@Investor_No_1 as you mention 1500Cr cash will get in 5 years but also need to payout some amount (Dont find exact amount) every year. Hence It will generate revenue not cash and may be company will report loss due to this.

@akash_das Ashish Dhawan and Porinju Veliyath are not reducing their stack. If you check the number of share they held in this March and Dec quarter are same. Only percentage of their holding is reduced due to equity dilution.

I am expecting more equity dilution moving forward to reduce debt. But the problem here is CMP is cheap and difficult to raise fund at higher price.

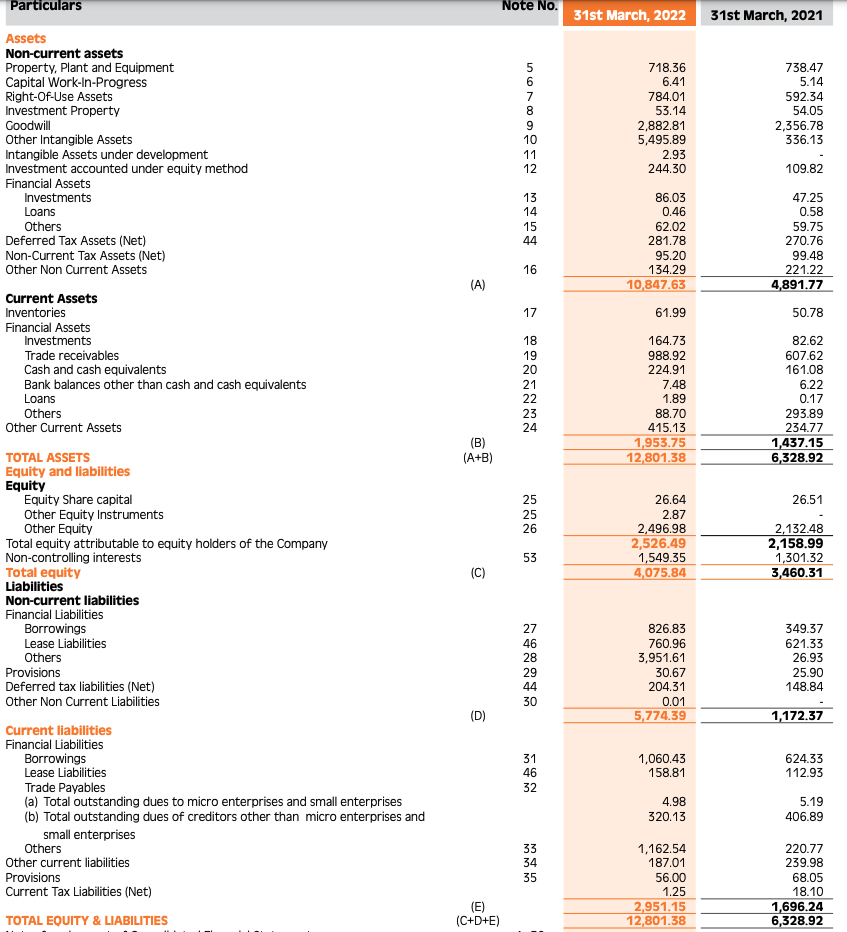

Does anyone know the payout number to BBCI for first year and next 5 years? I am not able to get the exact data. The only risk I can see here is debt of 2,807Cr. And dont see any debt reduction plan in presentation. Also note that the holding company FSL has debt of 1700Cr.

According to my estimates, the new IPL media-rights price should be very bullish for RPSG Ventures and mean that much of the cost of the buying the team and operations should be paid for by the media-rights given the ~500cr annual payout from BCCI plus additional sponsorship revenue. Thus the company would have bought the team at a fraction of the 7k crore headline price and much below where peer CSK trades on the private market

The revenues and costs from the IPL team should be consolidated into RPSG Ventures given the 51% stake in the venture so I expect EPS to go up due to IPL, which could be a trigger for the stock given the deep discount to NAV it currently trades at

Disclaimer: This is the work of an investment adviser affiliated with the author. The report is the result of the adviser executing its investment strategy. The adviser holds a position in the security, however there is no assurance that the adviser will continue to hold the investment, or make additional investments and will not update the information to reflect future changes in the adviser’s assessment of the investment.

Yes, we will see in revenue jump but not sure on profitability. Probability may impacted due to IPL team payout for first year.

Also, I agree that the 7K cr is not very high valuation because CSK is trading at 6300Cr market-cap and after 5 years value get doubled. Same thing management was explaining earlier.

For LSG bought 7060Cr which required high franchise cost. Here is the calculation:

Income:

BCCI pay 50% of Broadcast right 48000Cr to team for 5 years and 10 team = 480 per team(48000/(2510))

Remaining income can ignore(very less)[https://www.timesofsports.com/cricket/ipl/sponsors/]

Total income = 480Cr

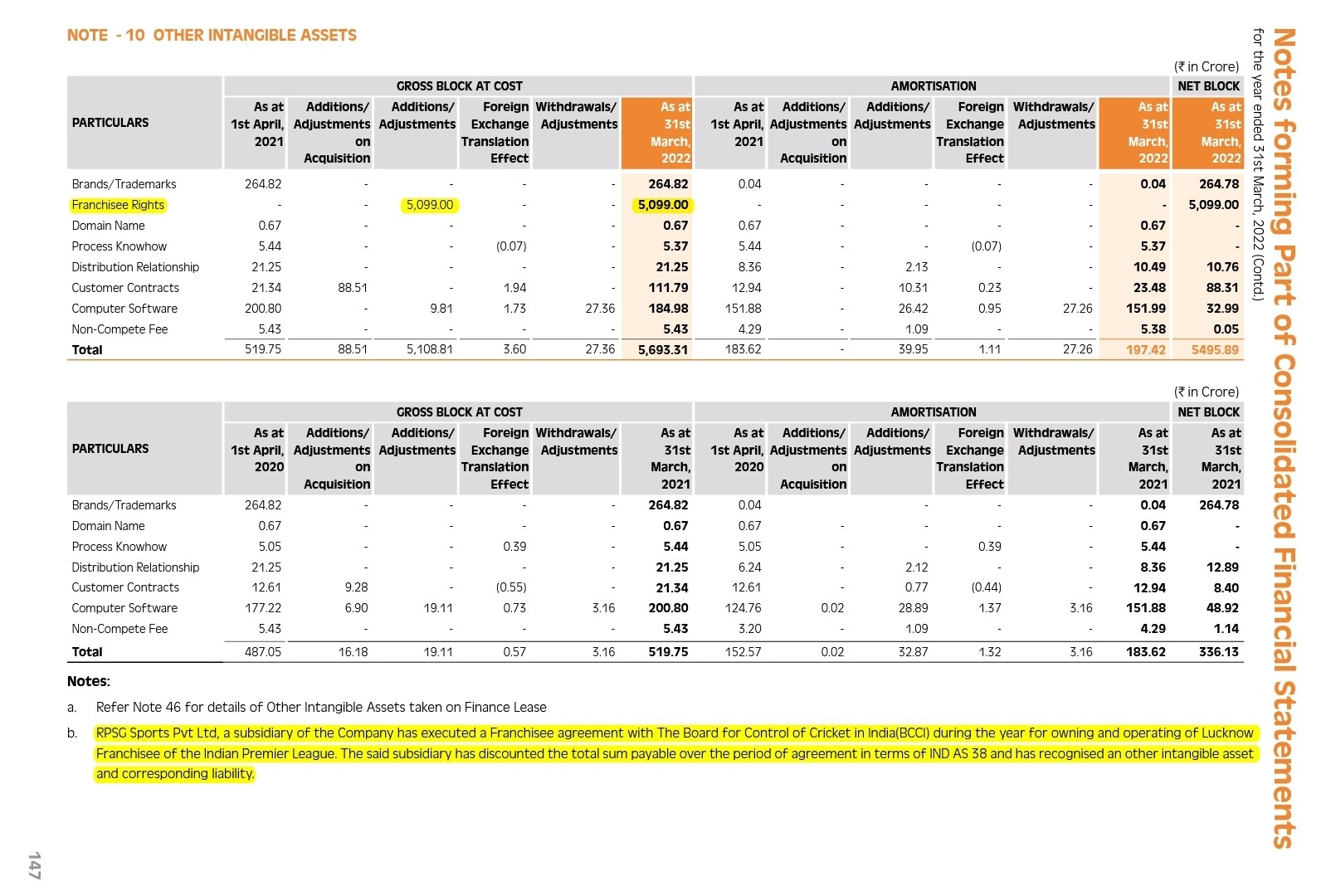

I dont think 7090Cr is the present value. I have watched all the interview and sanjiv goenka was quoted 3400Cr was the net present value. In the recent interview after broadcast right the IPL team valued @ 8100Cr and net present value 916Cr only. [Time 17:40. Sanjiv Goenka At India Today Conclave East 2022; Talks About Investments, Russia-Ukraine War - YouTube] I don’t think they are sharing wrong information in public. May be they have included team cost and maintenance cost in it for 10 years.

Also, balance sheet is bit complex to understand. They have shown full revenue of FLS and their profit in balance sheet this is not correct.