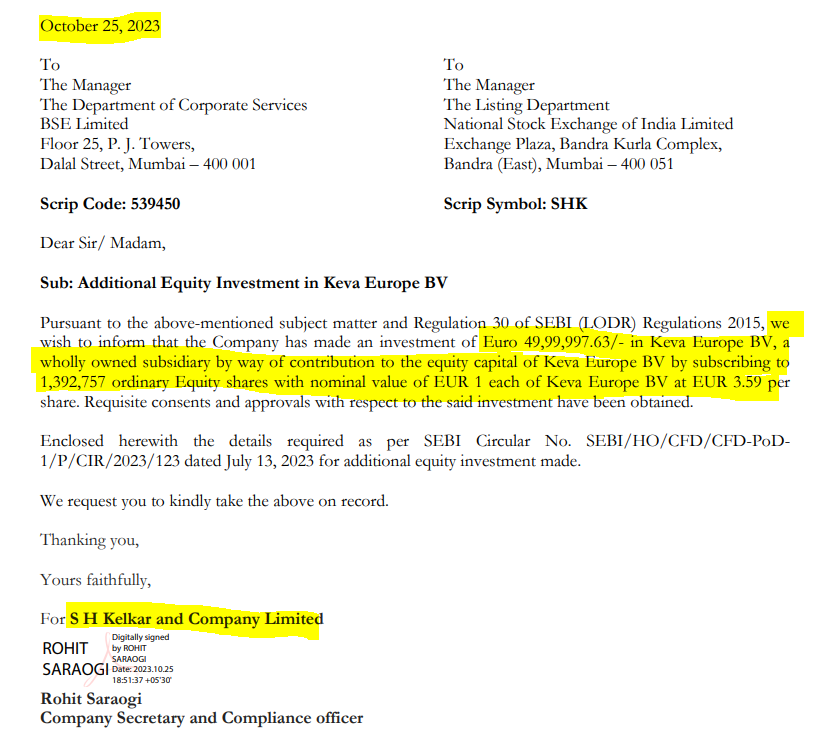

Additional Equity Investment in Keva Europe BV

1 Like

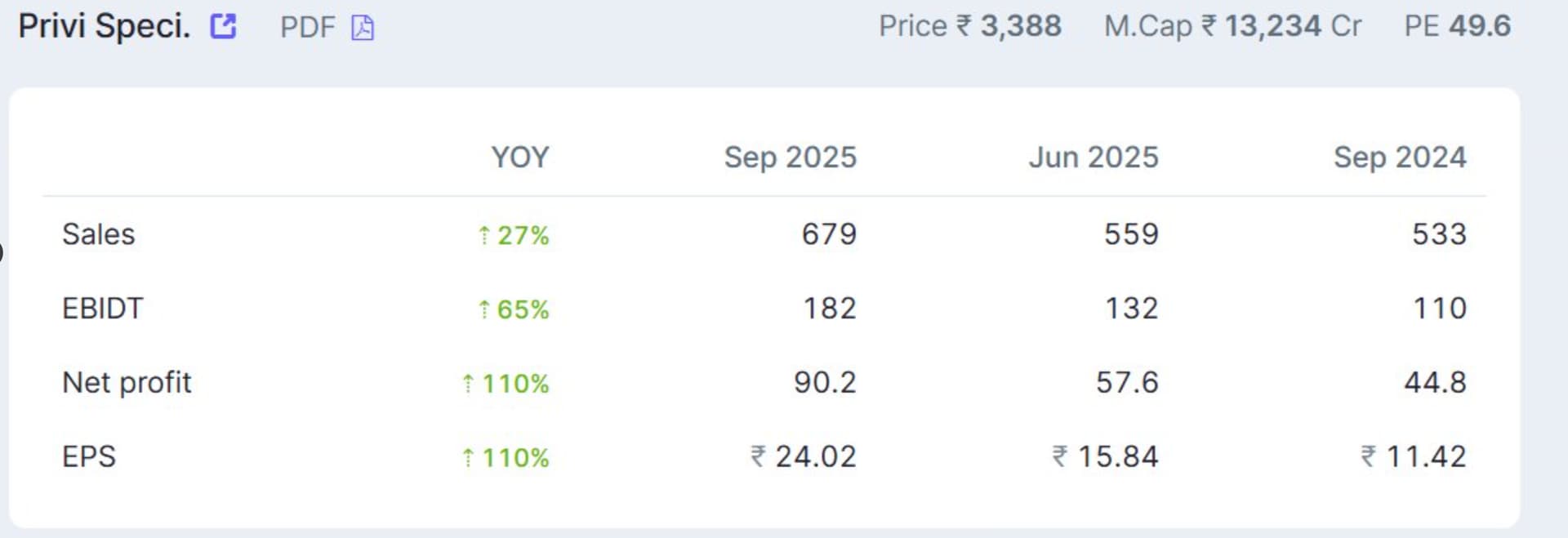

**privi specality results were announced

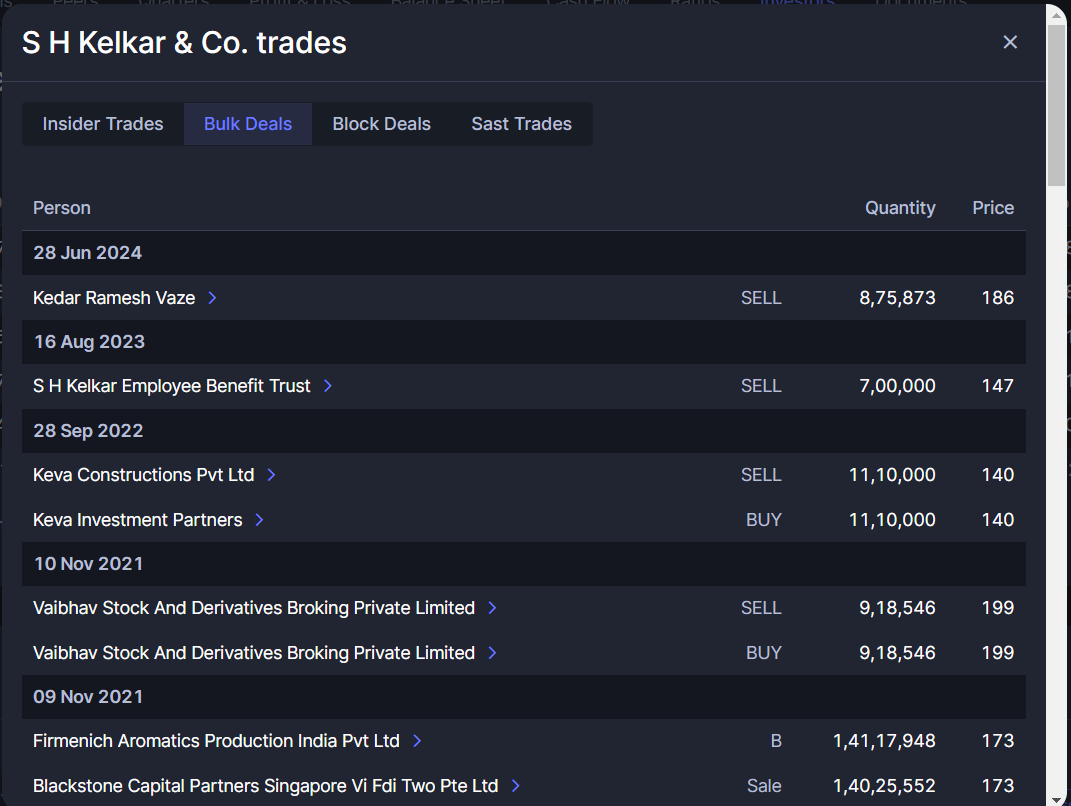

Why is the employee cost of Shk is more than double of Privi for the same amount of turnover and as per annual report employee are around 840 for both the companies.

can some seniors tracking throw some light please

Regards

2 Likes

Very interesting observation. I have not tracked Privi but based on a review of their investor presentation some possible explanations

a. The nature of the business is different - Privi is in a different part of the value chain - so they provide bulk chemicals / formulations as an input into blenders like SH Kelkar (Keva) - see page 11 of Privi’s latest investor presentation. SHK has a more specialised business of blending multiple inputs to match exact requirements of FMCG customers (who are their direct customers)

b. Part of this difference can be explained by the factors of production - though the employee cost is lower, the depreciation cost for Privi is approx 50% higher (and perhaps therefore the cost of finance? - just a guess). So it seems that part of the value chain is more equipment heavy whereas the SHK part of the value chain is more employee expertise heavy (I have seen a similar trend in tea - where tea blenders are a very highly paid and expertise based service).

Though they have similar profitability, the market seems to reward Privi with a much higher multiple (the JV with Givaudan probably helps -as they will likely be a captive buyer).

I think SHK has been trying to backward integrate a bit as well (into what they call Global Ingredients) - but that is a small part and to derisk sources rather than as a line of business.

5 Likes

Very Well Explained @sujay85, Whoever asking FMCG Valuations, for their understanding I would say, Fragrance in detergents typically ranges from 0.1% to 0.8% by volume and in soap typically ranges from 3% to 5% of the total soap weight depending on quality which means there is not bulk use of F&F in FMCG Products and they are moslty into B2B Category where RM prices fluctuate a lot plus B2B players have limited pricing power.

So frankly dont get exiced about FMCG valuations.

1 Like

Can you please explain why SH Kelkar have very low interest rate 5-6%?

Q2FY2026

S H Kelkar and Privi Speciality seem to have gone on completely different trajectories.

In a rising input costs environment for aroma chemicals, Privi seems to have benefitted a lot from its backward integration for manufacturing of alpha and beta pinenes using by-products of paper industry.

They are at an advantage of 15-20% compared to players like S H Kelkar, Oriental Aromatics using GTO (gum turpentine oil).

S H Kelkar had guided earlier that their margins should improve from H2.

Management call scheduled on 12th november 2025 (Wednesday)

1 Like

Have you listened to management call ?

Hey rohit,

With so many results & concall to follow I haven’t got time to go through. But planning to listen to it in a day or 2 & update the nuances here.