Company has reported two profitable quarters after 7 years of loses.

Is anyone aware what’s happening in the company?

Company has reported two profitable quarters after 7 years of loses.

Is anyone aware what’s happening in the company?

Latest Q result was mindblowing & hence continuous UCs with huge volume waiting to enter everyday

I read many negative comments about the promoter on this thread in past - like he didnt mention that 80-85% revenue was coming from Visa, dodging the questions on TV interview etc.

Is the bad time over for the company?

please share the view if anyone started tracking it recently

Disc : invested tracking Quantities.

How do you get to take the position in continuous uc after the great quarterly result. I also want to invest but not getting chance to enter due to uc.

I was going through the AR and linkedin posts and it seems their investments in product development has finally started to bear fruits specially in US markets.

If they are able to sustain Q3 results then a big rerating will happen in the company (just like what happened with NPST last year)

Payment/banking software/platform cos enjoy very high OPMs and trade at high valuation multiples

RS SOFT CEO interview

Have done 100crs investment in last 5-7 yrs for developing software/platform in entire payments valuechain. Looks like these investments have started to bear fruits now. Recent quarters already show turnaround happening!!!

I am not tracking the company now but i know during 2015-2017 the company made many tall claims and took the investors for a big ride. Raj Jain has a habit of promising big things. During those times, they used to say that they are working with NPCI and they are part of all the digital stakes India has build including UPI. However, the revenue never became visible and eventually the investors suffered. So we should not just judge them by 1-2 quarters of results.

Disc: Not invested.

I invested in RS Software way back in 2013. Made very good multibagger returns in this stock that time. This is a company which at that time did not disclose the name of its single biggest client. The share of this company grew more than 100 times and almost nobody still knew this company as it is a very secretive company.

After a gap of almost 6-7 years of negative returns, this company is finally turning out a new chapter in its life. It has invested 100-150 Crores of its own money in developing the backbone of new generation Indian payment system Unified Payment Interface (UPI). They have also produced Bharat Bill Payment System (BBPS) and various other popular softwares for Fraud Risk Management etc. Many other countries are now waking up to the huge payment revolution in India and they and their financial institutions want to copy this success in which RS Software can help them. These software implementation tenders can be in millions or billions which only the future can tell.

But one thing I have learnt from past times is that this company generally has a good performance window (fundamentally) of atleast 4-5 years, once it starts growing. If the company can just repeat its current quarter Consolidated EPS of Rs 3 in the coming quarters, then the yearly EPS in future can be easily Rs 12. I am not including extra Rs 2 per share of Depreciation being shown yearly in the P&L which if added will make the EPS Rs 14 as Depreciation is not actual cash going out of business.

If the company grows for the next 4-5 years as its products have finally started gaining traction, then sky is the limit and EPS could be Rs 40-Rs 100 in that long time frame. In good times a fast growing company could easily command a PE of anywhere close to 50 which can make this stock a Mega Multibagger like NPST (EPS*PE). Hence I am a long term investor in this company until and unless I get a serious red flag, on which I can easily sell my entire holding. Hoping for the best for this exciting fast growing company and multibagger returns for myself.

Disclosure: Invested in this company since almost one year for the very long term. Will sell in an instant in case of some serious red flag or the growth slowing. My calculations can be wrong. I am not a SEBI registered advisor. Please take anything I say with a pinch of salt. This is not a buy or sell recommendation. I have contract notes to prove my point.

Amit Goyal

The overall results seems to be pretty good, if viewed from the long term perspective. The best part about these March 2024 quarter results is that they prove that the results of the previous quarter December 2023 were not a one time fluke. The sales of March 2024 quarter are almost the same as the December 2023 quarter, but due to increased Employee benefits expense, the profits are a little less. The increased Employee benefits expense (Almost 60% increase) from December 2023 quarter is a huge positive sign for the upcoming quarters. Year on Year, the results are simply tremendous. When all of the Big IT companies across the world are firing their employees, this small IT company is hiring aggressively.

The opening of a branch office in Canada is a huge positive sign. The declaration of no dividend is somewhat negative. But the company is in an infant growth stage and it may be requiring cash for exploring new markets and clients. In a nutshell, the company has recovered from a period of 6-7 years of negative returns and degrowth to a higher orbit of growth with a very good chance of multi year growth ahead of it. It has a track record of becoming a 50 to 100 bagger, a couple of times earlier in its history.

So my personal thesis for investing in this stock is intact, that over a period of 4-5 years it EPS can grow to anywhere between 40-100 and in a bull market for a growing company, the rerated PE can reach anywhere between 50-100 (before this quarters result, the PE of this stock anyway reached approximately 63 on an TTM EPS of Rs 4.8 till December 2023). Even many other payment and fintech companies like NPST and Trust Fintech have PEs in excess of 100-120.

Hence I am still a long term investor in this company until and unless I get a serious red flag, on which I can easily sell my entire holding. Hoping for the best for this exciting fast growing company and mega multibagger returns for myself.

Disclosure: Invested in this company since one year for the very long term. I will sell in an instant in case of some serious red flags. My calculations can be wrong. I am not a SEBI registered advisor. Please take anything I say with a pinch of salt. This is not a buy or sell recommendation. I have contract notes to prove my point.

Amit Goyal

Did any one notice if they have plan for quarterly concall scheduled for Q4FY24? So far I have not noticed in any communication so wondering if I missed it?

I don’t think they have any plans of concall they haven’t done that in years.

Hope they do that, and give some insights.

Does any one have their revenue mix:

Country wise revenue break up in %.?

Questions for AGM on 10th July 2024

Hi Everyone

Example of another solid collaboration exercise.

Let’s try and get answers from RS Software Management in a structured way. Anyone who gets an Opportunity to ask questions at the AGM, please pick a few from here. Also looking forward to add more questions to this list. Request active Collaboration from all interested/tracking/invested.

[for the moment, let’s keep aside the past experiences and be open to asking the right questions ![]() ]

]

46% of global real time payments processed on platforms built exclusively by RS Software - is a claim made by RSSL in some of the official videos. Is this taking into account only UPI? What other platforms if any, are we referring to here.

The outsourced services for VISA’s card platform. Please help us understand the genesis of that seemingly very strong relationship. Apart from RS core competence validation, what were the contributing factors - How was respect for Visa’s IP validated by them for that kind of trust to be built up.

Why did RSSL win the initial UPI Tender? As many as 70 plus Vendors had probably responded for the RFI/RFP included global biggies in payments domain like FICO, FIS, ACI, Nice Actimise. What were the contributing factors for that win against what one could term as overwhelming odds?

Is it fair to say IntelliEdge EFRM is RSSL core strength, and the one single product that uniquely differentiates and benchmarks you as among the best in the world? Please take us through that journey right from the initial days with VISA on Risk and Fraud Management.

Apart from meeting high availability and scalability requirements, The UPI experience has obviously bolstered product IP. How much richer has Data Stream Analytics incrementally grown - from rules based predictive patterns learning base to AI and deep machine learning enabled detection of fraud on real time transaction basis. What did UPI experience add to the product/IP

Please talk about your Sales Process/Consultative Selling? Go-to-Market partnerships needed to Target customers at Large Banks/FIs and Fintechs in export markets like US, Canada, UK and Europe. Vendor registration must be a regulatory requirement of Central Banks also (just like RBI’s) so that they can intervene when needed or question sustainability of individual vendors. Do you have vendor registrations with small/large Banks and FIs in these markets already? When talks proceed to an advanced stage with customers, do they help expedite the registration process?

Or, the way forward is go-to-market partnerships with the right Partners in each country/region?

Please talk about a few of these partnerships in US, Canada, UK, Europe. Are these the Accentures of the world and/or more payments domain focused consulting firms. Why cant TCS, Infosys and other Indian IT majors - who probably already have all the required vendor registrations, be your natural go-to-market partners for Banks/FIs in every market?

UPI Tenders mandate the sharing the Source Code. How are they maintained securely.?

In the Initial years till the 2023 next version of UPI, RSSL owned the IP rights, while Data was owned always by NPCI. Now IP is co-shared with NPCI. What are the implications for this? Does it mean NPCI is free to choose to develop this further in-house and/or go with other vendors as they choose.

Current share of licensed product sale vs Solutions Sales is 60:40? Can you please elaborate more on the product licensing terms. How are these structured? Are there multi-year licenses or perennial? Has it become a mandatory requirement for Sales to any Central Bank/Central Infrastructure to a Country (like NPCI in India) for vendors to give away the source Code? Does the IP also need to be shared? What has been the experience so far.

Is it a correct inference that other than Central Bank/Central Infrastructure Sales - the Product License IP rights are always owned ONLY by RSSL? No shared IP Sales?

just for our understanding - Is it a fair argument that Revenue Share deals are primarily seen for products that are at the Edge/Overlays. Products at the Core of Central Infrastructure are unlikely to see such deals.

Recent PayAbbhi deals in the US are revenue sharing deals right? Please tell us more on how exciting that opportunity is for RSSL. An idea of what kind of scale up is possible (as more merchants are acquired on the platform) would be great to have. Why is 5x or 10x in a few years not possible?

Is it correct to say that the singular market driver for Real Time Payments (RTP) and the consequent payment modernisation acceleration seen in recent times - is the Customer Expectation/Demand. Kindly comment on this and if this is now an irreversible trend.

While UPI is hugely successful and traffic is already at 13 Bn transactions annually, the one argument often made about UPI success and huge scale up seen is that nobody is making money. There are no MDR charges, Maintenance/Enhancement of central Infra is limited, and capped. And at edge solutions/gateways/aggregators nobody is making any money. Is it now CLEAR that the user will never be charged. But in future it might move to a system where high value transactions for Merchants are charged a much smaller transaction charge compatred to current and/or some kind of capped service fee is attached - for sustainability reasons

At the same time evolving regulations are also hastening the process? SWIFT the de-facto money transfer network for cross-border payments is making it mandatory for all participant banks to adopt ISO20022 messaging compliance for cross-border payments by November 2025. Australia is in compliance already, US and UK efforts are on at FedNow, and BoE. Does it point to RS Software Central Infra and Banks/FI targeted products have a huge opportunity knocking at the door? 2024 AR is full of ISO20022 compliance reference for most product suites.

AR 2024 refers to TCH-RTP, FedNow, PayPal and Zelle integration ready products like DigitalEdge. These are Networks having their own set of participating banks. We have been talking of FedNow deployments. Is it fair to assume that wherever RSSL has gained a foot-in-the-door, multiple opportunities at participating banks are addressable for central payment rail connector, payment hub solutions as well as legacy-RTP overlay products/solutions. How strong is the Sales/Marketing effort therein? If at this point/size of RSS partnerships are the way to go, what kind of Team have we built for Partner engagement/focus.

Please help us put a dimension to this opportunity. We hear that all Big Banks have earmarked huge budgets for this transition. RBS or NatWest Group’s ISO20022 budget is 100 Mn Pounds. This will of course involve huge amounts of legacy connects/overlays but what portion of this budget say is RSSL Addressable Market here. Of the $340Bn (RSSL presentation) opportunity by 2027, how much is imminent by 2025, and RS addresable size?

We hear ISO20022 message structure makes 3 fields mandatory now for SWIFT cross border. Purpose, Structured Address (conforming to the country banks set fields), and Legal Entity Identifier (LEI). While there are many other fields that make for much richer payment data set, what are the main problems that are being addresed, and what are the opportunities for Banks and FIs that adopt ISO20022 even for domestic payments.

UPI Tender Scans (filtering out hardware/servers, computers et al) shows up a few companies like Montran (ACI company?) - mainly around NACH clearing ( total 42 Cr), Phi Commerce - RuPay Clearing and RuPay EFT switch, EMV 3D secure with IP ownership but source code to NPCI (total 21 Cr), FIS - AMC EFT switch (IRGS) Rupay domestic settlement (total 12 Cr); also IISC Prof hired for AI/ML. Of these RSSL clearly has the Clearing and Settlement Solution, why did RSSL not bid/get this piece too?

Can you please talk about RS Open Payment Modernisation Framework (RS OPMF) as described in 2024 AR? What does this Architecture Framework bring to the table additionally. Does this help RSSL differentiate its Product Offerings from say that of biggies like FICO, ACI, or FIS? Does it help accelerate Customer solution deployments, why and how?

(will try adding more later with inputs from more VP Collaborators)

I deeply respect and have high regards for Donald Ji and Valuepickr Forum. I also deeply respect Hitesh Ji, Ayush Ji, and many others. I soak in information and insights from Google, Youtube, and Twitter. Thanks to God’s grace and all of the above, I have experience of investing in mega multibaggers throughout my investment journey of 20 years. As a result, I achieved financial independence at the age of 32-33 many years back. But my main problem was investing less and booking profits early after 4-5 times return.

This is the first time when almost my 100% of portfolio is invested in high conviction RS Software in which I began investing afresh for the second time in April 2023 at very low prices and I have already earned around 10 times returns at my portfolio level. My very first investment in RS Software was in early December 2013 through which I completely booked and earned very handsome multibagger returns.

I have never talked to any company management in my investment journey till date as I don’t have too much time and also many managements lie openly. I don’t have great indepth knowledge of RS Software but just historical enough to earn good returns from it. I can think of a few pros and cons of the company.

Pros:-

After so many years of no action, the tone of the management in the Annual Reports has changed completely for the positive.

This company in the past has shown that once they turnaround, then for atleast for the next 3-5 years they have very good growth prospects.

They are not a fake company. They have done some real good work including developing UPI, BBPS, Fraud and Risk Management software etc. over the past many years.

They always have almost zero debt.

The promoter shareholding is less but it is not pledged.

They have invested almost Rs 100-200 crores of their own money in developing their Payment software products. That’s why their Net Worth is so small.

They have almost 170 crores of accumulated losses remaining even after adjusting for last year profits, which can be used to reduce tax on the profits of coming years.

They will keep charging Depreciation for the next few years, which in fact gives us more real profits than the cash profits stated in the P&L.

I so much wish that Fintech continues to remain one of the hottest sectors to invest in the coming years. Some of the companies like NPST and Trust Fintech are trading at much higher valuations.

Cons:-

Previously in 2015, the company didn’t disclose promptly the bad news of their main customer pulling the plug on them. This resulted in many investors suffering losses in their investments.

When the times are bad, the shares of this company can destroy value in no time and with great speed. The management goes completely silent. They will give no extra information and there will be no concalls, investor meetings, or anything else.

Disclosure: Invested in this company since more than one year for the very long term. I will sell in an instant in case of some serious red flag or the growth slowing for 3-4 quarters. I am not a SEBI registered advisor. Please take anything I say with a pinch of salt. This is not a buy or sell recommendation. I have contract notes to prove my point.

Amit Goyal

Revenue Contribution from USA:

June-24: 1482

June-23: 117

Agm seemed to be a total washout…

Mgmt did’nt discuss/answer much to most of the relevant business related questions raised by investors.

Most of the query’s answer were deferred to some concall which they might conduct in next few weeks due to “Paucity of time”

Asked investors with significant holdings to visit them in person.

Orderbook currently stands at 60% higher than Fy2024 numbers.

I doubt they have a clear roadmap towards monetization of their product portfolio.

Requesting senior VPer’s to comment if they get a chance to visit them in person.

Asked investors with significant holding???

What does that mean?

Are they ignoring retail?

I remember VIP industries doing the same in the past. The management barred the retail in attending and asking questions.

Someone do clear me if i am wrong.

Orderbook currently stands at 60% higher than F2024 numbers. Does this mean that they should do revenue of around +90 crore in FY25?

In a bid to bring everyone on the same page quickly, Let’s try and demystify the RS Software investing puzzle before us

[Disclaimer: This is half-baked work-in-progress - discussions on with payments domain experts; ]

Undeniable technology platform/architecting/product strengths: UPI Platform is handling monthly transaction volumes of 12Bn+; June 2024 volume was 13 Bn up from June 2017 volume levels of 10Mn 0r about 1300x in 7 years. Especially noteworthy is EFRM (Fraud & Risk Management) product (RSSL owned IP till last year; co-shared with NPCI from 2023) scaling up in tandem to support that volume of transactions with high availability, without degrading customer experience, with transactions getting completed within 5-6 seconds. No other Real Time Payment (RTP) infrastructure is anywhere near these transaction volumes - or has seen that kind of scaling up and therefore cannot claim that kind of high availability, high performance having been delivered.

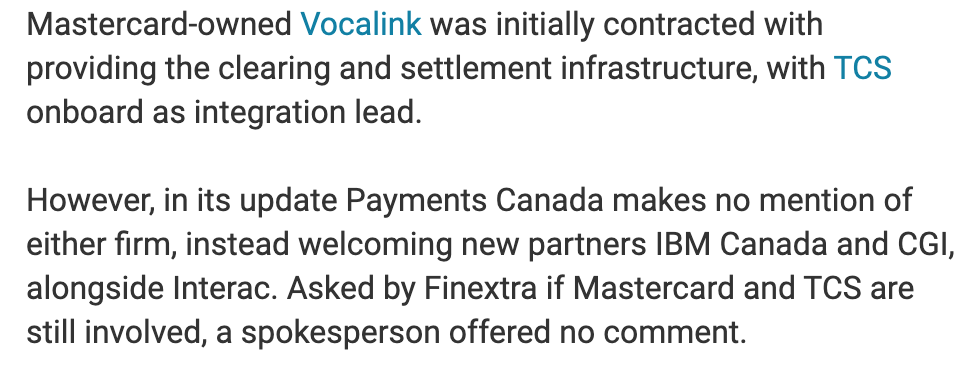

High foot-in-the-door Convincing/Success rate: RSSL was and still is a very small company when it won the UPI Tender in 2015 competing against ~70 other competitors - many were much bigger, well-entrenched payment companies like FICO, FIS, Fiserv and others like Volante, Vocalink. Yes, they were probably helped by some like FICO who refused to share the source code (mandatory for our sovereign payment infrastructure) and withdrew, but most others stayed in contention. Which means only one thing, RSSL could demonstrate RTP technology, process, and architectural superiority over other contenders. They won again the design and architecture contract for Payments Canada Real Time Rail (RTR) project. Implementation was through Interac - but launch has been delayed several times, now pushed to 2026! Ostensibly the Clearing & Settlement module is the latest cause of delays. Clearing & Settlement Vendor selected by Payments Canada in 2020 was VocaLink (a MasterCard company)

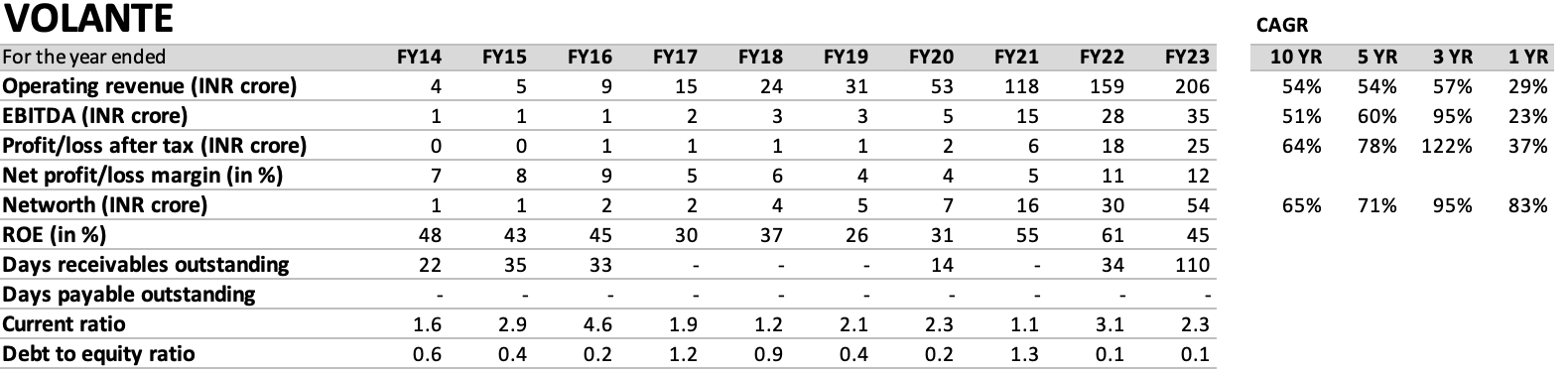

Unable to Leverage/Build on early success: On the other hand, RSSL hasn’t been able to leverage these early successes and scale up on the revenue front (annually still somewhere at 60-80 Cr), although profitability is back with a bang and operating margins at all time highs of 36% in latest Qr). Surprisingly some other small businesses like Volante (in almost similar payments modernisation space) has scaled up 10x in revenues and profitability since 2018 (FY23 Revenues 206 Cr, EBITDA 35 Cr).

Investments by Networks/Large Banks/Fis in RTP Vendors: MasterCard invested in VocaLink in 2016. Other Investors in VocaLink are HSBC Holdings, NatWest Group (earlier RBS group), The Co-operative Bank. Visa has invested in Volante, so has Citi Ventures, and other FIs like Sixth Street

Small Vendor Success/Scale-up Strategy: The “easy” game in town looks to be to get investments in from leading payment networks like MasterCard or Visa, and other large Banks like Citi, Wells Fargo and the like. So your investors are also your customers. and it works fine bothways - why?

Hedge against big payment vendors: [being verified from other sources] from a source working with a large UK Bank, the banks modernisation roadmap is often hostage to entrenched big vendors like FIS and their rigid product roadmaps. A good mitigation strategy thus is to get smaller vendors in like VocaLink, Volante, and others; also investments in them ensures (the vendor remains financially robust/stable.

Why couldn’t RSSL play the same easy game: One possible reason some experts point to is that 90% of RS business was derived from Visa, and logically Visa should/could have invested in RSSL at some point of the relationship (17 years) journey. However Valuations would have been a moot (sore) point - as Visa was also the main source of Revenues! Probably in its latest independent (Product-License) vendor pivot RSSL could explore the same - IF they are so inclined.

RSSL Success Planks: Central Market Infrastructure, Acceptance product, and EFRM are the 3 planks of RS success roadmap/push in the next 2-3 years. While the first 2 product/solution lines - there are several entrenched competitors in RS primary target markets of US, Canada, UK, Europe (both big and small vendors), it’s a good educated guess that they have a very decent differentiator in RS IntelliEdge (EFRM) deployed at a scale that none of the big vendors can lay claim to. Even a single product IP License sale for EFRM RS IntelliEdge to a leading Bank could probably take RSSL to a different league (?)

Win some/Lose Some/Come Full Circle (?): There is some talk of many vendors like VocaLink and Volante facing implementation issues/delays leading to even change of vendors. Case in point VocalLink substituted by Payments Canada.

[Inviting VP members experienced in payments domain/connected with domain experts to raise their hand and help take the discussion/examination forward. Feel free to DM me or other VP Collaborators. We need help on establishing the competitive landscape/positioning with clarity]

Disclosure: very small investment in family account

Here are Volante’s financial statements from the last decade. The company has shown a consistently high CAGR; quality growth it has been.

Volante Financials v1.xlsx (13.7 KB)

Can RS Software deliver similar return ratios and growth if (big IF) and when the co starts firing on multiple product lines?