Curiously this valuation also gets promoter stake to ~75% …the permissible limit…

Thanks Mahesh. I agree that valuations are not exorbitant.

@Mahesh and members tracking,

Any reason why the working capital is stretched over the years ? (data from screener)

There seems to be some inaccuracy in data posted by you. Do refer prospectus/past consolidated ARs of SHK to arrive at figures and they seem to be more or less stable over last many years. The nature of the industry is such that the company has to hold on to a large inventory of varied RMs as each F&F blend is composed of multi ingredients mixed in minuscule proportions.

Rgds.

Discl. - Not Invested in SHK

@Mahesh Yes. There was some inconsistency in the data I extracted from sceener. Got the below data from RHP. Thanks

Attached are my notes from annual report (posting link, since jotted too many points):

Disclosure: Invested

4 Likes

Hi Kaustubhkale,

would like to know on SH Kelkar,last week Kedar Vaze Reuduced his holdings.Any idea?

what is going on SH Kelkar.

Thanks,

Venkat.

Yes saw that he reduced his holding. Stock price has done nothing in the last many quarters, in-line with company. I am not adding more, but continue to hold existing holdings. Wondering whether it is a case of good company, great business and not so good management (not saying from CG perspective, but from managing the business perspective). Can be a case where mgmt is not mcap hungry also. Will have to watch and wait. Can tolerate mistakes, but not mischief. I am pretty sure this is not a case of mischief.

1 Like

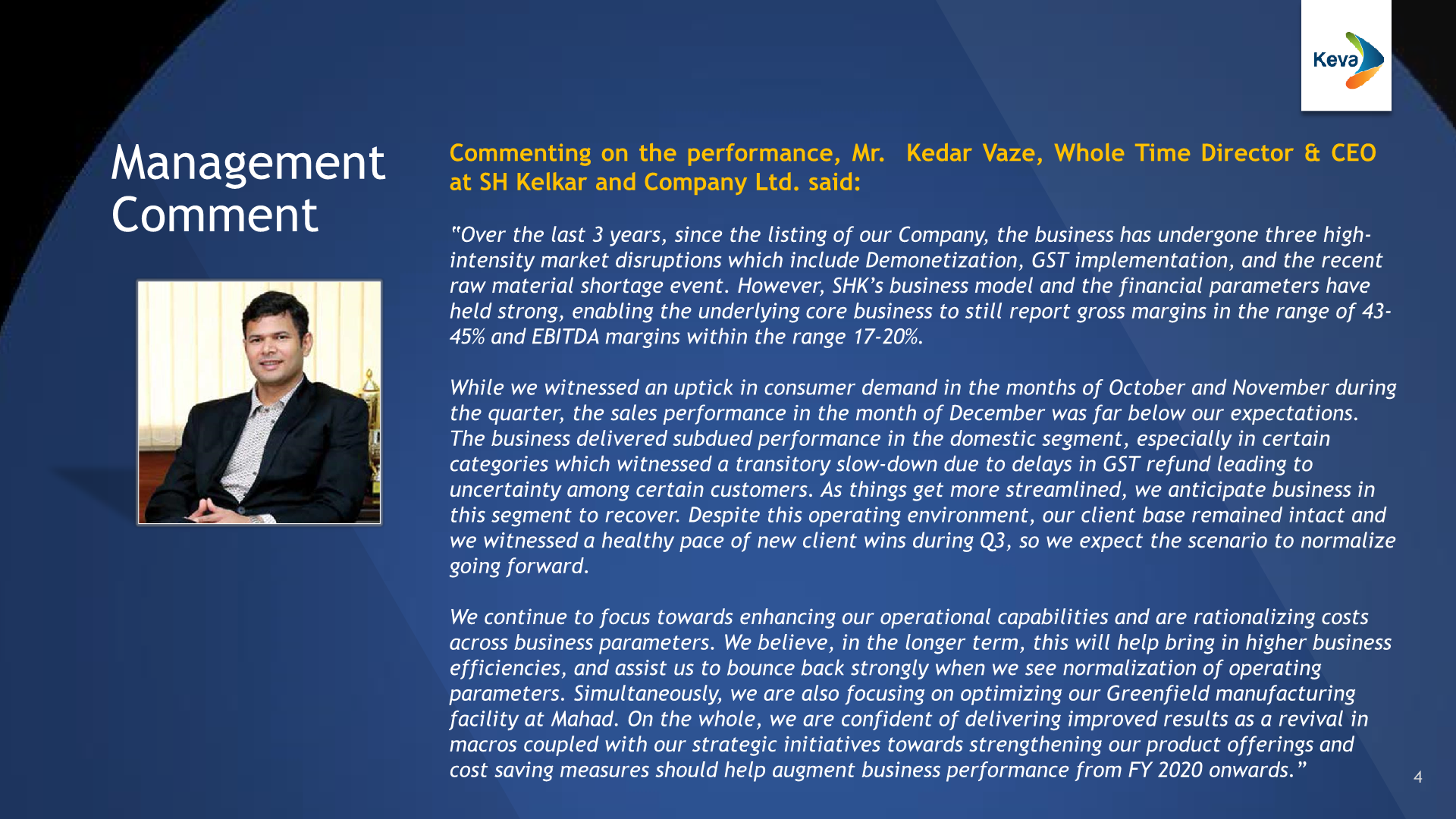

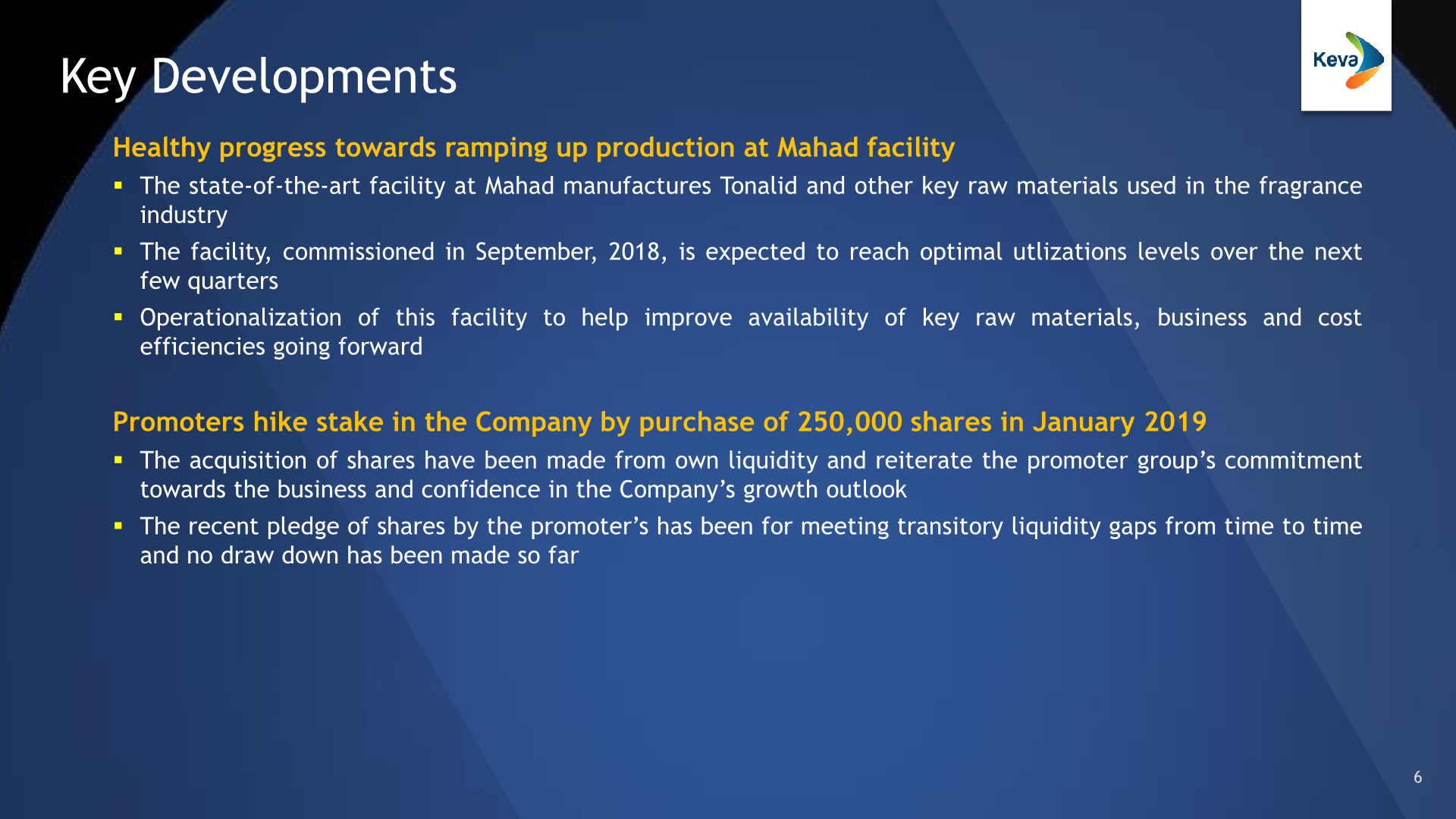

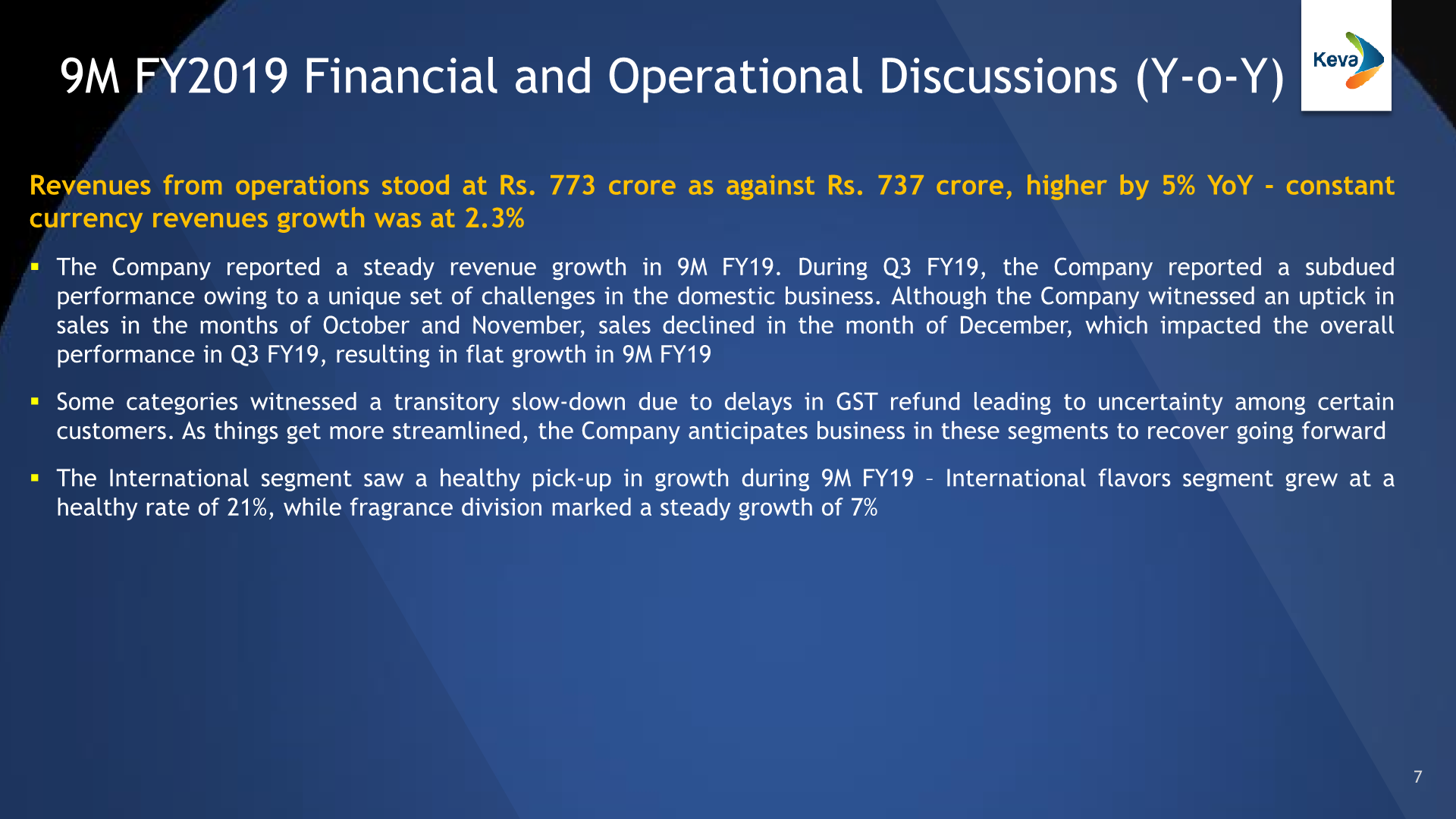

Results & Presentation:

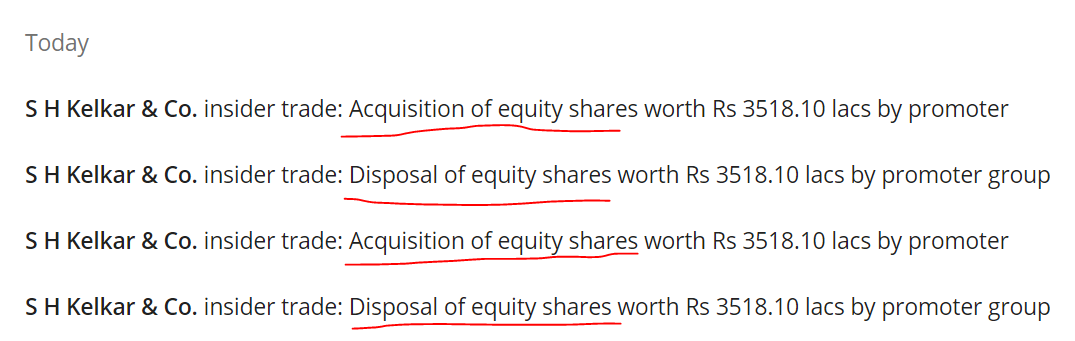

Its only single trade of 18 lakh shares between promoters .Nothing to get alarmed on that.

1 Like

Investor Presentation:

BUYBACK APPROVED AT 180/-.

any idea what is happening on this stock. The company is one of the largest players in the country and supplies flavor and fragrances to FMCG…why is stock getting battered so much despite a semi chemical play

But only now it is getting to sensible valuation of 17 PE.

Here is the last quarter earnings’ report by Motilal Oswal.

SHKL sources 30% of its raw material from China.

1 Like

that is due to exception item of 36 cr in Q3. Once you remove that its close to 10

I am following this script from 80-90 levels. Nothing seems to be wrong except the lockdown blues.

- It was expensive but the nature of business and high value client justifies that.

- Has broken all its support levels

- Prima facia looks like a MF or FPI has moved out of the script.

- If the management is not hiding anything, it can easily multiply 3x from here.

Disclosure- Entered at 65 level. Looking to accumulate.

3 Likes

Any way you can repost this link? The site is not assesible