Speed and reaction times of fmcg /consumer facing managements are faster while b to b managements Like oil companies managers hv to be typically laid back They respond with less alacrity but maybe good otherwise pls be a little flexible though I don’t hold any brief for management

1 Like

Dear MrKakade, do you have the current capacity utilisation levels post all the new capex ?

As per last updates, thier capacity utilization was in the range of 60 to 70%. Need to check latest figures once Q4 data is available. Point to note is revenue is not linearly proportional to the capacity utilization. It’s not typical manufacturing or processing company. 15% rise in capacity utilization may even double revenue in case of SHK.

1 Like

Acquisition update a few weeks back + debt levels reducing.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/3aa0e20d-0669-4ddf-8b4c-5d645d9b5fae.pdf

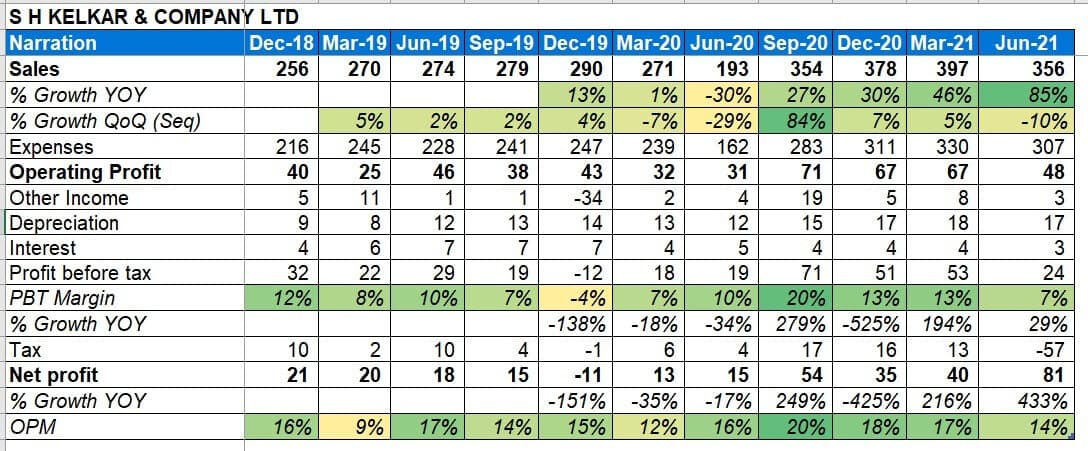

Latest position for Malabar

3 Likes

Just putting up a case for PE re-rating!

Galaxy Surfactants trades at 23-24x EV to EBITDA (TTM) and 3.9x EV to Sales (TTM). Galaxy Surfactants 3 year & 5 year sales growth rates are mid single digits. Galaxy Surfactants growth depends on the FMCG growth (quite similar to the F&F players). However, there’s a considerable difference in valuations between Galaxy and some these F&F players valuations. If SHK management is able to deliver low-mid teen growth with 19-20% EBITDA margin (as guided on con-calls), there’s definitely a case of re-rating here.

Disclosure : Invested a token amount, Looking to increase the allocation

2 Likes

| | The bull (but misguided) argument is that SHK should trade closer to FMCG valuations given they are an indirect play on FMCG. As a supporting evidence, people will sight how global F&F players such trade closer to global FMCG multiples. |

|---|---|

| | The problem with that argument is twofold 1) Global F&F players have been growing faster than global FMCG and have similar return profiles (marginally lower). 2) S H Kelkar has been growing slower than Indian FMCG and has a materially lower return profile. SHK thus deserves a substantial discount to Indian FMCG players. |

What can the company deliver in the next 3-4 years?

- Organically, revenues can grow high single digit if one is reasonably conservative (I am modelling in 8%). The management keeps guiding for double digit growth and if they deliver that, the stock will substantially re-rate from here. But there is no reason to have that conviction today to model in double digit growth.

- In terms of margins, this seems to be a mid-teens margins business on a normalized basis. Margins are volatile ofcourse, as you would expect in any business with average pricing power. Management has been guiding for 20% EBITDA margins for the last five years – and margins have ranged from 13-17%; so even in their best years, they don’t make 20% margins. Management has historically guided for blue sky like numbers on both margins and sales growth and failed to deliver on those. This comes through when one reads through historical call transcripts.

12 Likes

Interesting thesis @Rohit_Kadam . Below is my take:

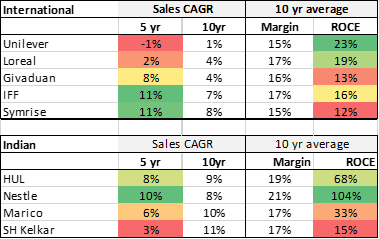

Global F&F players have grown 5-7% in last 3 years, but have witnessed significant consolidation of market share among the major players (GIV, IFF & SYM)

Further, there has been significant focus on being organic, healthier and Environment friendly for such ingredients where these company have been able to prove superior R&D.

These factors have driven margin improvement leading to their overall re-rating.

But for SH Kelkar which is a very small player (<15% market share in India). Apart from above, it benefits from lower exports from China giving SHK the opportunity to take share in domestic market.

Based on the order wins in the last 3 quarters, I expect the revenues to grow 15% for FY 22 and 23 and then slow down towards 8%.

Margins: it has caught up this year to finally breach the 18% mark, and if they can maintain it at 17-18%, the stock has upside opportunity.

Whats your view on valuation?

1 Like

I don’t think the argument was ever that a SHK or any F&F player will command a valuation comparable to HUL or P&G.

Though for the sake of this discussion on valuations would put up the 3 possible comparable scenarios

a) SHK v/s IFF, Givaudan, Symrise

b) SHK v/s HUL, Dabur, Marico, Godrej CP

c) SHK v/s Galaxy Surfactants

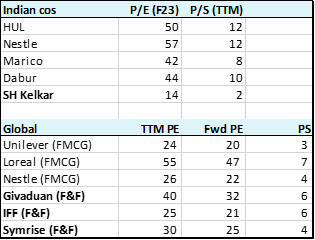

a) SHK v/s IFF, Givaudan, Symrise

| Company | 5 Yr Sales CAGR | 5 Yr EPS CAGR | 5 Yr Avg Operating Margins | 5 Yr Average ROIC | P/E TTM | P/S TTM |

|---|---|---|---|---|---|---|

| SHK | 5.90% | 14.40% | 11.50% | 10.00% | 15.2 | 1.66 |

| IFF | 10.90% | -9.20% | 14.00% | 5.40% | 77.6 | 5.69 |

| Givaudan | 7.50% | 3.60% | 16.00% | 10.00% | 50 | 5.88 |

| Symrise | 6.23% | 3.20% | 13.80% | 7.00% | 49.9 | 4.23 |

The fact that some of these Global F&F players have grown way better than SHK seems to be misguided, though SHK definitely has been some sort of a laggard. Other return ratios for SHK are also not all that poor. Given the data points it’s surprising to see such a steep discount when it comes to valuations.

b) SHK v/s HUL, Dabur, Marico, Godrej CP

| Company | 5 Yr Sales CAGR | 5 Yr PAT CAGR |

|---|---|---|

| HUL | 8.00% | 16.00% |

| Dabur | 4.00% | 7.00% |

| Godrej | 6.00% | 6.00% |

| Marico | 6.00% | 13.00% |

| Colgate | 5.00% | 15.00% |

| PGH | 5.00% | 0.00% |

| SHK | 7.00% | 13.00% |

Comparing SHK’s growth rates to Personal Care FMCG companies (since SHK is a dominant fragrance player). The margins and return ratios for SHK are of course nowhere near and argument of SHK trading at the multiples these FMCG companies would fail to make any sense.

c) SHK v/s Galaxy Surfactants

For the reasons stated above, the argument was never about SHK trading at similar multiples to that of a HUL or a P&G. The argument though was to compare its valuations with

a chemical company which has these FMCGs as customers (or) raw material manufacturers for these FMCGs. The reason this would make sense is that these companies have the same end user industry which would drive the volumes and limited to no pricing power (these large FMCGs hold the entire bargaining power). The best comparable with the mentioned characteristics in the Indian listed space imo is Galaxy Surfactants.

| SHK | Galaxy Surfactants | |

|---|---|---|

| 5 Yr Sales CAGR (2016-2020) | 5.96% | 6.77% |

| 5 Yr PAT CAGR (2016-2020) | -13% | 28% |

| 3 Yr Sales CAGR (2018-2020) | 4.28% | 6.27% |

| 5 Yr PAT CAGR (2018-2020) | -30% | 15.66% |

| 5 Yr AVG ROCE | 14% | 25% |

| 3 Yr AVG ROCE | 12% | 25.20% |

| 5 Yr Avg OPM | 14% | 13% |

| 3 Yr Avg OPM | 14% | 13% |

| EV/EBITDA | 10 | 24 |

| EV/SALES | 2 | 4 |

| PB | 2.4 | 8.6 |

One can also look at other cash flow ratios as well.

The PAT growth rate numbers for SHK do not reveal the true story because of the year chosen, however I will not shy away from the fact that PAT growth for SHK for the past few years has been surely muted because of several issues. Though the point here is whether the steep discount in valuations as compared to Galaxy Surfactants be justified considering similar top line growth and similar operating margins.

Imo this is a turnaround story and looking at past 3-5 year growth numbers might be misjudging it. One can see last couple of quarter numbers and clearly gauge the difference on all fronts. And my reckoning is if the management is able to deliver even a lower to mid teen top line growth with a 17 % OPM, the re-rating case would only get stronger. The very reason for the stock getting beaten down was management not able to deliver because of a whole lot of reasons. And those issues are of the past now and there looks like a clear roadmap set by the management to achieve the numbers they’ve mentioned.

From an investor pov though, a more conservative approach would be to wait for a couple of more quarters however, majority of re-rating part might already take place by then.

Disc. : Invested.

8 Likes

Good perspective given. Thanks @Dhruv_Desai and I agree to most of the points.

SHK is well placed turnaround story and IMO following points would help to grow both topline and margins -

- Synergies of CFF and Nova acquisition will come into play. Nova is good acquisition for 13.4 Cr (70% stakes) which will open up more customers in the premium category. Also it will help to diversify revenues geographically with better margins.

- Greater engagement with India FMCG and MNC companies and SHK getting more orders from these big players going forward for new product launches will help in increasing topline and margins. More to that sticky nature of business will ensure steady revenue stream.

- Management has mentioned that growth rate in flavours business is more. Though its not considerable (10% of overall revenue), I hope it will help improving topline and margins going forward.

Not concerns, but improvement areas need to closely watched for SHK would be -

- Sandalwood distribution rights from Santolal may start contributing slowly from this FY. This will be lower margin business but any addiiton in topline and bottomline from this non-core activity would be welcome.

- Better inventory management as SHK has considerable working capital as compared to sales. Raw material cost is major cost factor (60 to 70% of sales). I acknowledge that some of issues like raw material price rises couple of quarters back and recent covid wave 2 might have some impacts, but this is one area where better management is expected

- DSO still stands high @105 days. With greater bsuiness from bigger FMCG players I hope to see this come down.

In all, at current valuations positives outweigh the other factors mentioned and convince me about well places turnaround stroy. I expect stock to go back to its median PE of 25-26 in near future giving a good upside from the current price.

Disclosure: Invested

2 Likes

IMHO some biggest positives in SHK at present are:

^ very high operating leverage going forward as company is operating at very low capacity

^ very reasonable valuations due to poor performance in recent years

^ predictability and consistency, up to some extent

^ cash generation and focus on debt reduction

Negatives:

€ avg management without aggression

Analysis:

^ valuation is cheap, no doubt;

^quality of business is average

^ growth is moderate

^ at current valuation, may be a good idea …

2 Likes

Earnings call transcript - Q4/FY21

Business Overview

Overall Growth

- We have had many years of double-digit plus growth in our portfolio and business. The 5% CAGR actually was a result of the dual effect of demonetization and GST, where lot of smaller clients’ businesses actually de-grew

- the base of this customers has reduced from a roughly 20% to approximately 10% in FY19-20. With the new customer base, which is most of the large and medium sized FMCG in India and overseas, we are continuing to grow at a steady double-digit growth

- Our larger customers are still growing at more than 12% maybe even around the 15% CAGR in the last 2-3 years and we anticipate that this growth will continue.

- we anticipate a good level of new, what I would call, modern age start-up FMCG products to come up in the next 2-3 years, which will help us further get a growth in the regional markets

- We have obviously the Italian acquisition which will help us to grow in that market. That will assist us to take new markets.

- 12%-13% underlying business growth is what we anticipate and we will manage to continue to grow that within our current portfolio customers

Competitors

- We have now almost 45% of our business outside India

- we have 4 or 5 global F&F companies like Givaudan, IFF, Firmenich, Symrise, which are the global competitors.

- in general, top 4 to 5 players are controlling 70% to 80% market, in pretty much all the markets that we are operating.

Markets

- Domestic market

- across all categories, we have maintained our market share vis-à-vis the overall FMCG fragrance and flavour. There is no particular category or client type which has done better or worse.

- Europe

- Italy

- the Italian market is as large as the Indian market. So, it is quite a sizable market

- The underlying business growth in Italy has been around 1%-1.5% industry growth. So Nova and CFF together have grown at 8% to 9%, 3 to 4 times faster than the average market in Italy.

- We look at it as a good platform for us to build further growth in Italy and then from there on to other countries in Europe

- CFF

- CFF is among the top 2 or 3 companies in the market share in Italy

- our business in CFF has not been negatively affected by the pandemic even last year or this year. We continue to see good growth across all the categories where we are operating

- CFF growth rate has been in excess of 8% organic in the core business in last 15 odd months

- With the addition of Nova we are also able to go to additional clients which were not accessible to CFF in the past.

- Nova

- Nova product range is in the premium Haircare, Beauty products. It is at the higher end of the margin profile. Consolidated core business margin of CFF is around 53%-54% gross margin level and with the addition of Nova, which is slightly higher at the ballpark 58%-59% gross margin

- Going forward, we anticipate we will continue to grow at a healthy pace of a roughly 10% per annum in CFF-Nova combined entities.

- Italy

Santalol

- we have been working with Isobionics via our PFW R&D team. Isobionics, a Netherlands-based company, has been taken over by BASF but we continue to keep our relationship and manage this product

- In terms of business size, sandalwood oil market is in excess of Rs. 100 crore a year. There is a good opportunity but what we see is that having a renewable source with a stable supply will encourage the use of sandalwood oil again in perfumery, which has been declining in terms of volumes year-on-year and as the volumes continue to grow.

- The typical top-line we would be considering is something like Rs. 25 crore from this business and we are basically distributing the product, the margin in that would not be very high. I would anticipate a 10% margin but there is no additional cost, so maybe 1% or 2% marketing costs and 7%-8% would be the net margin for us on that product.

- there is a lot of know-how within the company and in the industry for using sandalwood oil, which we are also seeking to revive as an additional leg for growth.

Financials

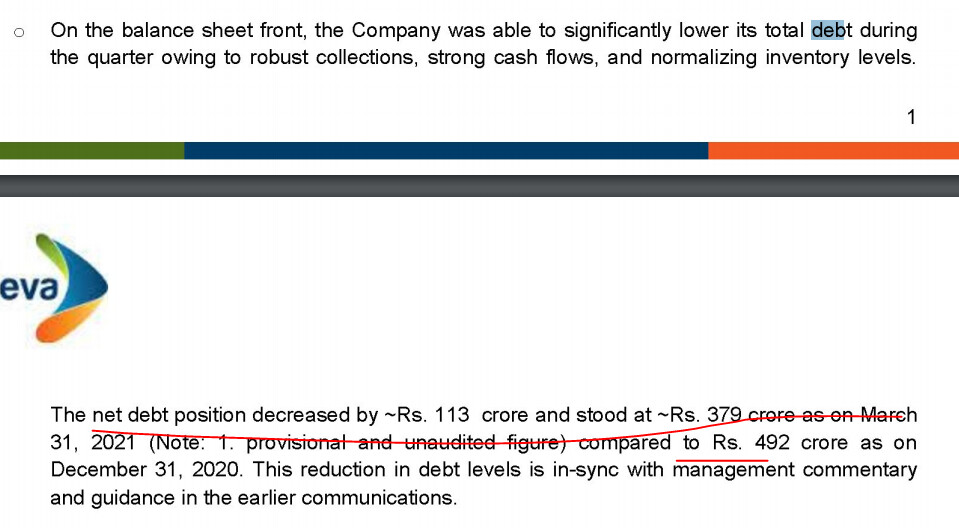

Balance Sheet

- we were able to significantly lower our net debt by Rs. 112 crore during the quarter owing to robust collections, strong cash flows and normalizing inventory. It translated to a healthy debt to equity ratio of 0.4X.

- I am confident that we will be able to generate Rs. 300 crore of cash flow in these 2 to 3 years’ period. I would just put a disclaimer on the current situation. Given COVID, there may be a few months of difficult growth but anywhere between 2 and 3 years, we anticipate a positive cash flow of odd Rs. 300 crore, which will enable us to reduce the debt

- as a part of business continuity risk management, last year, the Board had mandated us to increase the cash holdings at various bank accounts, which we are operating in the region. We will review that post pandemic and bring down our free cash held in balance to reduce the overall cash in the balance sheet.

- CWIP

- if we look at last 3 years, we have been adding up around say Rs. 15 to 20 crore of expenses every year

- at this moment we are more or less in a steady state. We are writing off some of the projects that did not complete or did not materialize into sales. And at the same time, we have new projects where there is a work in progress.

- We keep them capitalized in the balance sheet and when they are actually materialized, either they are successful in which, they get into capitalized asset, intangible asset. If they are not successful then they will get written-off. Ballpark this is quite steady state so in terms of what is written-off and what is capitalized on new projects, it will not result in any additional costs or deferment of cost.

Margins

- We have been quite prudent in our inventory and as the prices have been going up, we have accumulated additional inventory. we are selling basically to our clients from stock-in-hand so that in case of any large input changes, we try to pass it on to our clients with a 2-3 months lag

- we have cut down on our R&D expenses by 1% as alluded earlier from 5.5% to 4%

- We will pass on the additional cost increases to our customers as far as possible. I think there will be some transient margin pressure, may not be very large but maybe one odd month or one odd quarter, we may see some decline.

- So, the gross margin for bulk products is lower and for speciality category is higher. Our average is around 42-43% and we are talking about 4,000-5,000 different products. It is not that one product or new product introduction is going to change the nature of the business. It is all incremental.

Returns

- if you kind of look at a 20-year average, we are more close to the 20% return on investment

Capacity/CAPEX

- Fragrance capacity utilization is around the 55% mark

- Flavours is also around the 50% mark

- We have capacity at China plant, which is also available for further expansion for us.

- We do not need any large CAPEX for increasing the capacity, so within kind of Rs. 3-4 crore investments, we will be able to increase our capacity by 20% to 30%.

- CAPEX outflow for next 6 to8 years of growth is already done

Forward Looking

- FY 22

- Q1 FY22 is softer than the previous quarter. It is already almost two months of the quarter and we are seeing some softness in this quarter

- For the rest of the year, if I extrapolate from last year, I would imagine that from the second quarter, our growth rate should resume to the average 12% YoY growth that we have in the underlying business that we do

- in the long-term, the full year basis, the gross margin will continue to maintain the trajectory of around 42% to 43% level

- We will manage around a 19% to 20% EBITDA margins

- 5-year story

- we have done sizeable CAPEX in the past 3-4 years and prior to the IPO as well. We are now looking at a maintenance growth business, where we have sufficient capacities and we are looking to continue to grow the business with the capacity utilization and value upgradation of our current product mix

- We are planning for a normalized 12% CAGR growth in the next 2 to 3 years and this will automatically slowdown in terms of cash flow and profitability growth as we grow our operating size vis-à-vis the CAPEX and the operating leverage kicks in.

- our operating margin should slightly improve - should go up to 45% in a 5-year period.

- our expectation is to focus on future growth and continue to invest on growth keeping steady state 20% EBITDA level for the business. And incremental gains, we would like to invest back in faster growth rather than more margins

- we will then focus on continuing to work with the markets, which are the 3 markets of Europe, India and South East Asia, where we are currently operating

Regarding the recent discussion about growth prospects - The concall has management perspective regarding this... FYI

7 Likes

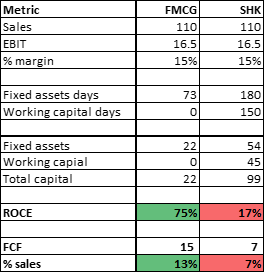

The problem with this business is that the high capital intensity compresses the ROCE. which also matters for the PE.

Below is an illustration to show how ROCE and FCF conversion is inferior for SHK versus FMCG despite both growing at the same rate and with a similar margin profile

2 Likes

My take on the valuation debacle (FMCG vs SHK). I have made points against and in support.

Why I am not ready to pay SHK FMCG multiple

-

SHK is a Chemical sector company and is therefore prone to RM price volatility. Being a B2B company it is certainly not able to pass on that to the end FMCG company promptly. So, margins and profits will remain more volatile compared to FMCG companies which owing to their pricing power can more readily pass on any RM hike.

-

Also being in the chemical sector, SHK is more succeptible to regulatory headwinds.

Why should SHK trade at FMCG like valuation

SHK indeed has characteristics which should make it trade at ‘less-premium-FMCG’ like valuation (read Jyothy Labs).

In comparison to other chemical segments which are proxy to FMCG, e.g. surfactants, SHK makes up only a small part of overall cost of a product. Also flavour/fragrance is Impossible to duplicate exactly. So, if the product is popular enough the FMCG company is highly unlikely to switch from SHK to other similar company, whereas they can easily switch to another surfactant company which can give more affordability with similar quality.

4 Likes

Can anyone provide clarity on 119cr of Investment in gp companies done by them ?

In FY20 (June 2019), the company did a buyback worth Rs60cr (2.5% of capital) at Rs180 per share (20% premium to the then prevailing price of Rs150). This was not taken well by the market and the stock fell post the buyback announcement. Strangely, the promoters participated in the buyback when instead they could have stayed on the sidelines and let their stake increase (~they owned about 56% then). Secondly, the logic of returning cash was strange as the company has Rs300cr of debt on its books and was paying interest of Rs25cr on that. I think the reason they did this was to take advantage of the favorable taxation on buybacks over dividends, a loophole which came in after 2018 budget and since then has been plugged. It was not a signal from the management that their shares were undervalued else they would have not participated in the buyback. Had they not participated; re-rating was likely.

5 Likes

The 300 cr debt is a pure acquisition play of CFF the Italian buisness is looking very good the most important thing is now the management has a clear vision there is no additional capex required for even the doubling of the top line and if we look at the competition the evebita is in range above 20 they are a kind monopoly in india better of than the camphor players

Technically also looks at a breakout point around 175 not a bad bet in this market

Disc invested

1 Like

img_5b0bfd40a208c6.79276568_Avendus_Report_081017.pdf (1.8 MB)

Very interesting read which explian the moat of s h Kelkar

5 Likes

quarterly updates…steady performance n commentary…Given difficult quarter gone by… not bad at all…can do a 45-50Cr+ PAT on 350 cr+ revenue for Q1 and FY22 profits should exceed 200 cr+, available at 2500 cr mkt cap. There is a clear mistrust in mgmt capital allocation etc but seems performance is speaking for itself, pessimism is overdone and upside potential is visible. Technically is looking good.

Another development Promoter today pledged some shares in personal capacity as well, called out intent of not selling …timing is interesting

3 Likes

Dull results… (QoQ), due to negative sequential revenue growth. Bottom line looks good only coz of the tax provision reversal. On the other hand, the announcement of New CFO Appointment found more interesting… his credentials include Head of Finance, Bajaj consumer, Marico, Coca Cola, Diagio … etc.

Board of Directors of the Company at its meeting held today, has considered and approved the appointment of Mr. Rohit Saraogi as the Chief Financial Officer and Key Managerial Personnel of the Company designated as “Executive Vice President & Group CFO” with effect from November 15, 2021.

Invested/biased. (about 3% of PF)

6 Likes

Has anyone been tracking this company closely last two quarters? Margins have been trending down with weak like-to-like sales growth. They have debt on books which remains stubborn and still, they are doing buybacks? Don’t know why they do not choose to become debt-free first.