has also resulted in very high charge in P&L account for the company. In fact, in FY19, the company has paid total amount of Rs 2.82 Cr (including Seating fees of Rs 0.45 Cr) as against Ceiling of Managerial remuneration of Rs 2.20 Cr. The company discloure indicate that Manangerial remuneration (excluding seating fees) is Rs 2.19 Cr which is withing Ceiling of companies Act. In my limited understanding (which may be wrong), the company has breached the ceiling of payment in managerial remuneration and need approval for Central government to regularise. Even Company Secretarial audit report is silent on same (hence there is high probability that my concern is not valid).

Also, in FY17, total seating fees paid to director was Rs 20 lakhs which has increased to Rs 63 Lakhs in FY19. Total managerial remuneration has also increased from Rs 81 Lakhs in FY17 to Rs 282 Lakhs during FY19

Further, most of time, we find increase in managerial remuneration being higher for executive director (operating person) as against Non-executive directors. However, in this company, EDs remuneration is very much in limit but NED remunderation is exceeding ceiling. We need more understanding of this.

3) Good Corporate citizen but higher financial cost

While already dealt with fair treament to employee, coming from Royal family, it has also attempted to improve quality of life in negihbourhood area. Beside providing school and other aminities (as shown in CSR), the company has contributed Rs 1.85 Cr on CSR budget in FY19 as against regulatory requirement of Rs 1.67 Cr (Page 45 pdf AR FY19). While that is not material and can be ignored, in FY19, the company has seen jump in Donations and contribution, from Rs 1.7 cr in FY18 (this is in addition to CSR) to Rs 19.7 Cr (almost 11 times) in FY19. While part of it can be explain to provide better amedities to neighbourhood and creat goodwirll, but still such large expenditure need explanation.

I believe it is not a political party donation as same need to be specifically disclosed in Annual report as per companies act.

4) Interest cost:

In FY17, the audit report says that the company is generally regular in depositing various statutory due on time. The company also had no borrowing/debt as on MArch 31 2019. However, despite above factors, We find almost Rs 7.2 Cr of Finance cost being interest on dealyed payment.

5) Delay in regulatory compliances:

FY17 Secretarial audit report has following concerns: (Page 45 PDF file AR FY17)

- Dealyed in Filing E-return with MCA

- Non-compliance in process to issue duplicate share certificate

- Delay in filing vacancy of Non executive director

- FY16 financial statement filed without auditor report and opinion (non complaince with SEBI guideline)

- Delaying in filing information to stock exchange for issue dupliate share certificiate.

FY19 Secretarial audit report has following concerns (Page 42 pdf FY19)

- Non filing of Form RE-2 under explosive rules, 2008 for April and May 2018 months

- Composition of Nomination and remuneration committee was not as per SEBI regulations (BSE imposed fine of Rs 2,17,120/-, Page 44)

- Few forms with MCA filed with delay

From the explanation provided in directors report it appear that company is not able to get right manpower to fulfill regulatory requirment. Probably, it may outcome of paying lower salary to executives (already mentioned in Point 2). CS Divya name does not even appear in top 10 employee in term of remuneration and she is not even considered as Key managerial person (hence salary is not disclosed). Same being case with CFO. CS and CFO by definination of companies act are KMP and there salary disclosure is must in audit report, but same being missing from the annual report of the company over FY17-19. I think this lapse in reporting in my understanding which shall be corrected. Having said that, not very material issue as well.

6. Financials

a) Very High Investment property :

The company has Investment property worth Rs 50 Cr as on March 31 2019. This include one residential and commerical property with estimated fair value of Rs 79 Cr as on March 2019. The company get only Rs 33 lakhs (Rent Rs 59.6 lakh- Dep Rs 26.5 lakhs) from this property which is substantially lower than Cost of capital in my opinion. The company may explore way to liqudiate same or use assets more productively. Total Property Plant Equipment as on March 31 2019 is around Rs 90 Cr (Net of Depereciation Rs 74 Cr). So almost 30% of gross block (without consider capital WIP) is blocked in investment assets.

b) Very high cash and bank Balance

The company carry very high current account balance of Rs 22.6 Cr as on March 31 2019. Total operatin revenue being Rs 702 Cr (so around 2 Cr per day), the company have 10 days sales as balance in current account which is very high. They have move same in fixed deposit and earn income.

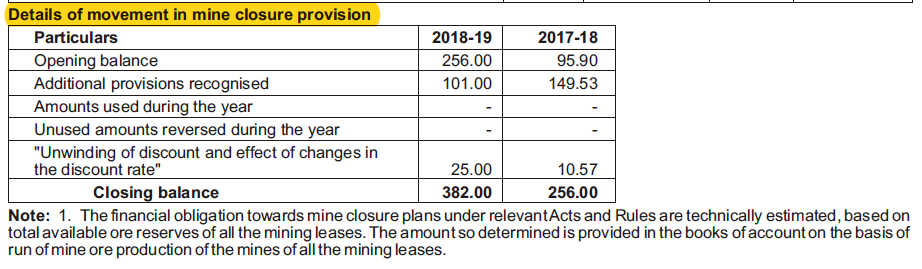

C) Mine closure provision

The company has provided for cost of mine closure basis on estimate. This is positive point as even very large mine owner like Hindustan zinc, I have not seen such provision. Once mine operations are over, there is huge cost inolved to surrender the mine back to Government (which may mean to minimise environment impact and also uliise waste dug generated from ore extraction. It is very high cost element in global market in my limited understanding). This is first company I have seen which provided for mine closure which is very positive in my view.

I was not able to go through new project of 1 mn tpa capacity expansion. The company has tied up fund of Rs 470 Cr with Banks as per note. There was no loan outstanding as per March 31 2019 financials.

Summary: While there are some complinace related issues, the company having board committee evaluating Environment (Reclamation and rehabilitation plan implemnetation committee since 2012), Risk Management committee, environment concern surrendering land for forest, 3 years 5 Star rating, Care for all stakeholder including employees, disclosure of analyst meet QA to stock exchange), I form overall very positive view for the management. In my personal scale of ability and willing (Credit analyst evaluate credit in ability to pay and willing to pay of maangement, I modify same as ability to perform and willingness to share with stakholder for equity investment), I find company willingness to treat stakeholder fairly exceptionally great . On ability to perform, they have managed in past mine well (but cost may be higher due to ESG concern), one need to see how management perform on new project implementation on time and without cost over run. The project is very large to scale of operation and hence they may need new team and skill-set.

Disclosure: No investment, My view may be biased, have limited understanding of steel sector, not sebi registered advisor.