Valuation of portfolio stocks - Part 2

Continuing from the previous post.

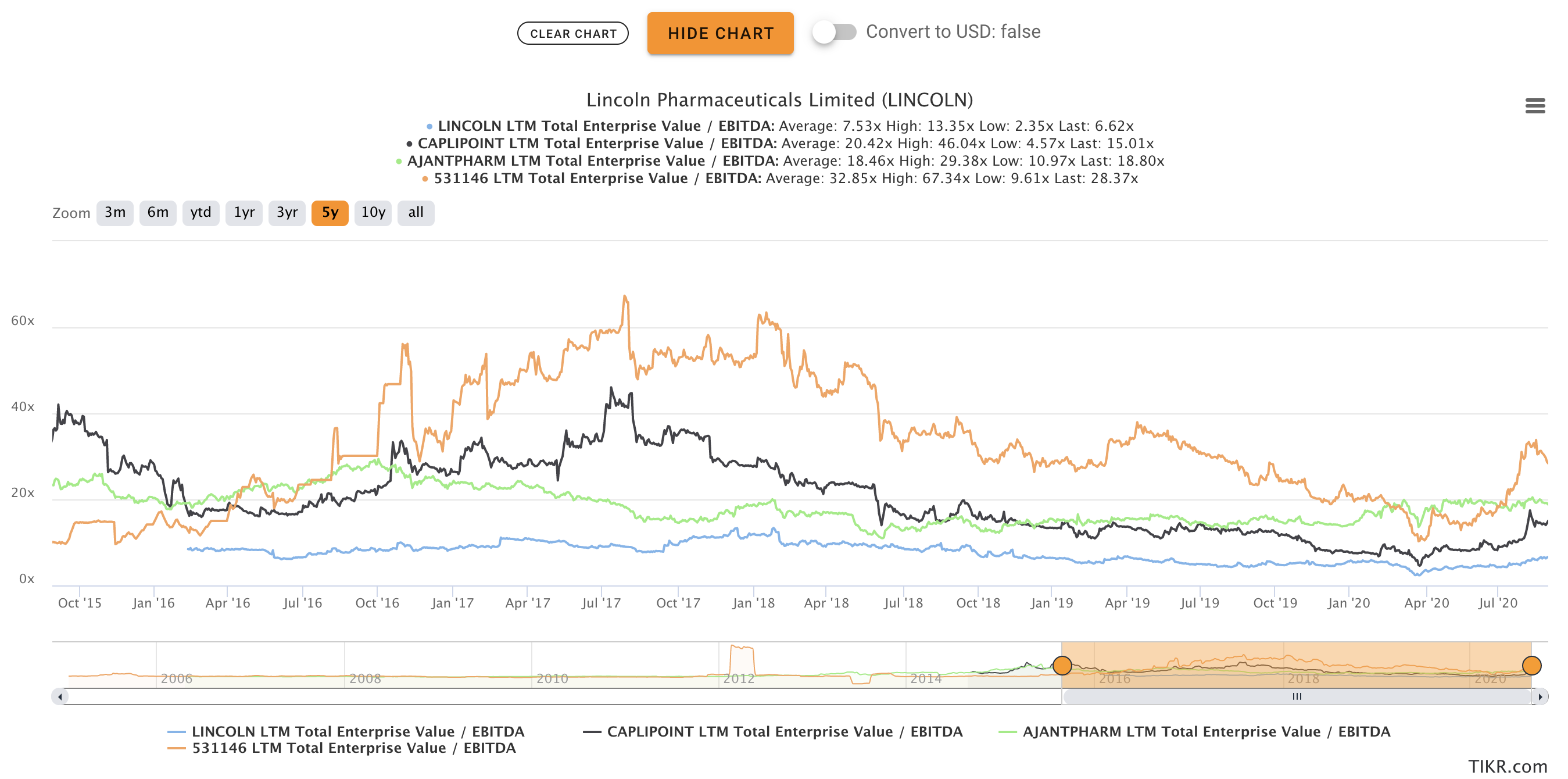

6. Lincoln Pharma

Lincoln is also a turn-around story. From being a pure trading and marketing company, they have started manufacturing their own formulations (FDFs). They also recently got EU GMP certification from Germany FDA. Like RACL and Chemcrux, due to their small size, their valuations have been rather muted compared to peers.

Current Under-valuation compared to peers average: 3.3x

Current Under-valuation compared to peers peak: 6.8x

Current Under-valuation compared to self (past history): near average valuations and 2x compared to peak valuations.

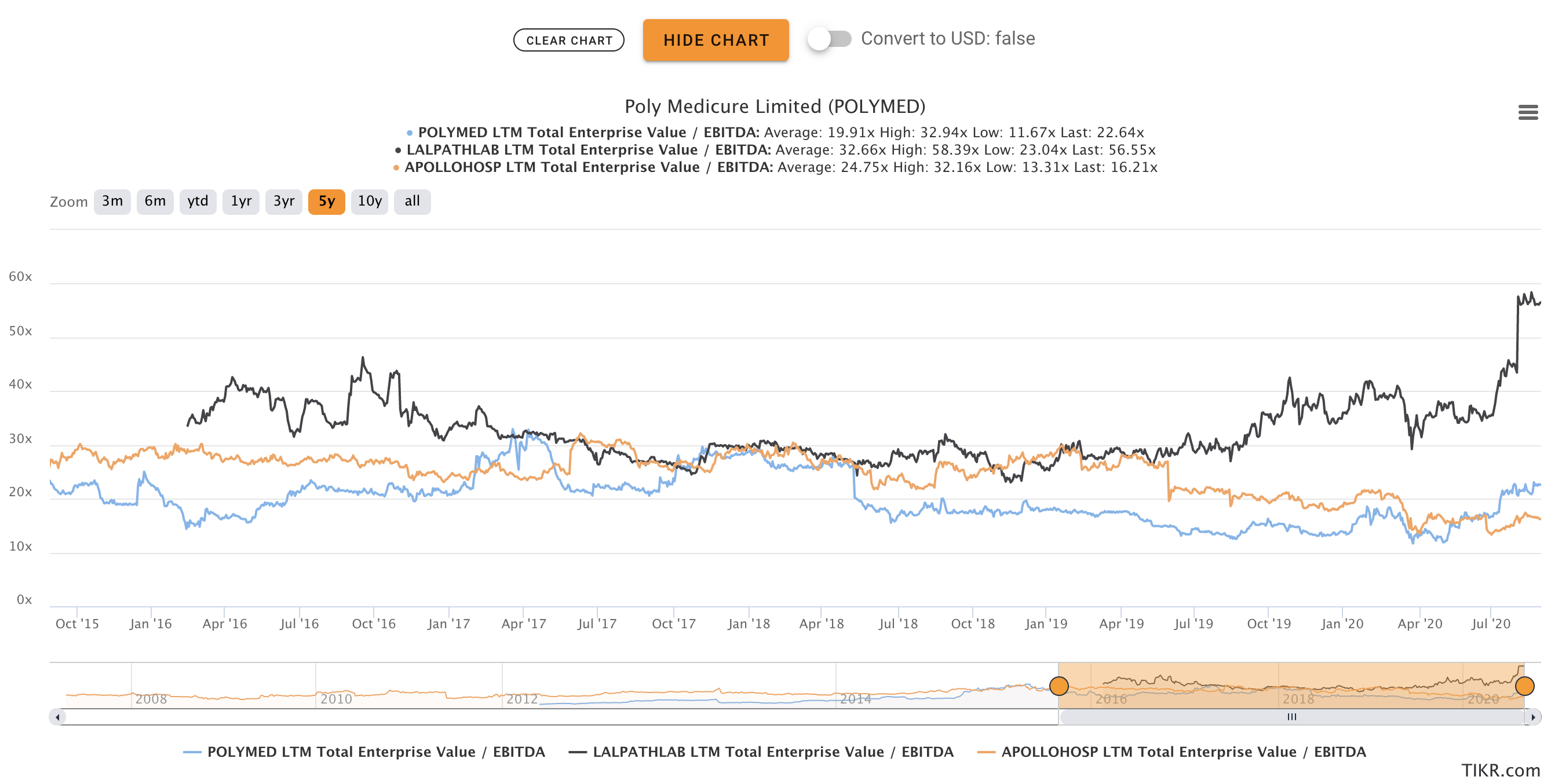

7. Poly medicure

One thing worth mentioning is that Poly medicure really does not have a listed peer which is even comparable. I have added lal path labs which is into diagnostics and apollo hospitals which is a hospital chain. Polymedicure is one of the 2 purchases which i did near the average valuation of the company (fairly valued) due to the large size of opportunity ahead. They have given consistent 15% sales growth in last 9 out of 11 years. Are just getting into dialysis. Also have an untapped market potential in USA. The opportunity size and strength of past performance made me purchase poly medicure at near historical average valuations.

Current Under-valuation compared to peers average: 1.2x

Current Under-valuation compared to peers peak: 2x

Current Under-valuation compared to self (past history): near average valuations and 1.5x compared to peak valuations.

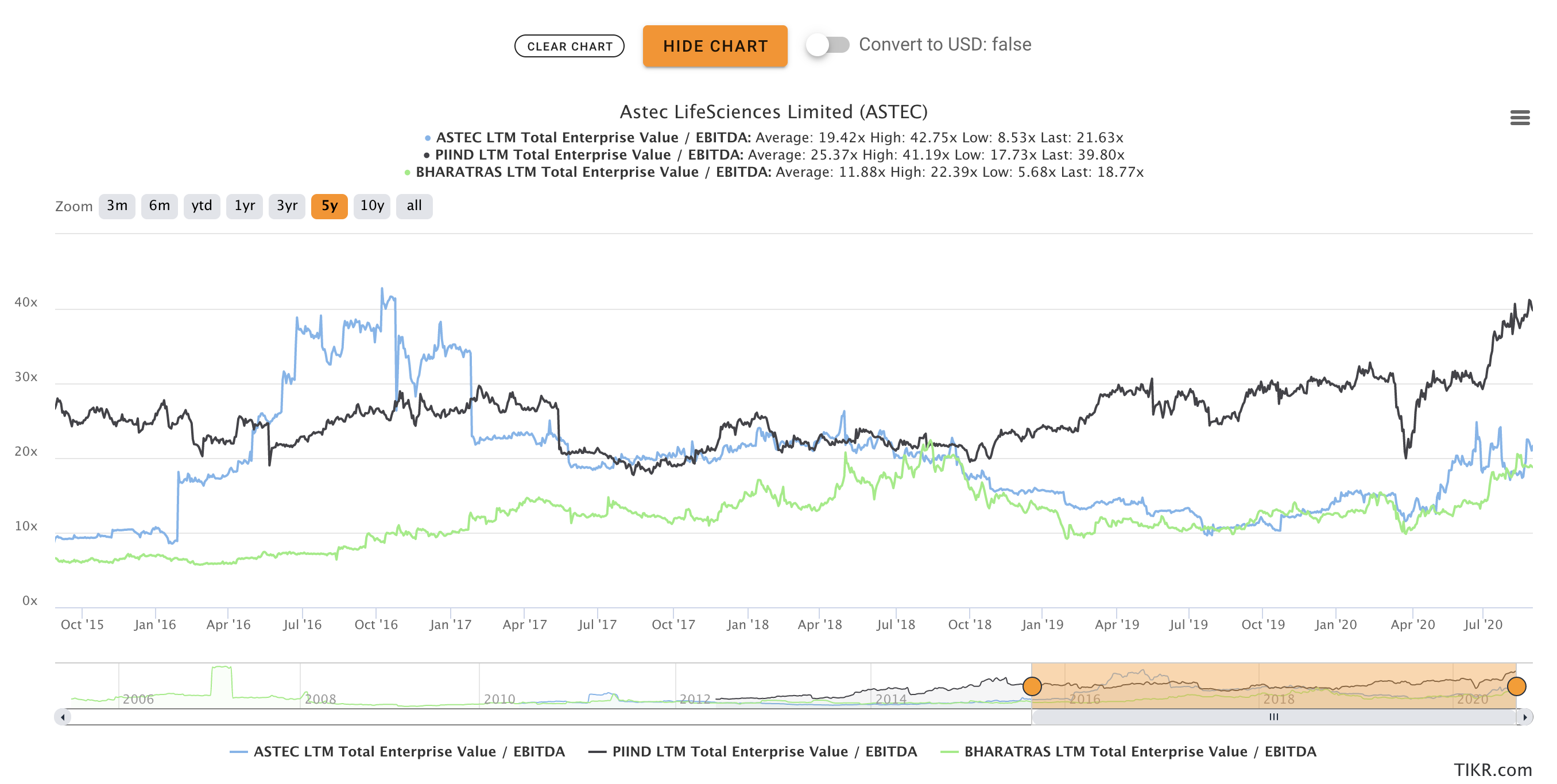

8. Astec Life sciences

Comparing astec with two different types of peers: PI industries and Bharat Rasayan. Astec is owned by Godrej group, and is the second company that i bought near long-duration historic average valuations. Again due to the large growth runway in front of them. Given the industry tailwinds with Make in india, import substitutions, China-to-india migration growing farmer income in India I also realized it would be very difficult to find it near average historic valuations again.

Current Under-valuation compared to peers average: Not under-valued

Current Under-valuation compared to peers peak: 2x

Current Under-valuation compared to self (past history): near average valuations and 2x compared to peak valuations. (I do not value bajaj finance because I intend to sell out of bajaj finance eventually and deploy the money into IDFC First).

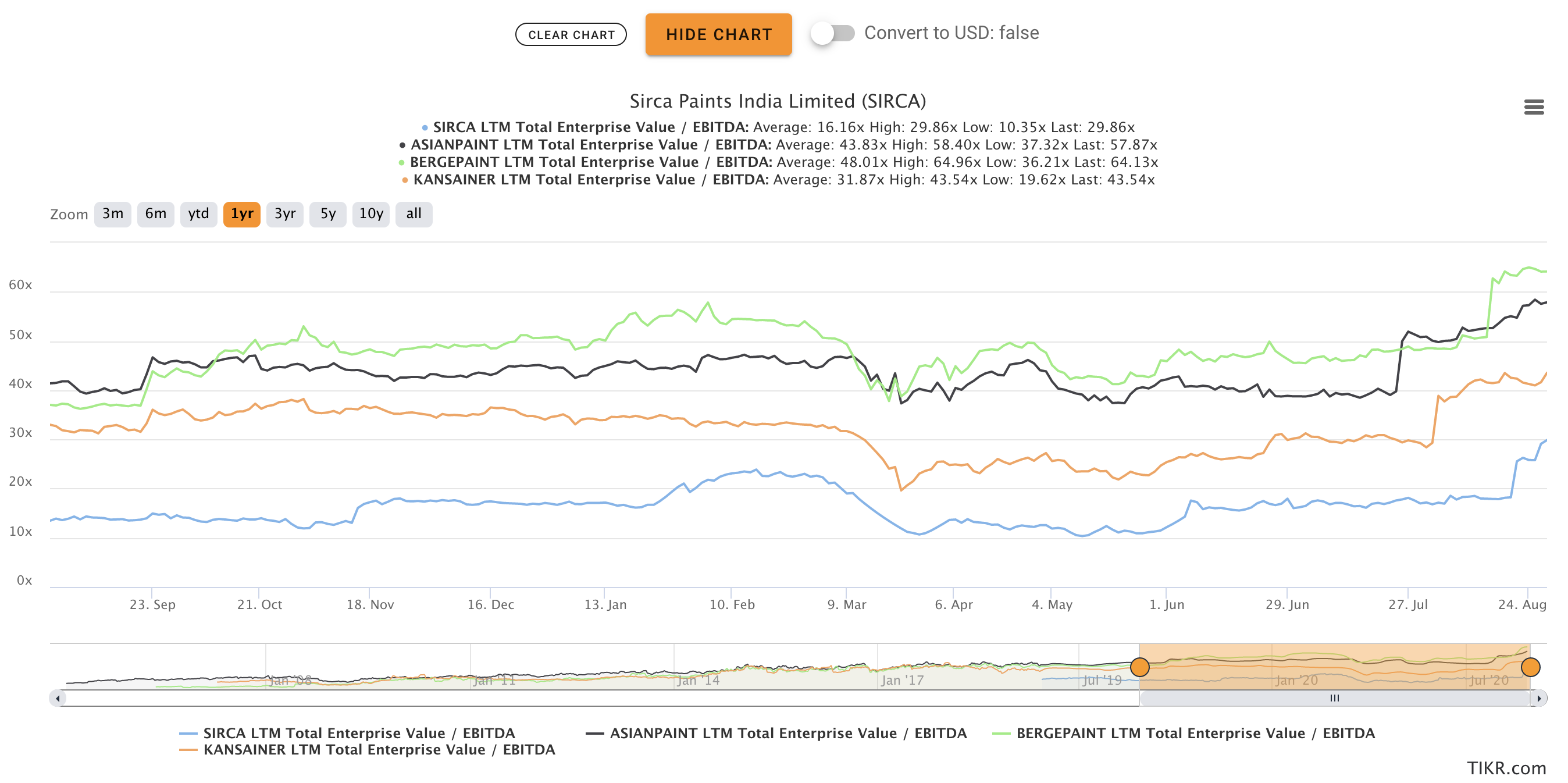

9. Sirca Paints

Small wooden coating maker with strong lineage from Italy. It recently raised capital in IPO to start manufacturing plants in India. Also intends to diversify into wall paints. Due to their small size (both business and also brand recognition), trades at a much larger discount to other paint companies. Rerating would depend on management capabilities to operate well and scale up the business sustainably.

Current Under-valuation compared to peers average: 1.33x

Current Under-valuation compared to peers peak: 1.66x

Current Under-valuation compared to self (past history): Company has only been listed for 1 year so I dont think it is reasonable to look at this.

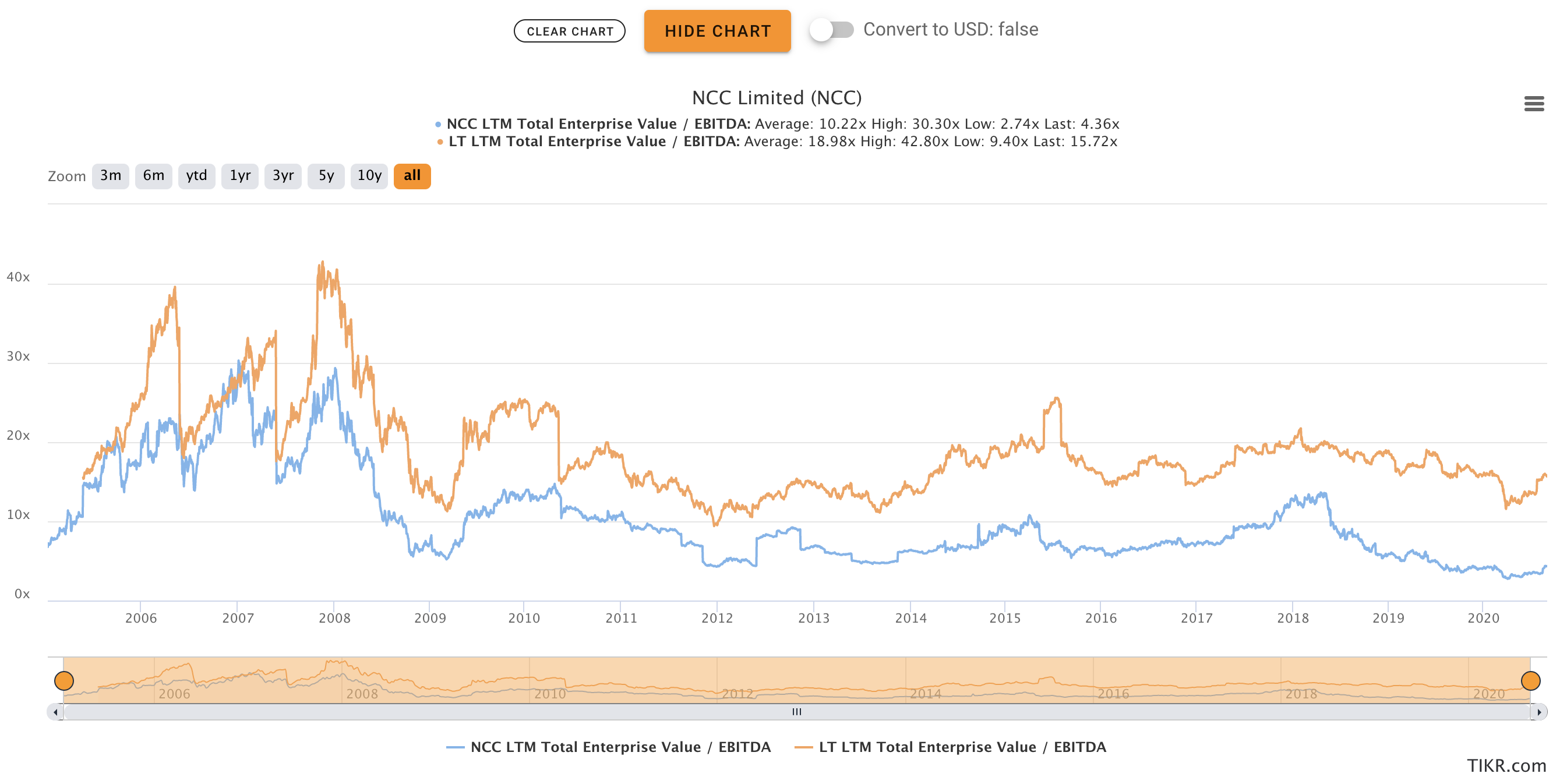

10. NCC

NCC is the second largest listed construction player in India after L&T. In the last few years, construction and infra has fallen out of fancy. That, coupled with the better perception in quality of management of L&T has resulted in much lower valuation for NCC. The National Infra pipeline will provide the required impetus to improve NCC’s cashflows and valuations. If they can grow their scale of operations successfully, I believe an even bigger re-rating is possible.

Current Under-valuation compared to peers average: 4.33x

Current Under-valuation compared to peers peak: 10x

Current Under-valuation compared to self (past history): 2.2x

I only intended to analyze these top 10 holdings since they impact my net worth the largest.

In conclusion, my portfolio is definitely under-valued as per my understanding.