Market Size

The total market size of the Indian fragrance and flavour industry is estimated at 3800 Crores in terms of value and 63.72 thousand tons in terms of volume for the calendar year 2014. Out of this total value, 55.0% was attributable to the Indian fragrance market, and 45.0% to the Indian flavour market.

Disposable incomes are rising in the world’s emerging markets together with consumer spending, especially in the emerging middle class that is increasingly able to afford packaged food and beverages and personal care items. Emerging markets are expected to be the primary growth driver of the global fragrance and flavour industry. As the economy grows, people consume more products. A number of these products are concentrated across half a dozen fastest-growing categories. By providing the largest quantum of fragrances in India, Keva has emerged as an indirect driver and faithful proxy of the Indian economy.

Fragrances and flavours are considered to be one of the important factors for consumers in deciding whether to repurchase a product and these factors often influence their decisions, thereby making them one of the key components of FMCG and integral part of product attributes.

- Barriers to Entry The global fragrance and flavour industry is characterized worldwide by high barriers to market entry. Some of these barriers to entry include Established long term relationships between fragrance and flavour companies and their customers, especially FMCG manufacturers, may pose an entry barrier for new players to the global fragrance and flavour industry

- Fragrance and flavour companies typically have to enter at an early stage of product development and such timely opportunities may not always be available to new entrants.

Market share

- Givaudan – 23%

- IFF – 14%

- Firmenich – 14%

- SHK – 12%

- Symrise – 7%

- Others – 29%

While SHK has 12% overall share, it has 21% + in fragrance and is number 3. In flavours it has just 2%

About the company

-

Earlier it was called Kelkar Gorup , but now name changed to KEVA.

-

Has three brands, SHK, Cobra and KEVA

-

Cobra is their branded fragrance – 10% Contribution

-

SHK, set up by two Maharashtrian brothers in 1922 - inspired by Gandhi’s Non-Cooperation Movement that had urged India to ban imported materials.

-

This is the 3rd Generation in the business - All Family members are trained chemists. Family settlement happened in 2010 and current family got the business.

-

They hired a professional CEO to run the business from 2010-2014

-

Professional CEO B Ramkrishnan was bought in in the year 2010 – Ram used to run his own fragrance firm called Privi Organics, which was later bought over by Givaudan. He then headed fragrance business of Givaudan – but effective 2014, he has been Director Strategy

-

Kedar Vaze, worked for 4 years under B Ramkrsihnan in 5 departments before becoming CEO

-

Raised 243 Crores from Blackstone in 2012 for 34.5% Stake, valuing the company at 700 Crores

-

IPO done at Rs. 180 in the year 2015

-

Global MNC’s are biggest competitor – but large part of their customer is Global MNC Brand

-

In Indian FMCG Cos SHK has the highest share – by a wide distance

-

Domestic FMCG Cos have 50% market today – and SHK has 21% share in that

-

Factories

Pre IPO

- Raigargh – 40% cap utilisation in 2015

- Vapi – 35% cap utilisation in 2015

- Mulund – 40% cap utilisation in 2015

- Netherland – 75% cap utilisation in 2015

Post-IPO

-

Year 2016 - Acquired flavour biz of Gujarat Flavours - Approx 15 Crore

-

Year 2017 - ought Mumbai-based VN Creative Chemicals Pvt. Ltd(VNCC) as part of efforts to cut costs in its overseas fragrance division - Mahad facility added

-

Year 2017 - Set up Fragrance Studio in Amsterdam – will help it in premium fragrances

-

Year 2018 - Acquired Creative Flavours & Fragrances SpA (CFF) in Milan – this will help in building Fine Fragrances – Acquired 51% for 8

-

Acquired Anhui China

-

Portfolio

-

Fragrance Portfolio

-

Personal Care

-

Hair Care

-

Skin Care

-

Fabric Care

-

Household Products

-

Aroma Ingredients Flavour Portfolio

-

Dairy products

-

Beverage

-

Confectionary

-

Bakery

-

Pharma

-

Jams and Spreads

90% Revenue 10% Revenue

-

-

3000 Local and MNC Customers

- Marico – uses SH Kelkar in Parachute Hair Oil

- Godrej – uses it in Godrej No. 1 Soap

- Jyothy lab

- Vini Cosmetics

- JK Helene Curtis

- HUL

- No Customer has more than 5% contribution

- Flavour is sold to Britannia, Vicco, Vadilal

-

5 Development Centres – Indonesia, Netherlands and 3 in India,

-

Globally fragrance firms command valuations in price/earnings range of 22-23, similar to that of FMCG businesses.

-

In 2010 they made their first acquisition – Netherlands based PFW Aroma Chemicals

-

Top 10 Suppliers contribute 35% of their RM Requirement

-

Attracting and retaining talent is very important – because there is limited numbers of skilled perfumers and flavourists - The family owns Kelkar Education Trust which runs Vaze College (popular as Kelkar college), where there is an advanced course on perfumery.

-

There is hardly any chance of a decline in revenues as 90 percent of the customers are sticky.”

-

Spends 3% on R&D - Large fragrance and flavour companies spend approximately 6.5% to 10.0% of their sales proceeds on research and development

Global

- The global fragrance and flavour industry is estimated to be worth US$ 23.90 billion with an almost equal split between the fragrance and flavour markets.

- The top 12 companies operating in the global fragrance and flavour industry held approximately 83.0% of the global fragrance and flavour industry. These top 12 companies can be further broken down into the top four companies, consisting of

- Givaudan SA,

- Firmenich,

- International Flavors and Fragrances, Inc. and

- Symrise AG,

that individually hold a market share of above 10.0%, and collectively hold 57.0% of the overall global fragrance and flavour industry among them.

Risks

-

A persistent problem has been its inability to pass on the costs of high inflation to the customers with immediate effect. While it is able to raise prices, there is typically a lag which hits profitability in the medium term. “We have large stock-in-trade which results in huge working capital requirements,” says Vaze. The lack of trained manpower is another impediment in this process-driven business.

-

Keva Aromatics Private Limited and Purandar Fine Chemicals Private Limited, are engaged in the same line of business as our Company – but there is no major activities in this

Key Raw Materials

- Geraniol

- PEA

- Lemon Grass

- Lavender

- Geranium

Annual Report takeaways

Year 2016

- It took us nine decades to reach the 1,000 crore-revenue milestone. We expect to achieve more than six times this growth in a decade

- Emerge among the ten largest global fragrance companies within this decade

- Account for a 1% global market share over the next four years and 2.5% of the global market share over the next decade

- Enhance our share of the Indian flavours market from 2% to 10% over the foreseeable future

- At Keva, our vision is to emerge among the ten largest fragrance companies in the world within a decade

- Traditionally, Keva has focused on six large downstream sectors, which are not only faithful proxies of the country’s economic growth but also use large quantities of fragrances in their products. These comprise personal care, hair care, skin care and cosmetics, fabric care, household products and fine fragrances

Year 2017

- In the past, we were content being a large Indian company. We soon realised that our market was relatively small by global standards; the time then has come to evolve from the ‘small big’ Indian Company to the ‘big small’ global company.

- Keva will enter select countries instead of spreading thin across a large number. In view of this, our global presence will be generally built bottom-up through a deeper understanding of grass-root customer needs as opposed to sitting in India and attempting to guess what might work in remote markets.

- For one, we do not expect to enter a large number of countries at one shot; we will enter only as many countries that fit into our strategic attractiveness criteria. Besides, we will enter only those geographies where we see demographics unfold the way they did in India, leveraging our familiarity into how consumer response and appetites will evolve in the future.

- Did three small acquisitions but all in India – Different from stated objective

- Opened a fragrance Studio in Amsterdam

Year 2018

-

The Flavours business was also hit by strong headwinds due to geopolitical turbulences and a sharp hike in citrus oils and other raw materials leading to 18% decline in the international market

-

Interestingly, this performance came despite the unprecedented raw material disruptions in the later half of the year, which we weathered successfully through our focussed inventory management.

-

There were some unprecedented supply-side disruptions that impacted the industry during the year

-

External factors beyond our control caused these disruptions, which included some problems with supply of ingredients due to a major fire in BASF’s German chemical plant, forcing them to declare a force majeure.

-

Then there was the environmental clean-up drive in China that led to the closure of several chemical plants in the country.

-

The hurricane Irma, which hit Florida in September 2017, adversely affected the availability of citrus oils and other raw materials, which hit the supply chain quite badly.

-

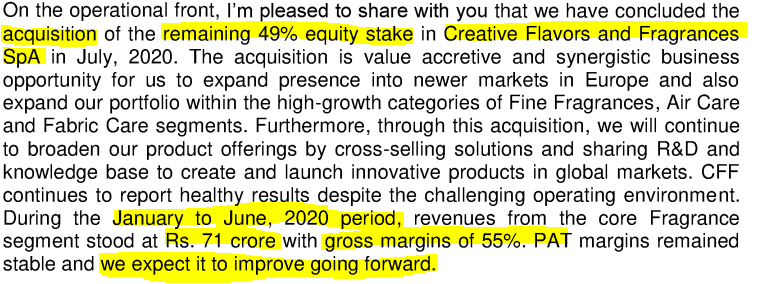

The acquisition of Creative Flavours & Fragrances SpA (CFF), an Italian company headquartered in Milan, endorsed this strategy. With the acquisition, which took place in January 2018, we have acquired 51% ownership stake in CFF, which is one of the top five players in the Italian market today and is engaged in the production and sale of fragrances.

-

As per the agreement, the company is to acquire 51% stake upfront for approx. Euro 12 million. Remaining stake shall be acquired within three years, consideration for which shall be paid based on CFF’s performance.

-

We believe this acquisition, along with our Fine Fragrance Studio in Amsterdam, will strengthen our strategy to expand our presence and product offerings in our focussed growth areas.

-

The Studio has excellent synergies with the newly acquired CFF, as both Amsterdam and Milan, being fashion capitals of the world, will provide us with access to the premium ingredients.

-

Keva Fragrances Pvt Ltd has acquired 100% share capital of VN Creative Chemicals Pvt. Ltd. (‘VNCC’), which is in the business of aroma ingredients. The acquisition provides us full control of land and manufacturing facility in Mahad, Maharashtra, giving us the lever to optimise our Opex in the overseas fragrance division. We expect to showcase higher operational efficiency in the Fragrance division from FY 2018-19 onwards as a result of this initiative

-

One major step that we expect to significantly add to our cost efficiencies is our decision to operationally reorganise PFW Aroma Ingredients B.V. (‘PFW’), which is expected to be completed by mid-2018. Restructuring of the PFW operations is expected to allow greater flexibility in backend manufacturing, leading to better profitability going forward. Our R&D facility in the Netherlands remains fully functional and will continue to be a key focus area for powering our future forward growth strategy.

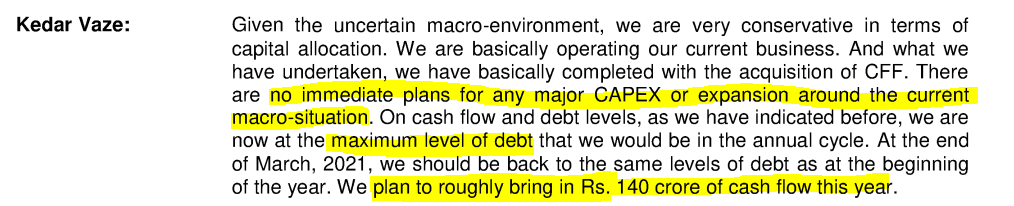

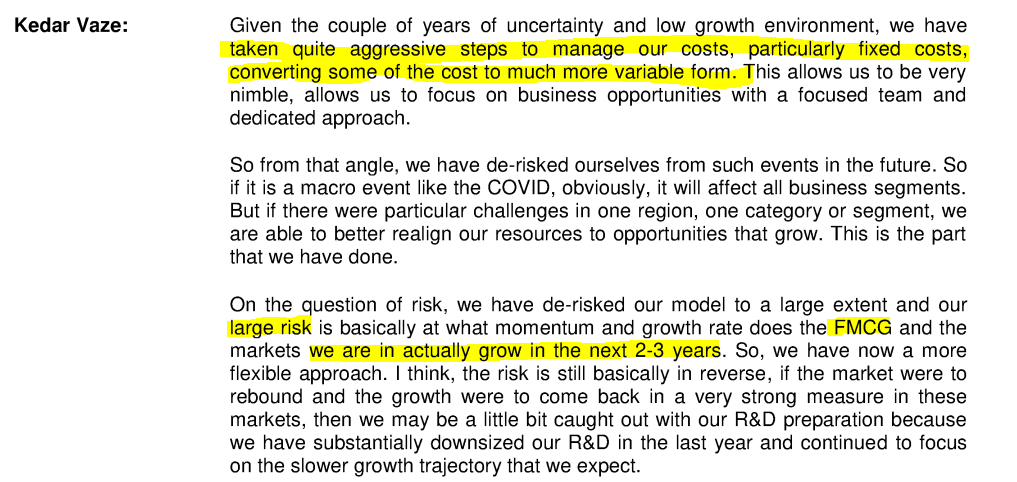

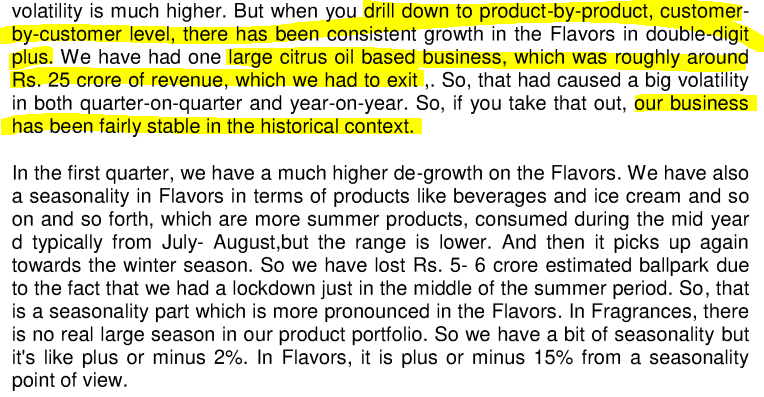

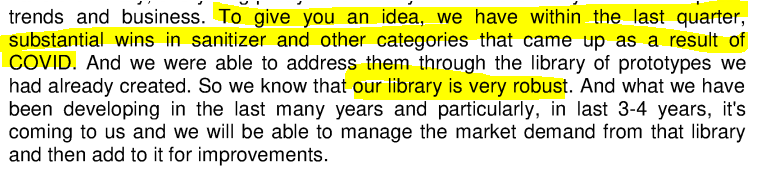

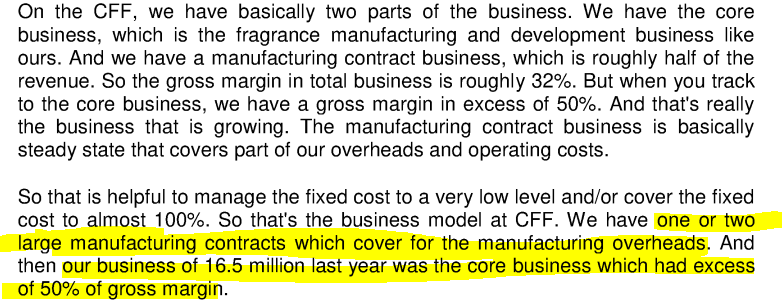

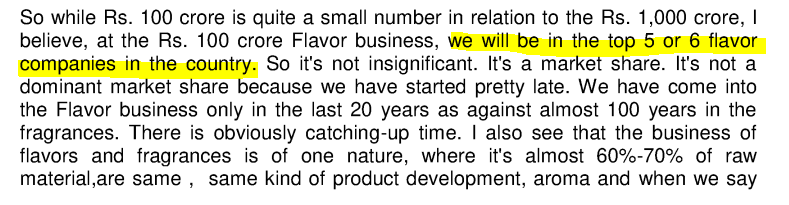

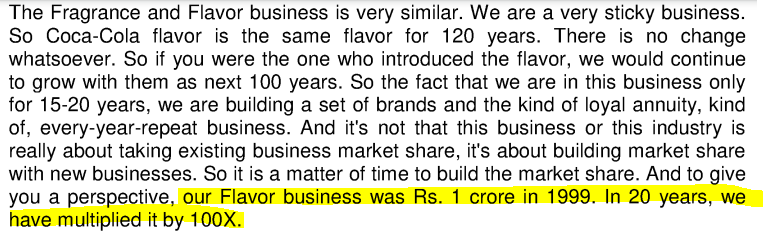

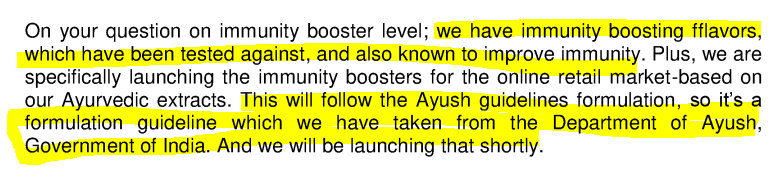

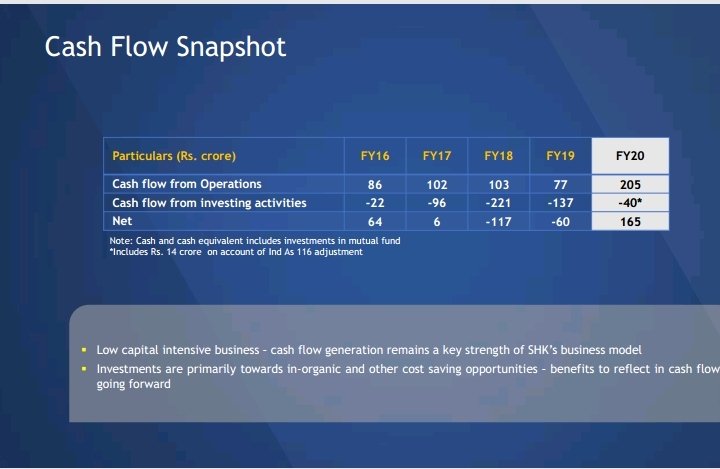

Earnings Call for Q4FY20 and Full Year")