Not necessarily. We shouldn’t forget that there were some IPO lock-ins expired in March.

I feel this is a decent mix given the current supply in terms of expired lock-ins. There are also chances that they’re waiting for higher levels to make an exit.

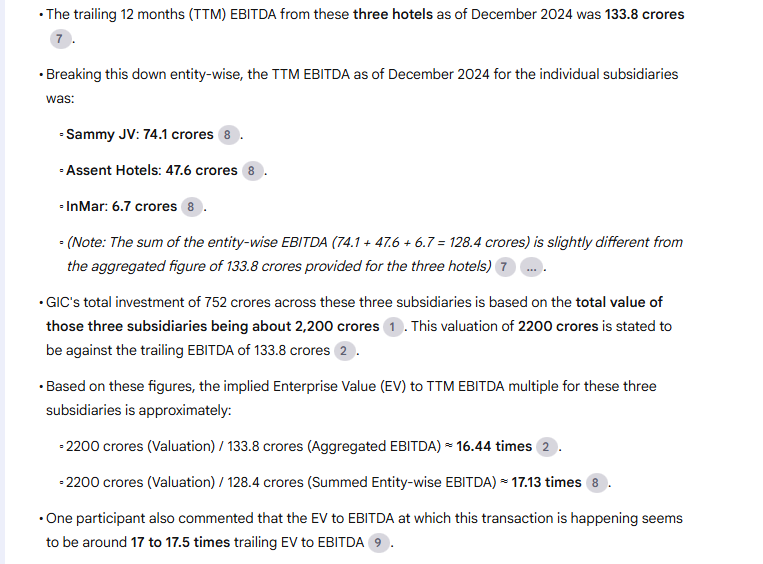

As stated earlier, Golden period started for this stock today, GIC invested 2200 cr. Debt reduced from 2070 cr to 1460 cr, Debt/ EBIDTA level now at 3.5, interest saving 60 cr, minority interest 43 cr. Increase in profit 16-20 cr.

Samhi Hotels has partnered with GIC to form an upscale hotel investment platform in India for upscale and higher-category hotels in India

GIC will invest ₹752 crore for a 35% stake in three upscale hotel subsidiaries (Courtyard & Fairfield by Marriott Bangalore, Hyatt regency Pune, Trinity Hotel Bangalore Whitefield)

the total investment implies a valuation of approximately ₹2,200 crores for the three subsidiaries

₹603 crore upfront will be used to reduce debt and a small amount towards deal expenses and ₹149 crore will be invested over 2 years to partly fund capex for the Westin and tribute Portfolio hotel

debt & balance sheet impact:

debt reduction of 580 crores

net debt to EBITDA at closing falls below 3.5x, better than earlier guidance.

they wants to reduce this below 3.0x within 12 months and target 2.5x long term without slowing growth.

the non-JV assets will initially have a higher leverage (around 4.4 times), but the plan is to normalize this across the portfolio over time

finanical upside

they see 15–20% upside in PAT driven because of lower interest costs and the creation of minority interest. this estimate currently only factors in debt reduction and not potential savings from lower interest rates

they see reduction in interest rates (currently around 9.4%) due to the stronger balance sheet and partnership with GIC

platform structure:

this JV structure will allow samhi to:

retain 65% control

earn 4% of EBITDA generated by the hotels as an asset management fee

this fee flows directly to the parent entity’s EBITDA

tap into GIC’s ₹1000+ crore future capital runway.

strategy and growth outlook

samhi will continue to see opportunities in the midscale segment

samhi prefers inorganic growth (acquisition + turnaround of assets) in the upscale space over greenfield development.

the partnership with GIC provides capital and credibility to grow the upscale platform beyond the initial three assets.

Q&A highlights

GIC is a long-only investor with a patient capital profile.

no immediate exit pressure; focus is on building a premium, cash-generating platform

no put options for GIC on Sami Hotels, except in an event of default

Though stock price ran significantly starting 15th Apr .I am assuming it was due to this partnership. Did the information was public or we missed something? If no , isn’t it insider info leakage?

One of the subsidiary, Ascent Hotels, has a debt of about 200 crores. The interest on this debt will also be shared in the JV ratio.

Out of the two remaining subsidiaries, one is already debt free and the other will become debt free after this transaction.

They are giving up 40 crores of EBIT for a 750-crore investment and 2200 crores valuation. GIC paid 55x EBIT, which is high…That’s how one should see it. That’s actually pretty good.

need to change my mind here and look at it with fresh eyes.

But you’re understanding is right.. We’re giving up some EBIDTA for upfront cash to reduce debt levels without equity dilution. And we’re getting a fantastic partner who will be active in operations as well as for future capital. This is definitely a win from SAMHI’s perspective.. Also, it’s heartening to listen to Ashish saying that they’ve heard investors voices loud and clear about the Debt and so this…

Just one change in the numbers here as per my understanding. The EBITDA at the consolidated level in the reported numbers will not change since GIC has acquired a minority stake.

Sorry bad…EBITA on TTM basis is 370 crore. Applying similar EBITA multiple we get a valuation of approx 6300 cr which is significantly higher than current MCap

Blue chandra and GTI have exited, founders are out of company when fundamentals are improving. ACIC Mauritius is biggest now. Don’t know how to take it, it has become REIT