… this is a continuation of the earlier post.

To design my 2030 portfolio, I have taken inspiration from the “Peter Lynch Playbook” shared by Mayur Jain (you can google it) to ‘pick right players for the right position in my sports team’.

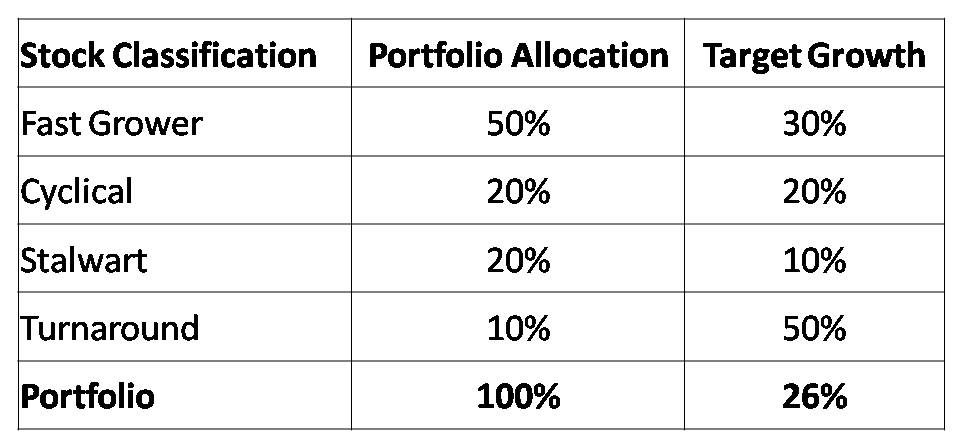

I have chosen a mix of Fast Growers (Growth Stocks), Cyclicals, Stalwarts and Turnaround to achieve the target return of 26% CAGR.

Many a times, one stock can fall in more than one of the above classifications (eg Fast Grower can be a Cyclical, or a Stalwart can be a Turnaround candidate) and hence the above guideline is a framework to guide capital allocation decision rather than being prescriptive. It also avoids two categories of stocks: Slow Growers & Asset Plays for obvious reasons.

My notes on these classes of stocks:

A) Fast Growers:

- Minimum Revenue and Earning Growth at 20%-25%

- Big companies have small moves, small companies have big moves

- Moderately Fast Growers (20%-25%) in slow growth industries are ideal if they operate in a niche, since they can capture market share without price erosion

- Hunt for ‘great companies in lousy industries’, rather than ‘hot stocks in hot industries’

- Identify Fast Grower early (Startup Phase), but get on in next phase (Rapid Expansion), ride till Maturity/Saturation and sell before it hits the Slow Growth phase. This is akin the 4 Stages defined & popularized by Stan Weinstein & Mark Minervini.

- Earnings growth is the only growth that really counts - keep checking and asking yourself “what will keep the earnings going?”

- Inability to maintain double digit growth may see a re-classification into Slow Grower, Cyclical or Stalwart. High fliers of one decade are groundhogs of the next.

- Every Fast Grower turns into a Slow Grower, fooling many people. People have a tendency to think that things won’t change, but eventually they do.

- 20%-25% is more sustainable than 30%

- Emerging growth stocks are more volatile than Stalwarts, like ‘riding a tiger’ (a phrase mentioned multiple times in this forum by @hitesh2710 ). Have the guts to face -10% markdown and still hold on to your conviction

- Expect high PE ratio for Fast Growers, as long as the Earnings growth keeps pace with Price growth. Refer to Chapter-4 (Value comes at a Price) of ‘Trade Like a Stock Market Wizard’ by MM (Mark Minervini), when in doubt.

- 20% growth @20PE is better than 10% growth @10PE

- If you sell at 2X, you won’t get 10X - be greedy as long as Earnings keep growing

- Consider selling (& rotate proceeds into another fast grower) when: Earnings start slowing down, stratospheric rise (>50% in one month) without any change in earnings growth, end of Stage-2 as per technicals, wide covage in media or PEG starts to increase beyond 1.5-2.0

(B) Cyclicals:

- Identify, acknowledge & accept Cyclicals as they are: their revenue, profits and stock price rise and fall in/out-of-syn with the economic cycle (a-la interest rates).

- Detect early signs of business change (eg: inventory buildup) to detect an up-cycle/down-cycle

- Prefer High OPM (proxy for low-cost producer), since it will bode well in times of grief (down-cycle)

- Best time to enter is when economy is at its weakest, low earnings, dividends are being cut , doom-gloom scenario

- It is perilous to invest without working knowledge of the industry and its rhythms.

- Timing the cycle is only half the battle. Other half is picking the companies that will gain most from an up-cycle. Choose companies with ‘Staying Power’ (strong B/S, low D/E, high Interest Coverage Ratio, etc)

- Cyclicals have inverse PE cycle: low PE at the top of cycle and high PE at the bottom of cycle

- Don’t hold on to Cyclicals thinking it is a Stalwart of Fast Grower. eg: Motherson Sumi (SAMIL) has seen 2 cycles since 2016 and I have been through them without making time-adjusted returns. Similar is the story for Tata Motors and those who are cheering that it is nearing its ATH of 600, may as well note that being a Large Cap cyclical, it will cycle-down as it has thrice in the last 2 decades. Disclaimer: both are great companies and are part of my current portfolio from multiple price levels and are cited as examples only, its not a recommendation to buy, hold or sell DYOR.

(C) Stalwarts:

- Growth is decent (2X of GDP growth), but not very high (like Fast Growers)

- Long history of consistent business, have built their name (brand) in the market. Mostly found in consumer facing industries and have a deep Moat

- Provides a cushion in hard times - do not fall as steeply as others & do not go bankrupt

- Don’t hold on after it’s 2X, hoping for 10X (except when you bought in times of rare distress for the Stalwart)

- If you can find a company that can raise prices without losing customer, you’ve found a terrific investment

- Be wary of ‘de-worsification’ as capital allocation is the toughest for a cash-rich B/S

- ‘There are many possible reasons to sell a stock, but only one reason to buy’ - insiders know something you don’t know - keep a track

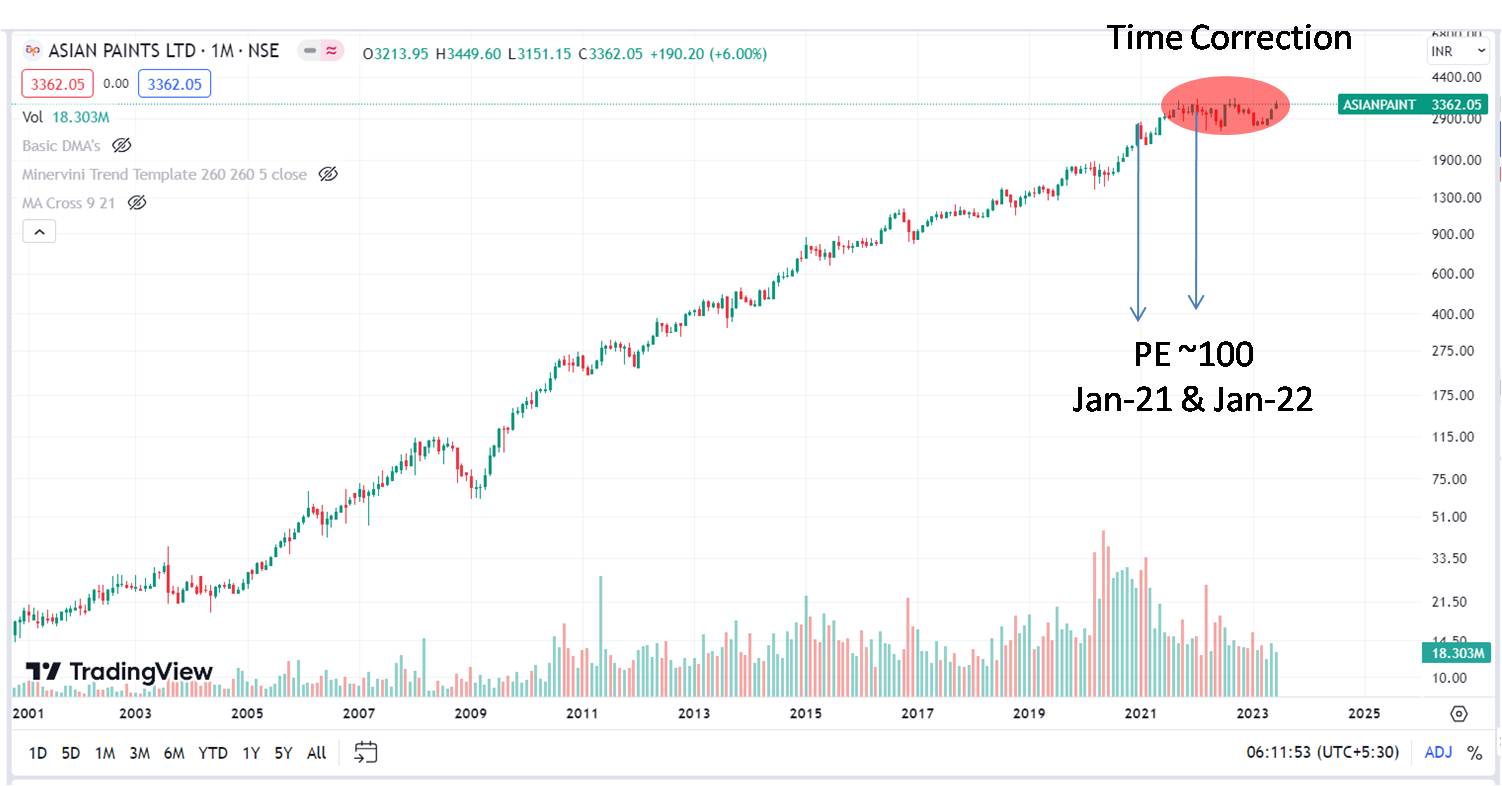

- Sell when PE gets heated compared to nearest competitor or industry. These are signs of ‘rest’ (time correction) or decline (price correction). eg Asian Paints in Jan-21 & Jan-22 had ~100 PE and was ripe for correction through price or time.

(D) Turnaround:

- Distressed due to one of the reasons: waiting for Govt bailout (eg. Voda-Idea), sudden policy change (eg: IEX), restructuring candidate, years of poor management leading to takeover by superior management (eg Eveready), High Debt, etc

- Cyclicals with poor B/S may fall into Turnarounds

- Survivorship Bias rules here: failed turnarounds are nowhere to be found since they are long dead

- Improvement in business can lead to quick upswing, key is to track the business metrics.

- Buy when first good news has arrived (in terms of growth, margin improvement, restructuring, management change, reduction in Debt, etc)

- Never rush to buy a distressed company thinking it can’t go lower, it can go lower than you can imagine (eg Yes Bank)

- Sell when the turnaround story is well known, Debt is reduced, rich PE