Franchise Fee is 20% of total revenue after 10 years. Can be checked in the financials of RCB and CSK, where the initial franchise period has elapsed.

How much of rpsg capital does rpsg venture own?

LSG valuation 8K Cr. Don’t understand this valuation.

1 Like

Q4 result is very bad and there is negative EPS of 53.72 against positivie 49.55 in FY’22.

loss in FMCG division increased to 309.38 Cr and interest expense increase.

any one tracking this company has some details to share

1 Like

I think it will take at least 5 years to come back to positive due to heavy liabilities of IPL team.

Check balance sheet page 155.

5,346 - Non Current liabilities

3,805 - Current liabilities.

Total 9000Cr. Too huge. Their main income is only dividend from FLS.

2 Likes

This will mean the promoters will increase stake by infusing capital over time.

Retail investors do not stand to gain much just like the profitable exits RPSG ventures has made till date which have not provided retail investors anything.

Their FMCG business is yet to show real profits.

also there is not much disclosure on volumes, strategy and performance of FMCG business or investors presentations

1 Like

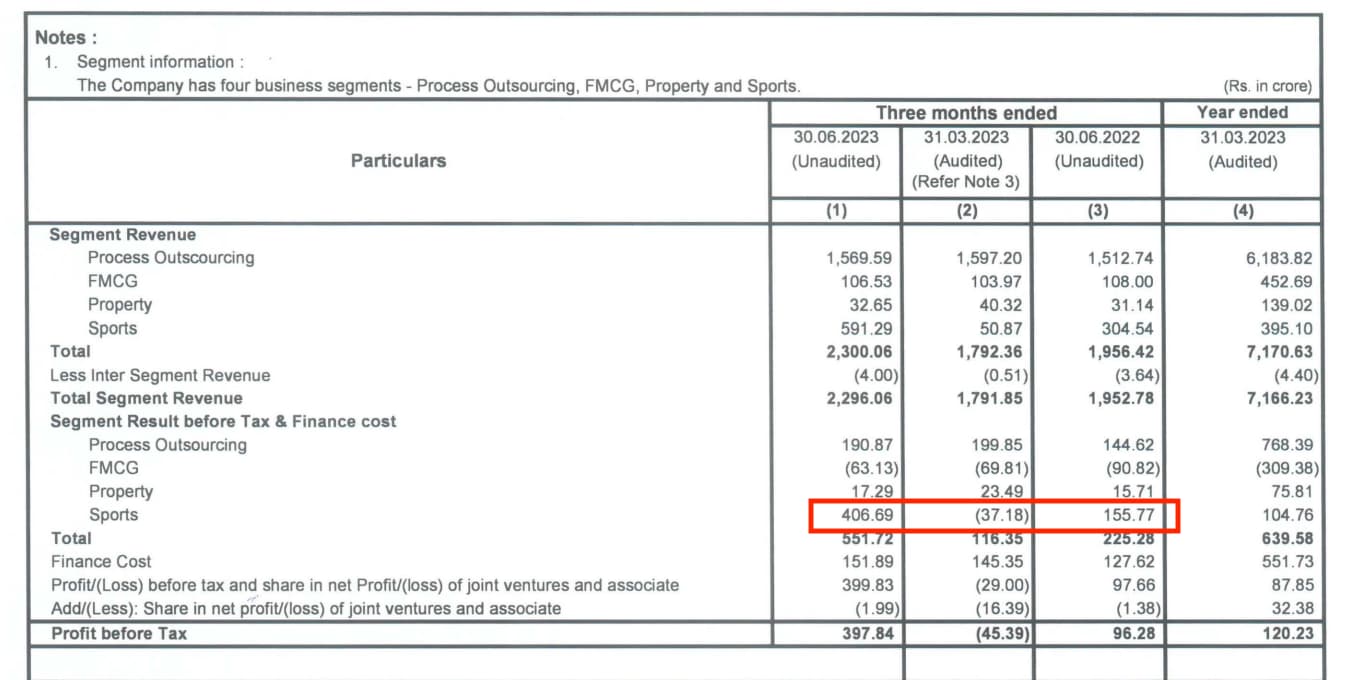

Amazing results. All thanks to their IPL stake. YOY growth in EBIT from 155 Crs. to 406 Crs. This will go even higher as they build their brand value and from next year the increased media rights are enforced.

3 Likes

As per the video, Macquarie believes that even if the promoters don’t go for voluntary delisting, the discount at which the holding companies trade should get reduced.

2 Likes

Hi,

Any idea reason for sharp up movement in last 15 days with approx 25%+ ?

No announcement or news, hence wondering…

OR following market bull swing ?

Thanks.

Saudi arabia has proposed funding 5 billion in IPL.

https://twitter.com/TimesAlgebraIND/status/1720426592806277600?t=Bixk9Yd6lLZgQTI3YcCufg&s=19

Arihant Capital sees target of 2500 in long term.

https://twitter.com/darshanvmehta1/status/1727173894942187594?t=kUlH1i4CnQRBzdhJaYui0Q&s=19

Sanjiv goenka group share prices rising.

Bought just 100 share @540 few months back

1 Like

Thanks, Rohit for prompt response. Appreciate it.

1 Like

- Potential of listing of the FMCG business in future, which is currently in the scaling up stage

with good prospects of generating profit in future. - Too Yumm brand is growing well while it has relaunched its personal care business.

2 Likes

Hello Everyone,

Have a look at the RPSG Ventures scrip, its from the stables of Goenka group owning several recognized names like CESC, CEAT, SAREGAMA, Spencer retail, Philips carbon and First source solutions.

Rationale for investment:

-

54% stakeholder of First source worth 7k Cr (54% value)

-

49% holder of Lucknow Super Giants IPL team worth 4k crore (49% value)

-

Owner of other sporting franchise like ATK Mohun Bagan in Kolkata

-

100% of Quest mall in Kolkata worth 700 cr

-

100% owner of FMCG brands like Too Yumm ( Virat Kohli is the brand ambassador), Dr. Vaidya for ayurvedic medicines (mainly viagra), Shampoo brand promoted Kirti Sanon

-

It also funds several D2C startups ups which could be sold or go for IPO with windfall profits.

-

Promotors are have last week added 10% stakes at 795/share via Qip.

-

Renowned investors of this gem include CLSA, Ashish Dhawan and many more.

**All the above for a market cap of only 2300 cr … **

7 Likes

There’s a 3k crore debt that you’re missing. Also, the holding company discount is pretty common in such cases, & a lot of these are private businesses, whose valuations might not be accurate.

That being said, the promoter participation in the QIP does give some confidence…

6 Likes

Debt certainly is there and its pretty sizeable compared to the market cap. This actually could turn to be a positive factor once the rate cycle starts to reduce, the reduced component of interest cost on the P/L will be significant.

Holding company valuation is usually around 30-40% of the actual value, however still its a very undervalued scrip with a fair value of atleast 7500cr i.e. a 3x opportunity.

speaking of holding company discount, does the same apply to Jio Finance valuation for its 6.1% holding in RIL …!

2 Likes

Unlike typical holding companies, which are mostly pass-through vehicles of ownership, Jio finance actually has a much greater use of the Reliance holdings. It can easily borrow at extremely good rates, keeping the Reliance holdings as collateral & earn a respectable RoA… So the holding co discount should be treated differently here IMHO

2 Likes

Apart from Holding Co, RPSG Venture has steady earning through IT services being provided to CESC (another group co.)

1 Like

Tata has renewed the title sponsorship at 2500cr for next 5yrs, earlier they paid 670cr for the same contract of 5yrs.

at 50% distribution among the franchisees its 25cr for each team each year, compared to 6.7cr last year.

This should again add to to P/L of RPSG

3 Likes