Q1 FY25-

Q3 and Q4 are best qrtr.

Revenue and EBITDA starts flowing from FY26,but from FY27 it will flow strongly.

And by the end of the current fiscal year, we are fairly confident to generate incremental INR225 crores to INR250 crores of froe cash.

But we believe we are very well set to deliver high single digit to early double digit in terms of total revenue growth.

We believe that this incremental EBITDA growth will start coming in FY’26, but very small portion. FY’27 onwards, you start seeing this EBITDA growth coming into our P&L.

So you can clearly see the big cities are showing RevPAR growth, which are pretty robustthan tier 2 and tier3.

The combination of all the above, which is same-store growth, renovation, rebranding opportunities within our existing portfolio, inventory addition in our core markets within our cxisting portfolio, and then last but not the least, addition of new inventory, continue to drive a sustainable compounding of revenues in EBITDA and create a significant value for our stakeholders.

80% revenue from - Banglore, Hyderabad, Pune and Delhi NCR

Capex this year- 138cr including all renovation ,room addition etc.

And if I deep dive into your performance, you have a better performance than peers but a lot of it is driven by occupancy rather than ARR.

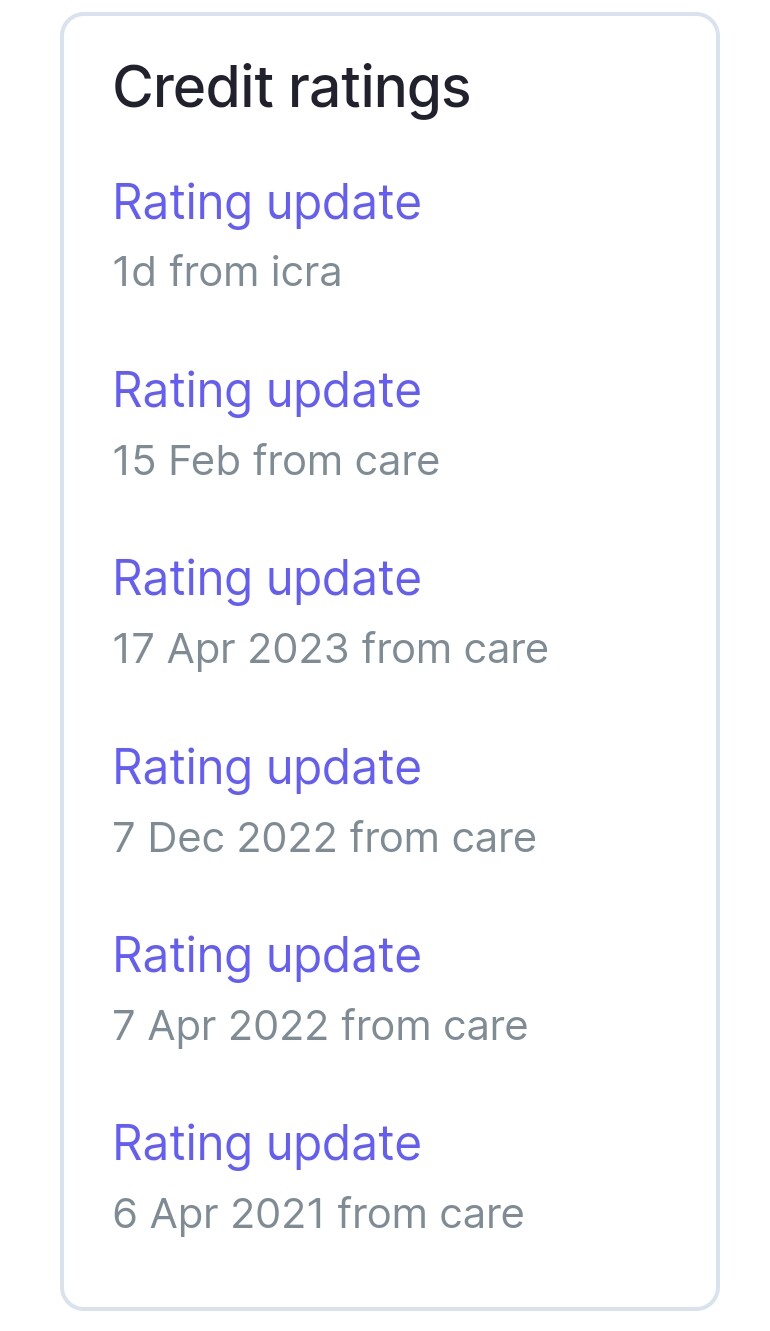

ICRA has updated our credit rating to A- stable, which is a testament to the steps we have taken to improve our capital structure and P&L.It will reduced interest cost to 9.7% and will further reduce to 9.5%

Obviously, part of this will be used towards contiuous deleveraging , or it will reflect in our net debt because of the cash we hold , either two ways, right?

We actually use a word called capital cfficient, which is delivered through our variable longterm leases, where we actually don’t end up paying for land and building, and we only pay for fitting out the building and very quickly start adding that EBITDA to our overall portfolio.

We’ve not been doing so far, but there r a lot of comments that we get. We will start allocating capital towards growth, which will bring near-term EBITDA. So, investors have a very clear visibility of how we foresce the balance shect growing in future.

With ACIC portfolio conversion to managed hotel under Marriott, coupled with the integration benefits with our existing Marriott portfolio, we should sce material margin improvement over the coming quarters.

In the last reported quarter, our same-store assets, which excludes the recently acquired ACIC portfolio and the Caspia Pro in Greater Noida, which is under renovation, delivered a 13% RevPAR growth in Q1 FY25, driven by robust demand as demonstrated in the office space net absorption and aviation growth in our core markets.

We arc currently renovating our 137-room Caspia Pro in Greater Noida and rebranding it to Holiday Inn Express, which is scheduled to open in October this year. Greater Noida tends to be a very strong market in H2, and this hotel will be open to benefit for that period.

We’ve also signed the agreement with Marriott to renovate and rebrand the two ACIC portfolio assets in Pune and in Jaipur, totalling 330 rooms.

Additional renovation plans to upgrade rooms and facilitics in Hyatt Regency Pune, Sheraton, Hyderabad, Fairfield by Marriott Hyderabad, and Four Points Vizag will further drive incremental revenue growth from these hotels.

We have sct a target of delivering about 10% to 15% inventory cater over the years. As of now, we are scheduled to open 163 new rooms in Calcutta and Bangalore between September and November of this year under the Holiday Inn Express brand.

We are also very happy to inform you that we have identified the opportunity to add 54 rooms at Sheraton Hyderabad by converting some underutilized F&B and third-party leased office spaces. As you know, Hyderabad is a very strong performing market, and being able to add 54 rooms is highly accretive.

Seeing strong performance of the hotel in Sriperumbudur, which is Fairfield by Marriott, we are starting to plan the addition of 80 rooms there, and we expect that the total incremental revenue from the additions that I have just spoken about will be in the zip code of about 70 crores.

In addition to these internal growth opportunities, we also have a very highly visible and actionable pipeline of both acquisition turnarounds and long-term variable leases. These have the potential to add at least 25% EBITDA on FY "24 pro forma basis.

So we think these three — Greater Noida will be a complete new addition, even though if’s a rebranding. And Punc and Jajpur have a significant EBITDA upside between those two assets.

So, Caspia, Delli, current, we alrcady have a contract signed with Marriott for a Fairficld by Marriott, We have not yet started the work on this asset. This is one of the assets that we would consider, you know, to be part of our asset recycling strategy. And that’s why we’ve held it for renovation. Vizag, is an asset where there is no rebranding. Ifs just improvement in the guest rooms. We have completed the planning cxcreise. I think by the end of the year, we’ll have the markers completed. And then we’ll start the work on that hotel.

The total repayments due over the next 12 months is about INR50-0dd crores, - INRS0 crores, INRSS crores. So as far as repayments are concerned we have a very strong profile of repayments over the course of the next 10 to 12 years. Only the ‘maturity due is in Jan 2027 which gives us adequate time to refinance that.

Not major supply is coming in Hyderabad, Pune, and Gurgoan, where we are expanding.

Navi Mumbai- So as of today we expect about 1,300 rooms as the stated supply in that market. Existing supply is 1,300. We think if everything gets added by end of FY28-29 we expect this to go to about 3,000 rooms so that’s doubling almost doubling of supply, butif you look at it from an absolute perspective 3,000 rooms catering to New Mumbai airport and whatever is happening in New Mumbai that’s just about Aerocity.

we are guiding towards 10% to 15% inventory CAGR over the years.

We believe that cities sometimes tend to be more important than segments . Ifyou look at the RevPAR growth by cities we’ve scen Bangalore grow almost at about 17% year-on-year. No surprises. Largest office market in terms of net absorption.

The sccond highest growth rate was both in Hyderabad and Pune in the zip code of about 16% cach, again driven by the growth of the office markets. NCR was at about 10%. And if you look at ow portfolio spread, Jinesh, right, almost 70% of our revenues come from Bangalore, Hyderabad, Pune. And if add NCR, about 80%. So when you have, you know, your presence in markets which continue to have good growth in terms of office space, the weighted impact reflects in the overall portfolio, right?

Two, we will also clarify that we don’t operate in leisure markets, right? And therefore, we tend to probably over the years deliver more stable growth rates, because leisure markets are the markets which tend to have higher fluctuations between seasonalities . Business hotels also have scasonality, but not to the extent that you will see in leisure markes.

The integration of ACIC portfolio is going exactly as planned.