No absolutely agree on that Sunil.

The challenge is that as per revised norms RBI reuires 5% upfront provisioning - the the point of disbursement. That on a perfectly fine/healthy loan. See ECL model is based on “Expected credit loss” - so you make sufficient provision on the day any loan gets delayed or gets pushed into SMA 2. But the revised norms earlier suggested by RBI are beyond onerous.

The disclosures historically have been quite good as the management has always shared specific project details on NPAs etc. Also under no circumstances can a company keep classifiying a project as an NPA if it stops paying given all this is now much closely monitored by RBI.

To you earlier point reversal of provisions - these loans are of longer duration - 5/10Y - introducing such lumpiness creates a situation wherethese companies will start reporting EV/VNB like metrics in growth phase which doesnt make sense per my view.

Anyways…It is in the hands of RBI and I am sure that industry players conveyed their views and sanity prevails…I am ok with any of the accounting related jugglery rules ( provision etc)as long as loan is recovered…In a way , I prefer lumpiness which gives opportunities to add the stock as most of the market players prefer certainty…RBI shall keep big stick first sothat industry players ask for small stick…If RBI itself keeps small stick , industry players shall ask for No Stick…These are things which are not under any of our control and the past clearly has reasonable amount of bad loans given to pvt players by these power psu nbfcs…I only hope they give fewer bad loans…

Again circling back to my post which was a bit unpopular at the time since stock had just made all time high start of May 2024, delivering handsome returns to their investors.

Since then stock is 13% down in 7 months despite all the euphoria, positive news flow and positive management commentary that we have seen in the same period.

Nothing really changed much in fundamentals except drying up of liquidity and valuation mean reversion. There was too much liquidity till 1st half of last year and everyone was justifying stretched valuations offering some positive narrative.

Now those who booked profit in the REC counter 6 months ago did the right thing. While those who got sucked into the counter at ATHs purely based on news flow and narrative will have to settled down with very modest return.

REC is in a space where customers are known for defaulting and there is inherent cyclicity to the business. RBI can only impose guidelines but they can’t run businesses of borrowers’ on their behalf. That business hasn’t changed in last several years. And that’s the reason this business has never got the multiples which other private lenders have been getting.

So stocks like REC may be good for short term trades, but they will never deliver long term compounding that we have seen from private lenders. Even a stock like HDFC bank with most pessimism has managed to keep its investors happy during current correction.

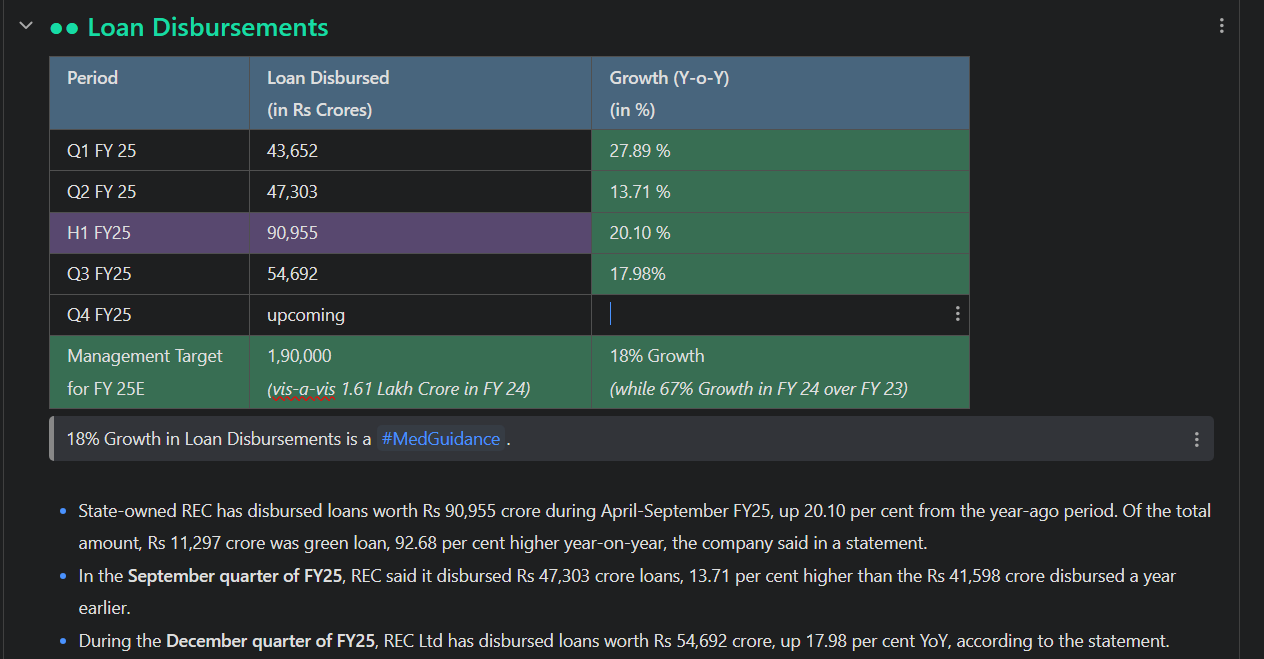

REC Q3 update-Loan disbursements up by 18%. Emkay Global on REC & PFC

Discl: Invested from lower level with 9-10% dividend yield. It is one of my long term bets. currently Sitting with 4X returns apart from 9-10% dividend yield.

I may be biased. Please do your own assessment before buying / selling

Renewable energy ( Solar , wind) loans carry comparatively less risk due to low gestation period of 6-12 months.

By the way , IREDA loan disbursement in q3 also increased by 41%.

So renewable energy is in focus and if this trend continues, most RE related stocks and ancillaries are well.poised for growth in future and there is less likelihood of trend reversal.

This is my view considering the thrust in renewable energy, though I may be wrong in my assessment.

Discl : Not a buy sell recommendation. i remain invested in renewables for the last 3 years and hence I may be biased. Please do your own assessment before investing.

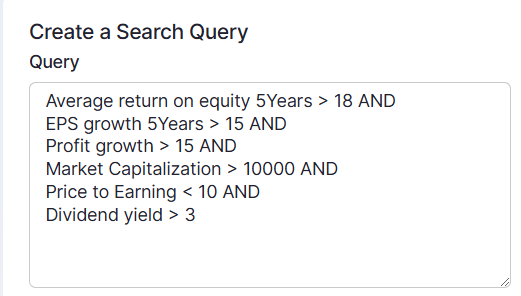

Amidst the brutal correction, the biased me (discl. invested) ran this screen with just one output on screener:

To be fair - growth expectations have come down and I am sure RoE in the years ahaed would settle at 17%-18% rather than the 20%+ numbers have seen in recent times