Dear VP members, I have been a silent learner of this forum since early 2015 and have benefited from the knowledge & wisdom shared by its esteemed members. I have experience working in Renewable Energy, Electric Vehicles, Automotive, Pharma, FMCG and Food & Beverages industries. I believe these to be the investing domains where I can further build my knowledge apart from new exciting ones (such as Defense, eCommerce, IT/ITES).

Objective of this Thread: I have followed multiple investing strategies since I first started investing in 2010 and have received decent above market returns. But, I have ended up with a zoo-full of stocks of all hues and colors. I am in the process of rebalancing to a concentrated portfolio and will post my rationale for selection/entry/exits for feedback/comments from fellow members.

Investing Strategy: In the past, I have been investing in large cap blue chips (Tata Motors, ITC, Dr Reddy’s, ICICI Bank, Asian Paints, etc), midcap compounders (PI Industries, CDSL, etc) and few risky bets which are now out of the portfolio. My portfolio churn has been very low, even in times of euphoria or doom & gloom. While this is good for long term investing, but it also means that I have lost in cyclical plays (such as Motherson Sumi, where I have been through peaks of 2018, 2021 and troughs of 2019 & 2022 without any gains). For my RR-2030 portfolio, I aim to follow fundamental analysis for selection of stocks and technical charts for entry & exits, and I do not claim to be adept in either.

Portfolio Returns Expectations: I have averaged between 10%-12% CAGR while following a mix of investing strategies highlighted above. Now, I am in a position to take a more aggressive approach and hence I am targeting 26% CAGR returns for the next 7 years with an aim to quadruple it by then. I have factored in one recession and one bull run in the Indian market while arriving at this target return rate.

To design my 2030 portfolio, I have taken inspiration from the “Peter Lynch Playbook” shared by Mayur Jain (you can google it) to ‘pick right players for the right position in my sports team’.

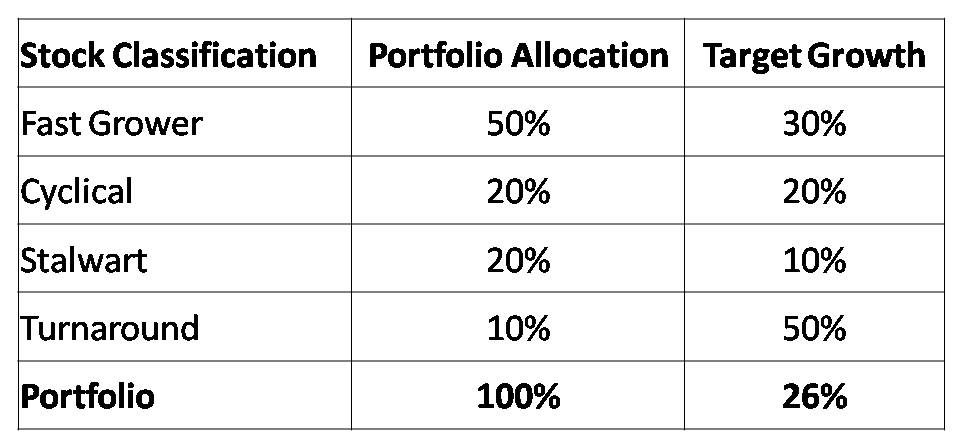

I have chosen a mix of Fast Growers (Growth Stocks), Cyclicals, Stalwarts and Turnaround to achieve the target return of 26% CAGR.

Many a times, one stock can fall in more than one of the above classifications (eg Fast Grower can be a Cyclical, or a Stalwart can be a Turnaround candidate) and hence the above guideline is a framework to guide capital allocation decision rather than being prescriptive. It also avoids two categories of stocks: Slow Growers & Asset Plays for obvious reasons.

My notes on these classes of stocks:

A) Fast Growers:

Minimum Revenue and Earning Growth at 20%-25%

Big companies have small moves, small companies have big moves

Moderately Fast Growers (20%-25%) in slow growth industries are ideal if they operate in a niche, since they can capture market share without price erosion

Hunt for ‘great companies in lousy industries’, rather than ‘hot stocks in hot industries’

Identify Fast Grower early (Startup Phase), but get on in next phase (Rapid Expansion), ride till Maturity/Saturation and sell before it hits the Slow Growth phase. This is akin the 4 Stages defined & popularized by Stan Weinstein & Mark Minervini.

Earnings growth is the only growth that really counts - keep checking and asking yourself “what will keep the earnings going?”

Inability to maintain double digit growth may see a re-classification into Slow Grower, Cyclical or Stalwart. High fliers of one decade are groundhogs of the next.

Every Fast Grower turns into a Slow Grower, fooling many people. People have a tendency to think that things won’t change, but eventually they do.

20%-25% is more sustainable than 30%

Emerging growth stocks are more volatile than Stalwarts, like ‘riding a tiger’ (a phrase mentioned multiple times in this forum by @hitesh2710 ). Have the guts to face -10% markdown and still hold on to your conviction

Expect high PE ratio for Fast Growers, as long as the Earnings growth keeps pace with Price growth. Refer to Chapter-4 (Value comes at a Price) of ‘Trade Like a Stock Market Wizard’ by MM (Mark Minervini), when in doubt.

20% growth @20PE is better than 10% growth @10PE

If you sell at 2X, you won’t get 10X - be greedy as long as Earnings keep growing

Consider selling (& rotate proceeds into another fast grower) when: Earnings start slowing down, stratospheric rise (>50% in one month) without any change in earnings growth, end of Stage-2 as per technicals, wide covage in media or PEG starts to increase beyond 1.5-2.0

(B) Cyclicals:

Identify, acknowledge & accept Cyclicals as they are: their revenue, profits and stock price rise and fall in/out-of-syn with the economic cycle (a-la interest rates).

Detect early signs of business change (eg: inventory buildup) to detect an up-cycle/down-cycle

Prefer High OPM (proxy for low-cost producer), since it will bode well in times of grief (down-cycle)

Best time to enter is when economy is at its weakest, low earnings, dividends are being cut , doom-gloom scenario

It is perilous to invest without working knowledge of the industry and its rhythms.

Timing the cycle is only half the battle. Other half is picking the companies that will gain most from an up-cycle. Choose companies with ‘Staying Power’ (strong B/S, low D/E, high Interest Coverage Ratio, etc)

Cyclicals have inverse PE cycle: low PE at the top of cycle and high PE at the bottom of cycle

Don’t hold on to Cyclicals thinking it is a Stalwart of Fast Grower. eg: Motherson Sumi (SAMIL) has seen 2 cycles since 2016 and I have been through them without making time-adjusted returns. Similar is the story for Tata Motors and those who are cheering that it is nearing its ATH of 600, may as well note that being a Large Cap cyclical, it will cycle-down as it has thrice in the last 2 decades. Disclaimer: both are great companies and are part of my current portfolio from multiple price levels and are cited as examples only, its not a recommendation to buy, hold or sell DYOR.

Growth is decent (2X of GDP growth), but not very high (like Fast Growers)

Long history of consistent business, have built their name (brand) in the market. Mostly found in consumer facing industries and have a deep Moat

Provides a cushion in hard times - do not fall as steeply as others & do not go bankrupt

Don’t hold on after it’s 2X, hoping for 10X (except when you bought in times of rare distress for the Stalwart)

If you can find a company that can raise prices without losing customer, you’ve found a terrific investment

Be wary of ‘de-worsification’ as capital allocation is the toughest for a cash-rich B/S

‘There are many possible reasons to sell a stock, but only one reason to buy’ - insiders know something you don’t know - keep a track

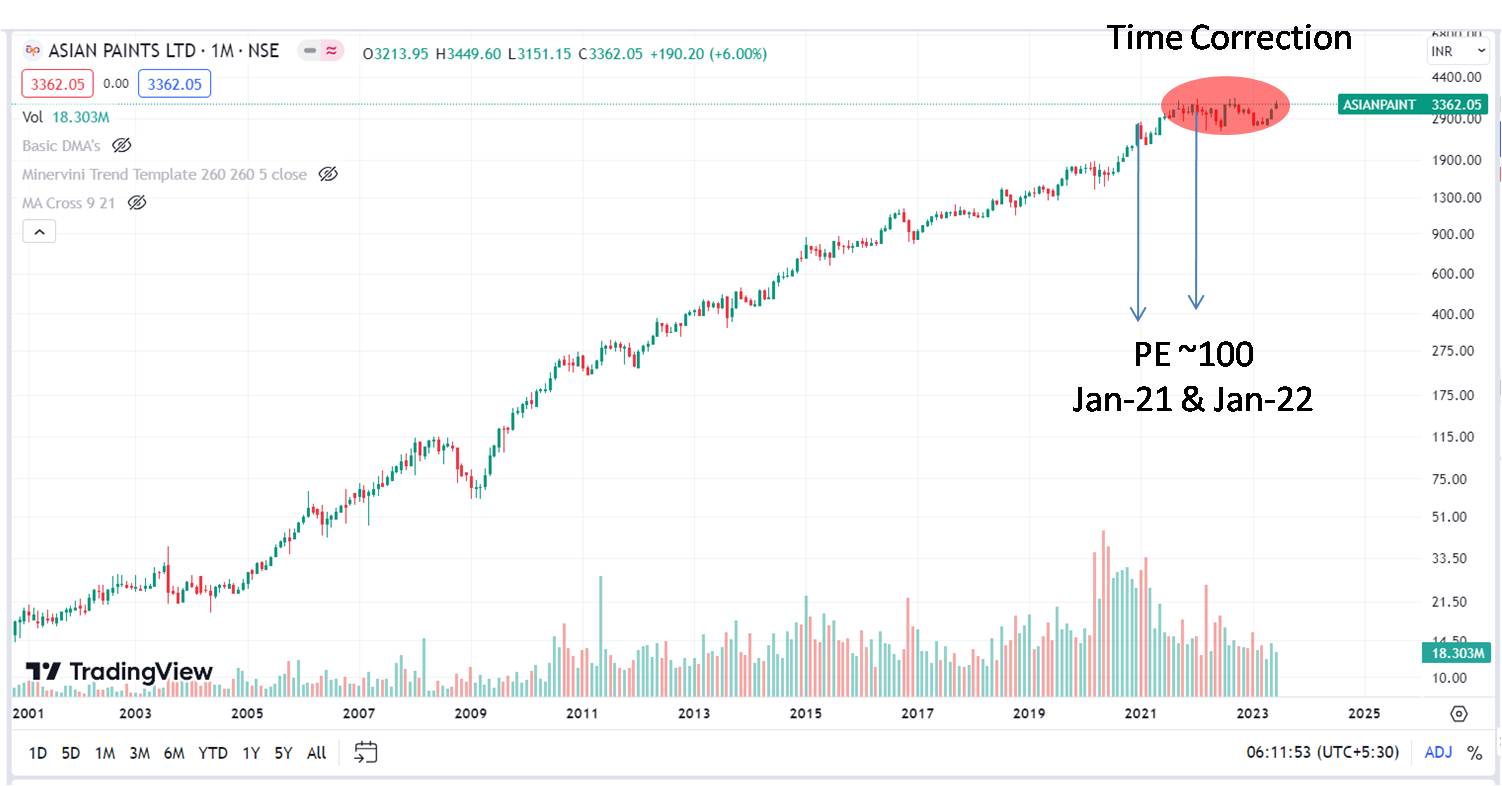

Sell when PE gets heated compared to nearest competitor or industry. These are signs of ‘rest’ (time correction) or decline (price correction). eg Asian Paints in Jan-21 & Jan-22 had ~100 PE and was ripe for correction through price or time.

Distressed due to one of the reasons: waiting for Govt bailout (eg. Voda-Idea), sudden policy change (eg: IEX), restructuring candidate, years of poor management leading to takeover by superior management (eg Eveready), High Debt, etc

Cyclicals with poor B/S may fall into Turnarounds

Survivorship Bias rules here: failed turnarounds are nowhere to be found since they are long dead

Improvement in business can lead to quick upswing, key is to track the business metrics.

Buy when first good news has arrived (in terms of growth, margin improvement, restructuring, management change, reduction in Debt, etc)

Never rush to buy a distressed company thinking it can’t go lower, it can go lower than you can imagine (eg Yes Bank)

Sell when the turnaround story is well known, Debt is reduced, rich PE

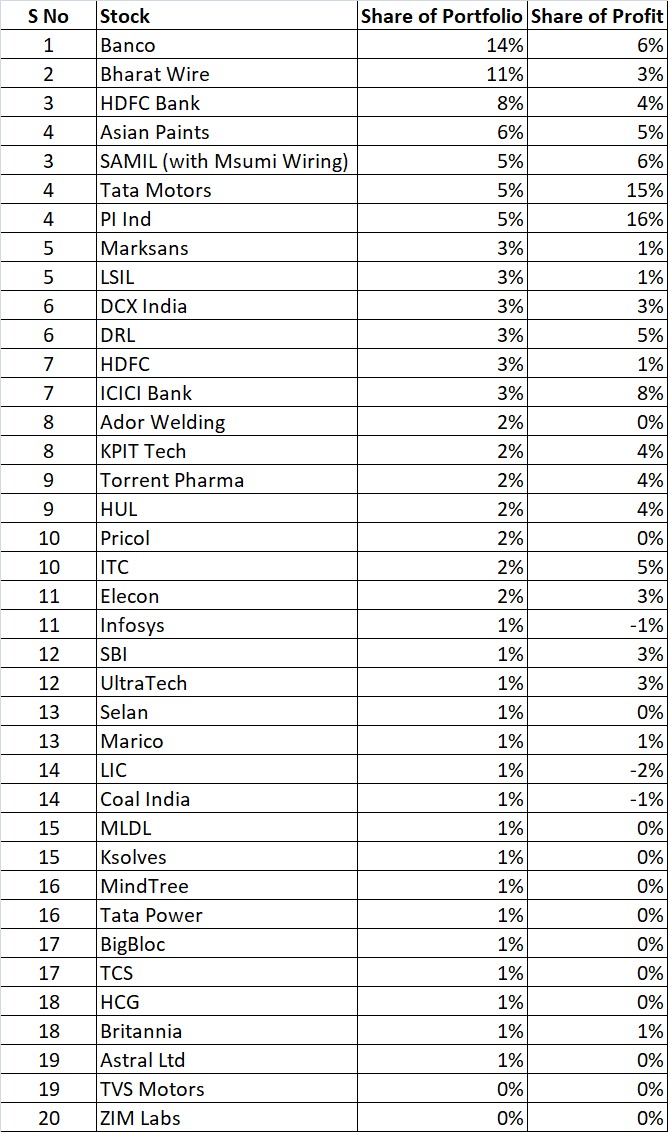

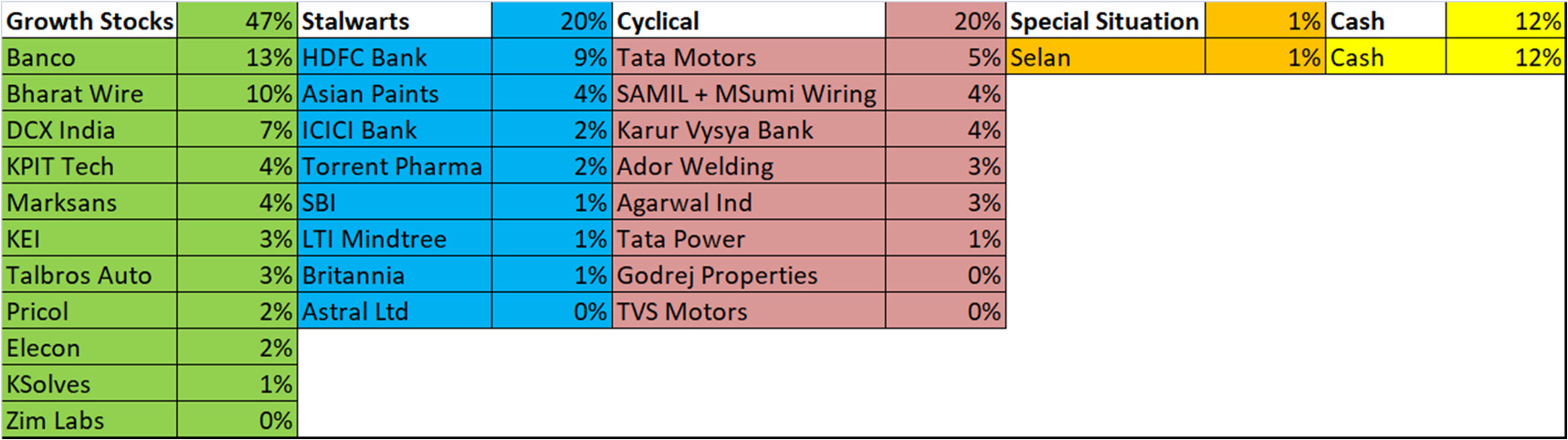

Here is my PF as on 18 June 2023, when I started the portfolio restructuring. As mentioned in my first post, it is a zoo and hence my endeavour to move to a more concentrated PF for better returns and PF management.

Please note that I am restructuring this PF with an aim to move to 10 stocks in total (5 Growth, 2 Cyclical, 2 Stalwarts & 1 Special Situations). There are inherent risks & rewards involved, but I am willing to take the risk, since almost equal capital is invested in index MFs as passive PF.

Disclaimer: My posts are not recommendations to Buy, Hold or Sell. DYOR.

To build my Investment Rationale, I am taking inspiration from “The Investment Checklist - the Art of in-depth Research” by Michael Shearn.

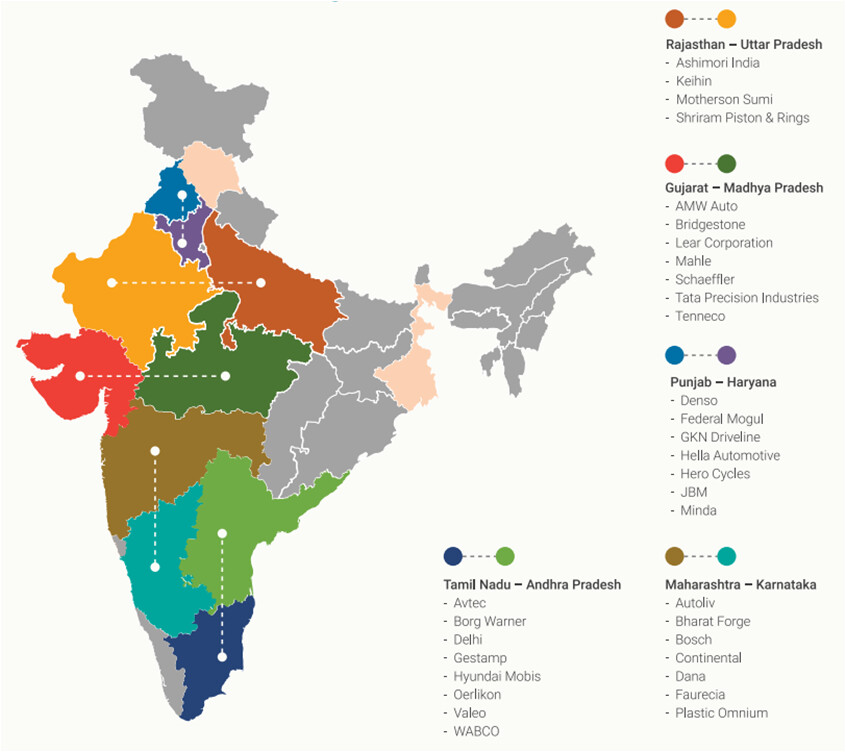

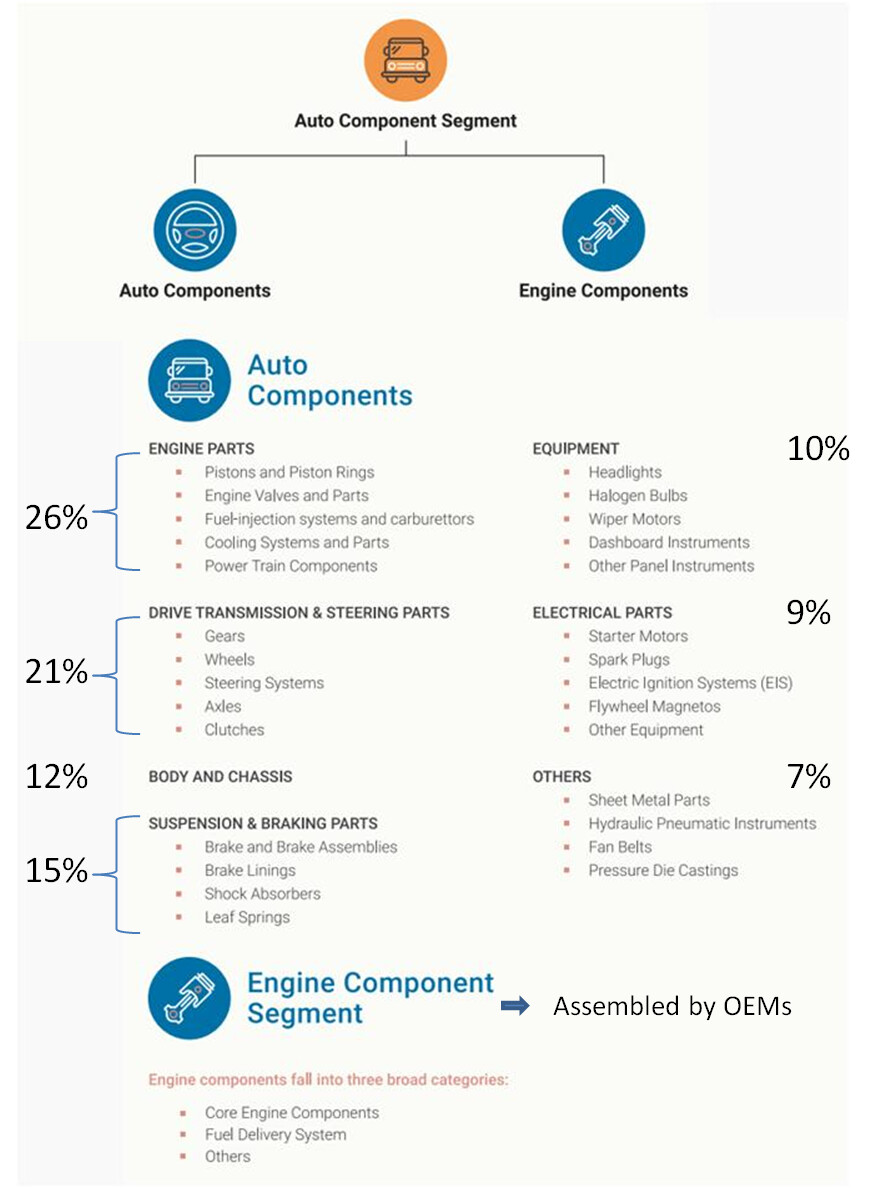

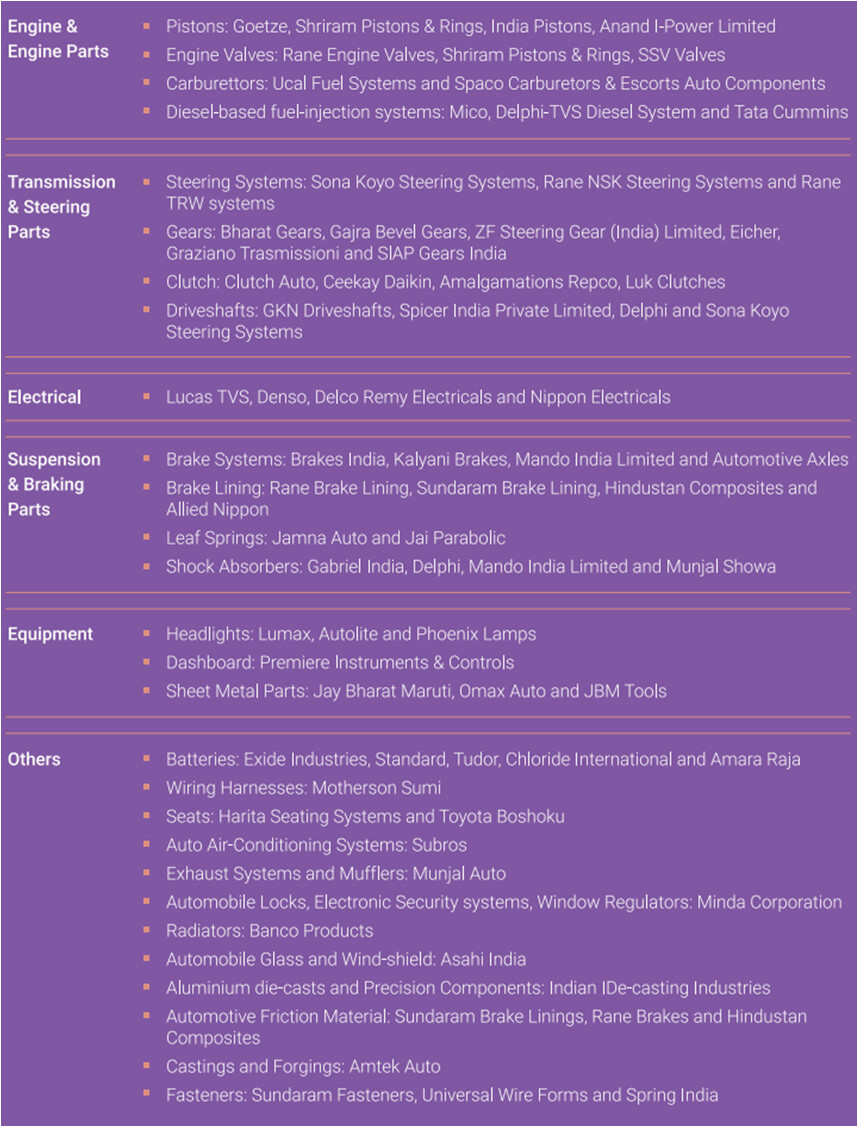

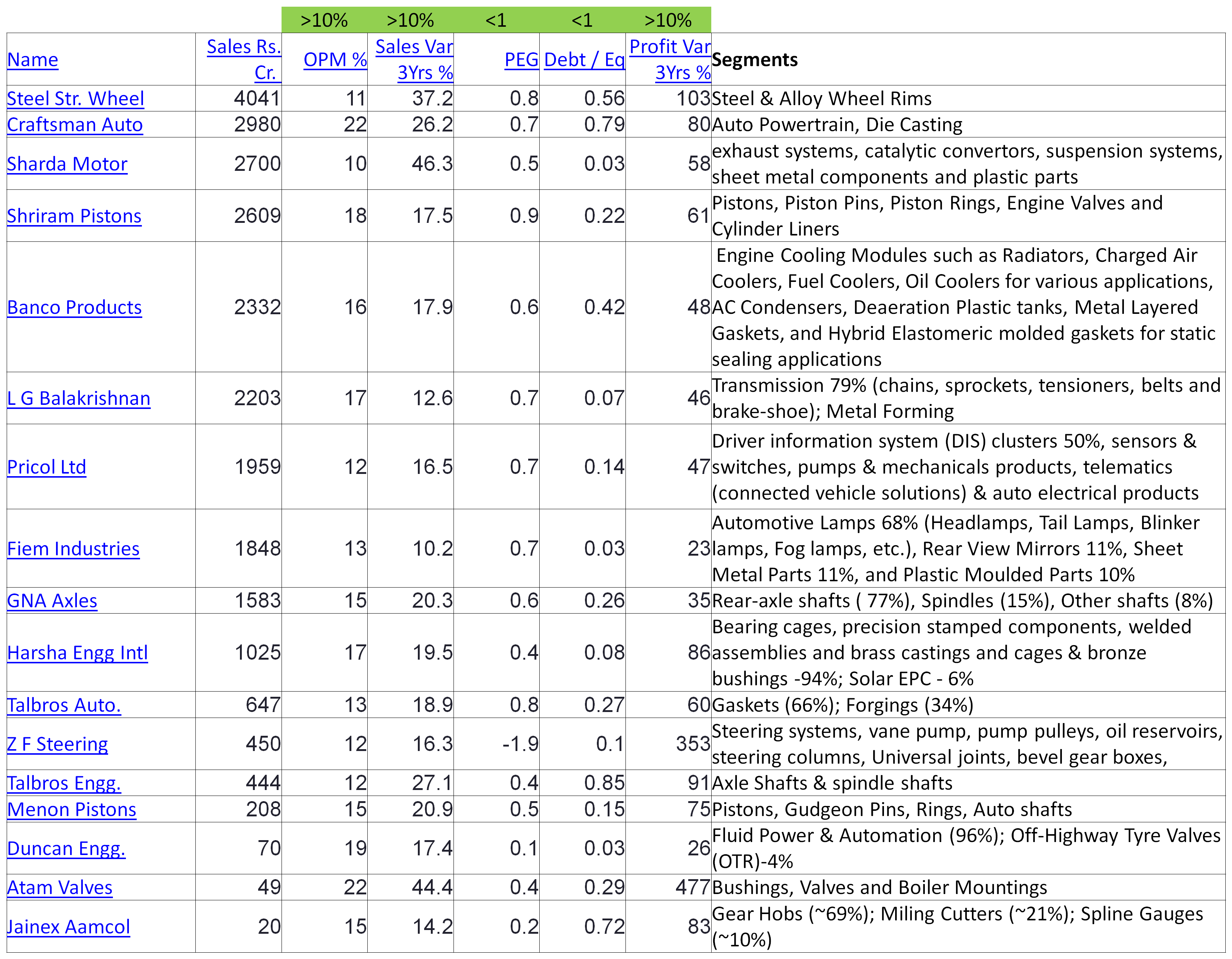

The first sector where I see good opportunities are in Auto Ancillary space, since we are in early phases of interest rate down-cycle and this sector has been picking up well in the last few years (Sales growth in L3Y for median 110 companies as per screener is 2X of L5Y (17% growth in last three years compared to 8.6% growth in last 5 years). There is a dormant thread on VP on Auto Ancillary for more info this sector.

Next steps: further shortlisting based on other financial metrics and Pros & Cons of each to zero down on top 4-5 fundamentally good growing companies.

Refer the thread on Auto Ancillary for further shortlisting and analysis of shortlisted companies.

Thank you for your suggestion on Small Cap. The plan as I have mentioned in my earlier post is to have 50% allocation in Fast Growers, which will be mainly Small & Mid Caps. In Defense, I have 3% allocation in DCX Systems (which was a a technical call). This will increase with conviction & the company delivering as per its plan.

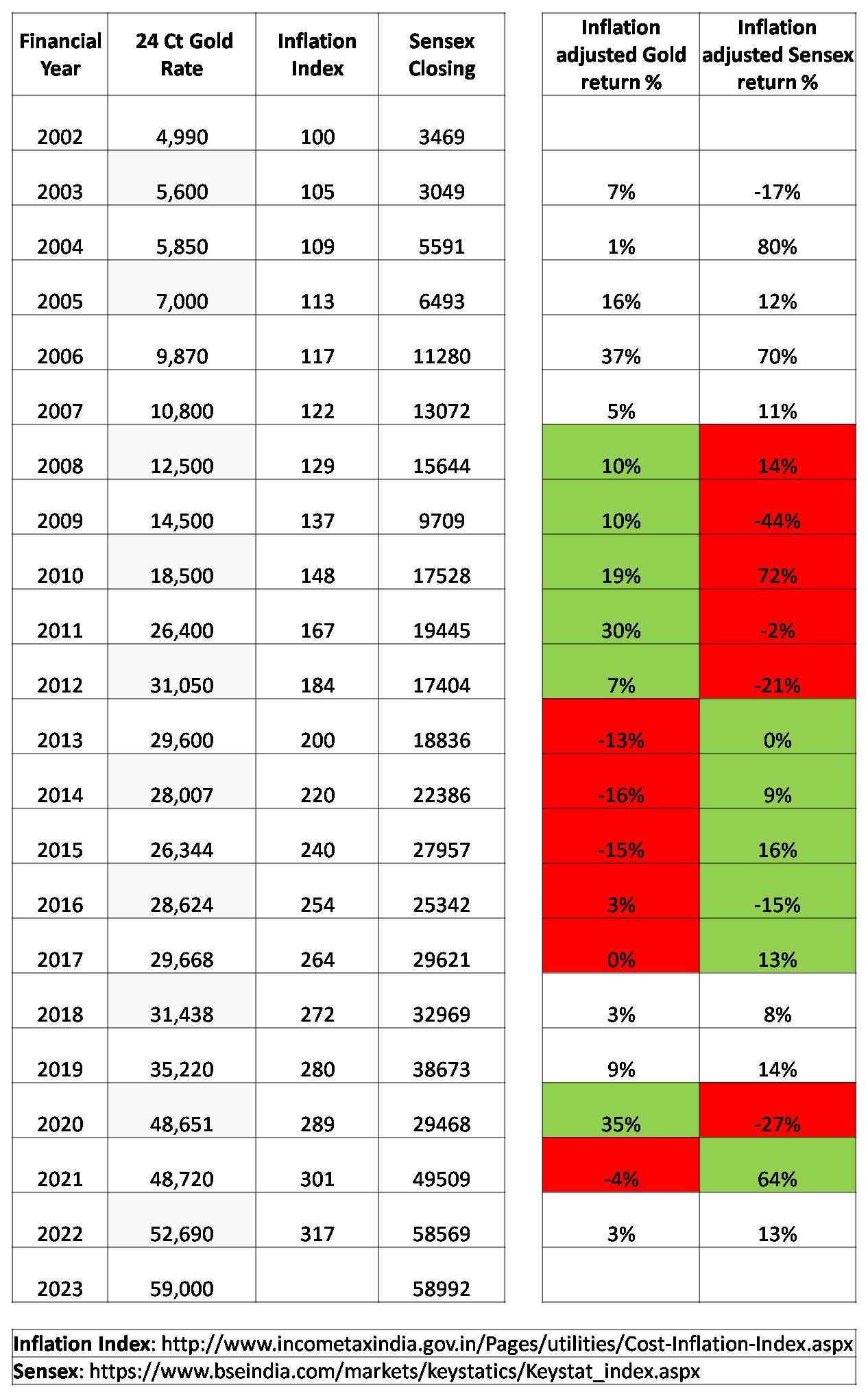

I have a longer term & different view on Gold. Gold as per me should be kept in physical form as the ultimate form of financial security in times of not only doom-gloom (eg, 2008 Subprime Crisis, 2020 Covid), but also unexpected and unforeseen social unrest (eg: think 2022 Ukraine War for Ukrainians or other countries undergoing internal or external problems). I am not expecting/wishing that we will see such situation in India in our lifetimes, but if it happens, Gold being a ‘store of value since ages’ will be highly useful when all else (fiat currency, demat shares, etc) will fail.

I have tabulated three data points: 24 carat Gold rate, Inflation & Sensex values since FY2002 and I can clearly see a negative correlation between ‘Inflation adjusted Gold return’ vs ‘Inflation adjusted Sensex returns’ for multiple chunks of years. So, Gold returns will be high when Financial Market return will be low and vice versa.

But for now, we are in a healthy growing economy, so my all focus is on getting the target return till 2030 which will come mainly through financial markets.

Since the primary expectation from physical gold is financial security & not returns, one should not link it to net worth. Instead, it should be linked to family’s expense (6-12 months) as per appetite to block capital in non-productive asset.

Disclaimer: This is my personal view and many will not agree with the above rationale

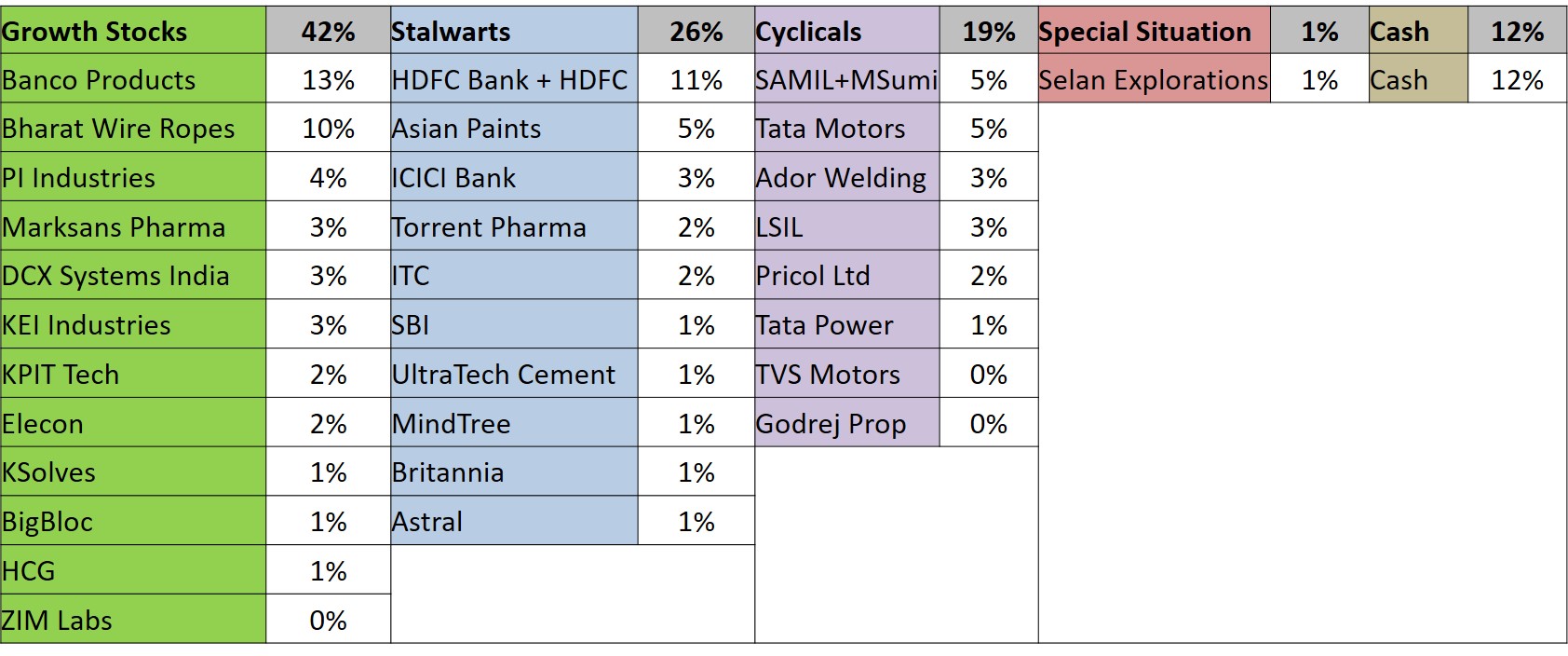

July Portfolio Update: Allocation in line with target for Growth, Stalwarts & Cyclical classification discussed in first few posts. Cash waiting to be allocated to Special Situations or Growth Stocks. Number of Stocks (29) still high.

PI Industries:

Fundamental weakness in Chemical & Agro stocks. PI also broke below its support at 3670 & 50 DMA. RSI declining. Bearish engulfing candle in week-1 of July in weekly chart.

Note: PI remains a superior business and holds a special place amongst my ex-stocks as it has been a 5 Bagger for me (avg Purchase Price of 675 since 2015-17. I look forward to entering it again at lower levels

ITC: ITC has been on a dream run since Feb-22 and has grown 2.5x from 200 to ~500 levels. Demerger announcement of its Hotels business triggered a steep fall in last week of July. It was only 2% of my PF (despite holding it ~150 level) and exiting it is part of my conscious decision to move to a concentrated PF.

LSIL: This was a purely techno-funda bet that panned out well. Cup and Handle formation on daily chart with High Volume on up days and Low Volume on down days. There was a BO with good volume in 1st week of June followed by a retest as per textbooks, before ~40% jump in 2 week. Sold anticipating a correction, while the stock ended up moving sideways for 2 weeks before firing up by 10% again !

In my view: Mayur Uniquoters (MUL) is not a pure play Auto OEM, with revenue coming from following segments: (source: screener)

Footwear: 31%

Automobile replacement: 21%

Auto Domestic OEMs: 15%

Auto Export OEMs: 20%

General Exports: 8%

Others: 5%

Footwear segment has been a drag on revenue growth as well as margins for a long time and the company has not been able to address it adequately.

MUL thread on VP documents the company’s journey from being discovered by VP stalwarts (Nagabrahma, @Donald@hitesh2710@basumallick and many more) in 2010 to becoming a 50-bagger and then losing the plot due to problems of scaling up and internal succession plan. I re-read the entire thread today and could visualize all of it like a cinematic story.

Coming back to answering your question:

MUL can be a turnaround story with revenue growth picking up since 2022, after years of stagnation at ~500 Crore. The revenue growth guidance from Mr Suresh Poddar in 23 May 2023 con-call is 17%, 18%, 25% & 30% for the next few years.

However, as per my assessment, the candidness of top management, which used to be one of the key highlights of con-calls during its early years are missing. So, I would like to see these numbers being delivered before taking a positive investing decision.

Not much activity on technical charts as well:

Stock is in Stage-1 (Basing Area) and is oscillating around its 50 & 200 DMA, which are both flat. As per Stan Weinstein, “the basing action can go on for months or, in some cases, years”.

The immediate resistance levels as per Fibonacci are 550 & 630, which are also major supply zones.

RSI in this raging bull market is sub-60 and minor 2-3 signs of volume spikes in last 3 months.

Buying/Selling/Holding depends on a lot of factors such as your Risk Appetite, Holding Period, Portfolio Construct, etc. All of these are different for everyone, hence you have to take this decision yourself.

Nothing really wrong with your portfolio . I dont intend to over analyze. Obviously you need to understand competitive strength of each company and judge their ability to grow their segments . They should be adding market share or penetrating adjacent sectors. I would be wary of story stocks or Next big thing stocks or stocks where huge run up has already taken place. 1% holdings need to be questioned for rationale and if they have significant potential going forward … Bigger companies are well understood but smaller companies … unless you have insider knowledge you cant be sure whats going on…

Thanks and a side note

Is this % of portfolio based on current market price or amount invested ??

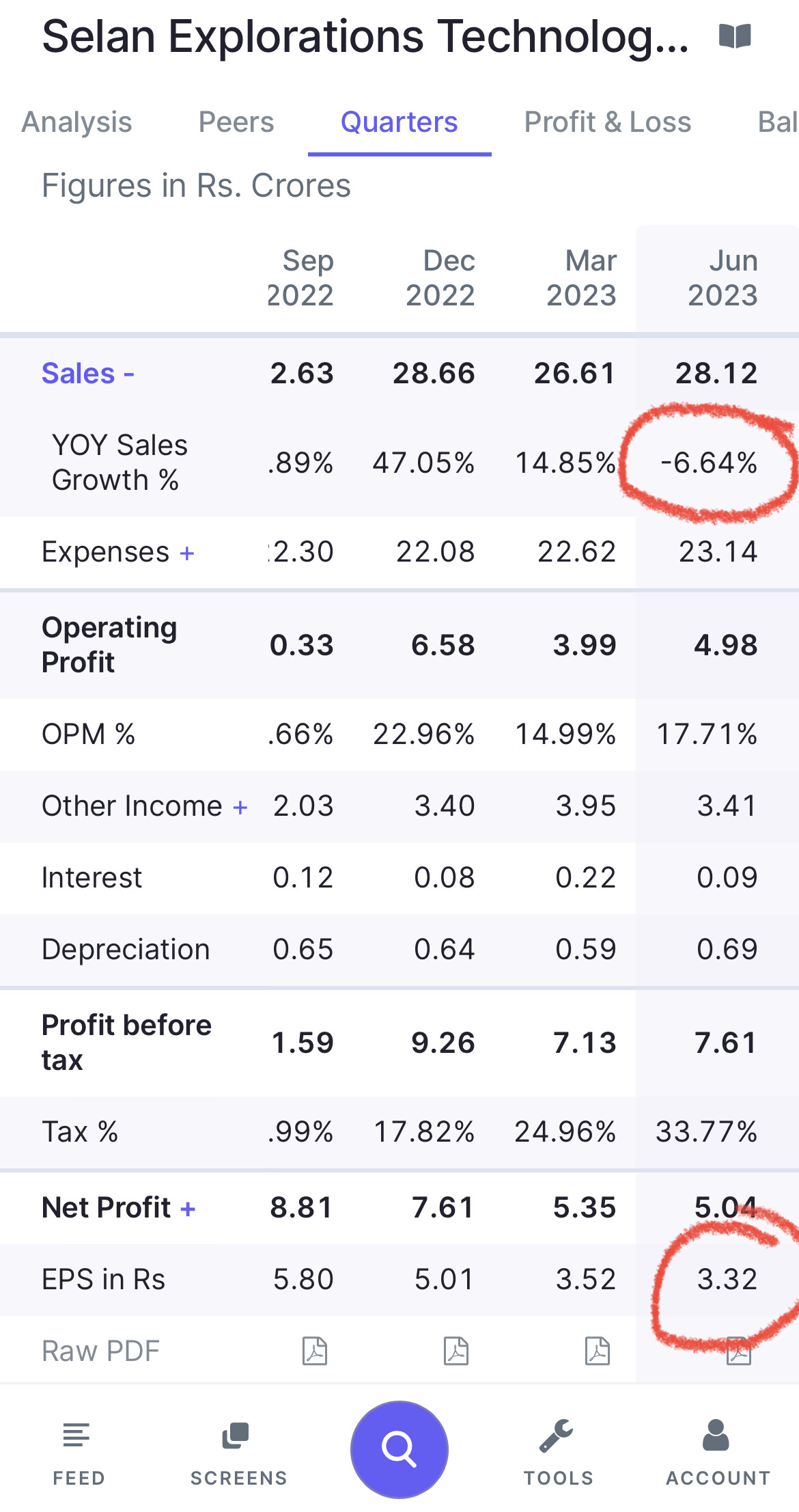

Selan is a turnaround situation with a new management in place since last year, who I believe are more capable and determined to turn it around. There is also a merger (reverse merger) on the cards. More details about it can be found on this blog by Pawan Kaul.

Disc: I have exited Selan in Aug after a drop in Revenue and EPS in AMJ quarter and in pursuit of greener pastures. This post is not a reco to buy/sell/hold any stock. DYOR