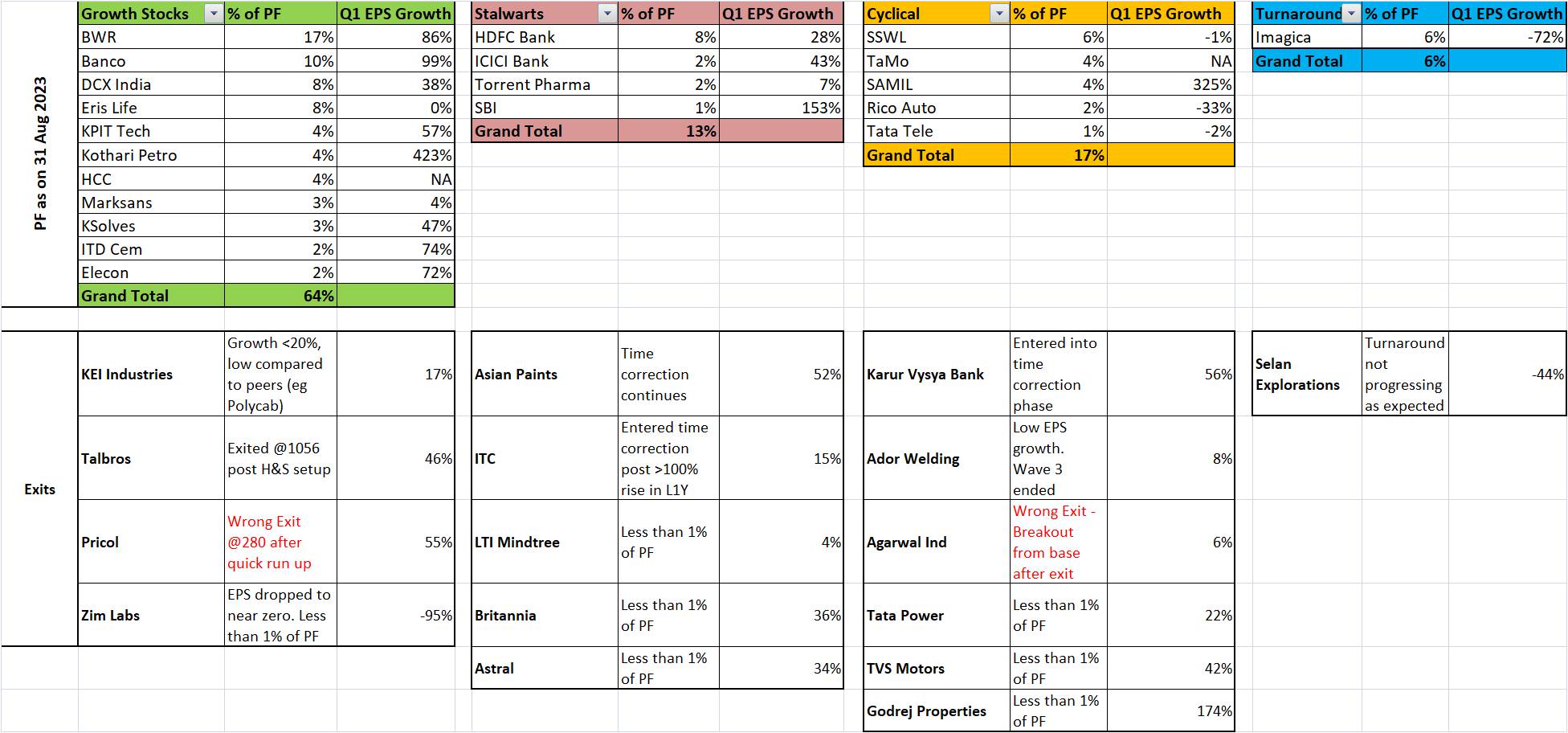

Consolidation of PF progressing well with the number of stocks now down to 21 compared to 29 in Jul end & 38 in June. Top 10 stocks have 74% of PF value at current market price.

Growth Stocks now account for 64% of PF, which is deliberate to ride the current bull run in Midcaps & Smallcaps.

I did not see any differentiation in the offerings of BigBloc, since the same product is available across all states at (probably) cheaper rates. Its logistics will be similar to that of Cement (local production required, since transportation will be costly), and hence a big constraint on regional expansion and growth.

The stock has however grown +80% from my level, thanks to improvement in Revenue Growth & EPS in last two quarters and the roaring bull market.

Note: This is an update after 3 quarters, hence there have been many changes in the PF.

Stocks in PF

Sector

Classification

Rationale

Saliency (at CMP)

Lloyds Engineeri

Heavy Industrial Machinery

Cyclical turned Growth

High Growth (Rev & EPS)

10%

Action Const.Eq.

Construction Equipment

Cyclical turned Growth

High Growth (Rev & EPS)

10%

Inox Wind

Wind Turbine EPC

Turnaround

Debt Reduction, Margin improvement expected

9%

ITD Cementation

Infra EPC

Cyclical turned Growth

High Growth (Rev & EPS)

9%

Inox India

Industrial gases, LNG, Green Hydrogen

Growth

Green Hydrogen theme

8%

Vertoz Advertis.

AdTech

Growth

High Growth (Rev & EPS)

8%

Anant Raj

Real Estate & Data Centre

Cyclical turned Growth

High Growth (Rev & EPS)

8%

Bharat Electronics

Defence

Stalwart turned Growth

Defence Theme with high growth

7%

Azad Engineering

Aerospace components and turbines

Growth

Defence Theme with high growth

6%

Nuvama Wealth

Wealth Mgt

Growth

High Growth (Rev & EPS)

5%

NPST

Digital Payment

Growth

High Growth (Rev & EPS)

5%

IREDA

Green Finance NBFC

Stalwart

Renewables Theme

5%

Emami

FMCG

Stalwart

Rural Consumption Revival expected

5%

Tata Motors

Automobile (PV, CV)

Cyclical

Legacy holding, High Growth

3%

Cash

2%

PF Concentration: 14 stocks at present, with highest allocation being 10% and top 10 accounting for 80% of PF. So, a healthy concentration and spread.

PF Construct: Majority of the stocks have been chosen for Growth (in Revenue & EPS), since the current bull market has given outsized returns to growth/momentum way for investing. There is one stock chosen for Turnaround and one as a Stalwart, though the boundaries between the four classification are blurred in a trending market. Many of the stocks in the PF were bought at lower/higher levels.

Disclaimer: My posts are not recommendations to Buy, Hold or Sell. DYOR. Changes is PF can happen without being mentioned here.

Business Segments: Footwear continues to drag the business in terms of revenue and margins. However, MUL is trying to focus more on the profitable segments: Auto OEMs (Domestic & Exports) for growth & profitability. (source: May 2024 concall transcript)

Revenue: Qtrly revenue breached 200 Cr mark for the first time in Mar-24 (as per screener). Management guidance for growth is 20% to 25% for Auto OEM Export and 10% to 15% is for Domestic.

Margins: Margins continue to be near 20%, and management does not expect it to go back to 25% to 27% level which was achieved around 2016-1018. (source: May 2024 concall transcript)

Stock has broken out of long consolidation with high volume and this new-found momentum is expected to continue if the subsequent quarter performance supports the move.

Disclaimer: I have no position in this stock. My posts are for my own learning purpose and are not recommendations to Buy, Hold or Sell. DYOR.