Q2FY26:

• Content licensing (AI Datasets) revenue stream can be lumpy in nature and does not follow a seasonal sales cycle like our traditional Education content businesses.

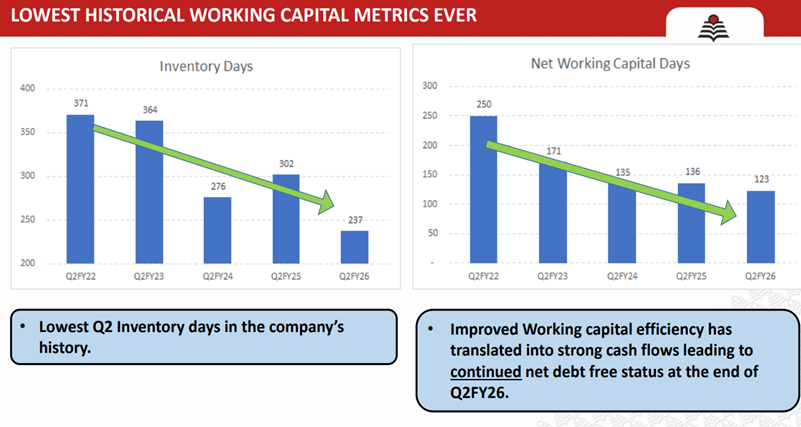

• We remained net debt free at the end of the quarter with a net cash balance of Rs235m (vs. net Cash of Rs93m in Q2FY25)

• We look forward to NCERT releasing books on the new syllabus over the course of the year. We expect FY26 and FY27 to see maximum adoption of the new syllabus books which should help our growth trajectory for the company.

• On an absolute basis, we billed content licensing (AI Datasets) revenues of Rs142m during H1FY26 vs. Rs160m in H1FY25.

•

•

• Guidance maintained

• We are confident of a strong sales season on back of new syllabus books in January, 26 - March,26.

•

•

•

•

•

• Approved to invest upto an amount of Rs. 12.00 crores (Rupees Twelve Crores only) in one or more tranches for a potential acquisition of a Company engaged in the supplementary books adhering to the International Curriculum for the K12 school segment.

CONCALL NOTES:

• NCERT NEW SYLLABUS BOOKS: PDF versions of the new NCERT books have been released and available for Class 4th, 5th, 7th and 8th on the NCERT website. We would wait and watch for its physical availability in the market. We expect the full adoption of the new syllabus books for Classes K-12 by FY27 and are fully equipped to utilize this opportunity over the next 2 sales seasons.

The guidance remains the same, as we have said earlier. And the physical availability of books is still not there, and we are waiting for it. And now after this, more or less, the curriculum will be complete of NCERT, after the release of these books physically. NCERT is releasing their books in a piecemeal basis, not in a full stack basis. So, this time, after doing this, the market, would not be that confused as it was last year. So, they will know that now the new syllabus has come out and the physical NCERT books is also out. So, market would be clear on that regard.

Basically the NCERT curriculum is being launched in a staggered manner, and the full curriculum will be launched by this year end, and then we will be able to get the full results of the NCERT curriculum benefits. So, the books were not released in a full stack basis, they were released in a piecemeal basis. So, it got staggered. And that delay basically confuses the schools and we were not able to get the amount of growth of benefits that could have come in. But now after the release of these books, we might see better benefits in the coming years. So, this year we might get some benefits. But, we feel that those benefits will start coming in from next year onwards.

• We have entered multiple partnerships for content and Licensing including Allied (ICSE Books), Discovery, Amar Chitra Katha, Money Prep (Financial Literacy), Speedlabs (JEE and NEET Foundation) etc. These various initiatives will help us expand our catalogue offering to Schools.

• AI DATASET BUSINESS: The AI Datasets business is evolving, and the deal timings may vary quarter to quarter. We are working towards making this a steady business through various initiatives and last year we had two Clients, this year we have got four and we are speaking to the fifth one also. With the AI LLMs evolving, the need to train the LLMs on quality, verified and researched / copyright data will continue in the near future. Our large repository of text, illustrations, images, videos, question banks and audio data in multiple languages will hold us in good stead.

Sales Guidance: So, last year we did about Rs19.5 crores. This year we are looking at about Rs25 crores as of now. So, that’s where we are. This number could go anywhere. One single deal is about a million dollars. So, I mean, it can really change. The Rs25cr can become Rs35cr at any point of time. So, we continue to have conversations, but of course, once you sign on the dotted line is only when you confirm it.

Why it’s a lumpy business: Because these deals happen at different points of time. Again, it depends upon the customer’s requirement. So, between various customers, the requirement keeps on changing and the content that is required by our clients of course, also keeps on changing. Some of them are perpetual deals, some of them are fixed period deals. So, that keeps changing as well. So, it’s a new business, and because of which, there is no quarter-to-quarter trajectory as of now.

Perpetual versus limited duration deals: for last year, I would say, it was 50-50. But this year, it’s gone to 25% being renewal ones and 75% being perpetual.

Outsourcing of content: If a customer has a requirement and we cannot fulfil all of it then we have to arrange for that from other publishers. We become the single source for them to get content. So, if they want something in a single language, no single publisher would have that much of content. So, we go out and source from multiple sources and provide them as a one-stop solution. So, that’s where it is. Of course, since we have to pass substantial percentage of it down the line, so there, of course, our margins would be lower on third party content.

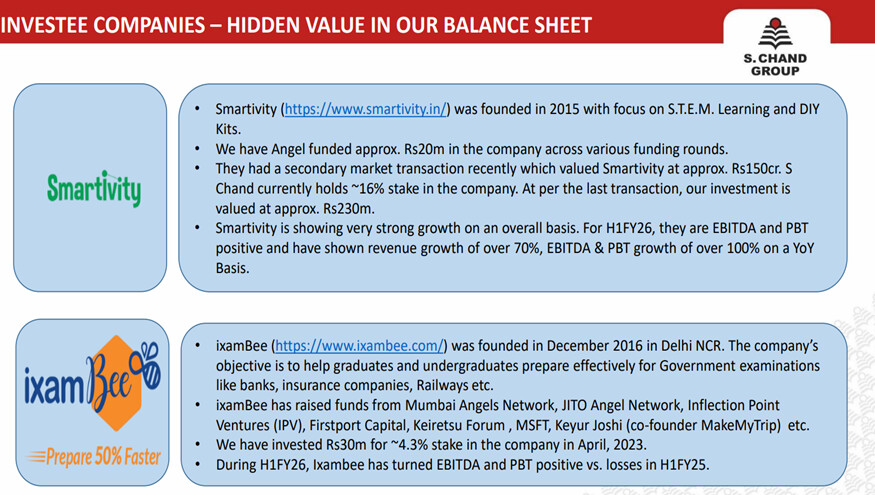

• ACQUISITION: We have finalized one acquisition, which is in the international curriculum space. I can’t share anything beyond that, but this should be completed in Q3.

International curriculum we are doing for the first time. And it’s almost around US$1.5 million. And, we might do some part of it as debt, although we have cash, but foreign currency debt is always easier.

So, basically, what we are trying to do is, we’re trying to fill in the gaps because see what happens is, like IGCSE or IB space, we don’t have many books and we don’t have a brand in that segment for international schools. That’s why we want to look at acquiring somebody.

So, they are about a thousand plus international curriculum schools in India. Growing very fast right now and currently, we have no products for that. So, plus of course, we have good relationships in Middle East, plus South Asian countries, Sri Lanka, All of South Asia, there are a lot of these IB and IGCSE schools. So, once we get a hold of content in that segment, which has been, of course, a good brand, that would help us expand in that segment. That opens a new vertical for us, which currently we are not addressing.

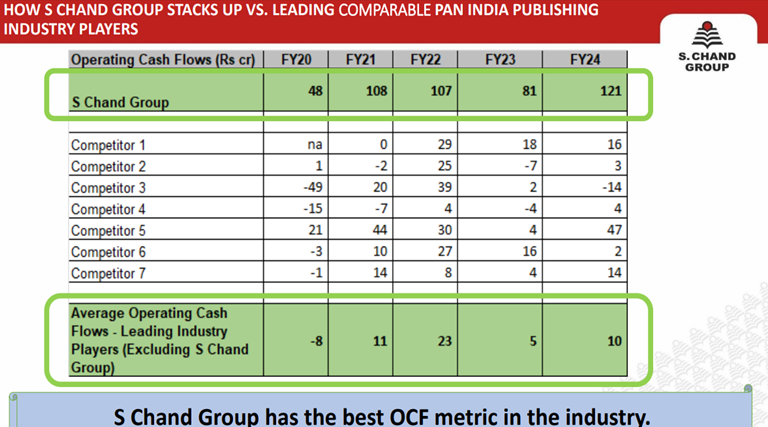

• So, I think our strategy continues to be conservative growth, but not very aggressive. I mean, we will not push too much to ensure that we are only growing revenues and not the bottom line. Our focus is to ensure bottom line and cash flows are important. We’ve been able to generate almost Rs100 crores of operating cash flows every year for the last five years. I mean, if you look at the industry, if you put in the even the top 10 players all together, consolidated, they’ve not been able to generate so much of money.

• We have some gaps in, I would say, like in international curriculum expansion. We have some gaps in I would say, school regional segments. We have some gaps in, I would say, like non-core textbook area, which is like supplementary books area, Test Prep area. So, we have gaps in computer sciences. We have gaps in 4-6 areas. So, as and when the opportunity comes in and the price looks decent, then we might look at acquiring. We have spoken to a couple of other companies, but the deal didn’t go through for some reason or the other reason. But if we find any good opportunities, we might be able to fill these gaps.

IN CONCLUSION:

S Chand thesis is still on track. Decent growth this year with accelerating growth next year as new syllabus textbooks get fully adopted and Acquisition + AI dataset segment adds further revenues. Still At dirt cheap, deep value valuations.

DISCLOSURE: INVESTED