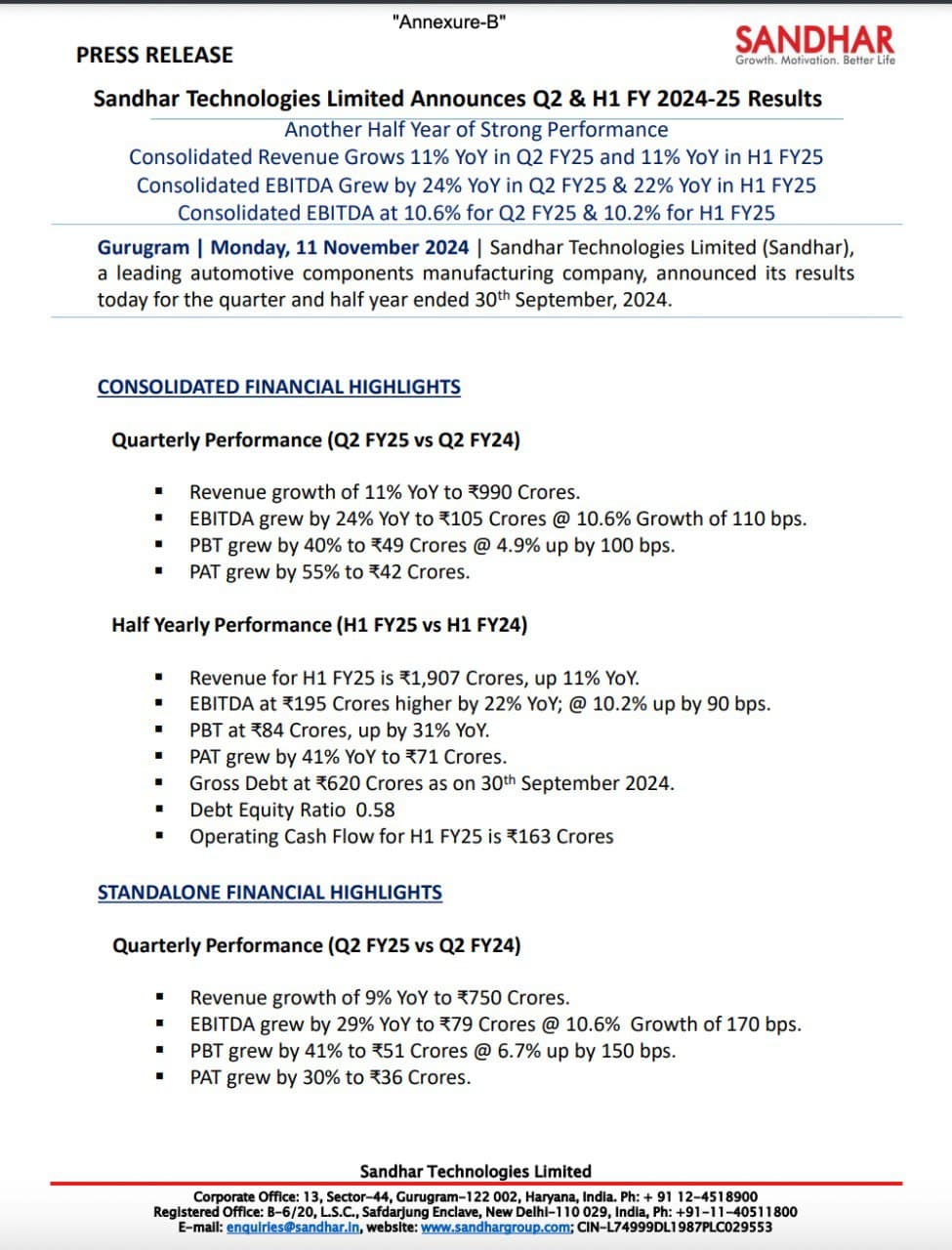

Sandhar Tech (Q3 FY24) (rough cut)

- Start of better utilisation of assets and capex done in few past quarters. Enormous growth is to be seen. EV space progressing well. DC-DC charger, motor controller and charger.

- Q3 – largest customers – TVS motors, 30% of revenue, Hero -19%, JCB – 9%, Honda-3% and so on.

- Capacity utilisation – new projects of casting and sheet metal – mid level (50-60% and likely to be fully utilised by end of FY25). Proprietary items (smart locks, DC-DC converter, MCU, EV Charger) need incremental capex but small.

- Romania is still at 10-20% capacity. Bosch, ERW? customers are planning to shift from China to this plant. Likely to reach good capacity utilisation by FY25/26.

- EV products – one product under trial, hope to launch by 1QFY25. Engaged with 2 customers.

- Q4 outlook – seems extremely strong.

- Election impact – commercial vehicles may see pull back. Others will not see pull back.

- Why set up capacity –at the call of customer. Only when customer says then only capacity is set up. Smart locks, EV: capacities are set up at the behest of the customer.

- Others constitute: tools and dies, after market, plastics business, clutch and break panels.

- What are the peak revenue for sheet metal – (my calculation: sheet metal in Q3 FY24 was ~105 crores, so annual run rate at 60% capacity is 400+ crores. Hence this may go to 600+ crores in FY25).

- Most bullish on proprietary products (smart lock): mechanical lock cost was – 200-300rs, smart lock shall cost 10x. Existing business will catapult. Revenue potential (from smart locks) is 10x. 10-20m vehicles are sold domestically. (my calculation: addressable domestic market for 15m vehicles is in 3000 crores to 4000 crores range). In addition, global market is also a huge potential. My own hunch is smart lock segment itself can be equal to it its overall revenue as of today in 3 to 5 years.

- Smart locks? for Honda, Suzuki, and Hyundai (4-wheeler) will be launched in FY25.

- Debt is at 554 crores. 100 crore debt re-payment likely next year.

- Margins are likely to be in 10-11% range in FY25. Potential is 12 to 13% in long-term.

- EV products capex – around on 10 crores in FY24, FY25 20-30 crores. Asset turn and margin: very asset light: MCU – output per piece supply is 1000s of rupees. Sub parts done already so capex is not required much.

- Bought a company in 2006 – oldest die casting facility. Patent came along the way. Tools for seat belt chair (not sure here) (60% market share) are made by us. Customers are extremely happy due to technology.

- Every casting for TVS is from us.

- Power and fuel 100 crore cost: solar power capacity: contract with solar power company - zero capex investment, 2.5 to 3 rs per unit savings expected.

Disclosure: own it and added more today.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.