NIM is 4% average of last 3 years as published during the IPO.

NIM that of REC PFC is 3.42 to 3.46 % .

But that does not explain so much difference in valuation.

Even 40% portfolio of emerging RE which IREDA has no competition does not explain such huge difference in valuation.

I can only say that it is an euphoric move by investors on renewals plus all PSU stocks getting re-rated. Market perhaps discounts PM Modi’s re-election in 2024.

Discl: Disposed off IREDA which I had got a small allotment in IPO and shifted the fund to PFC / REC where I see a lot of scope for catch up. May be i will catch up IREDA in declines if there is an opportunity.

This is not a buy sell recommendation. Please do your own assessment before you invest.

PSU stocks have inherent risk of frequent Govt policy changes , elections ahead

@1957 The valuation piece with this company is very tricky. Nobody liked it below 2 PE and market seems to find value at ~8 P/E. So, this is a difficult call to take - Right now, my thought process is to hold majority of my position and may be do a small bit of profit booking.

@LarryWink Yes, one should always do the full Due Diligence of the investments. However, to my mind, the difference in these metric (if any) would not be sufficient to explain the valuation differential.

Disclosure: Own PFC and REC and Not a Buy-Sell recommendation. Pls do your own DD.

After having taken investment positions in PSU pack two-3 years back & tracking the performance of these stocks thereafter , my take as follows, though there are conflicting views from different analyst on PSU stocks.

The PSU stocks especially railway , defence, renewables, (REC- PFC is a part of renewables) have undergone re-rating substantially and may further continue to do so wherever there is a scope if the govt policy such as heavy capex in infra project, railway , defence capex and Atma Nirbhar Bharat scheme continues . The other reasons for re-rating may be as follows as per my views

Have you heard of any PSU

(1) where CFO of a PSU resigning or any auditors resigning ?

(2) Any manipulation of balance sheet ?

(3) Diverting fund by promoter to other unrelated areas or related party transaction ?

(4) Promoter share pledging ?

(5) with worries such as USFDA compliance such as in pharma ?

(6) Not paying a substantial dividend consistently every year - though the amount may vary - The Govt holds majority stake and they need money in terms of dividend from PSU

(7)facing Income tax raid or GST raid ?

(8) Promoter entity Caught with insider trading

(9) working capital issue or fund raising issue from domestic/international market- All agencies are ready to lend to the Govt with most convenient rates?

(10) Not getting enough order from its customers ? Well, in most cases, the Govt is the customer and so the order book is healthy as of date is full for next 4-8 years.

If any of the above happens to a listed pvt stock which keep happening every now and then , the market becomes nervous and the stock price crashes.

The risks i could see in PSU stocks:

(1) If the govt changes its current policy as mentioned in 2nd para of this post

(2) The Govt is a majority share holder of most of the PSU’s. At times, They may take decisions which may not be in interest of minority share holders,

(3) OFS is frequent and normally they sell at a discount of 8-10% every time. Good thing is that they first give a hint in digital media and after few days or a month or so, they declare OFS But then after having faced 2-3 OFS , i have found that the stocks have bounced back.It could be seen as a blessings in disguise as many institutional investors are on-boarded and the minority share holders gradually become majority and they can counter any decision by govt if it is not favourable to the shareholders.

Discl: Remain fully invested in a pack of Railway , Defence , renewables since last two years.

It is not a buy or sell recommendation in PSU stocks . Please apply due diligence before investing

One of the advantage with IREDA was financing small (rooftop) solar installations. With REC leading National Rooftop rural scheme, REC would be in much better position as compared IREDA as REC will be financing all types of Big & Small Renewable & non Renewable projects + Infra projects too.

This will open a very big market for REC and have the opportunity to grow many folds over next 5 years. I hope this help REC with PE expansion and 2-3x profit growth over next 5-7 years.

I am very hopeful of REC touching 1800-2000 over next 5 - 7 years.

Disclaimer - Invested in REC from double digit levels.

Post Q3, there are only buyers -no sellers for IREDA. While Q3 has been very good, but I am not sure if IREDA can repeat it’s performance. On roof top , IREDA is going to have a tough Competition from both pvt and PSU,'s

REC/ PFC are better placed to reap the benifits of both the world - Renewable & non renewable apart from financing other capex related themes such as infra projects. REC recently mandated to lend to railways too. The only thing we need to watch the NPA - which the management is very confident and has given guidance for net zero NPA.

Going by the valuation , REC ,& PFC are definitely better placed PSU for the medium to long term. I would not be a buyer for IREDA at this astronomical price.

Discl: Had got IPO allotment. profit booked and switched to REC , PFC . i may be biased. This is not a buy sell recommendation. please do your own assessment before you buy sell.

Om ! …nice info.

I wish i could find comparison of these 3. comparing interest margin,asset quality, porfolio, growth, OFS,Dividend,NPA,valuation,customer composition…etc.

Probably we might be able to find best amongst better ?

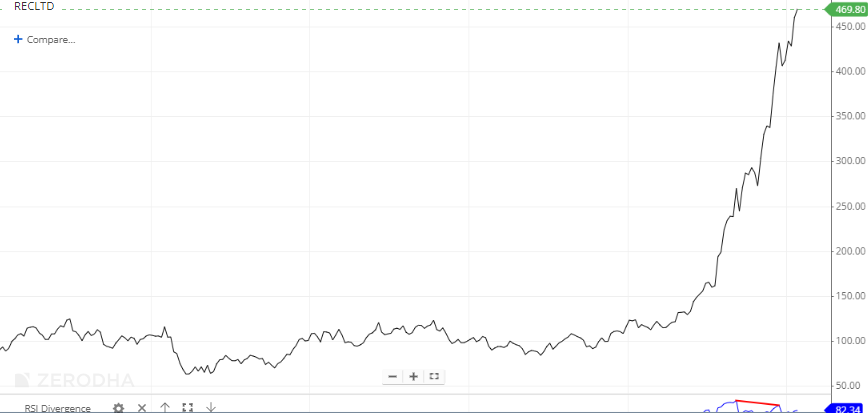

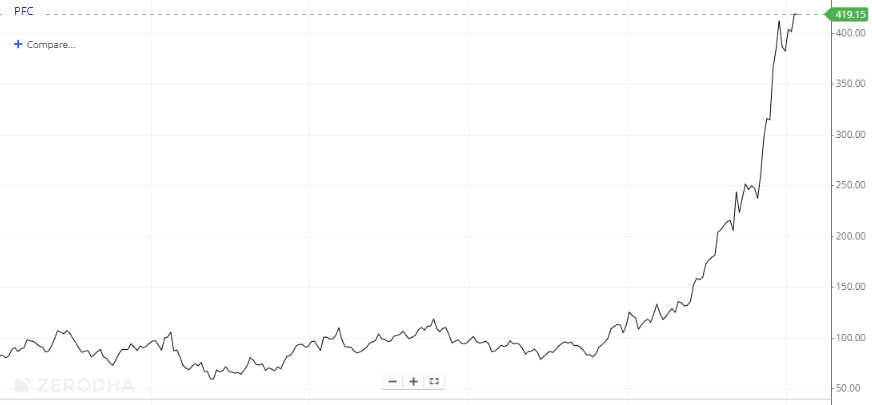

I can only compare 5 year REC/PFC chart…it looks identicle.

D-Invested in IREDA.

Dont know what is fueling the price of IREDA… IREDA @ PE 53 vs REC @ 9.5.

With all positive news in favour of REC in last 1 month, specially leading roof top solar, I would not be amused if REC goes 3.5x in next 1 year and reach PE of 30.

I think if REC changes the Rural to Renewable in its name, this only will trigger REC to double up

Green Energy , Green hydrogen, Green steel and all talking of Decarbonisation of the entire world - Now comes Green Loan - All our PSU power financing companies like REC, RFC, IREDA are are likely to receive this kind of Green Loan from developed countries

P/E is not the right valuation metric to value a financial stock. It should be price to book (p/b).

IREDA current trades at 5x p/b which makes it highly overvalued by any yardstick and seems to suggest a lot of “Green” premium. Fundamentally I don’t see any logic for green premium other than narrative and euphoria (which probably explains insanely ridiculous valuations of companies making solar panels and renewable energy).

A loan is loan, whether one calls it green or brown or any other color. A lending company, just by being in a green business, won’t be able to charge higher interest to its borrowers or borrow money at lower cost than its competitors who are NOT in green business.

When the hype around green lending starts cooling down, which could take several quarters, valuations should start reverting to industry mean.

Coming to REC, stock currently trades at 1.8 p/b which is higher than its historical p/b putting it slightly in the overvalued range. It’s interesting to note that when REC was listed it saw similar valuations as IREDA for a brief period before quickly settling down into 1.4-1.5 range. It’s only last year that PSU really has pushed its valuation into higher range giving it limited upside.

Given that REC mainly lends to power sector comprising of mainly government entities there is limited trigger for valuation rerating. But yes, smart narratives in bull markets can amplify the interest in a stock and if REC catches some of that we might see another round of action in the stock price.

We need to understand why re-rating of a stock happens ? Re-rating or De-rating of a stock does not take place without a reason. Market is collectively more intelligent than we as individuals.

Apart from P,/B ratio , P/E ratio, Prudent investors look at if the scope of business is growing with new opportunities opening up and quality / qty of order book/ Loan book , the asset quality in terms of NPA if at all it is a NBFC.

In case of REC, the NPA has come down quarter after quarter. Now it is reduced to 0.82% as of Dec 2023 from 1.12% as at 31st December 2022. The management of REC walks the talk…Now they are aiming at Zero NPA.Similar performance is seen in IREDA too !

If the asset quality worsens then de-rating may take place as rapidly as it goes up.

Why is it that we as investors look at 52 Week high , all time high etc.,? There Must be something… is it on merit or something artificial. I ignore if it seems artificial to me. but if it is on merit , i too take a plunge to buy a stock even if it is all time high- may be i must have missed the bus at the starting point but it is never too late.

I don’t challenge the market. At times market do over react , but then it corrects or re-rates based upon merit in course of time.

REC’s latest financial performance , asset quality , loan book and scope of opportunities are published by the Govt in this press release. This makes me to believe that this is an opportunity for me to remain invested for long term , given the descent Dividend yield, though I would like to keep an watch on growth in Net profits , NPA trend and govt policy on dividend distribution and if at all it continue to be investor friendly in all its policy matters.

Discl: Invested from lower level , has already given me more than 3X returns plus dividend yield. This is not a buy or sell recommendation. please do your own assessment before investing

To quote a wise investor, “market can stay irrational longer than one can stay solvent.

Someone else said that there is only king in the equity market which is valuation.

So I’d leave the time to tell us how much of this narrative in Ireda actually plays out in the long term. Again to quote (sorry) a very wise investor, the market is a voting machine in the short term and a weighing machine…”

Right now Ireda is enjoying an overwhelmingly majority of votes and all the narrative and numbers are perfectly aligned.

Can REC reach IREDA valuation or at least REC should be given Bajaj finance valuation?

REC PE: 10 PB: 1.93

IREDA PE: 38, PB: 5.6

Bajaj Finance PE: 30, PB: 5.59

Agree , REC has compelling valuations. if REC continues its current run rate with declining trend of NPA for next few quarters, Sky is the limit and it can reach IREDA valuation even exceed IREDA’s…or even Bajaj finance to that matter though Bajaj finance is a bit different kind of business with more focus on retail finance and clients are different and so both may not be comparable to each other.

The scope of business opportunities for REC are much more than that of IREDA if you see the Govt press release as per link in one of my

previous posts. REC is doing all that IREDA does plus much more.

Under Modi Govt , The PSU’s are expected to do well if there is policy continuance. The added benefit is the mouth watering dividend yield , though it has gone down recently after stock appreciation… I had entered when the dividend yield of REC was 10-11%.

However , there is always a risk of time wise correction - re-rating / de-rating keep happening for every stock / sector and for every business there is a cycle and investor fancy which is also applicable to REC / IREDA. Currently , investors and market fancy is for green energy , power financing as power demand is likely to remain high with a rising economy like ours .

If the growth rates remain sluggish for both , then De-rating could happen …more rapidly in case of IREDA due to its Current rich valuation. By the way, REC is Maharatna where as IREDA recently is upgraded to Navaratna.

Discl: Invested in both from lower level. This is not a buy sell recommendation. You may Please do your own assessment before investing.

I would not beyond a P/B of 2.5 on best case for these firms. Yes NPA is improving. But concern is that cycle repeats and current crop of loans from FY21-24 turn sour in FY27. There are expanding beyond core Power loans and funding other areas where they have no experience.

P/B of 2.0 - 2.5 should be fairly priced. Stock can indeed give decent 8-9% returns based growth and additional dividents which is currently 3%.

However if you bought at 150-200 a couple of years ago you can enjoy 10% dividend and '10% earnings growth. Easy Pickings and never sell.

That’s true that NBFC shouldn’t given such high valuation. But I a more concern with the difference in valuation between competitors. So, either IREDA or Bajaj valuation should come down or REC valuation should go up.

Baja finance is different. It’s mostly housing, consumer and personal loans. Different sector of financing and non-comparable. Not to say its not overvalued(thats up for debate)

Market usually gives a valuation premium to private players and more to the lenders who have quality promoters, clean corporate governance, execution strength and some sort of moat in their business model.

Challenge with REC is that they lend to government entities in power sector that itself is a big deterrent for investors who look for sustainable earning growth and predictable compounding in the stock prices Not only power sector is cyclical but is also one of the biggest contributors to NPAs in lending sectors. Plus recovery from defaulting government customers can be difficult given the political elements involved.

Right now there is a credit frenzy in the system and every lender is trying to grow their loan book. In this phase, stock prices of conservative lenders with high quality risk management suffer. When NPA cycle turns and bad loans start piling up in the books, investors start flocking back to quality names.

PSU stocks have been darling of the street in the past and we have seen similar rallies and rosy outlooks but they have flattered to deceive. Not sure if this time is different.

If you compare Bajaj Finance with REC, I know they are into different type of loans. But both should get similar valuation, they both have similar NPA. Hear me out why.

Valuation should be based on future growth. Till now PSU were not getting similar valuation to private player because PSUs were considered as a dying sector. Few year ago, there was no growth, management of PSU companies were not held accountable, asset quality was falling, whatever valuation was on the hope of privatisation of PSU. Whereas private player such as Bajaj had big future opportunity, little to no competition, good and clean management.

Now things have changed, due to government initiatives, PSUs asset quality have been improving, management is being accounted, growth has returned, many PSUs are now competing with private players. Whereas for private players Bajaj finance, future opportunity is still there, but now competition is high with many player pushing into the market.

I might be biased, I hold REC, I sold Bajaj Finance and bought REC on the basis of above thinking and it has been rewarding till now.