8 Likes

@Anant buys 130000 shares of RS today. Would be interesting to hear his views on this business.

15 Likes

So I read that due to the de-boarding of Visa as a customer (which accounted for 90% of revenues) their revenues declined. But my question is the constant 60Cr revenue which they made since FY’17 what is the source of that as UPI contributed very less so which clients/verticals accounted for these revenues?

1 Like

Based on the annual report they have only stated following, I have not found any other information

Annual report 2017

Diversified revenue sources Added 20+ US Clients in the last 12 months Added new geographies – India and Asia

But from 2019 onwards started to share geographic revenue which give India vs rest of the geography.

Indian work it is not just NPCI they provide solution to Banks and FI’s even with this still in 2019 it was much smaller compared to US business revenue.

3 Likes

This is the first software company I have seen which does not mention Chief Technology Officer on its website. seriously? Do they even have this role?

2 Likes

So I recently researched about RS Software and the question that pops in my mind is that how do you predict the revenue visibility for a company like this? I mean yes they’re adding clients and have built various in-house platforms. But how do I get that little bit of conviction/visibility that they can scale up from here. Would love to hear inputs.

3 Likes

To take the RS Software quest forward, let’s focus on their RS IntelliEdge™ EFRM product. (IP License sale to NPCI in last tender; going forward IP is now shared with NPCI). Probably THE product which can change the trajectory/fortunes of the company - whenever a license sale happens next globally.

Sharing what we have understood so far - from discussions with some industry veterans and domain experts. [purpose is to get this base level understanding validated/more refined through domain experts]

-

RS IntelliEdge™ includes a combination of the Rule Engine and AI/ML Models and addresses the requirement to manage fraud and risk for RTP transactions and multiple other rails. The AI/ML models are already developed as part of the product, and work with the concerned data to get trained and effectively manage fraud and risk. The product is market validated for large volumes of data across multiple rails (~ 13 Bn monthly transactions on UPI alone) and is probably ready to be deployed in any country where it would work with the local data for that country.

-

Leading global Competitors in EFRM space are Feedzai, Featurespace, NICE Actimize and FICO are leading global competitors in the FRM space. Other companies in the space are LexisNexis, FIS, Fiserv, Jumio, GB Group. Refer Top companies in Anti-Money Laundering (AML) Market

-

RS AI/ML models are trained on UPI data, but the data belongs to NPCI. So, when it deploys EFRM next anywhere globally, there will the need to train on the data of the customer. Domain Experts tell us that it is true that there are lots of commonality in fraud patterns globally, and therefore the potential to reuse the solutions and the models is fairly high, but customisation to local environment is just as important.

-

Timeframe for induction of a Risk and Fraud Management Platform on any RTP Central Infra (like NPCI) is like 3-4 years post gaining momentum, judging from our UPI experience (introduced 3.5years from launch). RTP/Faster payment systems are recent deployments in developed markets, yet to gain momentum (?) so expectations of Central Infra sales in US, UK, Canada would be down the line. Since RS designed Canada’s instant payment central infrastructure, RS IntelliEdge™, could be a good fit for it.

-

Visa/Mastercard on the other hand, have their own FRM solutions at the central level on their card networks.

-

Meanwhile Banks/FIs will need EFRM for faster payments like UPI as they can additionally leverage customer profile (NOT available to Central Infra). Banks in India have reportedly started looking for such solutions. However Banks/FI priority (and recognition of strategic importance) for EFRM is lower down the order say, as compared to ISO 20022 messaging compliance requirements (?).

Domain Experts are also of the opinion the next disruption window in payments modernisation space will be brought in by any player with elements of AI

21 Likes

While we FOCUS on understanding and tracking the EFRM space better, here are other questions that we can seek answers to:

-

Vendor Registrations at Banks/FIs/FedNow/BoE: Any large BFSI opportunity seeks financial stability of the vendor as there is regulatory oversight and product/service requires support for many years. Has Financial criteria eligibility been an actual hindrance till now for RS? For contracts beyond a certain size, other than P&L, are there accumulated reserves/net worth norms too - basically graded eligibility norms, basis the size of contracts?

-

Partnerships might be a good way to move things forward till RS achieves/exceeds the desired norms. What is the focus within RSSL on this strategic objective. Is there a dedicated Team being set up for this? Strength and Budgets?

-

Collaborated with any of the large Indian Tech providers like TCS, Infy? CBS players like Infosys, TCS, CoForge, Intellect all claim to have some or the other insta payments solution, also say they are ISO20022 ready - are they natural Partners for RS, or are actually Competitors?

-

What percentage of revenues is RS looks to spend on sales and marketing in next few years?

(For example, Newgen spends 25% of revenue on sales and marketing. Intellect Design Arena (IDA) spends 130 Cr on sales and marketing on revenues of 2500 Cr - around 5%). Current headcount in Sales and Marketing? -

Senior level ex-employees of target financial institutions are often onboarded by BFSI vendors - like say what Intellect Design has followed, which has opened significant doors for them. RS strategy on similar hirings?

-

RS had two wins for its Acceptance platform in North America. Both of these have been product licence sales in partnership with TSG. Are these deals an Annuity kind of business? How is a deal size arrived at? What is the revenue cycle in terms of licence sale/deployment expenses/AMC etc.? Is deal size a function of bank size?

-

Current understanding is that ISO 20022 standard compliance for SWIFT cross-border payments is necessary by 2025. Is that understanding correct? Also every country might have their own internal guidelines/timelines for domestic ISO 20022 compliance but for cross border payments the mandatory fields like Purpose, structured origin/destination address, and LEI (Legal Entity Identifier) have a definite timeline to comply with? Despite being THE Opportunity in payments modernisation space globally for next 2 years and also highlighted strongly by RS in 2024 Annual Report multiple times - why NOT a focus area?

-

FedNow and the related ecosystem seems like such a large opportunity. Apart from TCH (which is mentioned by RS) what is the participation in FedNow, and any other RTP Infra opportunities? Will RS be working on FedNow Technology Service Provider registration?

-

FedNow seems to have lower MDR rates than MasterCard/Visa etc. and it motivates merchants to develop payments over FedNow. This opens a large opportunity with merchants with a sales process not as difficult as large banks. How is RS pursuing these opportunities more vigorously?

-

Why has RS not focused on the BBPS Switch market in India - given that retail users are used to paying charges (1-2%) for making bill payments? Given RS reputation, it should have a decent opportunity to crack some revenue sharing deals in this space. What are the issues which are hindering in capturing these opportunities?

-

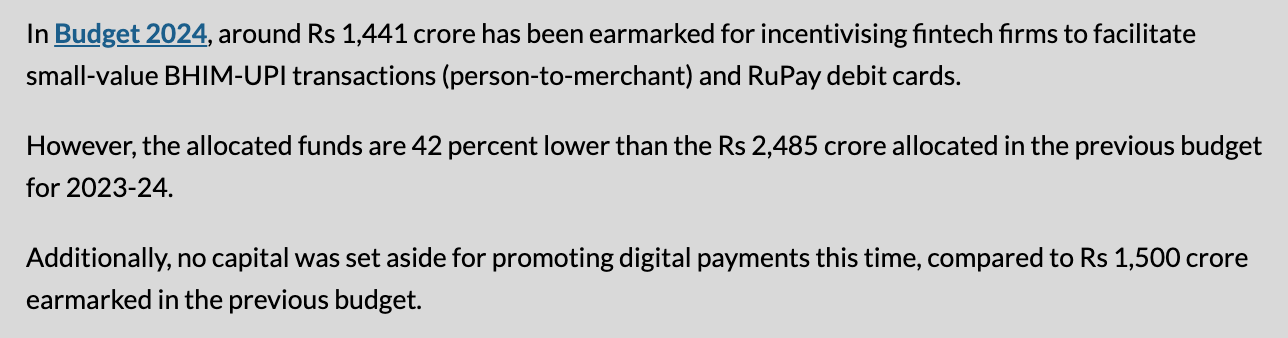

GoI Budgetary support for UPI incentives and promotion of digital data in 2021 was at 1300Cr, went up to 3500Cr in 2023 before going down progressively to 1441 Cr currently. P2M per transaction support has come down from Rs. 0.97 in 2021 to Rs 0.15 in 2023 looks like. Is this data roughly right? How does this impact the revenue models/viability of vendors that were getting a share of these budgetary support back from the Banks.

-

RS has often talked about/presented on the $800 Bn global opportunity in payments modernisation by 2027/2028, but given RS set of unique challenges/circumstances how does it define the size of the REAL addressable market, and what are RS ambitions for a reasonable market share in that in 3-5 years?

22 Likes

4 Likes

I found the below post about an investor having met RS Software management recently. Posting this since it is extremely difficult to get any information about RS Software. Please note that I am posting this “as is”. I do not know the poster nor have I ever followed him. I do not know if the information provided is authentic and correct.

6 Likes

linkedin page of rs software shows that over 1200 financial institution trust RS INTELLIEDGE for real time fraud prevention. Their quarterly rev is 18cr for all products and services. just want to understand their revenue model.It may be that these institution trust this product but not became their client yet or products are itself very cheap{widely available} and not a specialised one.

Any input is appreciated. INVESTED.

1 Like

At this current point in time, how exactly do we evaluate if RS Software will be able to deliver consistently good results w/o any updates or information from the company’s end? Anybody currently tracking/evaluating, what kind of info are we using here to judge if RS would be a good investment considering its current valuations (as it dropped in recent few months).

What I feel is that the US markets are currently in transition so if execution is good all will be good

2 Likes

The only positive thing I can gauge is the increase in FII holdings. They probably know something which we don’t ?

1 Like