I’d say it’s too early to say if PSU asset quality has started to improve. There is an inherent cyclicality to asset quality which keeps playing out. Last couple of years saw NPAs bottoming out which led to higher profits for lenders and more impetus for the latter to grow their loan book. But as we have started to see from the increasing provisioning of leading lenders, NPAs are now picking up and in some years they might start peaking out. Then we’ll see real difference between high quality lenders with strong risk management and the others. So let’s wait out 1-2 years.

Also I won’t be sure of quality of PSU management. Most CEOs are appointed by policy of revolving door with many pushing retirement age, with no real incentive to upset apple cart, and even the best ones find their hands tied with bureaucracy.

But again I could be biased against PSUs based on my experience with their stocks in the past and this time it could be different as you pointed out.

REC funds EV -Buses apart from Solar, Green hydrogen. Plans to fund Green Ammonia which has huge potential in overseas market apart from domestic demand.

REC has already funded 10,000 EV’s during Fy2024. They plan to fund 50,000 EV’s during next 2-3 years. There Is going to be huge demand from State Govt undertaking such as STU’s who are replacing existing and ailing Diesel bus fleet.

REC Ltd’s disbursal towards green hydrogen projects in FY24 stood at Rs 7997 crore from nil disbursements made in FY23.

The company’s funding in the solar energy space has more than doubled to Rs 20,956 crore in FY24 from Rs 9031 crore in FY23.

REC predicts that prices of green hydrogen which are close to USD 5-6 are likely to come down to USD 1 by 2026-27, on the same line as solar, which was costing Rs 16 per kWh, a few years back to current discovered prices of Rs 2.5 to 3 per Kwh with more players entering the space.

REC plans to support funding for producing green ammonia, which is in high demand in Western European countries such as Germany, the United Kingdom, and France.

Disclaimer : Invested from lower level for long term. I may be biased. it is not a buy or sell recommendation.

Please do your own assessment before investing. NBFC’s do carry risk of NPA and PSU,'s in particular are subject to frequent policy changes by Govt.

RBI proposes tighter project financing rules for long term under construction projects

Today , Stocks of NBFC’s and Banks engaged in long term.project financing are down today reacting to the news of the RBI draft proposal seeking higher provisioning for under construction projects , even if the asset is a standard asset Class.

The initial provisioning of 5% can be reduced to 2.5% and then further to 1% on subsequent years as the project progress successfully.

While the draft seeks suggestions from all stake holders , i think it is good for the overall health of the financial system in the long term since it should not come as a surprise as a large chunk of money for provisioning all of a sudden in case of under construction projects becoming NPA at operational stage due to various reasons. In the short term during initial period , it may impact bottom line of NBFC & Banks to the extent of exposure to long term project financing, though the providing can be reversed back during subsequent years of the project continue to be standard asset without NPA.

RBI is certainly ahead of many of their global peers in seeing danger signs of an overheating credit system and all these steps will ensure long term health of our lending system. That said it may cause short term pain to investors as we have seen with private sector lenders whose stock prices have taken a beating post RBI guidelines.

But still I will be more comfortable staying invested in Bajaj Fin’s, Kotak’s, HDFC’s given their track record, strong risk management processes and healthy balance sheets.

So, stock investing is not without any risks- any stock , any sector …or whether it is hdfc , kotak or Bajaj. Every sector every stock has its own down and up cycle. Let us recognise that Nothing is permanent and no stocks will keep rising for ever. There has to be a brake or intermittent correction at some point of time- we have seen in many counters and REC/ IREDA is not an exception. It is observed that Even with intermittent rise and fall , REC still has given 300% return during last one year, 80% CAGR fot last 3 years and 40% CAGR return during last 5 years. These returns don’t include hefty dividends yield of 10% . let us compare these data with that of Bajaj , hdfc , kotak which can give us some insights…

Given all these risks, as an investor , we are

here to make money.

so entering a stock/ sector early when it is in upswing or up cycle, profit booking intermittently and exiting early during a down cycle is an ideal way of making money in this risky stock market.

Identifying up and down cycle at early stage is an art by which many prudent investors make money

Fully agree. Somehow I realize I don’t have this talent in me to identify upcycle, downcycle, suitable entry and exit points to make money in short term trades. Only solace I have is that even some of the well known big investors don’t have this skill in them- to call out market cycles.

Those who can identify microtrends in stock market on a consistent basis, exploit them and build generational wealth are truly blessed.

Only thing I am good at doing is follow an age old dictum that investing is a loser’s game which means if I can protect my capital through ups and downs of cycle, minimizing unforced errors, I’ll end up making money which has kind of worked for me. Where there is risk, there also needs to be risk management. My idea of good risk management is to stay with quality stocks for a very long term with meaningful allocation to let compounding build wealth for me.

That of course comes at the cost of missing out on a lot of rallies and flavors of the day. But again there is not a single rule for making money. If something works for an individual they should stick to it.

I too don’t have the art of doing short term trading, upcycle, down cycle , very poor in technical chart analysis…

All my investments are long term. 50% of my current holdings are more than 3 years , 80% of my holdings are more than 1 year.

My expectations are moderate which I get through investing in to value buys, though I fail many times , which becomes a learning.

I am not an agressive investor…not in to small caps , mid caps…unless it is a PSU value buy. This strategy has worked out for me till now and I would like to stick to it… unless there is a drastic change in micro’s and macro’s.

According to.Company sources REC Ltd. and Power Finance Corporation (PFC) Ltd. will have no impact on their profitability due to the draft RBI guidelines on project financing.

The brokerage firm CLSA also confirmed in its note. The overall impact, according to CLSA, will be on their capital adequacy ratio and both companies are well capitalised.

I have gone through some of the YouTube video of pulak. He may be right to some extent…

While capital protection is important. But at the same time, as investors we also need to get some return at least more than Bank FD , though return expectation could be different for different people depending upon one’s risk appetite time horizon.

And with so many investment strategies available today in the market place , thanks to our so many Guru’s / authors on stock investing , it may be possible for everybody to make good money in the market place if the strategies are learnt and followed. Someone said , “market is my only Guru, and I still make money, though I pay regular tution fees to the market for teaching me lessons from time to time”

it may be worth mentioning that many conservative investors even without any Guru or without having to read those famous books on stock investing or technical charts and without any knowledge on Micro’s and Macro’s make Good money @30 % CAGR in a 10 years period through SIP in a couple of MF’s, if the investor is consistent in SIP’s. If you are aggressive in MF investment style in choosing Small Mid caps , one can still make more money in long run.

In fact , 40% of my investment is through MF SIP’s which I never stop whether we are in bear or bull market and it works great

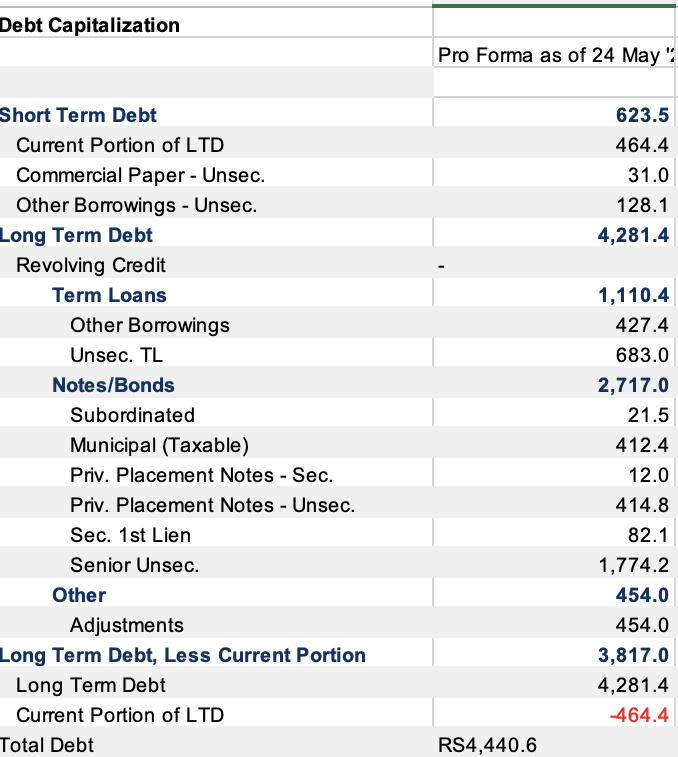

Can anyone point out what % of its borrowings are short term and % long term. In case in second half of the year we get RBI rate cuts, how does it impact NIM.

Agree !

But PSE index up 6% where as REC PFC up by 12 % , which means that Mr Market finds these PSU stocks are still value buys within the PSU pack with risk adjusted returns, we as individuals may differ in our views though