I came across a really interesting story in the auto-anc space, and wanted to share it with board members.

What do they do?

Sandhar Tech. started in 1987 as a sheet metal supplier to Hero. Since then, they’ve grown to offer a multi product catalogue, supplying 79

global manufacturers and have market leadership in a few product ranges.

The product mix has remained fairly unchanged in the last two years. (Note, they disclose their largest segments, so the balance is in others.)

| Products | Q1FY19 | Q2FY19 | Q3FY19 | Q4FY19 | Q1FY20 | Q2FY20 | Q3FY20 | Q4FY20 | Q1FY21 | Q2FY21 | Q3FY21 | Q4FY21 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Locking Systems | 0.22 | 0.22 | 0.21 | 0.21 | 0.21 | 0.21 | 0.22 | 0.20 | 0.20 | 0.22 | 0.21 | 0.21 |

| Vision Systems | 0.09 | 0.10 | 0.10 | 0.10 | 0.10 | 0.09 | 0.09 | 0.09 | 0.08 | 0.08 | 0.08 | 0.08 |

| Sheet Metal | 0.15 | 0.12 | 0.12 | 0.11 | 0.11 | 0.12 | 0.11 | 0.11 | 0.13 | 0.13 | 0.12 | 0.12 |

| Offroad Heavy | 0.13 | 0.12 | 0.13 | 0.14 | 0.14 | 0.12 | 0.12 | 0.13 | 0.08 | 0.10 | 0.15 | 0.15 |

| ADC | 0.17 | 0.16 | 0.16 | 0.17 | 0.17 | 0.19 | 0.19 | 0.20 | 0.25 | 0.22 | 0.20 | 0.21 |

| Assemblies | 0.19 | 0.14 | 0.15 | 0.15 | 0.16 | 0.17 | 0.14 | 0.13 | 0.11 | 0.10 | 0.10 |

Please note that locking systems, offroad heavy (OHV) and aluminium die casting (ADC) form the largest piece of the pie.

| Segments | Q1FY19 | Q2FY19 | Q3FY19 | Q4FY19 | Q1FY20 | Q2FY20 | Q3FY20 | Q4FY20 | Q1FY21 | Q2FY21 | Q3FY21 | Q4FY21 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2W + 3W | 0.59 | 0.59 | 0.58 | 0.57 | 0.59 | 0.61 | 0.60 | 0.58 | 0.58 | 0.61 | 0.58 | 0.57 |

| PV | 0.24 | 0.24 | 0.21 | 0.21 | 0.22 | 0.21 | 0.21 | 0.23 | 0.26 | 0.21 | 0.21 | 0.22 |

| Offroad Heavy | 0.13 | 0.13 | 0.14 | 0.14 | 0.13 | 0.13 | 0.13 | 0.14 | 0.11 | 0.12 | 0.16 | 0.16 |

| Electronics | 0.04 | 0.05 | 0.05 | 0.06 | 0.04 | 0.04 | 0.04 | 0.05 | 0.05 | 0.06 | 0.05 | 0.05 |

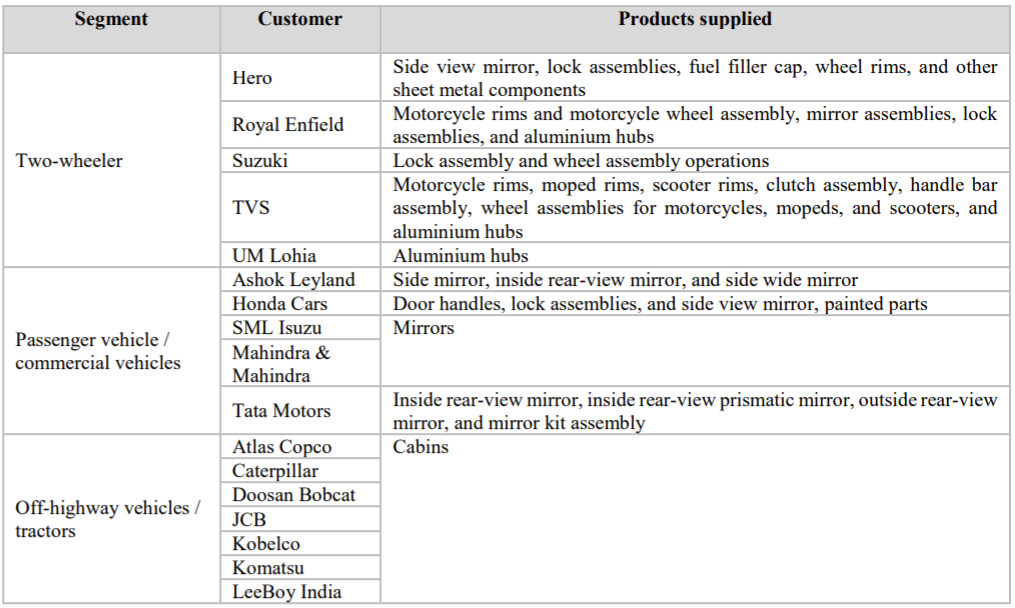

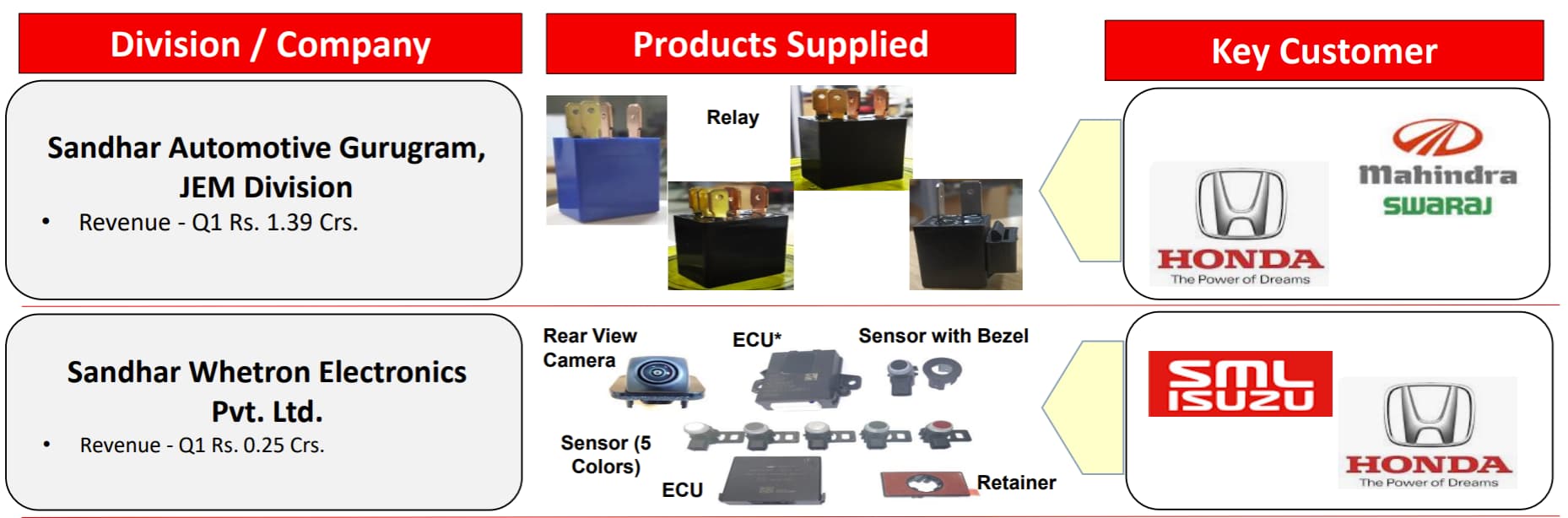

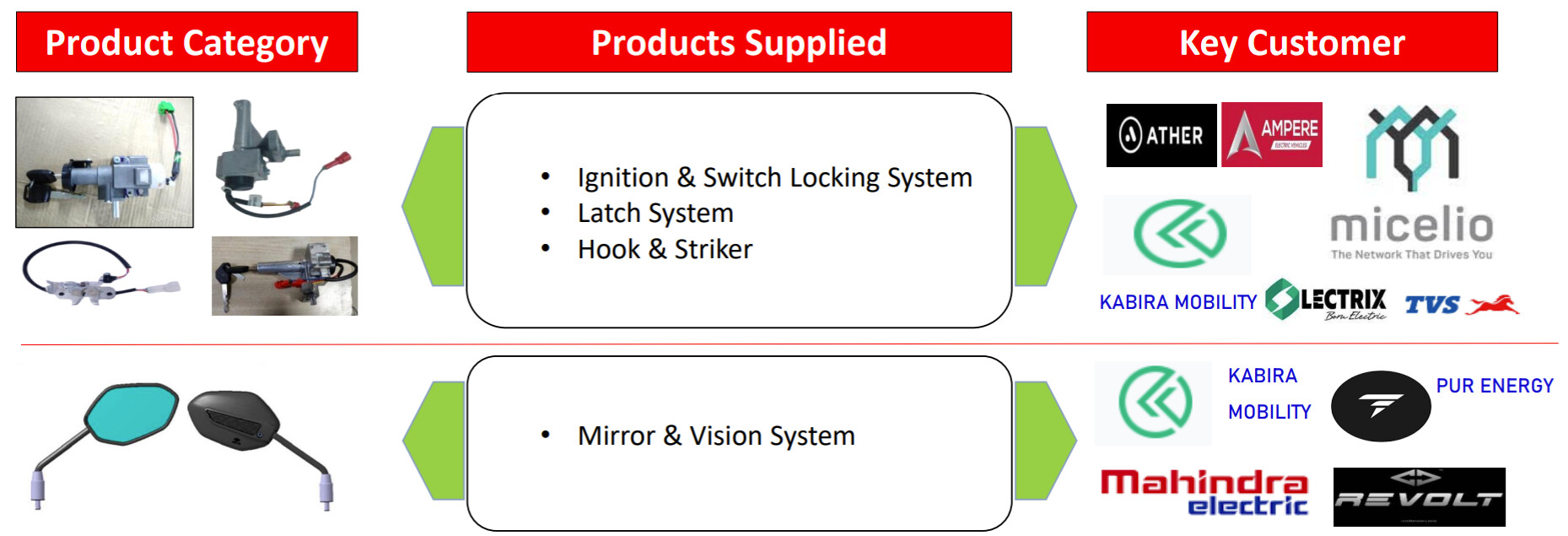

The 2/3 Wheeler segment makes up 60% of Sandhar’s revenue. They’ve made detailed disclosures of their revenue breakup across clients, most recently in Q2FY21.

Please compare this figure to the product supply image above to understand what Sandhar supplies to each of these clients, and you’ll see how they group into baskets.

How have they performed relative to the industry?

Sandhar’s investor presentations/concalls usually have a segment that talks about the industry, the OEMs they supply to, and the relative growth between the two.

| Relative Growth | Q2FY19 | Q3FY19 | Q4FY19 | Q1FY20 | Q2FY20 | Q3FY20 | Q4FY20 | Q1FY21 | Q2FY21 |

|---|---|---|---|---|---|---|---|---|---|

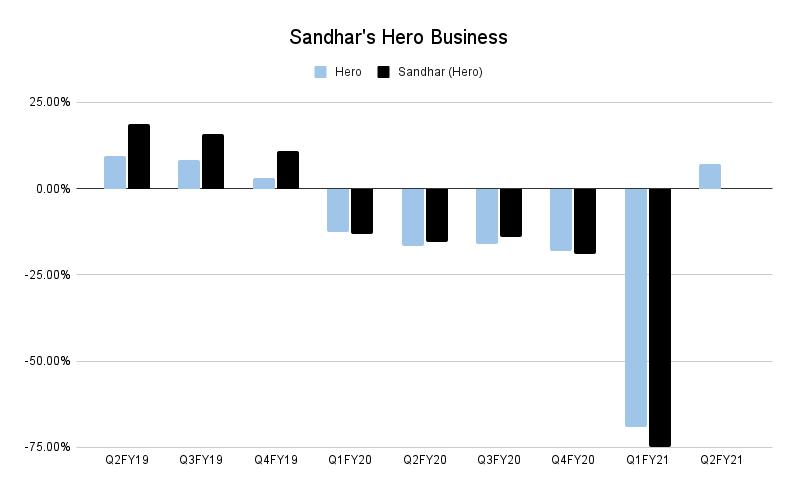

| Hero | 9.40% | 8.20% | 3.10% | -12.50% | -16.70% | -16.00% | -18.00% | -69.00% | 7.00% |

| Sandhar (Hero) | 18.70% | 15.80% | 10.80% | -13.20% | -15.40% | -14.10% | -19.00% | -75.00% | 0.00% |

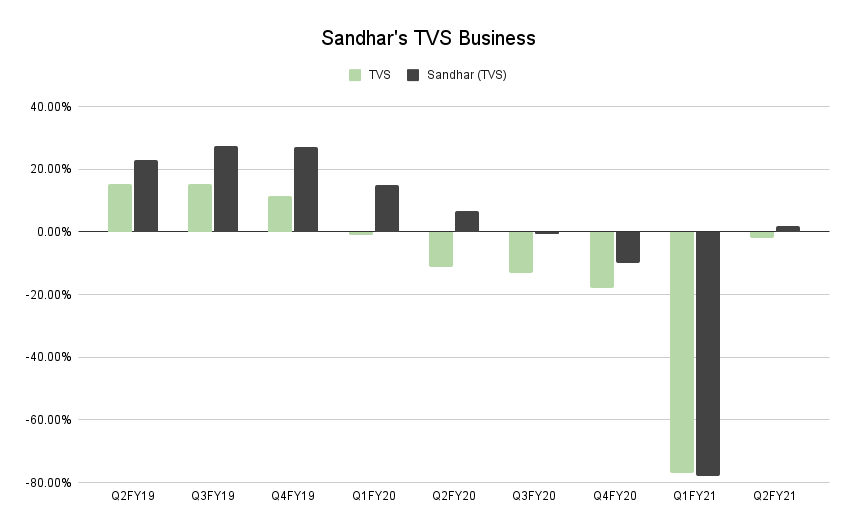

| TVS | 15.30% | 15.40% | 11.60% | -1.00% | -11.10% | -13.00% | -18.00% | -77.00% | -2.00% |

| Sandhar (TVS) | 22.90% | 27.30% | 27.00% | 15.10% | 6.80% | -0.70% | -10.00% | -78.00% | 2.00% |

| Honda | 3.90% | 3.90% | 7.40% | -20.90% | -35.20% | -36.10% | -44.00% | -95.00% | -18.00% |

| Sandhar (Honda) | 1.10% | -5.30% | 1.50% | -8.10% | -35.20% | -40.10% | -49.00% | -96.00% | -17.00% |

| JCB | NA | NA | NA | NA | NA | NA | NA | NA | NA |

| Sandhar (JCB) | 163.00% | 156.60% | 125.30% | 2.70% | -10.80% | -11.30% | -18.00% | -79.00% | 7.00% |

| Bosch | NA | NA | NA | NA | NA | NA | NA | NA | NA |

| Sandhar (Bosch) | 8.60% | 7.70% | 5.00% | -9.70% | -4.70% | -8.60% | -8.00% | -63.00% | 4.00% |

| Royal Enfield | 12.60% | 6.10% | 0.70% | -18.50% | -19.60% | -15.40% | -16.00% | -69.00% | -10.00% |

| Sandhar (RE) | 18.40% | 12.00% | 10.20% | -14.50% | -8.20% | 4.80% | -5.00% | -79.00% | -9.00% |

| TRW | NA | NA | NA | NA | NA | NA | NA | NA | NA |

| Sandhar (TRW) | 7.80% | 7.30% | 4.30% | -2.20% | 0.10% | -2.80% | -5.00% | -71.00% | -8.00% |

| Autoliv | NA | NA | NA | NA | NA | NA | NA | NA | NA |

| Sandhar (Autoliv) | 39.50% | 41.70% | 26.40% | -1.30% | 12.10% | 22.50% | -6.00% | -52.00% | -2.00% |

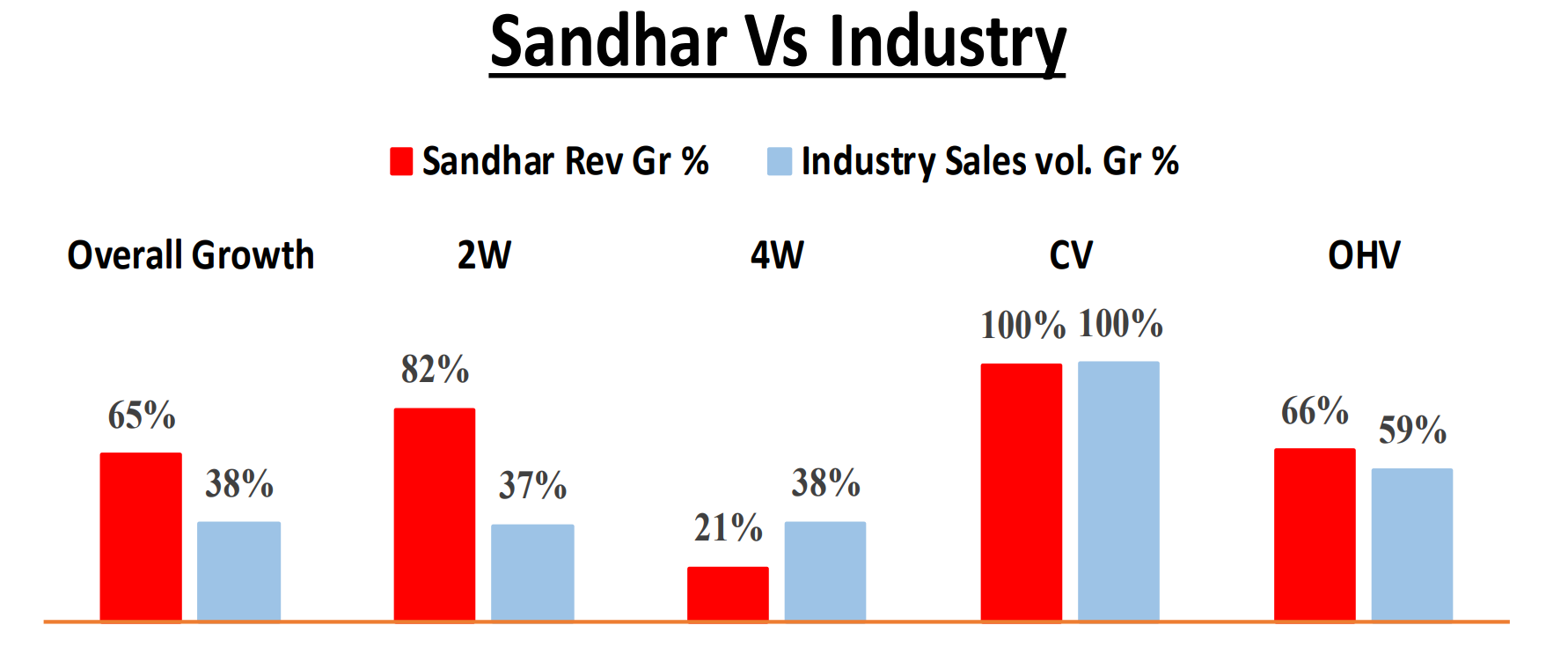

Since we know TVS and Hero form the largest share, here’s a chart comparing Sandhar’s revenue growth with client’s growth.

-

One notices that in upcycles, Sandhar’s business outperforms their client’s revenue growth. In downcycles, their degrowth is not as bad as their clients. This is evident in TVS more than Hero.

-

This data was disclosed in presentations only from FY19, so we only have data spanning 3 years.

On the industry level,

| Segment | Q2FY19 | Q3FY19 | Q4FY19 | Q1FY20 | Q2FY20 | Q3FY20 | Q4FY20 | Q1FY21 | Q2FY21 | Q3FY21 | Q4FY21 | Q1FY22 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Industry 2/3W | 13.20% | 11.90% | 6.60% | -9.80% | -13.30% | -12.50% | -14.00% | -73.00% | -7.00% | 14.00% | 26.00% | 117.00% |

| Sandhar 2/3W | 20.20% | 13.00% | 16.50% | -2.60% | -7.00% | -8.50% | -15.00% | -77.00% | -0.90% | 22.00% | 57.00% | 188.00% |

| Industry PV | 5.10% | 2.00% | 0.40% | -14.90% | -18.90% | -12.70% | -15.00% | -78.00% | -3.00% | 8.00% | 35.00% | 292.00% |

| Sandhar PV | 7.90% | 7.00% | 5.60% | -1.40% | -9.40% | -12.40% | -15.00% | -73.00% | -2.70% | 18.00% | 35.00% | 252.00% |

| Industry CV | 37.10% | 24.30% | 16.10% | -13.60% | -24.80% | -22.80% | -30.00% | -84.00% | -23.00% | -1.00% | 43.00% | 243.00% |

| Sandhar CV | 34.60% | 20.30% | 12.20% | 12.20% | -42.40% | -32.60% | -30.00% | -82.00% | 37.00% | 34.00% | 75.00% | 467.00% |

| Industry OHV | 20.60% | NA | NA | NA | NA | NA | NA | NA | NA | NA | NA | 106.00% |

| Sandhar OHV | 75.40% | 80.50% | 70.40% | 2.90% | -11.80% | -16.30% | -21.00% | -77.00% | -4.80% | 42.00% | 99.00% | 318.00% |

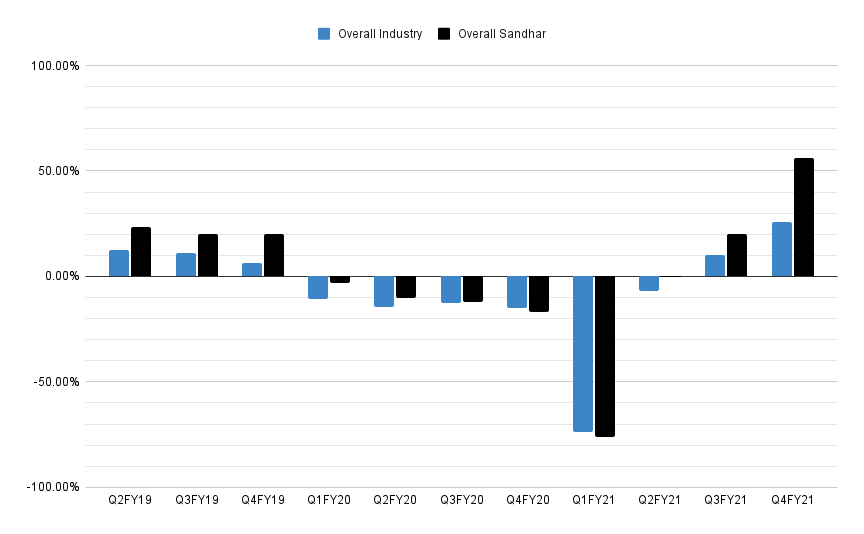

| Overall Industry | 12.70% | 10.90% | 6.50% | -10.50% | -14.40% | -12.80% | -15.00% | -74.00% | -7.00% | 10.00% | 26.00% | 138.00% |

| Overall Sandhar | 23.40% | 20.00% | 20.00% | -3.30% | -10.30% | -12.00% | -17.00% | -76.00% | -0.30% | 20.00% | 56.00% | 217.00% |

Here’s how the overall industry comparison looks like without Q1FY22:

What is their business strategy?

They’ve gone from having five manufacturing plants in 2005, to 32 in 2017, and 43 today in 2021.

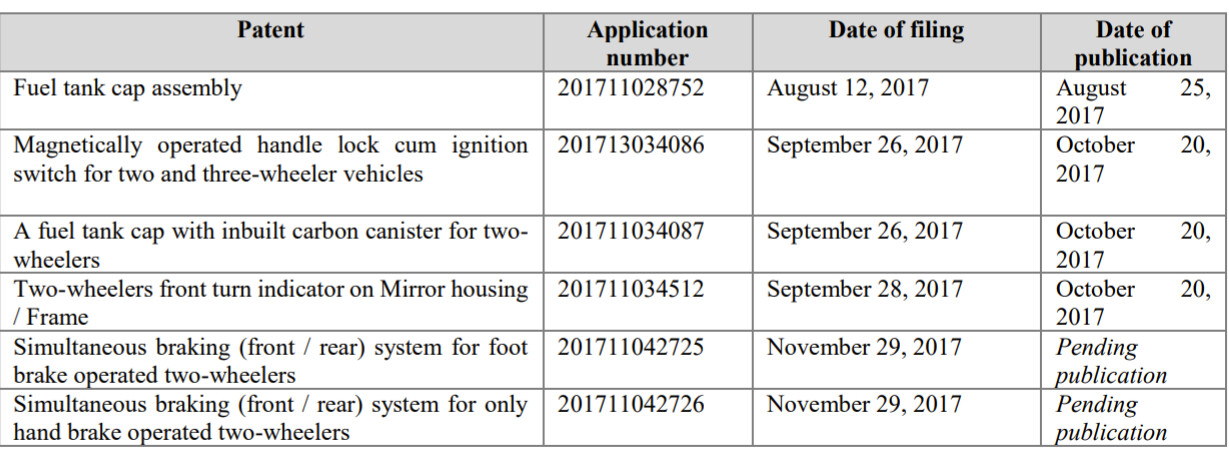

They had 12 patents published in 2017, here are some of them from the DRHP:

On date, they have 20 published, 24 filed and one granted. Published patents don’t give you as many benefits as granted patents, would be worth following the filings. I don’t have domain expertise in patents.

You can see this business strategy in play:

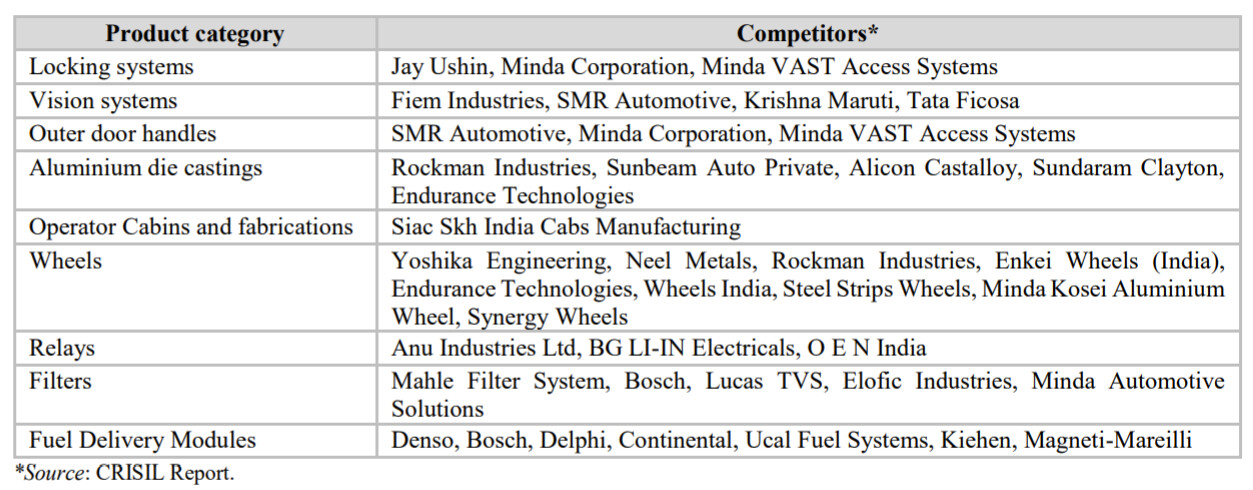

Their key competitors are:

In addition to this, they’ve done two things really well:

1. Increase wallet share from existing customers, intelligent choices in entering new products.

There’s one page in the Q2FY19 investor presentation that drives this home:

If you look at the investor presentations in the past, they list the new annuity business they’ve received, the new product launches, etc.

Their electronics division is very new, started only in 2019, and has a lot of headroom to grow:

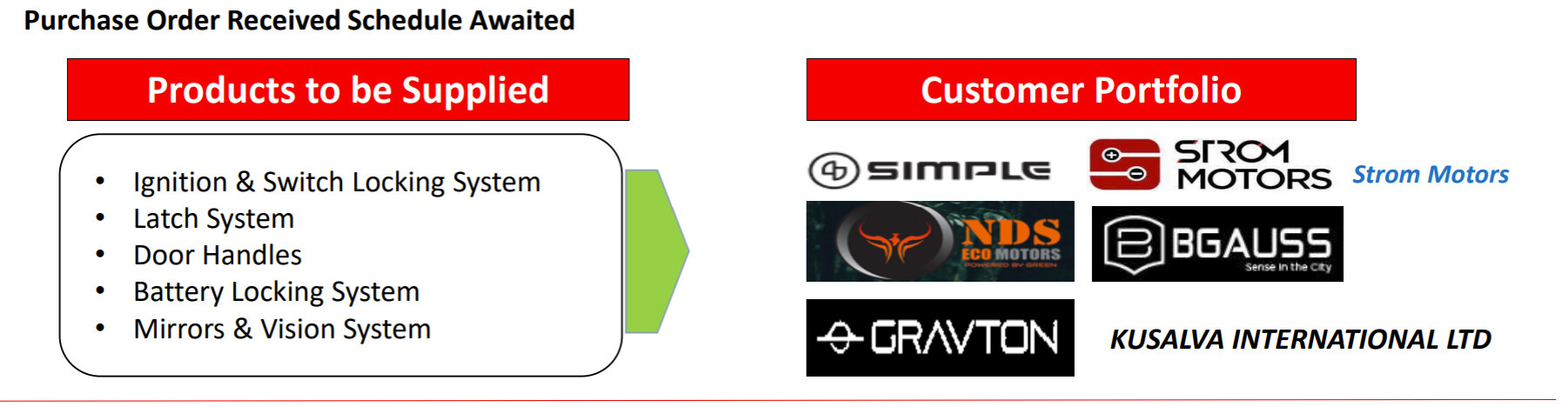

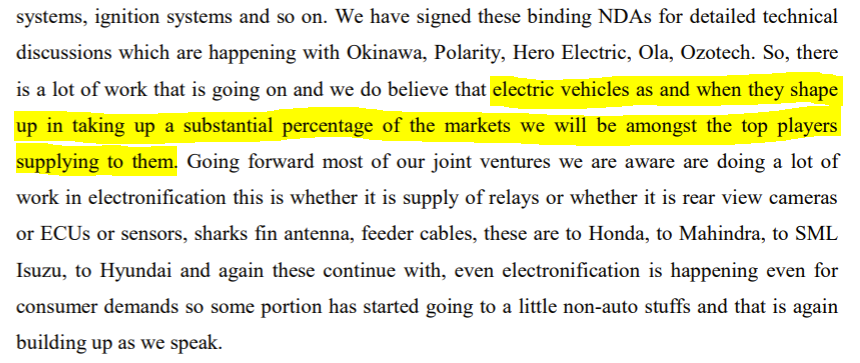

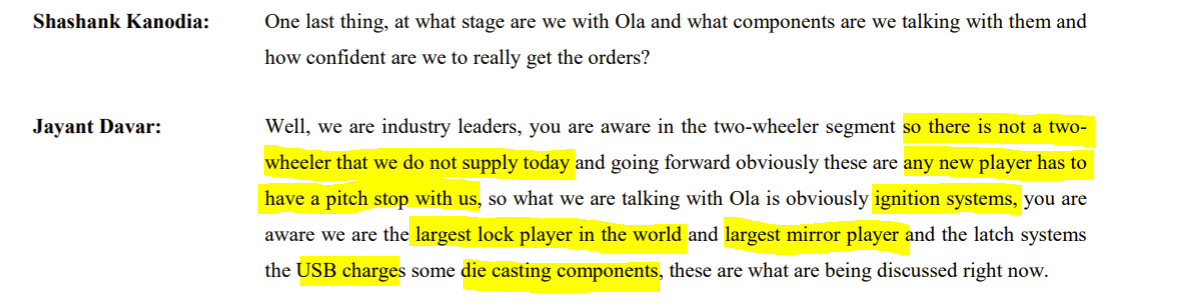

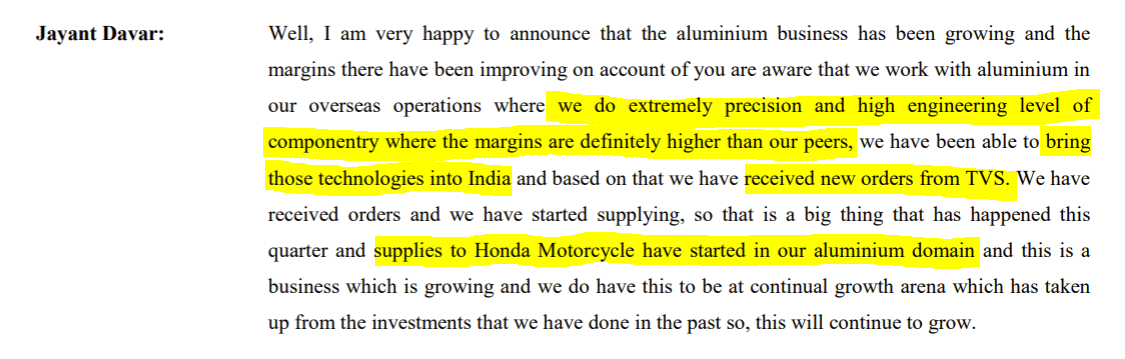

More importantly for a forward outlook, they’ve won a lot of contracts in EVs:

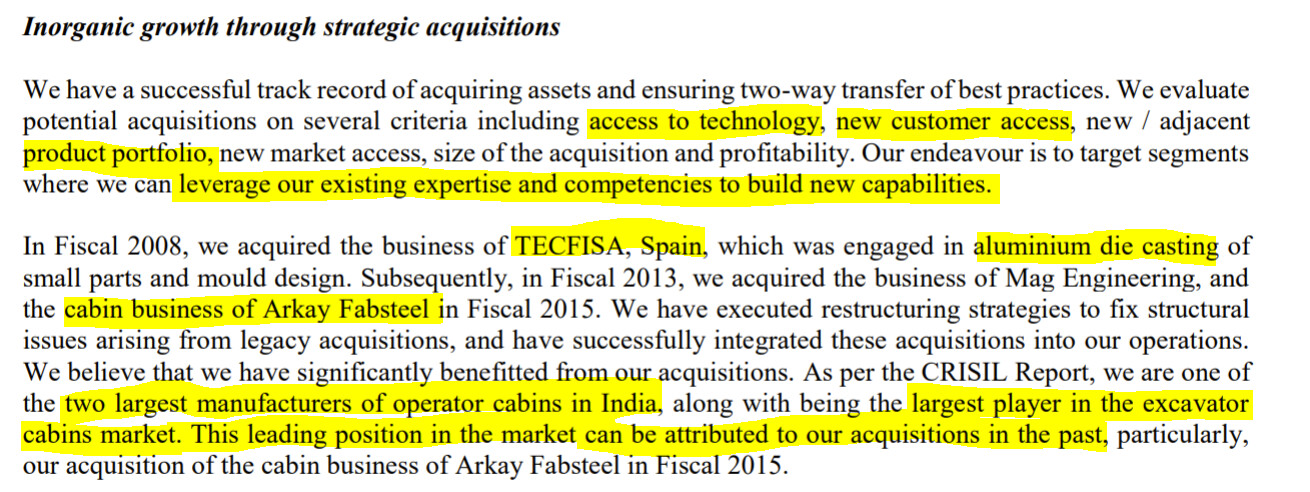

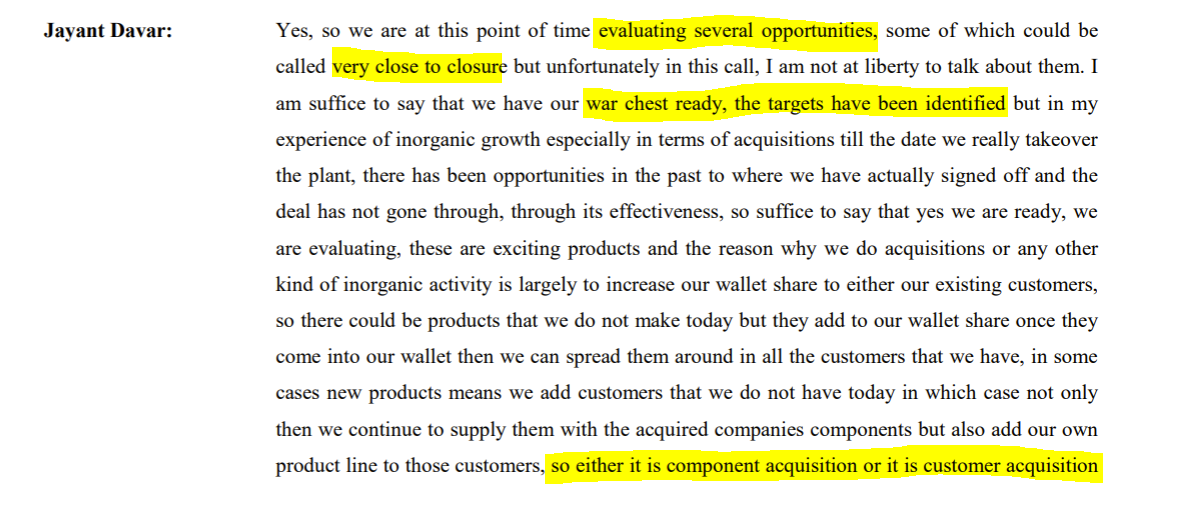

2. Strong inorganic growth choices through acquisitions that then leverage existing client network.

From the Q1FY22 concall:

Management targets RoE of 22-25% for new acquisitions.

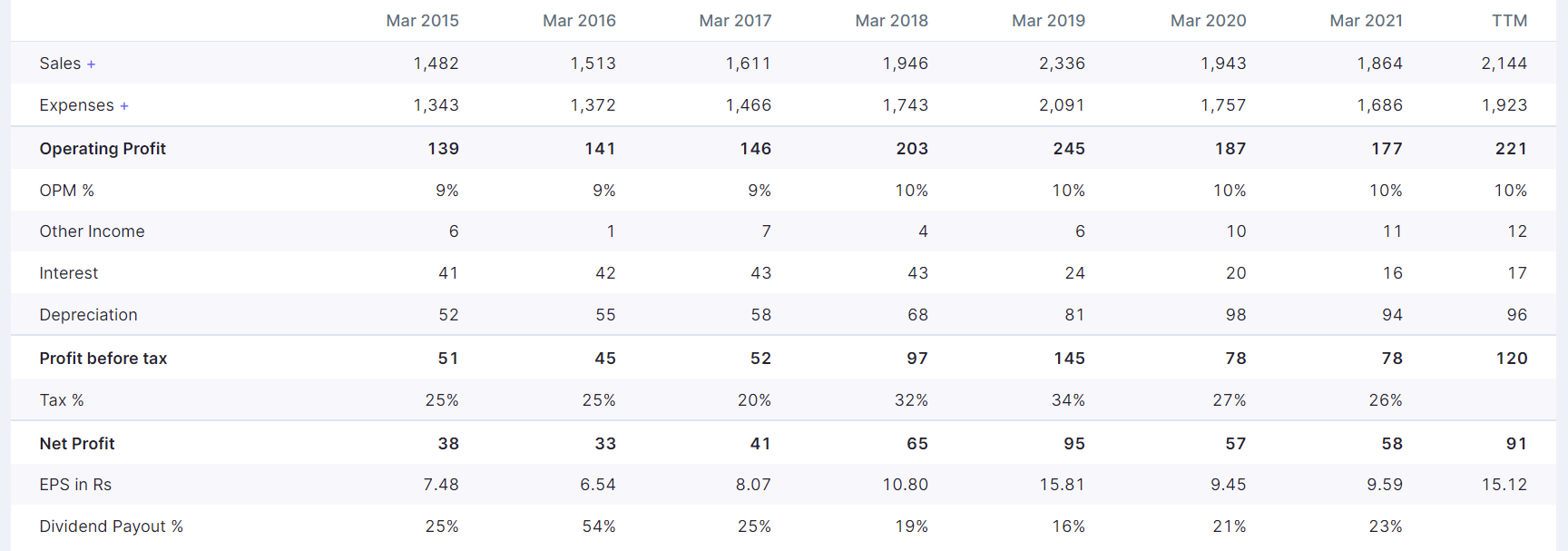

Financial Summary, Valuations, and Management Commentary

Taken from Screener.in

Management has guided 30% revenue CAGR over the next four years and margin expansion of 100-130BPS in FY22, expecting it to stabilise between 11-12.5% in the next few years. They claim this is from organic growth, discounting any contribution from new acquisitions. Detailed breakdown of the guidance across different segments is given in the latest concall.

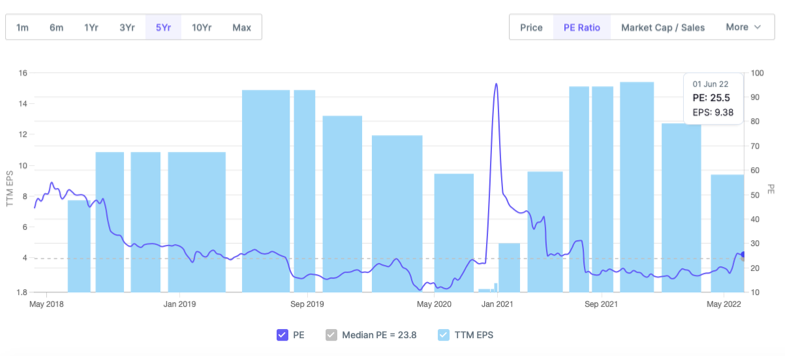

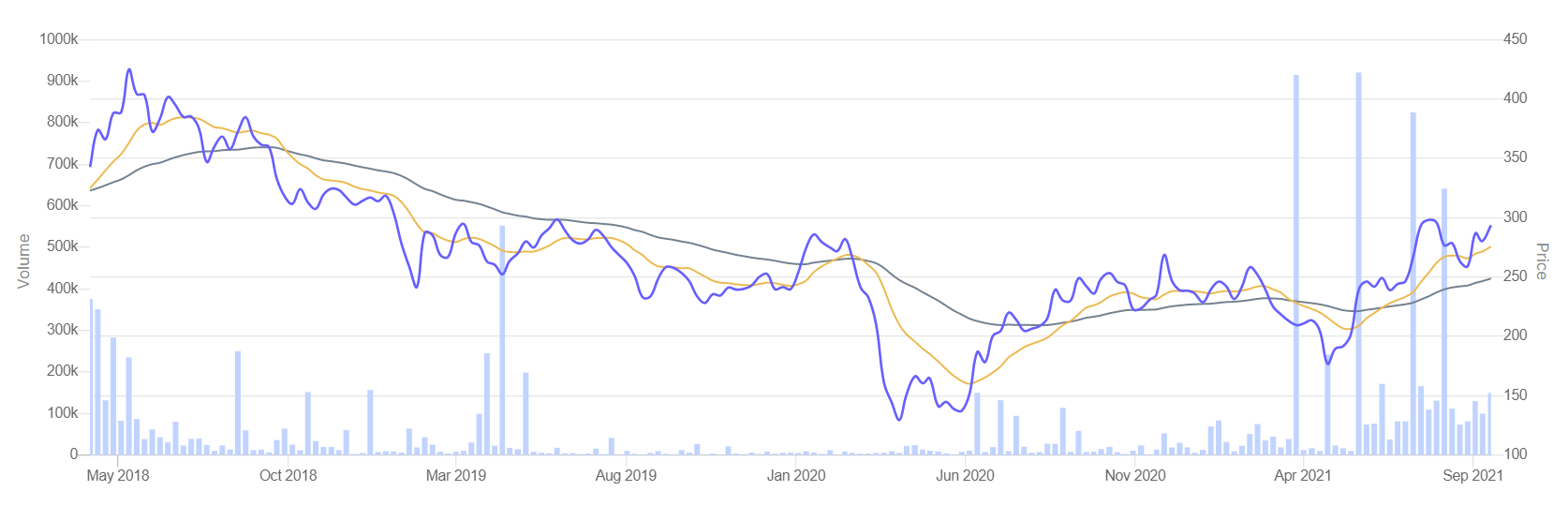

As of writing this post, the trailing valuations are:

| Sandhar Tech. | Price/Sales | Price/Earnings | Price/Book | EV/EBITDA |

|---|---|---|---|---|

| Valuations | 0.82 | 19.4 | 2.19 | 8.87 |

The forward valuations are even cheaper based on how you see the guidance playing out.

Meanwhile the stock price has been languishing since the IPO:

Key Risks

- 50-60% of the revenue for Sandhar comes from two key clients. If TVS / Hero go bust, or these deals fall through, the investment thesis in Sandhar falls through.

Counter argument: Sandhar has actively been trying to diversify product basket and customers. They also have long standing relationships with these two clients.

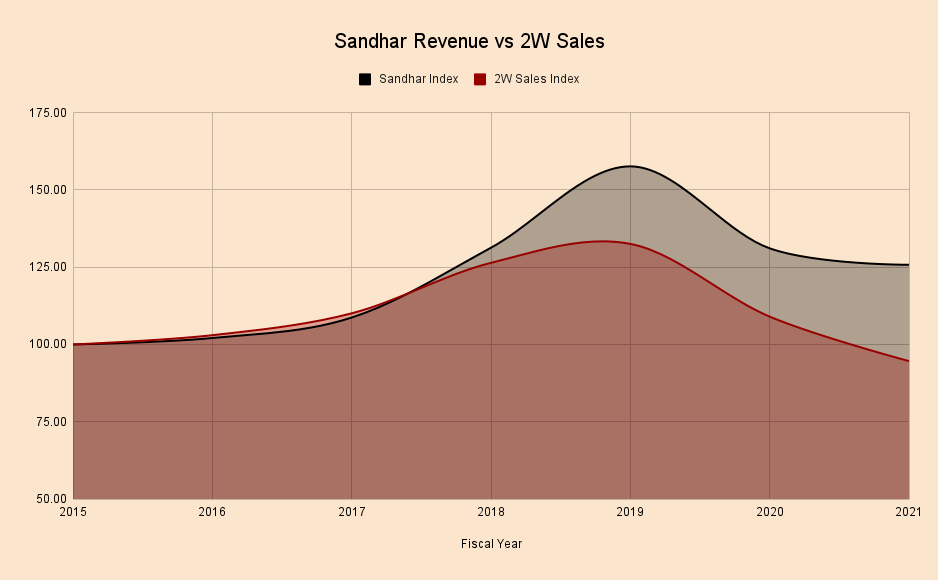

- A downcycle in the 2W industry would lead to headwinds for Sandhar. I’ve indexed the 2W sales in India to Sandhar’s consolidated revenue. While Sandhar performs better than the industry in a downcycle, it still faces headwinds.

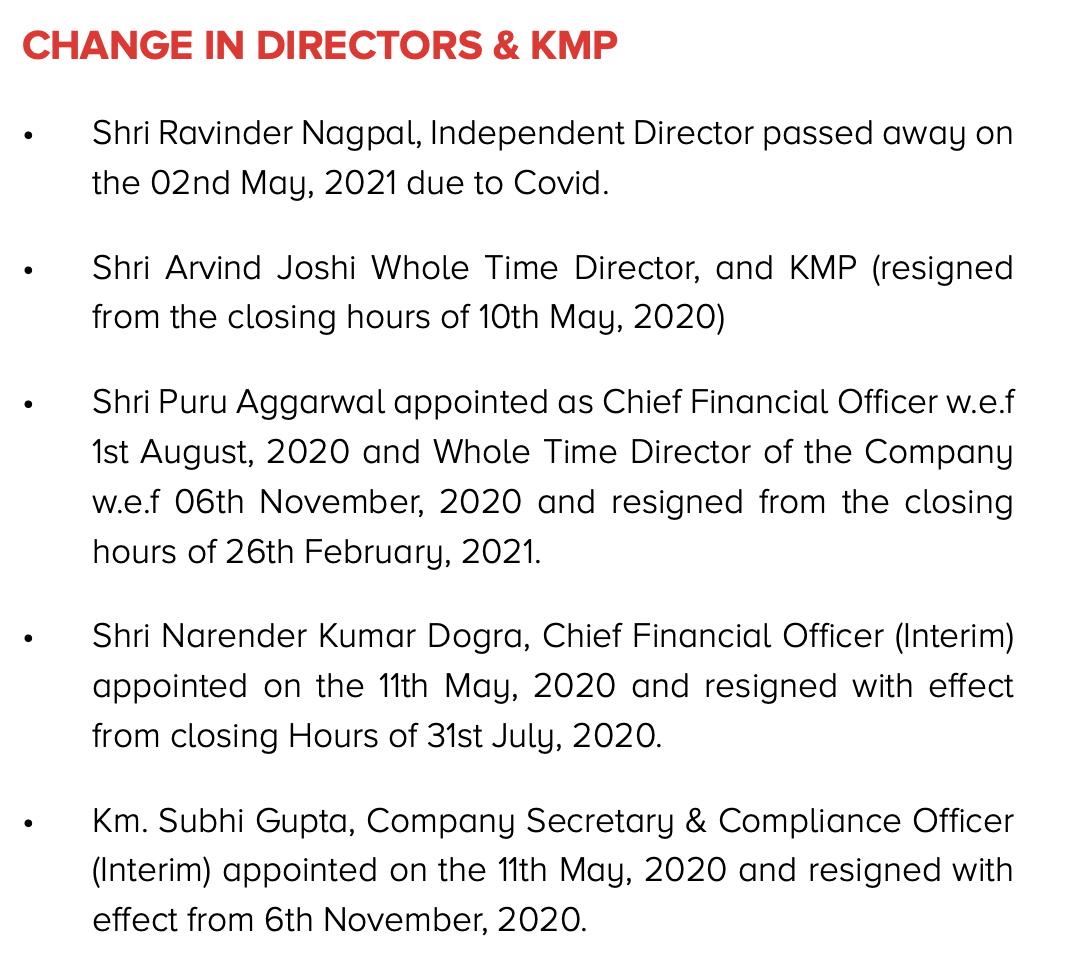

- There’s been some shuffling of management in the CFO position. Their longstanding CFO, Mr. Arvind Joshi resigned in 2019. Following this, they had an interim CFO for some time before appointing Mr. Aggarwal, a former VGL executive to the position for a tenure of 5 years. After only six months, he resigned. His Linkedin shows he hasn’t taken up a position at any other company since, so this could be due to personal reasons.

Investment Summary:

This is an auto-anc player with market leadership in a few categories. Their management has three decades of experience, and has led the company to diversify their portfolio offering, successfully mine clients, and make smart decisions to create new cash cows through inorganic acquisitions and product entries.

At present valuations, finding a company which claims to offer 30% earnings growth over the next few years at less than 1x sales looks to have a sizeable margin of safety.

There is no outstanding civil or criminal litigation.

Inviting all forum members to share their views, verify the possibility of management guidance, and point out red flags that I may have missed.

Disclosure: Invested in Sandhar Tech. Transactions in the last 30 days.