Addressable Debt market Rs 220-260 Lakh Crore during 2024-2030 across Infra (power, Roads , ports etc)- Beneficiaries mainly are REC, PFC, IREDA

investments required across infrastructure sectors in India (such as Power, Roads, Ports, etc.) totaling Rs 220-260 Lakh Crores between FY24 to FY30 as per the National Infrastructure Pipeline. Of this, the Renewable Energy investment is projected at ~Rs 30 Lakh Crore till 2030 unlocking an addressable debt market o

IREDA is seeing a stampede of trades since last week.

Is seeking FPO approval to raise Rs 4,000-5,000 crore.(long mentioned, not a news here though)

It raised Rs 1,500 crore via bonds, which saw oversubscribtion 2.65 times

It seems to me, In the last 6 months (3M,1M,weekly. on all timeframe), IREDA ran faster than PFC and REC. or did i miss something ?

So, what’s the deal here ? Has there been some major change speeding up IREDA? Is it the market’s typical irrational moves? Or is it just a Budget doparoll?

Wherever there is future earning visibility , investors are chasing those stocks…And IREDA is a Navratna PSU, so there would not be any corporate governance issues, Govt backed , no issue in fund raising , NPA’ s are good… For the investor , you get regular dividends.

The stock may continue to be in demand with a bout of ups and downs.

However, when compared with REC, PFC, Hudco , there is a wide valuation gap…

REC , PFC don’t carry Renewable energy Tag , but IREDA do carry the tag.

Given an option and if I have to add to my existing holdings , i would rather add to REC, PFC and Hudco rather than IREDA.

I am holding all the three from lower level with 9-10 % Dividend yield - IREDA i was allotted in IPO. Had Partly booked profit and later added back on decline

Discl: Invested. May be biased . please do your own assessment before investing. PSU stocks could be volatile at times due to change in govt policy

We are at the euphoria stage of the market. You and I have discussed this in out convos. Recent price action is completely out of whack with fundamentals.

What is the future, I am no guru to predict.

As regards to REC/ IREDA / PFC, look at loan growth and NPA to determine relative valuation for long term.

for eg: PFC has recently loaned the Shapoorji group some 15k crores for repaying old loans. Does it make sense. Is it part of their mandate.

Similarly, REC has started funding infra projects. Do they have clear understanding of the relative pitfalls. Infra projects in India are almost always delayed. Have they priced the risk.

I hold REC bought at current prices having but am doing so taking into account 15-20% dips and long term holding. If your outlook is shorter, maybe time is to take out profits.

With India’s plans to add about 85-90 GW of thermal power capacity by 2031-32, REC Limited, a major state-run non-banking financial company in the power sector, has declared its intention to fund 50 percent of the capital requirements of the thermal power capacities coming within the said timeline.

PSU Watch had earlier reported that India’s thermal power capacity addition plans for 2031-32 will entail an investment of Rs 6.67 lakh crore. Ajoy Choudhury, Director (Finance) at REC, said that out of the total investment of Rs 6.67 lakh crore, funding will be restricted to about Rs 4-4.5 lakh crore. “We are targeting roughly 50 percent of this funding opportunity that will happen over a period of time by 2031-32,” he said.

“The share of coal in our loan book is currently at 28-30 percent. And it is going to continue at that level until 2031-32 even as we tap into the funding opportunities presented by additional thermal power capacity addition. And that is because the share of renewables in our loan book will go up. Renewable Energy currently constitutes only about 7-8 percent of our loan book. And it is expected to go up to 30 percent by 2030.”

If they are increasing both coal funding and renewables, this should help them increase their loanbook and also get the ‘Renewables and ESG’ tag helping IREDA get the PE multiples.

At the same time, government’s LTCG and removal of indexation benefits will aid ita capital gains tax bond funding. Since they have to now compete with many large private banks as well for deposits, it will be an easy source of cheap funds.

How do you look into the PE multiples and valuation? Does it have a IREDA rerating potential? What are the triggers or weaknesses we need to look into for coal based funding.

Is this a risk for Power Financiers like PFC and REC?

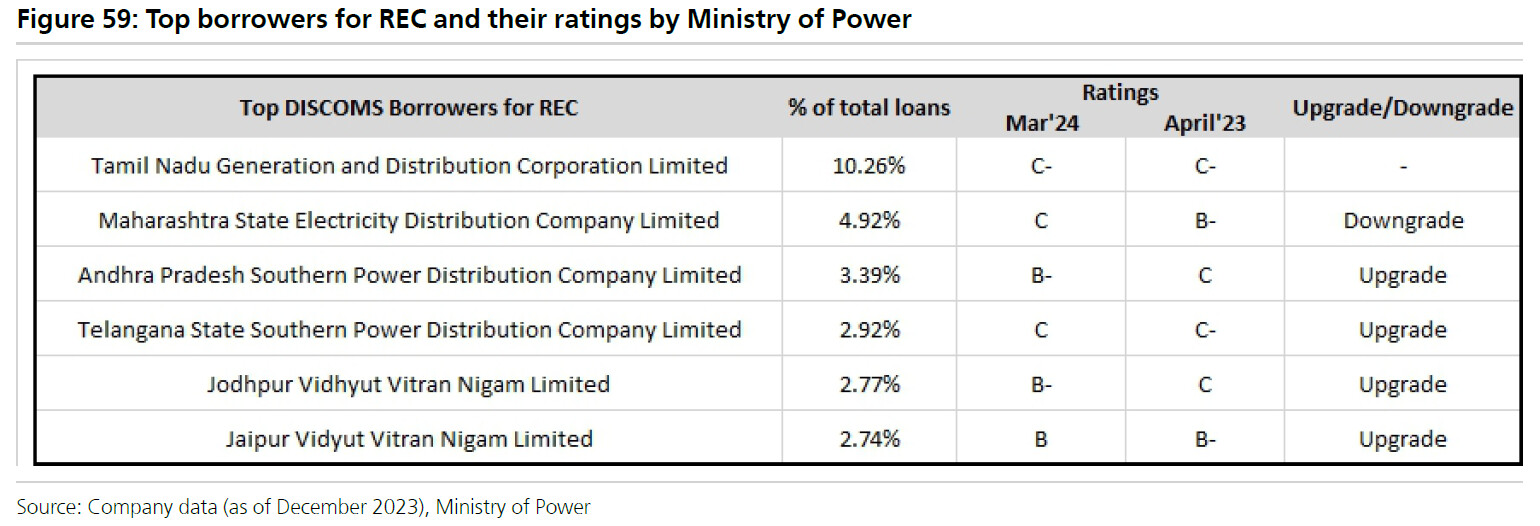

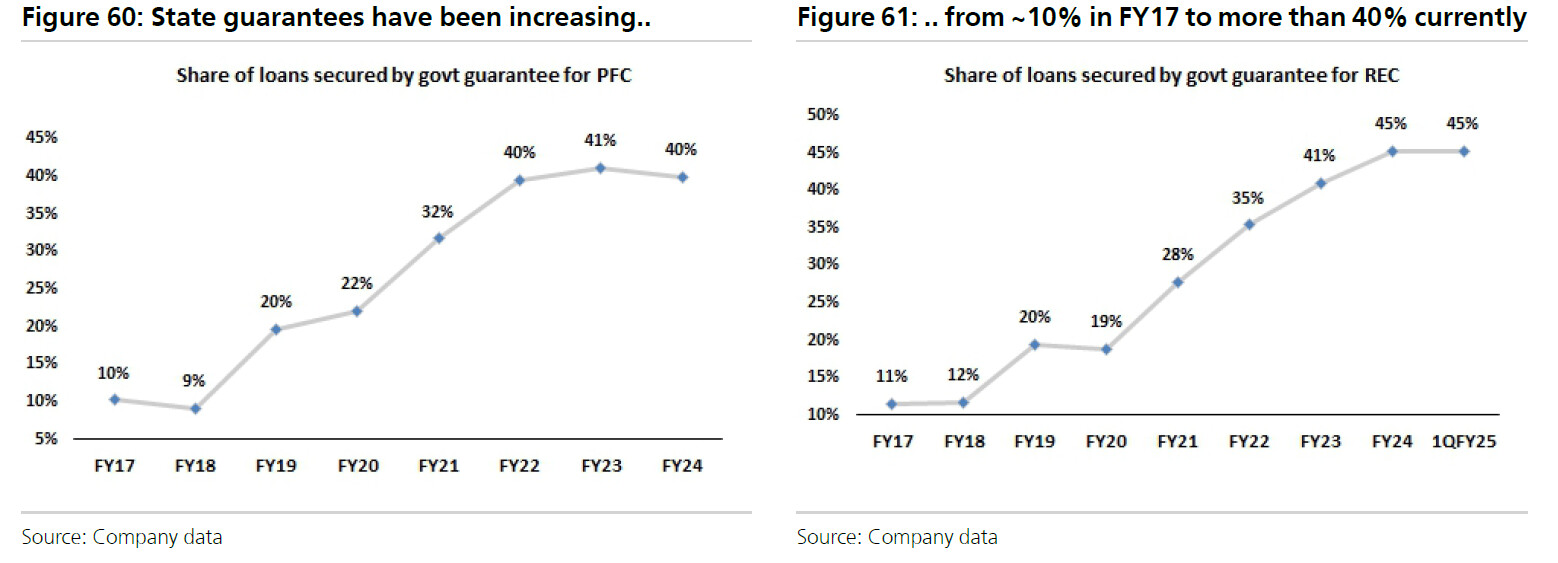

I understand that more and more loans are now guaranteed by state governments as

subsequent schemes by the centre has included conditions to provide cover for these

loans. But this is still just 45% currently.

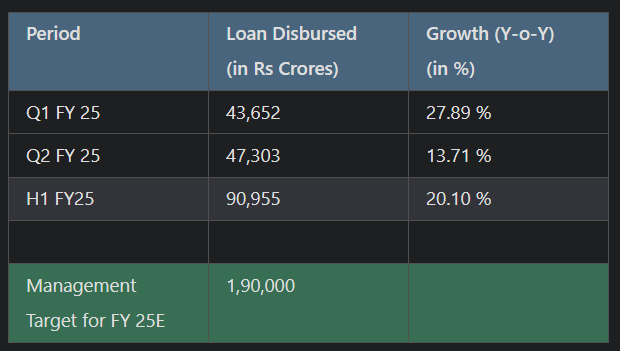

State-owned REC has disbursed loans worth Rs 90,955 crore during April-September FY25, up 20.10 per cent from the year-ago period. Of the total amount, Rs 11,297 crore was green loan, 92.68 per cent higher year-on-year, the company said in a statement.

In the September quarter of FY25, REC said it disbursed Rs 47,303 crore loans, 13.71 per cent higher than the Rs 41,598 crore disbursed a year earlier.

Dividend yield stock to earnings yield stock to growth stock - then npas come, restructurings happen then back to dividend yield stock—— Journey of stock shall be full of ups and downs- shall be interesting to see full journey of any stock —- REC’s journey has been interesting so far- lets see what lies ahead - googly from RBI reg provisioning and to b fair its good for REC in the long term…

Agreed. Since REC follows Ind-As, my understanding is that they would only be required to create a “reserve” in balance sheet and the added provisioning requirements will have no impact on P&L (as they follow ECL provisioning norms).

Further since their Capital adequecy ratio is high - the reserve (which will be excluded from CAD and tier 1 caluclations) - again would have no impact.

If anything banks may completely vacate the space leaving the entire market for REC/PFC.

Hitting the pnl or not is one aspect. As we have seen reckless project financing in the past by power psu nbfcs, it atleast lets share holders know more granular info about stage of execution of loan book which otherwise is not disclosed. And if the loan is good, whats the fear about provisons, they shall get reversed later if collections happen as per schedule. Ofcourse earnings may b lumpy . I am ok with that as the benefit of that being addl disclosures on project finance loans ( especially skeptical about loans to pvt ppl) .

REC Ltd Recent Updates: Major Financing Deals, Growth in Renewable Energy, and Nuclear Power Expansion

REC Signs Rs 3 Lakh Crore Financing Agreement with Rajasthan Government:

REC Limited has partnered with the Rajasthan government to provide Rs 3 lakh crore in financing over the next six years for power and non-power infrastructure projects. The company will contribute Rs 50,000 crore annually, a significant increase from the previous Rs 20,000 crore per year commitment, extending support until 2030.

H1 FY2024-25 Loan Disbursement Growth:

REC has disbursed a total of Rs 90,955 crore in loans during the first half (H1) of FY2024-25, reflecting a 20.10% year-on-year increase compared to the Rs 75,731 crore in the same period last year. Of this, renewable energy loans accounted for Rs 11,297 crore, a remarkable 92.68% increase over H1 FY2023-24. In Q2 FY2024-25 alone, REC disbursed Rs 47,303 crore, up 13.71% YoY, with Rs 5,946 crore allocated specifically to renewable energy projects.

PFC Secures $1.265 Billion Foreign Currency Loan:

REC’s sister company, Power Finance Corporation (PFC), closed a $1.265 billion foreign currency loan, the largest-ever by an Indian PSU. The loan will support assets outside of thermal power, promoting green energy transition and decarbonization efforts.

REC’s Growing Focus on Renewable and Nuclear Energy:

As global demand for electricity increases, REC is investing heavily in nuclear power as part of India’s broader shift towards clean energy. Though India’s nuclear power generation is still small, the push to increase capacity is gaining momentum. Nuclear energy, which provides clean, 24/7 power, has already saved 716 million tons of carbon emissions in India. REC’s focus on renewable energy loans and international transmission projects further highlights its role in supporting India’s transition to a 50% non-fossil fuel energy mix.

India’s Energy Transition and REC’s Role:

India is currently ranked fourth globally in installed renewable energy capacity, including large hydro, wind, and solar power. REC continues to support this transition through increased financing, expanding its role in nuclear and renewable energy to help reduce the nation’s carbon footprint.

These updates showcase REC’s key role in financing India’s green energy transition and its commitment to decarbonization, alongside notable growth in its loan disbursements, particularly in the renewable energy sector.

No absolutely agree on that Sunil.

The challenge is that as per revised norms RBI reuires 5% upfront provisioning - the the point of disbursement. That on a perfectly fine/healthy loan. See ECL model is based on “Expected credit loss” - so you make sufficient provision on the day any loan gets delayed or gets pushed into SMA 2. But the revised norms earlier suggested by RBI are beyond onerous.

The disclosures historically have been quite good as the management has always shared specific project details on NPAs etc. Also under no circumstances can a company keep classifiying a project as an NPA if it stops paying given all this is now much closely monitored by RBI.

To you earlier point reversal of provisions - these loans are of longer duration - 5/10Y - introducing such lumpiness creates a situation wherethese companies will start reporting EV/VNB like metrics in growth phase which doesnt make sense per my view.