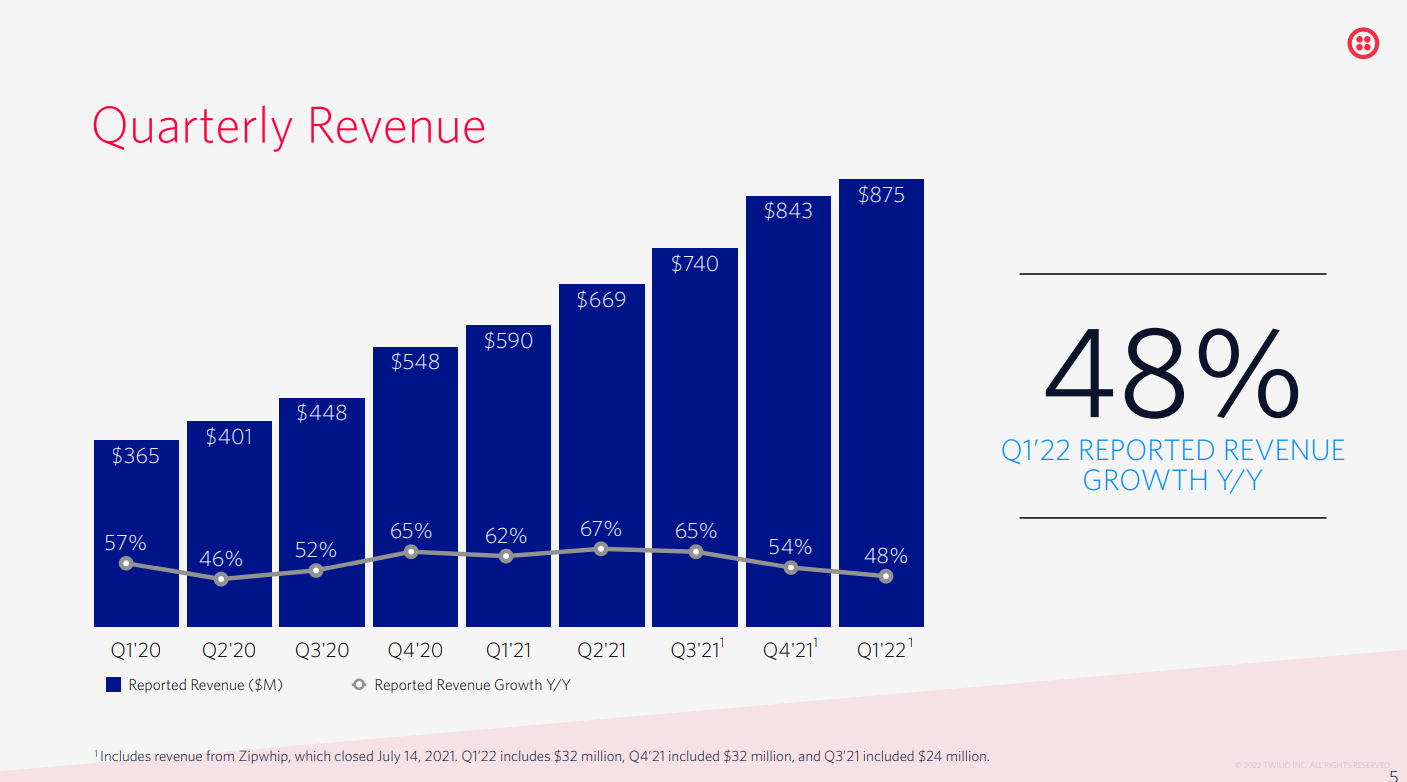

Twilio just reported quarterly results for March 2022. Revenue growth at 48%.

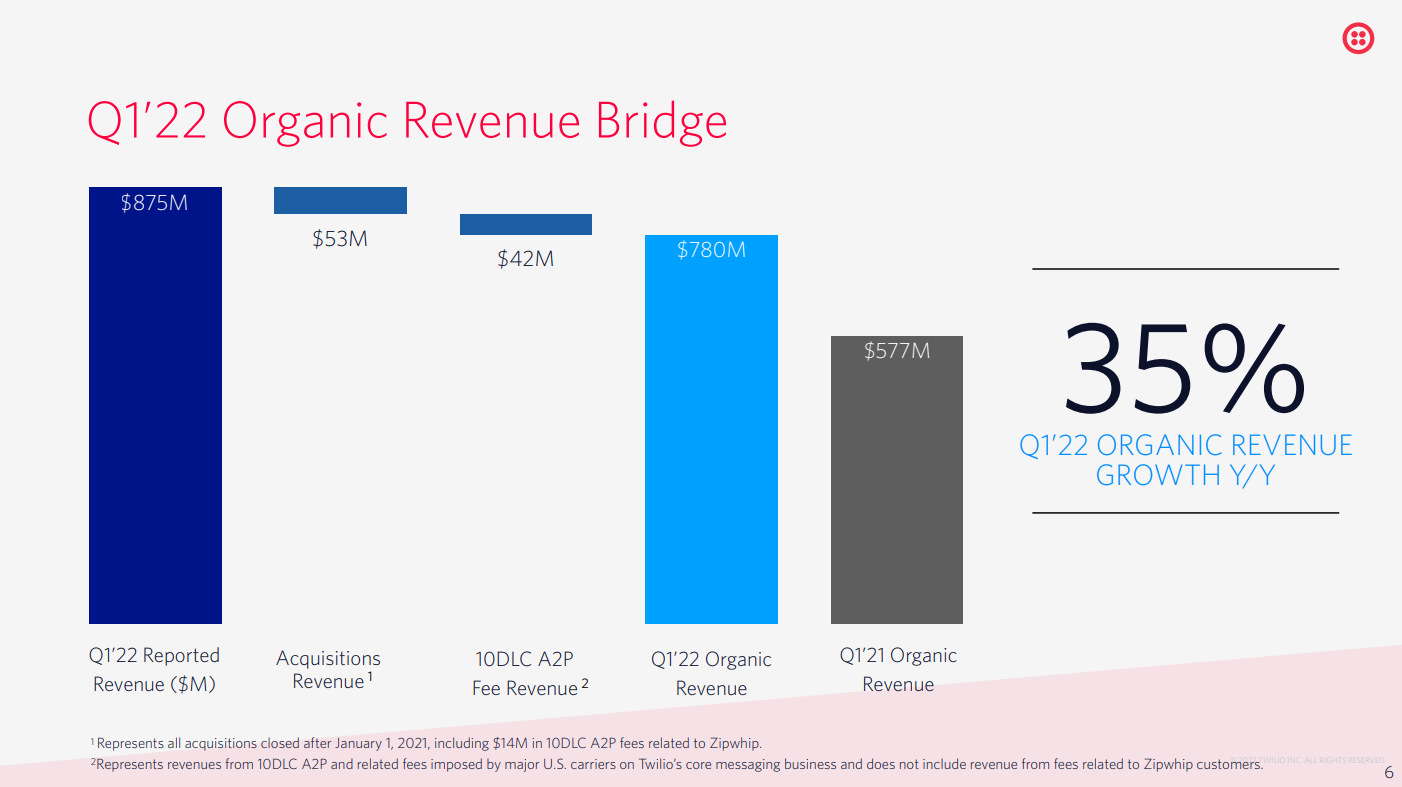

Organic Revenue Growth is at 35%

Full report here.

Takeaways for me:

- This industry has tremendous tailwinds. There is plenty of White Space in this industry.

- Twilio is down 72% from its high.

- 75% P/S derating down to 7 from 28. De-Frothing.

- Route is down 33%.

- 45% P/S derating down to 5.8 from 11.2

- Business momentum remains strong, valuations not so.

- What is needed for Route: Good revenue growth along with reasonable margin expansion (RM has low GM). Execution is key.

- What can help Route

- Organic growth of 25 to 30%

- Send clean momentum, this is a very high margin business

- Mr. Messaging, is slightly margin accretive, will add to revenues

- Masivian, good growth momentum

- Route has so far made good use of the equity capital raised in acquiring companies & tech. Management is walking the talk so far.

- What can go wrong

- Low growth

- Margin contraction

- Poor M&A Integration

Disc: Not an investment advice, RM is a significant part of my portfolio.