I feel the cycle can continue as we embark on a rate cutting cycle. While debt is planned to be managed, debt is highly required in such a business … Chalet also has high debt. As that’s the way you can acquire hotels faster rather than waiting for internal accruals or dilution. I think people are ignoring the operating leverage that will come to play. You can’t just look at top line and decide company has not performed … 30% EBITDA growth YoY is very respectable!

13 Likes

I will not compare Chalet with Samhi, given Chalet’s high promoter holding of 67%. Clarity from PE investors should come up after 21 March, if they choose to stay invested, then we might see mutual funds entering the stock.

1 Like

SAMHI Hotels -

Q3 FY 25 results and concall highlights -

Revenues - 298 vs 273 cr

EBITDA - 114 vs 90 cr

PAT - 23 vs (-) 7 cr

Q3 Rev Par @ Rs 5088 vs Rs 4248 ( up 15 pc YoY )

Segment wise RevPar growth ( except the ACIC portfolio - where the integration process continues ) -

Upper upscale - 16 pc

Upper Midscale - 18 pc

Midscale - 10 pc

Contribution to room revenues from -

Indian bookings - 66 vs 57 pc YoY

International bookings - 43 vs 34 pc YoY

Company profile -

Operate a total of 31 Hotels, 4800 rooms in 13 cities under 8 brand names

Upscale Hotel rooms - 1074. These include properties like -

Hyatt @ Gurugram and Pune

Sheraton @ Hyderabad

Renaissance @ Ahemdabad

Courtyard @ Bengaluru

Total - 5 hotels

Upper Midscale Hotel rooms - 2163. These include properties like -

Four Points @ Pune, Vizag, Jaipur, Chennai

Fairfield by Marriot @ Bengaluru (03 hotels), Coimbatore, Chennai (02 hotels), Hyderabad, Goa, Ahmedabad

Caspia @ Delhi

Total - 14 hotels

Midscale hotel rooms - 1564. These include properties like -

Holiday Inn Express @ Pune (02 hotels), Ahmedabad, Bengaluru, Nasik, Hyderabad ( 02 Hotels ), Gurugram, Chennai, Nahsik

Caspia Pro @ Noida

Total - 12 hotels

Growth Capex schedule to be operationalised over next 2-3 yrs -

Opening of Holiday Inn express - Kolkata ( will add 110 rooms ) - should open in Q4

Addition of rooms in Holiday Inn express - Bengaluru ( will add 54 rooms ) - should open in Q4

Renovation and rebranding of Caspia Pro greater Noida to Holiday Inn Express ( will add 137 rooms ) - started operations in Dec 24

Addition of 22 rooms @ Hayatt regency Pune - should go live in next FY, H1

Addition of 54 rooms @ Sheraton Hyderabad - should go live in next FY

Caspia Delhi - conversion to Fairfield by Marriot + addition of 142 rooms - scheduled to go live in FY 27

Four Points by Sheraton, Jaipur - conversion to Tribute by Marriot + addition of 114 rooms - scheduled to go live in FY 28

Fairfield by Marriot, Chennai - expansion of rooms by another 86 rooms - scheduled to go live in FY 28

Conversion of newly acquired office building to a 5 star hotel near Hitech City Hyderabad - 170 rooms - scheduled to go live in FY 27

Westin and Tribute portfolio - Bengaluru - 360 rooms - scheduled to go live in FY 29

Capex required to fully operationalise all the newly acquired assets in Bengaluru and Hyderabad should be - 80 cr to rebrand the existing Bengaluru hotel + 270 cr to add 200 to 220 rooms at the Bengaluru site + 180 cr of Capex at the Hyderabad site to convert the Office building into an Upper Upscale hotel. So this amounts to a total of 480 cr of Capex to be incurred over next 2 yrs. This should also take care of growth for next 3 yrs

Net Debt @ 2060 @ 9.4 pc

Net Debt / EBITDA @ 4.3 X. Aim to bring this down to 3.5 X by end of FY 26

Q4 is generally the best Qtr for the company. Should remain that way in current FY as well. Should easily report double digit revenue growth in Q4

The ACIC portfolio reported a 300 bps margin expansion on the EBITDA level. However, the revenue growth was flat for the ACIC portfolio. This is because the company deliberately focussed on premium / high margin end of the business and let go the low margin business. Revenue growth should start kicking in wef Q4 for ACIC part of the portfolio as well

Capex lined up of 200 cr for FY 26, 150 cr each for FY 27,28

Company believes their Consol EBITDA levels should inch upto > 40 pc in medium to long term

Current rate of Cash generation is > Capex + Interest expenses. So this surplus cash will keep flowing towards reduction of Gross Debt. Plus company can also go in for some asset re-cycling / hiving off non core assets - which can also be used to reduce Debt

Over medium term, company aims to maintain net debt of 1700-1800 cr of net Debt on the balance sheet ( on an expanded EBITDA )

City wise RevPar growth -

Hyderabad - 24 pc

Bengaluru - 20 pc

Pune - 17 pc

Even if there is no Rev Par growth for next 3 yrs, company is still expected to report 35 pc growth in topline because of all the capex that’s expected to go live in next 3 yrs ( as listed above ). If they r able to get 5-6 pc Rev Par growth, the total topline growth in next 3 yrs may well exceed 50 pc . The growth in EBITDA may be much higher because of the operating leverage

Interest cost should come down wef Q4 ( to aprox 50 cr vs 55 cr in Q3 ) as the overall cost of borrowing has reduced

Expect some asset recycling from the company in near future. Negotiations are in advanced stages - this can be a potential re-rating trigger

Disc: holding, biased, added recently, not SEBI registered, not a buy/sell recommendation

10 Likes

Full Disclosure: I had the stock before. Got out at almost nil profits.

Now coming to the stock. Why is everyone hyped or in love with this company. Yes, it has good assets and has strong branding tie ups for its hotels. So do many more. You have Ventive, chalet etc. Leela is in process of listing having submitted its DRHP.

Also why is the asset space so loved when you have other companies move to an asset lite business. Why is that EIH, IHCL and Lemon Tree moving to this model. Players like IHCL can fund asset buys at much lower interest rates than someone like SAMHI.

Still, it dosen’t. Worth pondering.

We are likely at peak of ARR. While there is indications of supply being lower than demand for next 2 years, it will not last far beyond that, Thats when an Asset heavy player gets hit.

Anyway, reasons why i got out. My 2 cents and all that.

8 Likes

Our job is to buy business at good valuation,till now business has performed very well but price isn’t appreciating,Now if industry cycle changes and supply would overcome demand then we have to exit.It would be our bad luck.If business hasn’t performed till now we would have reasons to exit now if stock price isnt appreciating we cant find reasons.Let’s wait for market to value the business and after that what will be result we would accept with full integrity

7 Likes

I think people liking the stock has to do with multiple factors - one of the strong reasons being the relative undervaluation, probably due to it being a turnaround story.

I was doing a little bit of unit economics on SAMHI yesterday. Consider this scenario:

- You are getting to buy a hotel key in SAMHI at a price of just below ₹ 100 Lakhs (EV per key given the current market price).

- Around 40L of it is funded by debt and the rest is in your direct ownership.

- You are getting ₹7.7L of rental income after expenses for this hotel key (TTM EBITDA per key).

- Now, granted, you will pay around ₹4.8L as interest on the debt every year from this (TTM Interest per key), but you’ll still be left with a very respectable ₹2.9L of rental income after debt payments every year per key.

People continue to buy real estate with much worse yields in today’s world, so why not a hotel which has added brand value and physical assets in prime real estate locations?

Also, contrary to many people here, I personally like SAMHI’s asset ownership model for the very simple reason that I’d like to own something tied to physical assets in the real world. There are far too many asset light business model options available today, and just owning intangible assets doesn’t really translate to a secure feeling for me, but then again, that could just be me.

When Elara Capital gave a buy call on SAMHI, it was trading at a share price of 189 and an EV per key of INR 110 Lakhs. Any fall from the current price would make the EV per key metric much more attractive, surely? Please let me know if I’m missing out anything here.

Disclosure: Not invested, but very much interested and looking to buy at a cheap price if everything else checks out.

14 Likes

There is a saying in stock market, “price is god, Bhav Bhagwaan hai”. It is difficult to dissociate with price when you are buying a business. Bear markets brings lot of opportunities just because of human behaviour as donkeys and horses both go down due to low volumes, large investors stay away as they buy business. Samhi was trading at 200 last year Jan when everything was in a loss and dropped by 40 rupees and soon will be available at IPO listing price of 150 when things are really looking promising. ![]()

![]()

Lemon tree has 29% promotor stake, 370 cr Q sales, 2000 cr debt, EV/EBIDTA 28, market cap 11000 cr. Samhi has some committed promotors stake at 21-22%, debt 2000 cr, sales 300 cr Q, EV/EBIDTA 20, market cap 3500 cr. Keepings your emotions in check during bull and bear markets only can assist in right decision making.

19 Likes

Thanks to the replies form everyone. What i have observed is markets take a fancy to a particular stock in the sector, like with IDFC in Banking. Its sometimes got less to do with fundamentals and sometimes it is following the herd.

Just look at discussions on this vs other asset plays. Look at discussion on IDFC vs other banking stocks. My limited point is let’s be careful with herd driven stocks.

Sure. Here the proability of change of business cycle correlates to expected growth of company in terms of PAT as interest on debt reduces. So how do you correlate the risk.

Also stock is now listed for a year. The market has given you the value. Look at how other stocks have performed.

Agree I am not here to discuss this.

-

Stock is cheap for precisely a single reason. No one knows when debt reduction will happen. Normally asset plays should be build on mix of internal accurals, debt and equity. When is there going to be internal accurals. Also this is a cyclical sector. Please observe 2012-2020. What happens when ARR and occupancy drop 20% and 10%. How do you pay interest let alone payback debt.

-

Asset plays generally do not work in India. Reason is cost of debt and cost of asset is to high in proportion to income arising from the asset. As a country we do not have asset to low cost debt. Still you can look at NESCO or a Phoenix mills.

-

That 2.9L of income has significant expenses in terms of high maintanence, hotel labour.

Agree, I am not arguing that lemon tree is priced well.

Please note that lemon tree does own the brand and does not have to pay royalty on someone else’s brand. Also moving to a franchisee and Asset Lite management model. Rest I have no skin in this game. I do not own single hotel play currently.

10 Likes

- I don’t think the stock is cheap merely due to questions looming over debt reduction. Lemon Tree has a comparable Debt/Equity ratio, and yet it is valued at ~22 EV/EBITDA. Yes, the risk of debt defaults is there, but I think there’s a good runway for the next 3 years or so, unless a black swan event occurs.

- This I agree. Assets may not produce lucrative cash flows in the Indian scenario today. The pricing of general real estate in India itself might be a bubble. But people have been saying this for decades, and still keep buying real estate.

- The 2.9L income comes after all expenses. It’s EBTD per key. It comes after even the interest on debt is accounted for. Only depreciation and tax is not accounted for. Very much comparable to rental income, and a good one by current real estate standards.

Thank you for your point of view! It’s interesting to see what different investors value in different companies. I’m in no way saying SAMHI is a screaming buy - I don’t have the valuation or industry expertise to claim that. But I do know that if stocks can irrationally go up on euphoria, it can just as irrationally come down on severe pessimism. I sort of believe we are in the latter cycle now for this stock.

10 Likes

They keep saying they are a business hotel group but going by the number of ‘Holiday inns’ in their portfolio i think they are working around that.

The 10% increase in topline is simply unacceptable when all other peers are doing 15-25 percent… The real reason is that they are holding quite a few duds at the moment in their 31 hotel portfolio … this concall we came to know that the delhi shalimar bagh property was not contributing to the ebitda … plus when prodded more in the concall they admitted that the ACIC portfolio has been flat … for a year or more now …

SAMHI correction in share value is a reflection of their inability to grow along with the industry… they had to do the IPO to pare down the debt which was becoming unserviceable…they went for the ACIC aquisition so they could get inorganic growth …well they have it on paper in terms of number of rooms but it’s not happening on ground…

Mgmt has given themselves no room for further excuses from Q1 of next year as they will start comparing figures for entire Portfolio and not ex ACIC… while in the near term the share price may technicallycorrect till 147 where it previously got support, it should be giving out strong q4 numbers in terms of net profit and i maintain that at some point of time it will be a great acquisition propositon for the big real estate hospitality players still playing monopoly…

I swallowed the bitter pill at 172 and booked loss, the biggest till date …I wish those still holding all the very best and I hope that I will regret that I didn’t have stomach to hold on to it when it eventually reaches my target … But as I take position in only 1 stock at one time it was a question of better immediate alternative which has helped me cut down part of the booked loss

Wish they didn’t do that 6.5 crores expense adjustment from net profit…30 crores wouldve given better optics to the market participants…

16 Likes

There is no issue in selling stock and getting out once you lose conviction, current market is offering several opportunities. Main difference between a asset light model and capex heavy model is that asset light model is a service company and margins are volatile so the valuations. You need to pay fixed lease to owner, run hotel and generate margins. In a slowdown scenario things changes very fast before you realize.

Companies owned hotels will be always valued higher as their survival in downturn is higher and book value will keep increasing due to real estate holdings.

Lemon tree operates maximum in 3 star section, volume is much higher as only agreement need to be signed.

Marriot, Hyatt, Sheraton are proven brands and will remain in 4 star and 5 star hence occupancy and margins will be higher in upcycle.

We really don’t know how long we are in Hotel upcycle as its a cyclical business but if Indian per capita catches up faster than this might be a structural boom also like what happened in europe twenty years ago. Marriot is expending in India very fast and they might have done ground research.

Current price of Samhi is like getting a dollar in 50 cents. Valuation corrections happens in stock market with time both upside and downside, we need to make sure where are we betting. Dmart was Shahrukh Khan in 2019-2021 and Shakti Kapoor now😂. No problem with Dmart, they are expending and generating profits however people paid 5 dollar for a dollar for years after its listing and now value is catching with time correction, still down 35% from its peak.

12 Likes

Loving the stock vs loving the undervaluation are 2 different things. Price is an output out of our control. Earnings increase per expectations is what we can predict and track.

3 Likes

I dont think book value has any relation with increasing real estate prices. Managment has to depreciate assets regardless. But I agree with your point that Asset heavy business have better clarity in cashflow hence can command relatively higher valuations.

When everyone is optimistic, that is usually the peak. When everyone is all doom and gloom, it’s usually the bottom. When even long term holders are disappointed and fed up, who is left to sell. Even the PE players won’t exit at ridiculously low valuations.

1 Like

Probably he meant real book value.

Since I believe balance sheet book value of any real estate heavy business is always less in India.

But in case of any severe slowdown/cash issue etc , its always an option to sell some and get the cash needed .

(My simplistic view)It’s like buying 20 apartments on loan and using the rent to pay the interest. If apartment value doubles due to real estate boom and I couldn’t generate enough rent. I always have an option to sell 10 apartments and pay complete loan.

So increase/decrease in real estate prices do have major impact. On paper book value don’t increase/decrease much but it increases/decreases in real .

2 Likes

Yup, you got it right, this was my thesis on safety of margin. Actual book value should be much higher seeing real state price rise in last 2-3 years.

3 Likes

One problem arises in down-cycle - Assets are sold at distressed prices because no one wants to buy. The realised value of a real estate (such as hotels) go down during a down cycle.

That is where the management style comes into picture - Managements should buy hotel real estate when the industry is distressed, at lower valuations.

My opinion is that SAMHI has acquired hotels during up-cycle which is completely opposite of what a smart operator does.

14 Likes

SAMHI Hotels Ltd announced on February 10, 2025, the signing of a Share Purchase Agreement for the sale of its 100% stake in Duet India Hotels (Chennai OMR) Private Limited to Greenpark Hotels and Resorts Limited for INR 535 million.

5 Likes

My opinion is that SAMHI has acquired hotels during up-cycle which is completely opposite of what a smart operator does

I am not sure if its true. They started in 2010.

Major acquisition were in 2010, 2012, ,2016, 2018, 2023

For a company this new, it’s impressive of a management to achieve this growth and obviously it would require major debt.

Disclaimer: Biased, Invested (2%)

7 Likes

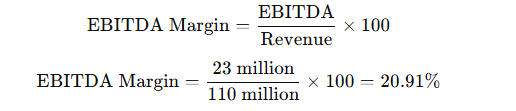

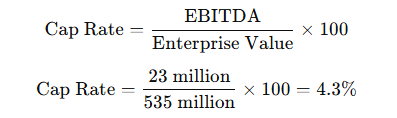

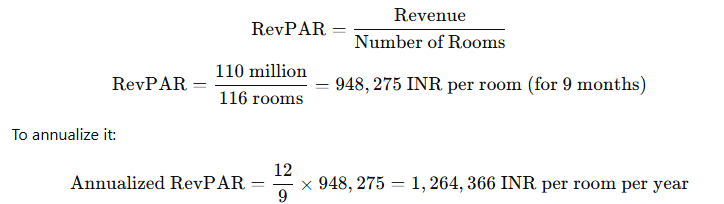

Calculations for stake sale of Fourpoint by Sharaton, OMR Chennai

- Revenue: INR 110 million (for 9 months)

- EBITDA: INR 23 million (for 9 months)

- Net Loss: INR 33 million (for 9 months)

- Number of Rooms: 116 rooms (Four Points by Sheraton, Chennai OMR)

- Enterprise Value: INR 535 million

Calculations for the following key metrics:

- Annualized Revenue

- EBITDA Margin

- Net Profit Margin

- Capitalization Rate

- RevPAR

- Enterprise Value per Room

Annualized Revenue

The annualized revenue is INR 146.67 million.

EBITDA Margin

The EBITDA margin of 20.91% indicating less profitability than SAMHI’s 37% OPM last quarter.

Net Profit Margin

The net profit margin remains -30%, which reflects a loss making asset for SAMHI.

Cap Rate

The Cap Rate of 4.3% , reflecting a good sell value in relation to the profitability.

RevPAR (Revenue per Available Room)

Now, let’s calculate RevPAR based on the 9-month revenue.

The annualized RevPAR is INR 1.26 million per room, which comes to around INR 3464 per room.

Enterprise Value per Room

Finally, let’s calculate Enterprise Value per Room.

The Enterprise Value per Room is INR 4.62 million, which reflects the value placed on each room during the sale.

Conclusion and Industry Benchmarks:

- The Cap Rate of 4.3% and negative net margin signal underperformance, which could be a key factor behind SAMHI’s decision to sell the asset.

- Industry Standards:

- RevPAR: Typically ranges from INR 5,500 to 8,000 per room per night for mid-range hotels in chennai.

- Enterprise Value per Room: For mid-range hotels, it typically ranges from INR 3-6 million.

Disc. - Invested. Biased.

17 Likes