Valuations are quite personal tbh but just to tell you how I look at it, it is trading 4x market cap to cash flow. The company is reducing its expenses and focusing on better cash conversion. The near term triggers like NCE/NCF Implementation might help the company to grow 20-25% for couple of years from current levels, in this scenario, the bottom line will grow much faster than top line.

While valuing I considered above points and added some margin of safety due to underlying risk and past track records before coming to a right valuations for me(There is no right answer). At the end, it’s a game of probabilities.

Disc: Invested, no recommendations

8 Likes

Some of the things which came to my mind -

During my school years, SCHAND books mostly came into my radar after 9-10th when focus shifted away towards science and mathematics stream. With the NEP, initial sense that I have got is that focus would be on wholistic dev of child and new age tech stuff and that would lead to more educational material related to -

- Giving proper knowledge of history of India and world

- Bolstering multi disciplinary thinking in child

- Focus on ethics and values in child

- Focus on life skills

- Focus on ethics and values in child

- Focus on new age technology skills

Initial sense I have gotten is that new curriculum will add new stuff to what is currently in the educational system and there will be some modifications as well. I do not know if there will be significant modification in science and maths where SCHAND is strong per my experience. Ofcourse I do not have any experience with other streams - Arts and Commerce if SCHAND books sell there as well or not.

Also, in the past CBSE used to say to schools that use NCERT books to teach students. And over time NCERT books got better as well to cover more material. If NEP comes, there can be similar risk again where NCERT updates all the curriculum and initially students flock to buy more NCERT material until SCHAND authors catchup. Some random thoughts while thinking what are NEP related risks… (can prove to be completely wrong)

6 Likes

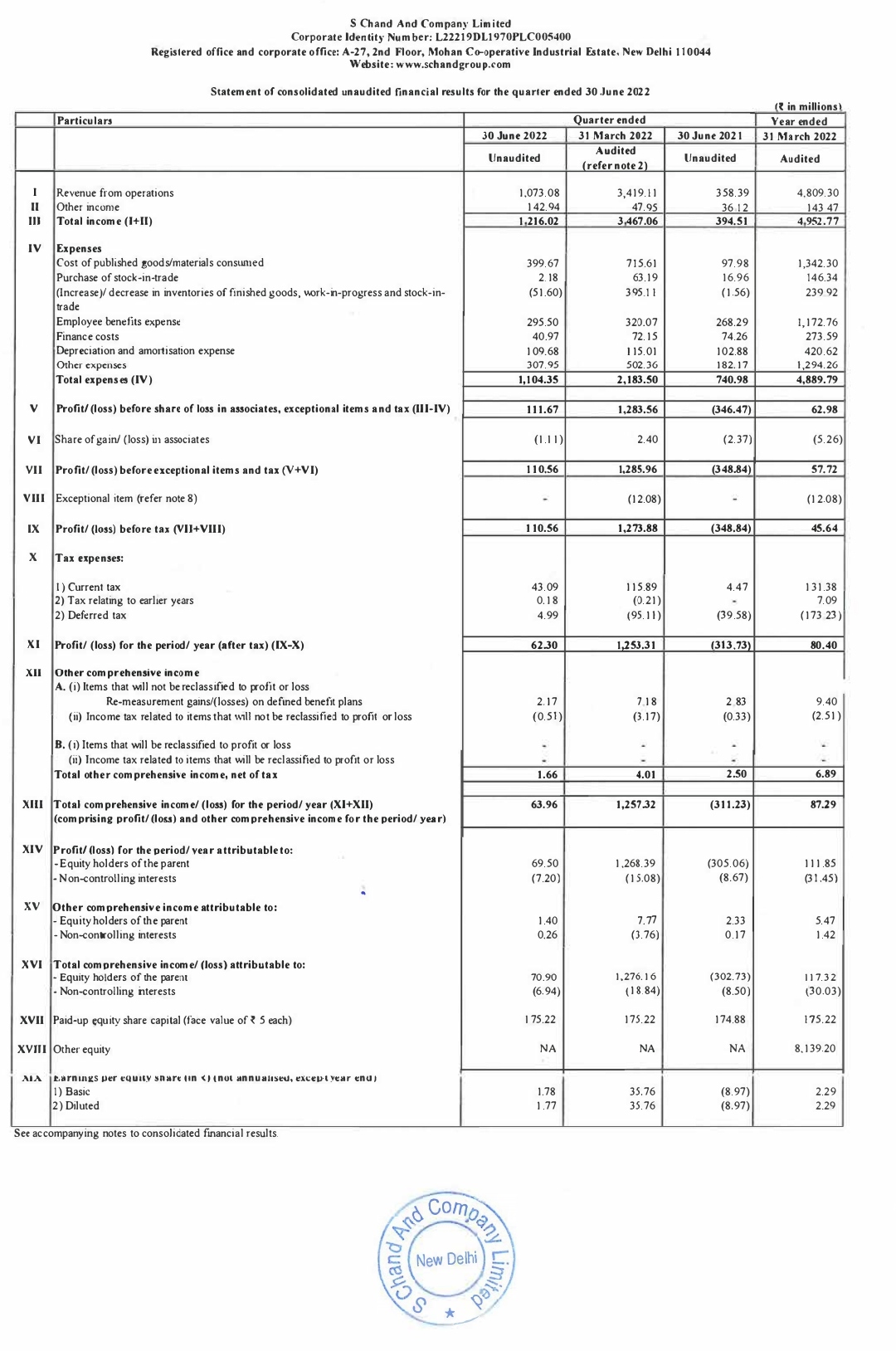

Q1FY23 Revenue is 107 cr. It’s very nice to see the management is walking the talk. Last concall they said they should be able to do 90 cr revenue in Q1FY23 and also told the reasons that made sense. Now it’s showing in numbers too. Hope they will be able to meet the guidance given for FY23 excluding NEP/NCF being implemented.

7 Likes

In the recent concall, the management stated that they wish to focus on their core publishing business rather than edtech businesses. They mentioned additional spends on edtech business won’t scale the revenues by significant amount. Hence, they will cut back on edtech spends.

Secondly, they mentioned that paper was no more available on credit to entire publishing industry. This will really help the big players becoming bigger, if the big players will be able to secure raw material timely and lead to market share gains. So far, they have secured most of the raw material supplies for the year and only 20% or so it left to be procured. (They import paper and buy from West Coast, Kuantum Papers in the domestic markets). Paper cost is 20-25% of their total cost as highlighted by management in the concall.

9 Likes

testbook was sold for 15 cr recently. according to q1fy23 concall

2 Likes

This stock is making a strong comeback. Significant improvement in fundamentals (both in P&L and Balance sheet). After multiple years of under-performance, looks like the company is poised for multi year growth. Their cash flows, debt and debtor days have shown remarkable improvement.

In the last quarter, FII “The Miri Strategic Emerging Markets Fund Lp” has taken 4.3% stake. Money control have included this stock in their latest coverage. https://www.youtube.com/watch?v=JhOLXeBFoNw

Anyone tracking this stock?

Disclosure: Invested

3 Likes

Yes, have been tracking.

Not sure if it’s a multi-year growth story - but looks undervalued for sure