Will you give higher multiple if they own asset or on asset light business? Does anyone have comparison data of peers along with Samhi, who owns property vs. who are playing on renting/lease model? & Why ?

Will you give higher multiple to own brands (Like IHC - Taj, Lemon tree) vs. tie-up of brands like marriot etc. ?

I am currently studying this sector & invested in recently listed IPO - Ventive hospitality. Both Ventive (Not much people are aware that it actually doesn’t trade at 50 EV/EBIDTA but actually on FY25 EBIDTA it will trade at 15-16 times) & samhi’s (may be around 11 times for FY25) lower valuation amuse me when compare with peers. Also I think both ventive & samhi owns property & doesn’t have own brands but have tie-ups.

So, market is giving lower multiple because of this reason ? It’s trap or opportunity?

Good breakdown of numbers.

The EBITDA per key here would be 12,64,366*21%= Rs 2,65,520 which is half of even the midscale Holiday Inn Portfolio.

With an estimated annual EBITDA of Rs 3.2 crore, the hotel has been sold at 16.7 times multiple on an EV/EBITDA basis. The asset,sold at a premium to Samhi’s current valuation, does an EBITDA margin, which is essentially half of Samhi’s portfolio average, which in my view augurs well for the outlook of Samhi going forward.

D: Invested.

Before August 2024, Ventive Had Only 1 Hospitality Property (JW Mariott Pune) And 4 Office Assets. In August 2024, promoter (panchshil realty) transferred 10 properties (Hotel) to ventive.

So, Whatever valuation of EV/EBIDTA of 50 is coming based on FY24 numbers (where they only had1 hotel). So, if you take proforma based data (Of all combined properties of 11 hotels) of FY24, EBIDTA was 870 cr. with Occupancy of 60%. Plus they have added 1 more property in maldives in Q2FY25. So, assuming moderate growth also, FY25 EBIDTA will be 1050-1100 cr. with market cap of 16k cr. at current price.

Yes Blackstone has 32% stake & even promoter holding is 88% so eventually they will come in market to reduce it to atleast 75% in 3 years, that overhang will be there. Also very high concentration to Pune (60% hotel rooms + all 4 office assets) & maldives is the key risk there.

Thanks. I was looking through the DRHP. So got bit of the info.

The two risks are real and will cap the upside. But Pune is also a stronghold for them. Additionally, I believe office assets are 95%+ occupation, so growth over there will be dull.

Upside revenue depends entirely on the Pune Hospitality market, which is strong enough. The only key risk is consistent selling, which we have also seen in Samhi.

I’ve compiled insights from various discussions on this forum along with my own analysis. Everything from growth potential to risks and valuations as of 11/02/2025

For those new to researching the company, this should bring you on par with ongoing discussions. For those who’ve been following it for a while, I’d appreciate any additional perspectives or counterpoints to refine the thesis further.

In my opinion market is playing on multiple Mental models when they value SAMHI -

a) High float: There is no promoter, float is very high which can be one of the reason for consistent selling and downward pressure on stock price.

b) Key Person Risk: Mr Jakhanwala is astute leader and he has been doing many good things in the business but market is Cognizant of the fact of no promoters is discounting on this risk.

c) IPO lock out Period: This might be short term blip, when the IPO lock-in expires in the March, we may see some more correction maybe but because of uncertainty involved, there is constant pressure on price.

But when we look at the hospitality industry demand is outpacing supply in almost all the major cities and we have been hearing this point constantly in the interviews from the Management and there is bullish tone in this sector for next 3-4 years.

Even with government giving tax benefit and trying to boost consumption will have some bit of benefit passed on to travel and tourism sector.

Overall this sector and SAMHI as a business looks very gloomy. I’m optimistic on this sector and SAMHI (being undervalued compared to competitors), have been adding on the dips.

Will track and remain invested for 3-4 quarters and change my stance if above factors overshadow the good business.

Can you please share which IPO lock-in period are you referring to?

I checked about the lock-in periods and came across following periods:

Anchor Investors:

50% of the allotted shares were under a lock-in period that ended on October 22, 2023. The remaining 50% had a lock-in period ending on December 21, 2023.

Promoters and Pre-IPO Investors:

As per the SEBI regulations, promoters and pre-IPO investors are typically subject to a lock-in period of 6 months/180 days from the date of listing. Given that SAMHI Hotels was listed on September 22, 2023, this lock-in period was concluded on March 21, 2024.

Lock-in period is not for all IPO or pre-IPO investors. This is for ACIC MAURITIUS, BLUE CHANDRA PTE. LTD and GTI CAPITAL ALPHA PVT LTD.

Refer Shareholding Pattern Public ShareHolder

In terms of an absolute number of where we expect the gross or the net debt to be over the

next let us say, 3 years, we actually think that it will be closer to Rs. 1,700-Rs. 1,800 crores of

net debt over the next let us say 2-3 years and that will be a factor of really the cash generations

and asset recycling. So, we see Rs. 1,700 - Rs. 1,800 crores of net debt in the business and this is without any so to say, expectation of the capital raise for an external capital.

I have observed that most Indian hotel chains are increasingly adopting an asset-light model to achieve higher growth and scalability in the hospitality sector. This approach focuses on managing properties through contracts rather than owning them, enabling faster expansion with lower capital investment. In contrast, Samhi Hotels follows a property ownership model, investing directly in real estate assets rather than relying solely on management contracts. This difference in business models raises an important question: does the market value these approaches differently? Since a company’s chosen business model significantly impacts its financial performance, risk profile, and growth potential, it plays a crucial role in determining its valuation. Consequently, the market may assign different EV/EBITDA multiples to each business model based on its perceived strengths and risks. Understanding how investors perceive these strategies can provide valuable insights into the dynamics of the hospitality sector. I’d be interested to hear others’ views on this topic as well.

Asset light model is good in an upcycle and worst in an downcycle. This is like a service company. Once you own the property than book value also increase and you have more cushion during down cycle hence valuations are higher. Chalet Hotels is best comparison as model is similar.

But isn’t a revenue sharing model. In that case in downturn, both Operator and Asset owners suffer. Infact asset owners may struggle to service debt. Operator has limited investments compared to asset owner.

I wrote about SAMHI almost 9 months ago. My thoughts about increasing allocation to it.

The management continues to execute well on all relevant fronts and the hotel upcycle (based on air traffic, incoming supply, and office space absorption metrics) continues to hold well, especially in the markets relevant to SAMHI (Pune, Hyderabad, Bangalore, and Delhi).

All the relevant metrics (RevPAR, ARR, Occupancy, Supply incoming in the relevant cities, Margin Expansion, Reduction in Other Expenses, ACIC portfolio) have been better or at least as per expectations. SAMHI has done better than most peers. The only metric that we think management can do better is Debt Reduction.

An incremental positive is the fact that they are inclining their portfolio more towards the cities/ markets which are doing good. This has heightened the debt levels more than I would have wanted for the short term. However, the management is continuously looking for asset recycling (from markets they see weakness in) and is not looking for any further acquisitions for at least the next 2-3 years which should reduce the debt pressure along with the free cash flow.

Don’t get me wrong! The debt has reduced but not at the pace we want it to! Tho the recent management guidance for their capex plans for FY26, 27, and 28 are less than my expected Cash Flow generation from the business. The latest guidance is 1700-1800cr of net debt in the next 2-3 years. This would have affected our IRRs on the investment, but considering how much the stock has fallen (~25%, which is actually better than the small-cap and mid-cap index), we increased our allocation.

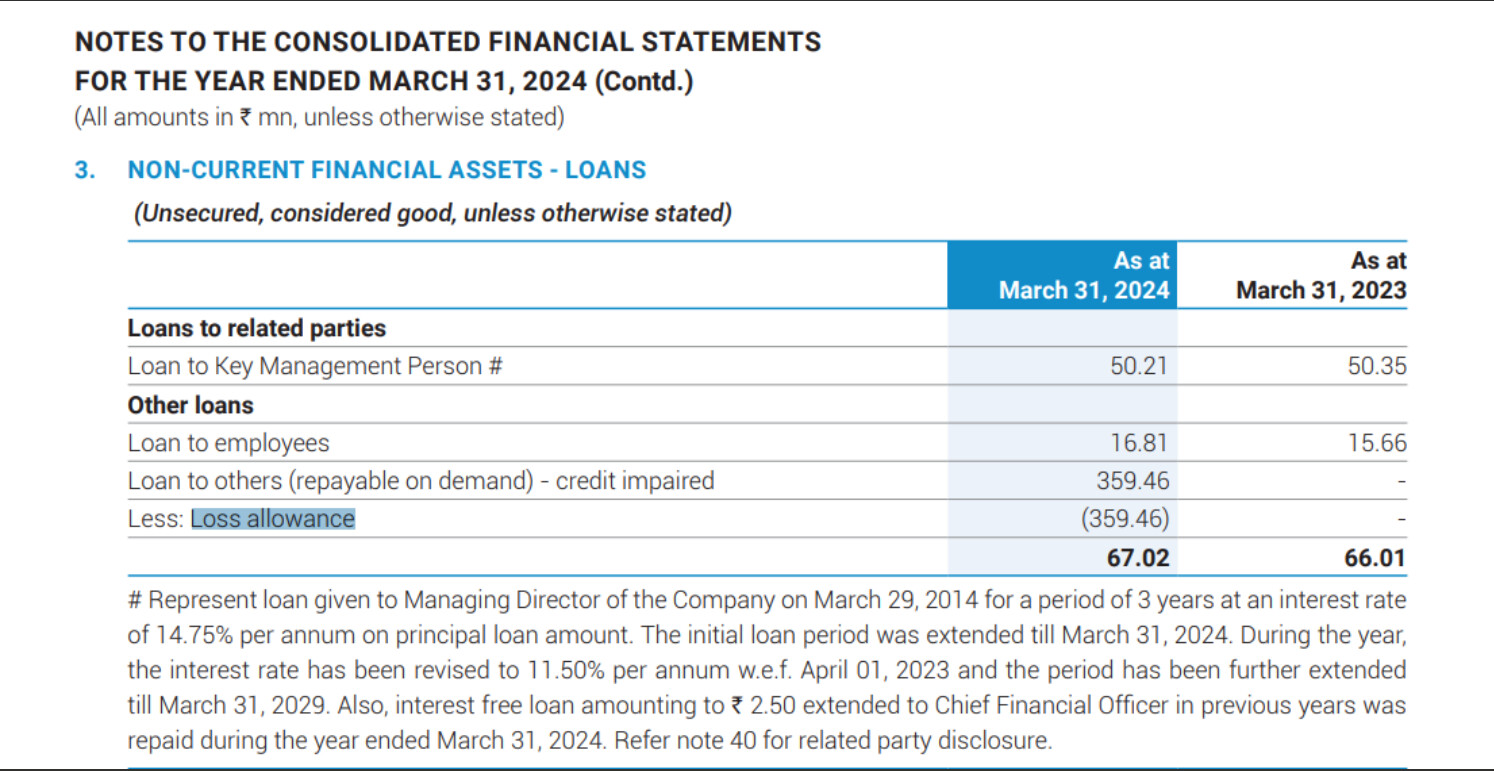

This has been shared earlier on the thread. Does anyone have any insights into this loss allowance taken. I have written to the IR contact and hopeful for a response soon.

As you rightly pointed out, only concern is their debt and management’t willingness to live with the debt rather than trying to reduce it. If economy slows down, that will be a rude awakening. I hope mamagement pull together a plan for an aggressive debt reduction.

@DeveshKedia@himanshu.dugar@Nishant_Sampat

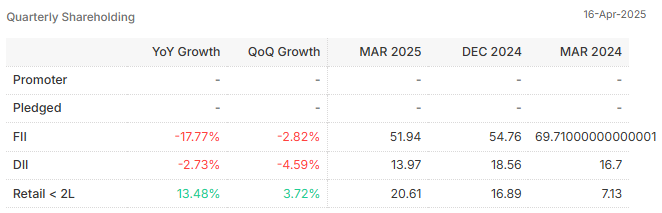

For Samhi even after sectoral tailwinds, in March 2025 quarter FII & DII are decreasing their holdings. On the other hand retail public allocation has increased.