Has Anyone attended the q2 Concall ?

Any Notes ?

Some quick notes from the concall:

- H2 steady growth expected

- smart grid, IOT devices, customised switch gears are growing

- smart grid requires advanced switch gear fuelling demand

- First order of 5cr for smart meters. Small step forward.

- 200cr worth of order which was earlier expected within smart meters this year does not look like a possibility this year. Next year confident for 700 cr though.

- Targeting margin of 11% by FY 26.

- DC fast charging and smart meters in the future to add significantly in the coming years.

- Other income includes shares of KC industry sold partly considering good valuation. Still holding 70% of the business.

- Expecting 12% margins for smart meters

- FY 26 Guidance - 1600 cr rev from switch gear, wire and cable and building. Plus 700 cr from smart meters with a blended margin of 11%.

- Fy 25 - 20 - 23% growth.

- Smart meter capacity is of 1000cr looking at the market 700 cr looks like realistic revenue target for next year.

- AMSPs have built big order books but the second line order from AMSPs to players like us is still in process.

- Building segment negative EBITDA for the qtr.

- capacity for set up for 100 chargers a month.

- total transformer business approx 250 / 300 cr. We are not into ditribution transformer. Low voltage segment. 690 V max. Application: building, equipments etc. Growth is good as It grew 30% plus.

If they meet their guidance of 2300 cr with 11% margin as per my rough calculation they can do about 125/130 cr of PAT which is about 14 times forward. Let’s see if the management can walk the talk.

Thanks for Notes !!!

FY25-20-22% growth with some improvement in margins.

FY26- expected 2300 Cr revenue, 1600 Cr from existing business and 700 Cr from smart meters.

EV chargers business issue will be solved by Dec’24 end, expecting significant revenue from FY27 with exisiting capacity of 100 Chargers/ Month at an Avg cost of 8-10 lacs. Capacity may ramp up in FY26

We can know about the guidance compliance by the Q4 end, key thing here is winning smart meter orders worth of atleast 300-400 Cr by Q4. This can give confidence in achieving 700 Cr or Revenue in Smart meters in FY26

FY26 should give some upside to the business

plus their 70 percent stake and synergies in kaycee

fy26-- 120 to 130 cr standalone PAT

120cr *30 times conservative should result in 3600 cr plus 400 cr kaycee stake with holding comp discount 4000 cr approx. should result in double of share prices. we can see many funds from MK fund to envision showing interest in meeting the Management and understanding the business projections.will see all depends on smart meters orders and execution

Agree with you, if every things goes well then they can do 120Cr PAT in FY26.

In addition to these new products some other legacy products demand is also going to boost as data centers theme is playing out.

We can expect the market cap to be near 4000 Cr by FY26 end if all goes well.

Salzer Electronics Ltd -

Q2 FY 25 results and concall highlights -

Q2 outcomes -

Revenues - 344 vs 280 cr, up 22 pc YoY

EBITDA - 45 vs 27 cr, up 32 pc ( margins @ 10.2 vs 9.6 pc )

PAT - 27 vs 10 cr, up 170 pc ( massive bump up in PAT is due to 15 cr of other income )

H1 outcomes -

Revenues - 701 vs 570 cr, up 23 pc

EBITDA - 69 vs 53 cr, up 30 pc ( margins @ 9.8 vs 9.3 pc YoY )

PAT - 42 vs 20 cr

Margin improvement in Q2 was mainly led by higher margin switchgear business. Q2 also witnessed some moderation in RM costs - a positive for the company

Company intends to maintain a balanced business mix between industrial switchgears and Wires + Cables division to maintain their overall margins

Company has received its first orders for smart meters - a testament to their team’s efforts in developing advanced smart meter technology

Q2 - product wise sales breakup -

Industrial switchgears and transformers - 61 pc vs 56 pc YoY

Wires and Cables - 34 pc vs 38 pc YoY

Building -electrical products ( like modular switches, MCBs, Changeovers etc ) - 5 pc vs 6 pc YoY

Q2 - geography wise sales breakup -

India - 65 vs 71 pc YoY

Europe - 11 vs 7 pc YoY

North America - 11 vs 9 pc YoY

Asia - 11 vs 11 pc YoY

Middle East - 2 vs 2 pc YoY

Company is already the largest supplier of rotatory switches to Indian Railways. Some of company’s top clients include - Schneider, Siemens, ABB, GE, ELGI, Valeo etc

**Aim to reach sales of Rs 1600 cr in FY 26 with increased EBITDA margins @ around 11 pc. Smart meters division is expected to contribute another 700 cr to company’s topline in FY 26. So - that would be a total of 2300 cr of expected topline in next FY. EBITDA margins in the smart meters segment is expected to be between 12-14 pc **

Beyond FY 25 - over and above smart meters, another pillar of growth that the company is banking on is DC fast chargers

The other income in Q2 results pertains to stake sale by a company in one of their subsidiary companies to the extent of 1.5 pc. Except for this other income, post tax profit would have been 13.8 cr

Out of the projected sales of 1600 cr for next FY, switchgear sales are expected to be around 50-55 pc of topline. Switchgear segment should clock an EBITDA margins of 12-12.5 pc. Rest of the sales are expected to come from Wires, Cables, Switches etc. The blended margins on this 1600 cr revenue should be around 11 pc

Don’t expect substantial revenues to flow in from the smart meters segment in the current FY

Company’s current capacity to make Smart meters stands @ 1000 cr / yr

WRT DC fast chargers, company intends to sell to both OEMs and to the Charging infra operators

The states where the initial installation of smart meters are expected to happen are - UP, Gujarat, Maharashtra, WB and Punjab. Next in line should be TN, Karnataka, AP

Govt has given out tenders for 13-14 cr smart meters in the first bout. Out of this, only 1 cr have been installed in last 1.5 yrs. The initial implementation has been slow. But is expected to now pick up pace as most of the high stakes elections are behind

The smart meters that the companies shall supply to the Govt are supposed to carry a 10 yr warranty and the suppliers are supposed to maintain them for this period of 10 yrs

Switchgears + Wires and Cables - both segments have grown by 20 pc in H1. This is due to increased economic activity, increased infra spending and capex by both Govt and Private players

In the building products division - company sells products like switches, circuit breakers, distribution boards, changeover switches and some other accessories. At present, company’s EBITDA margins in this category are negative. These r all retail focussed products. Company intends to grow this business in a slow and steady manner - without burning cash. In the medium term, company intends to grow this business to aprox 200 cr kind of topline

Despite the 1.5 pc dilution in their subsidiary company - Kaycee Industries, company continues to hold 70 pc stake in it

Company’s EV chargers are yet to get some critical approvals before they can start supplying / selling them. Company expects their products to get the requisite approvals by end of current FY. They already have the manufacturing capacity to make 100 EV chargers / month. Company expects the EV chargers business to really kick in post FY 26. Company has a technology tie up with a European player - Kostad for EV chargers business. They are an established player in Europe

Manufacturing fast EV chargers is not easy. It has taken them a 4 yrs long learning curve to be able to start manufacturing them

Company’s total annual revenues from their transformers business is around 250 cr. Their transformers business is one of low voltage transformers ( unlike most other listed players ). It’s for applications within various buildings, electrical equipment etc. Company doesn’t make power distribution transformers. This segment grew by 30 pc in H1

Current debt on books @ 320 cr

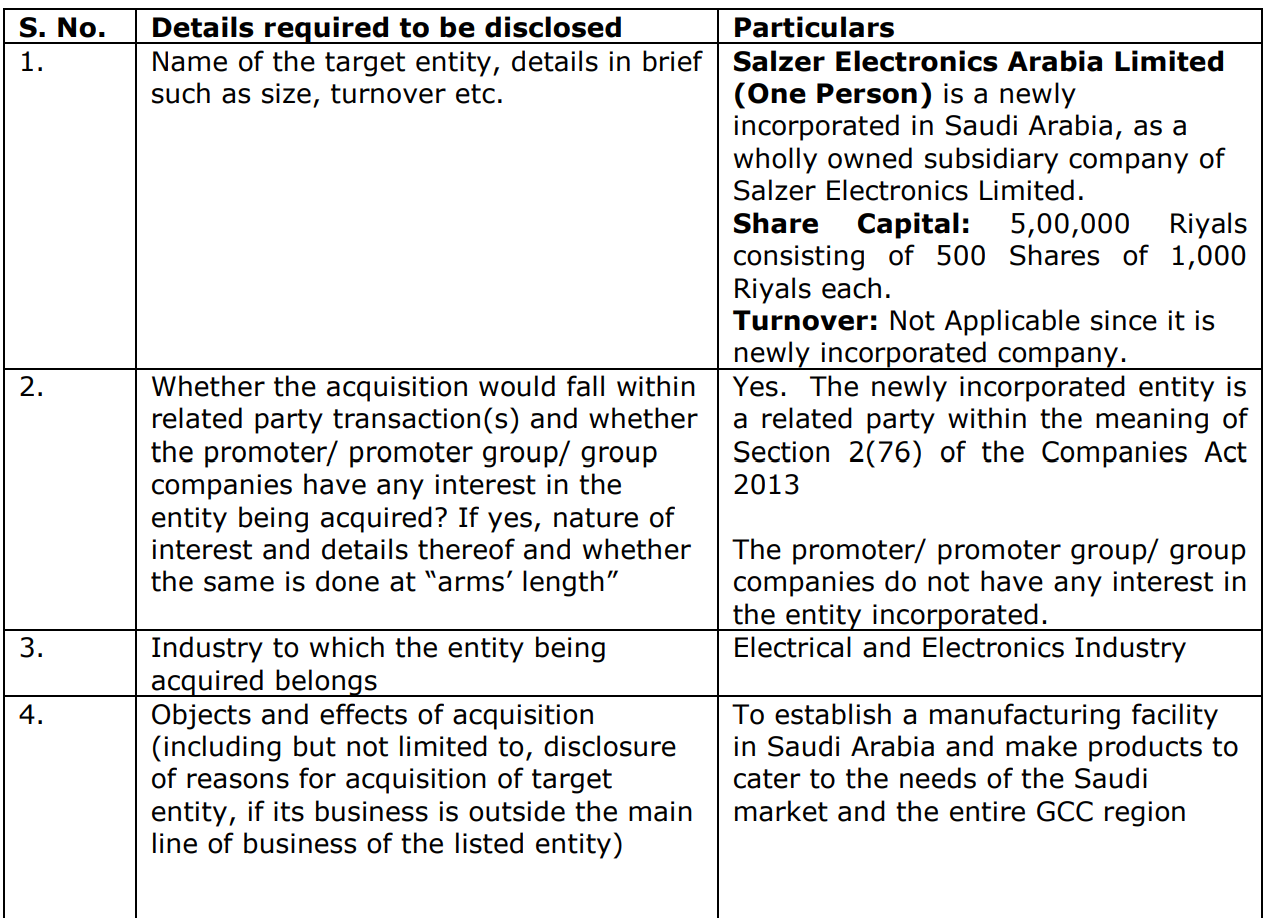

Company has set up a subsidiary in Saudi Arabia to make their Industrial swithgears. They intend to scale up their Saudi business to about 100 cr topline in 2-3 yrs

Company’s smart meters business has a good degree of backward integration. Its not merely an assembly business

Total addressable mkt in India for EV fast chargers may be around 8 lakh chargers ( once full fledged EV adoption happens ) - basically it should be 8 lakh chargers over next 8 - 10 yrs

Company’s installed capacity for smart meters should be around 40 lakh meters / yr - which corresponds to 1000 cr in annual revenues @ Rs 2500 / smart meter

Disc: initiated a tracking position, will keenly watch the progress of their smart meters + EV chargers business, not SEBI registered, not a buy / sell recommendation

Looking at the rally in the stock in last 1 month, seems like the statement made hold some truth.

Anyone tracking this company, can please share their research and outlook for next couple of years.

Disclaimer: - Closely tracking, started buying very small quantities.

I am tracking this company since last 1 year, getting order for smart meters is the key point here to achieve the expected revenue target.

We will get to know about this in Q3 & Q4 press release that how much order they have received.

If they achieve 2300Cr revenue with 13% margin then we will see EBITDA ~300Cr, which is 3x of FY24 & PAT would be in the range of 160-180Cr, which is ~4x of FY24 PAT.

Current rally could be due to optimism in the numbers, as management execution capabilities are very well exhibited in the past few years.

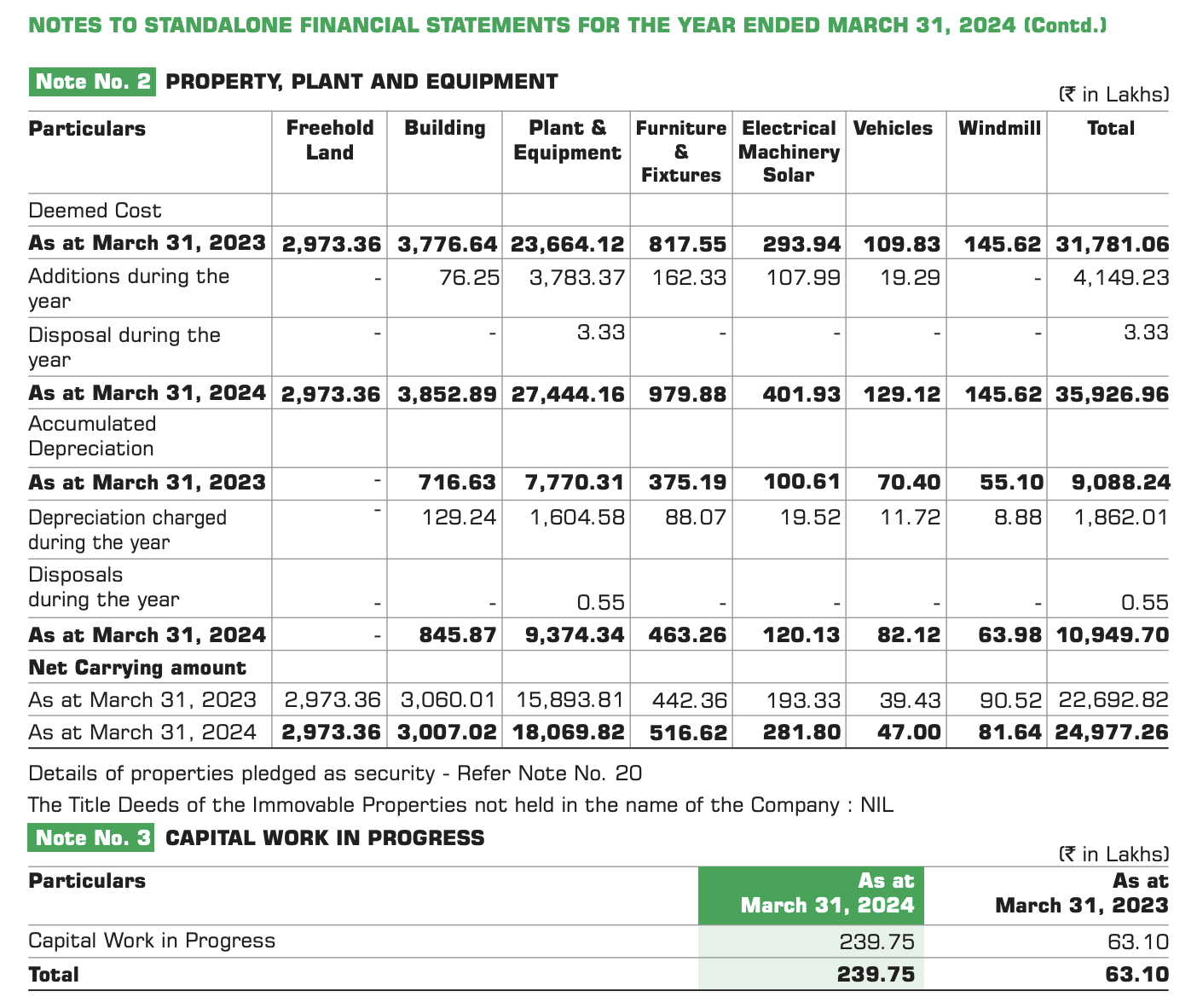

I was trying to figure out the cost to set up smart meter facility, couldn’t find it anywhere either in concal or annual report. I don’t see anything significant in CWIP or fixed asset.

Great observation. Please see FY 24 Annual Financial statements there is an increase in Capital work in progress, Plant and Machinery in the balance sheet, they have also started investing on CWIP and PPE in cashflow statement and Note 2 & 3 of Balance sheet. Though they have not expressly mentioned that this spent is on smart meters but we can assume.

Page 74 of annual report FY 24 also mentions

“Developments in Businesses during the Year:

Ø Salzer building “one-o f-its-kind Fully Integrated” Smart Meter manufacturing facility in India

to meet soaring demand”

Yes, I have seen it. CWIP is 2.3Cr while total addition in PROPERTY, PLANT AND EQUIPMENT was 41Cr is FY24 and 32Cr in FY23. But as mentioned by management, it has potential of generating 1000Cr topline at peak capacity utilisation, I am unable to understand how this small investment can generate such high sales? If someone can explain it, that will be very helpful.

I think it might be because Salzer already has a facility that manufactures most of the Smart meter components to supply them to other Smart meter manufacturers, This new investment should be an add-on to the existing facility which will enable them to build an entire Smart meter themselves.

They are already manufacturing some components of the smart meters earlier, so now they have invested very small amount ~20-30 Cr to start 4M smart meters capacity. Capacity can be enhanced by 6M more smart meters based on demand with some more nominal investment of 30-40 Cr

Yeah, makes sense. doesn’t that makes it very high ROIIC business? what took them so long to move up the value chain? So, return matrix should improve from here?

Recent cancelled contract to adani smart meter business by Tamil Nadu state government is beneficiary to salzer Electronics??

No, I have asked Mr. Rajesh 2-3 times regarding bidding in directly to the state Govt tenders but he told that as of now they want to supply to the AMISP’s but they are open for that option also.

Bidding for Govt tender require some more technical qualifications like past projects execution capabilities, which salzer doesn’t have.