Hi guys! This is my first post on this forum so please be gentle:) As this is a turnaround story its best to start with a bit of corporate history to see what went wrong here.

PART1

HistoryS Chand came out with an IPO in 2017 before which it was on acquisition spree and this helped the company grow its revenue at 33% between fy12-fy16 .In this business its very difficult to grow organically because its hard to incentivize schools to change books in their existing curriculum. Most brands have long relationships with schools. So the plan was to increase market share by acquiring new brands . It made its first acquisition by buying out Madhuban in 2012 . Subsequently, it acquired New Saraswati House that has a strong grip in Sanskrit, French and Indian regional languages. S Chand acquired Chhaya Prakashani in 2016, which has a significant presence in the West Bengal board.

But acquisitions came with challenges. At the same time it was investing in digital. 2018 is when one saw early signs of trouble started reflecting in their numbers. Receivables started increasing. There were sales returns from select dealers resulting in bad debt. Also there was a lot of confusion around the national education policy which was originally supposed to be adopted in 2019 because of which a lot book sellers did not buy books as they wanted to clear their existing inventory . (Right before an IPO theres a tendency to push sales aggressively . I am not saying thats what happened here but its possible)

S Chand 3.0 In FY19 Management started working on cost optimization through following measures

- Stopped working with dealers with bad credit history

- Rationalization of number of offices and consolidation of warehouses .Resulted in warehouses from 19 states to 4 locations.

- Inventory management- Focus on portfolio of faster moving titles and rationalizing number of printed SKU’s on basis of sale.

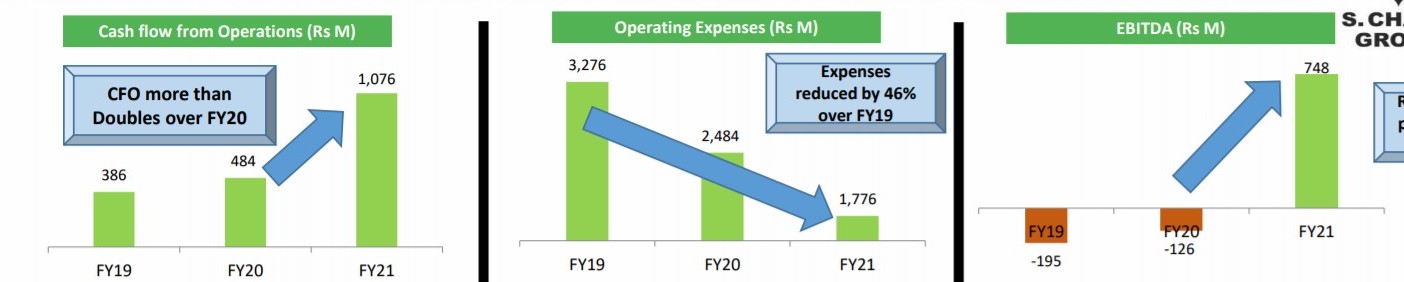

*Reduced their employee count thus lowering employee cost from 151Cr in FY19 to 99Cr in FY21 • Further due to covid .Travel expense of sales team reduced.Also educational events for teachers/schools like academic conferences were conducted online at a fraction of cost.Some of these cost will not come back as like a lot of companies S Chand too has learnt to do business in the digital way. All these let to a turnaround n FY21 this is despite collections being effected by covid

I will let the numbers speak for themselves. Pls see pictures below from investor presentation

Cashflows have more than doubled while revenue remained flat YoY

. most of the times its just management correcting their past mistakes. No reason to congratulate someone for putting band aid on self inflicted wounds. but i also believe sometimes it’s just bad luck.

. most of the times its just management correcting their past mistakes. No reason to congratulate someone for putting band aid on self inflicted wounds. but i also believe sometimes it’s just bad luck.