RPSG-Ventures-18022022-arih.pdf (545.6 KB)

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2b0f3d1a-6e78-4736-9fba-c6efe755f20d.pdf Results are out

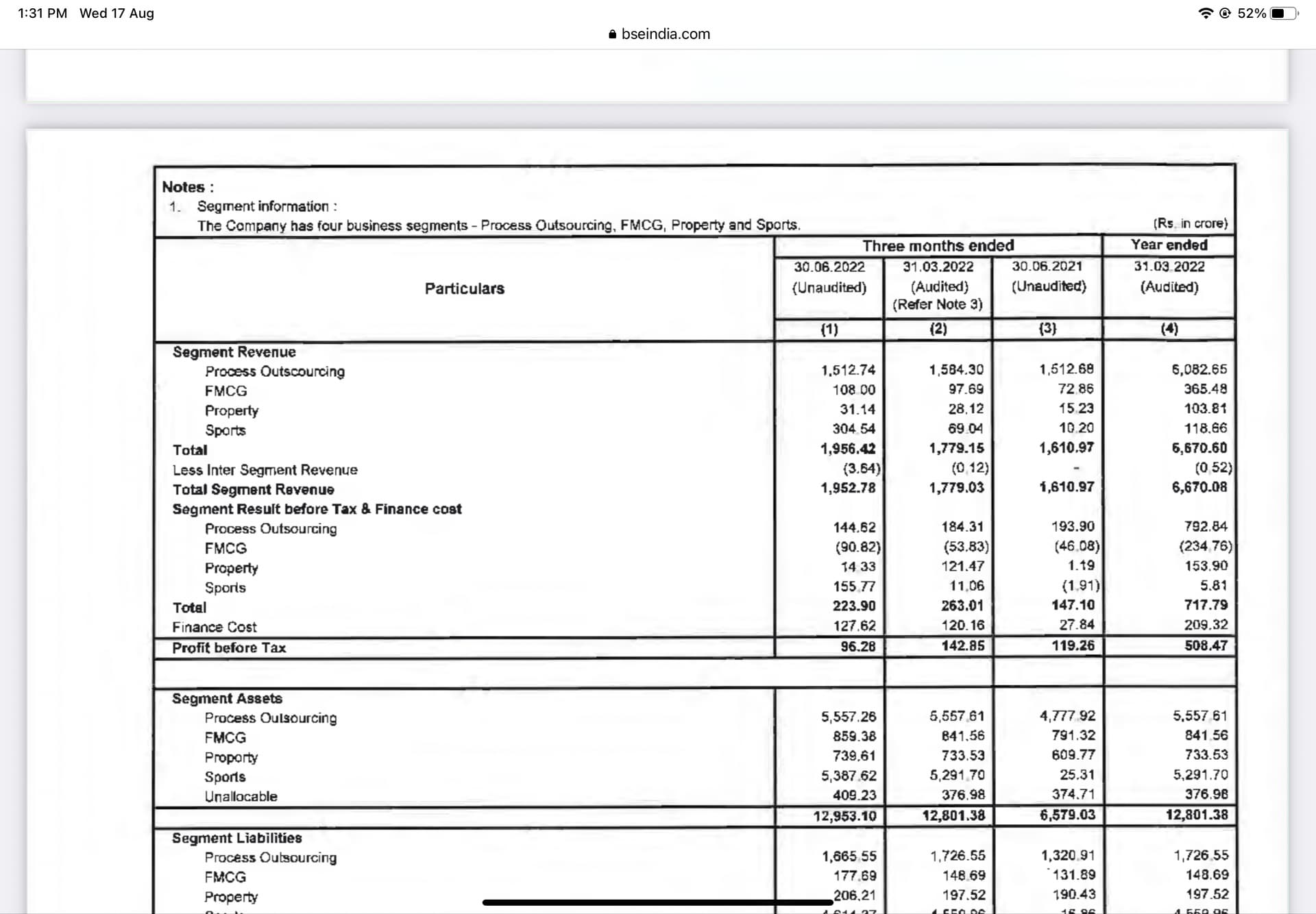

As expected ipl has contributed to both topline and bottom line. Next year will be much higher.

What baffles me is the burn rate wrt their fmcg business.

For 1 rupees of revenue they are spending about 1.9 rupees

I haven’t seen their advertisement etc but the burn rate of fmcg business is incredibly bad.

With current pace fmcg business will achieve around 450 cr of turnover.

Did anyone attended the agm (if yes, kindly share the notes)

1 Like

Rpsg venture capital made first exit with 7x returns. Readies 500cr for next round of investment.

But looking at the current results, the leverage is high and FMCG is burning cash.

2 Likes

If they can get their act together in fmcg business.company would be incredible.

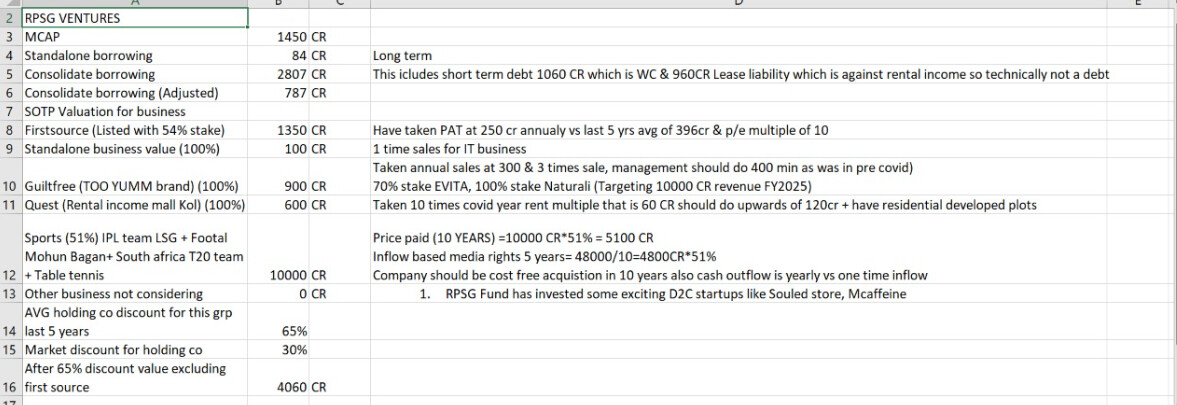

Having said that what’s your view on valuation of the company.

I would argue that holding in first source solution should not have a massive holding company discount.

As dividend are used to fund growth into other venture.

Rpsg venture fund is a success.

Ipl business is like a annuity business plus sports league with ipl’s viewership command premium valuation.

(Ipl teams should do a series like drive to survive) it had a massive positive impact on viewship of F1 in USA.

Fmcg is the laggard hopefully it picks up too.

2 Likes

Hello Seniors,

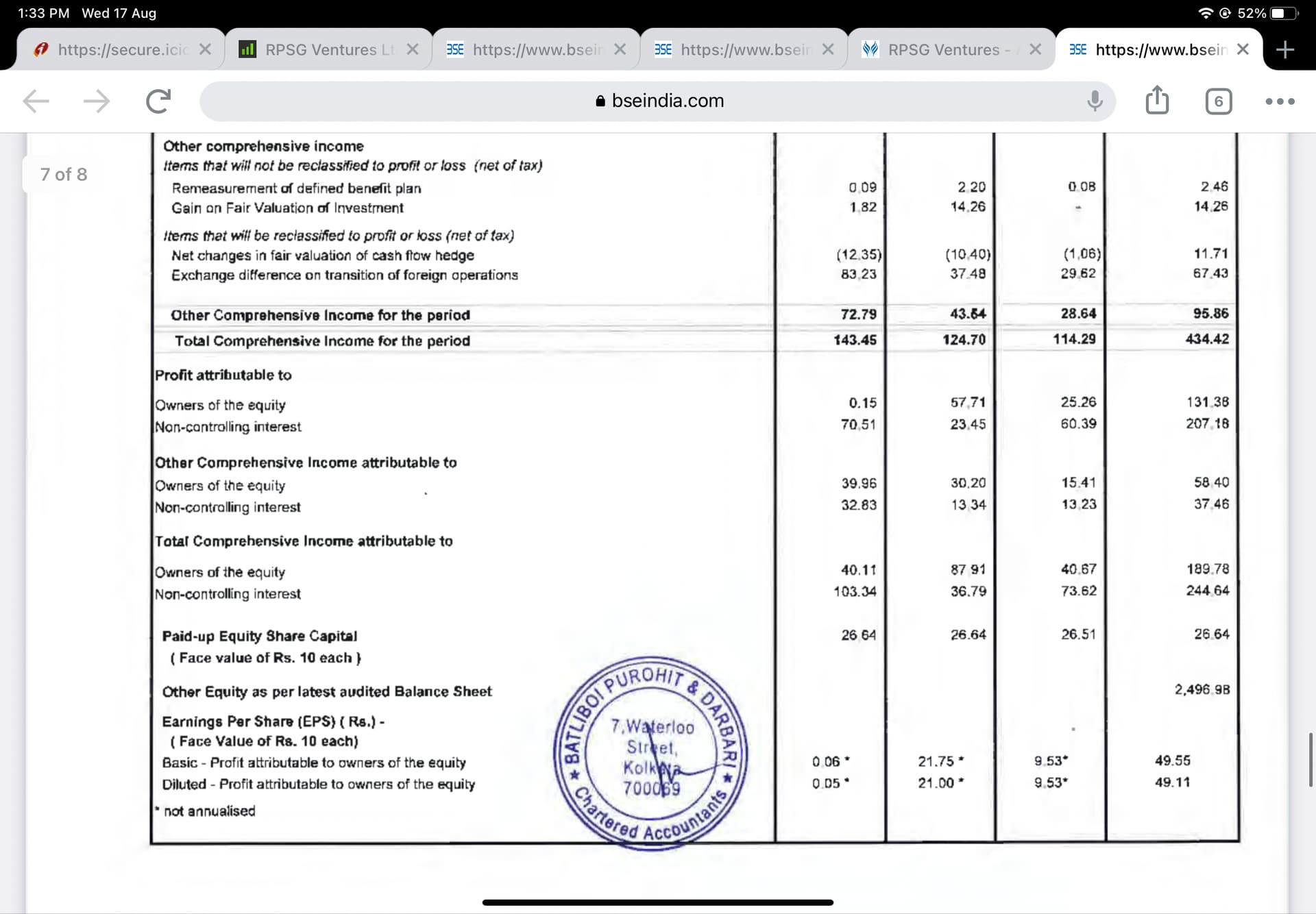

I am new to this forum as well as to investing. I have been tracking RPSG for quite some time. The recent quarterly result baffles me. Can someone please help me understand the huge drop in PAT in this quarter? I couldn’t find any info on this.

Disc: Tracking position

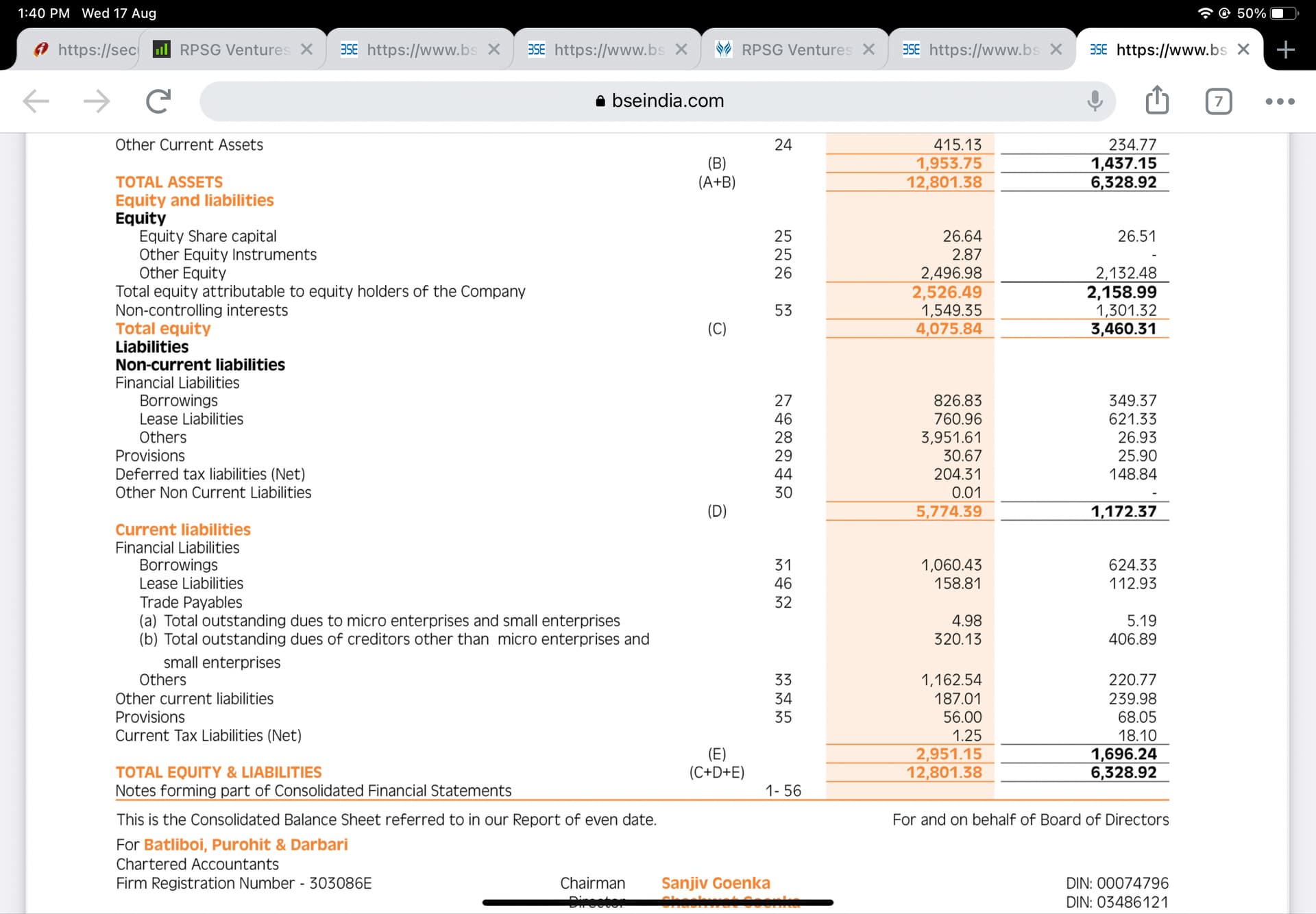

Company took loan for buying IPL team which increased the interest cost.

Some equity dilution was also done for the same purpose which reduced the eps further.

Thanks a lot Akash!! I will check further on the equity dilution part.

Rpsg venture is a holding company.

Results of it subsidiaries are consolidated.

Net profit before tax shows entire profit

Which is allocated between owner and NCI

Rpsg hold around 51% of the sports division and 54% of firstsource solution.

- Drop in profitability is due to following reason.

Increase in finance cost Unwinding of liability payable to BCCI (franchise fee is shown in books at present value and interest expense on the same is booked as expense).

Fall in profits from firstsource ( I have limited understanding of firstsource) they are facing headwinds due to the recessionary conditions in the USA.

Increase in losses from fmcg business (need to ask management reasons for the same)

1 Like

Isn’t the auction flawed? RPSG paid 2k crore more than the 2nd largest bid on Lucknow.

Also, did they have an option to choose between lucknow and Ahmedabad or was Lucknow selected to maximize the payout to bcci.

He says Present value of investment is 916 cr at present value. Going by that logic other investors were trying to buy it at a negative value?? because they were 2k crore less than rpsg. Frankly I dont get the exact logic. Surely all the other investors also know what they were doing.

RPSG would have got lucknow at 5200 cr also!! Ofcourse a diff of 2000 cr should be huge.

1 Like

The valuation, purchase cost and profits of the IPL team are not clear. The company has diluted it’s equity by a significant margin. FSL profits are stagnant and it’s multibagger venture exits are not trickling down to shareholders. Also the debt quotient is increasing over previous periods and at an all time high. FMCG is still not reliably profitable. The operating profit is 289cr but profit attributable to shareholders is 0.15cr.

The stock price has rightly corrected from 1100 to current levels and may test further lows. The promoters need to work on clarity and governance here. None of the Stocks from RPSG group is properly valued and this should be a concern to shareholders.

4 Likes

10% promoter holding is locked. Is it pledge?

Sadly, the growth is not trickling down to minority shareholders. There is a reason why none of the RPSG group stocks are valued strongly.

1 Like

Saregama is the exception here.

They have invested heavily in branding for FMCG but still it is not growing much. I have tried few namkeen items and its test is ok.

Why is that so, any reasons?

Can you pls elaborate on this? Thanks

1 Like

They recently exited a venture for multibagger returns. The shareholders have not been rewarded. Most Reputed IT and FMCG companies reward shareholders with dividends.

Also, the profit attributable to equity holders is a concern vis a vis total net profit.

Finally, the promotion and advertising is lacking for its customer centric FMCG brand.

The stock price has corrected to half from highs in October 21 and the markets are valuing the company accordingly.

Just my two cents.

Disclosure: holding the stock.

Just my opinion based on recent events and expecting some clarity from the company from now. No buy/ sell recommendation.

1 Like

RPSG Ventures have 3 main areas - IT enabled services (most value come from 1 co - FirstSource solutions and it is not doing well and looking at low or -ve growth in next 1-2 years). FMCG biz - most of its investments except yum brand not doing too well but can be a dark horse if they pull up their socks. Sports - overpaid for some franchises but a long term opportunity

DIsc: Adding at current levels. I copy some of Ashish Dhawan pf-this is also one of the overlaps

2 Likes

Again dilution CCPS share:

Allotted CCPS at 770Rs per share

Any I dea what happens to the franchisee fee after the 10th Year?

1 Like