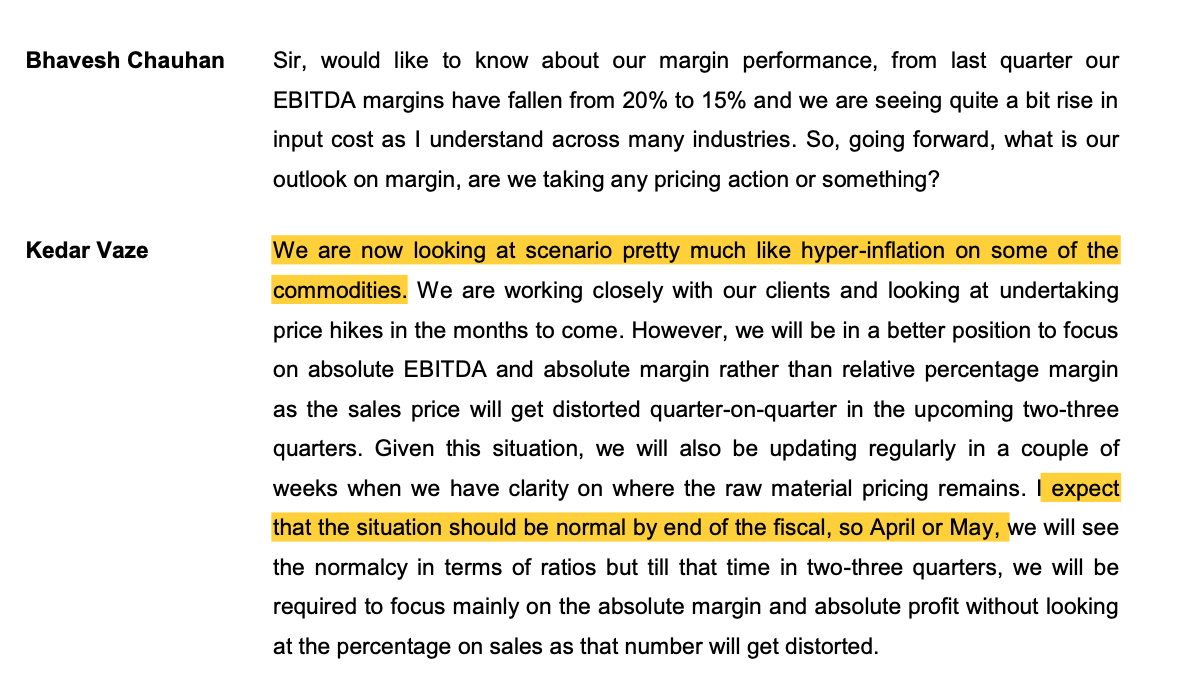

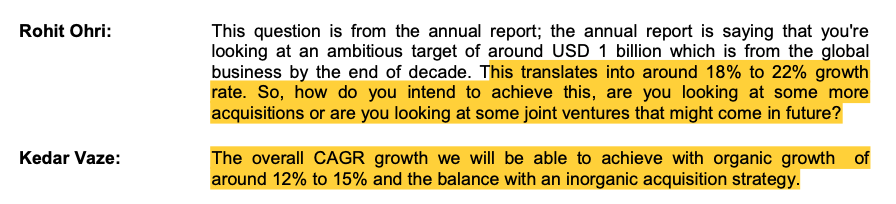

I completely agree. It always helps to have clear communication from the management…

After my reply, I had a quick look at the Earnings Call Transcript (from Tikr). They have given the following responses… (Highlights are mine)

Bhavesh Chauhan

Okay, sir. Sir, lastly, I would like to ask management on their views on capital allocation. Sir, we have some debt in our books, and then we are going for a buyback. And also, there could be opportunities for inorganic growth. So by doing a buyback, are we saying that we are not going to repay our debt in a very meaningful way, and also, there are no further inorganic growth strategy that the company is looking for?

Kedar Vaze

So there is a couple of points. One is that last year onwards, we have been maintaining very low ratio of profit distribution given the uncertainty around the pandemic. We are now looking at the post pandemic situation in Europe, and we expect that in various parts of the world. And this is anybody’s guess. Your guess is as good as mine. So we are now proposing and planning on the basis that we are in a post-pandemic situation and there is no extra need to conserve cash. We don’t see any effect of complete stoppage of business happening. So we are now restoring back our confidence in the cash flow and distributing the profit as per the profit distribution policy. In addition, we have had a onetime gain of INR 64-odd crores in the first quarter as a result of a tax refund. So this is passed through to the shareholders that the buyback proposes to do.

On the debt side, most of the debt in terms of the quantum is in Europe, acquisition in Europe, working capital in either euro or U.S. dollar. And the interest rate continues to be a very low interest rates. So we are comfortable to maintain the current debt level and continue to grow the business from here on. It doesn’t make a very big sense to reduce the debt in the European markets where the debt interest rates are very low.

Viraj Kacharia

Okay. Second question is, so you said that we have a good amount of visibility in terms of growth, and hence, we kind of hinted for a buyback option as well. But if I have to look at for the next 2, 3 years, given that we are still kind of quite very strongly positive on growth and margin recovery, would this be more like a regular feature in terms of buybacks? So I’m just trying to understand between buyback and repayment of debt. I mean, what is a – I mean, how…

Kedar Vaze

So we are committed to our distribution policy, profit distribution policy of 30% to 40% per annum. We will look at both measures, dividend, buybacks and any other route or distribution method that from time to time, what makes sense in terms of taxation, in terms of shareholder value. We also believe that buyback gives a better representation and better value for longer-term shareholders than dividend where effectively, people can own the share for one day and get a dividend rather than having to own it for a bit longer. And we are committed to the profit distribution policy which we have announced between 30% and 40% of the PAT that we generate.

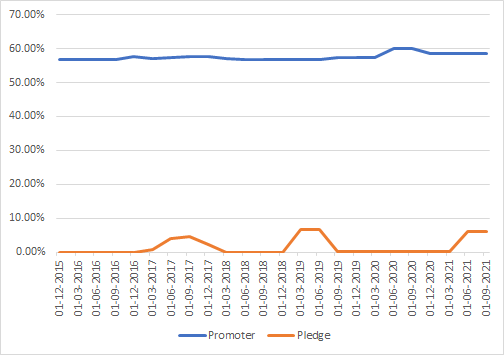

These responses have satisfied the doubts I had about the buyback vis-à-vis dividend. Also, I don’t think there is an ulterior motive to buybacks. The reason for pledge is personal and I am okay with management not elaborating on that…

Disc: Invested at lower levels. ~3% of portfolio