Hi everyone,

I wanted to discuss an upcoming IPO - Rossari Biotech which looks really interesting given recent market share gains, relatively smaller size and its unique flexible chemical manufacturing capabilities where company can interchange capacities across its segment categories and can manufacture any products depending on customer requirements (I am not sure if there are any other chemical companies with similar flexible business model). They also make ingredients and final products (BOTH) for their customers.

Rossari Biotech Ltd

Rossari Biotech is a specialty chemical manufacturing company which provides customized solutions to specific industrial and production requirements of customers primarily in the FMCG, apparel, poultry and animal feed industries through our diversified product portfolio comprising home, personal care and performance chemicals (HPPC); textile specialty chemicals; and animal health and nutrition products. Company operates in India as well as in 17 foreign countries including Vietnam, Bangladesh and Mauritius. According to the F&S Report, as on September 30, 2019, we are the largest manufacturer of textile specialty chemicals in India providing textile specialty chemicals in a sustainable, eco-friendly yet competitive manner. As a manufacturer of specialty chemicals, we focus on functionality and application of our products which form a key ingredient to our customers’ manufacturing and industrial processes.

Background

Promoters, Mr. Edward Menezes, and Mr. Sunil Chari, commenced this business in 2003. Both are career technocrats cumulatively having over 45 years of experience in the specialty chemicals industry. Promoters along with experienced Key Managerial Personnel who have over 80 years of experience in the specialty chemicals industry cumulatively.

-

Edward Menezes was previously associated with Clariant India Ltd (Red flag? as Clariant India had some corporate governance issue; see video from Candor Investing on Clariant https://youtu.be/xigATYEOfiY). He has over 25 years of experience in the specialty chemicals industry and has more than 10 years of experience in different roles within the company and has been actively involved in the day-to-day running of the company.

-

Sunil Chari is the Promoter and Managing Director of the company. He has over 20 years of experience in the specialty chemicals industry. He has more than 10 years of experience in different roles within the company and has been actively involved in the day-to-day running of the company.

Products and end market TAM

-

Home, personal care and performance chemicals (HPPC)

Rossari claims to be leading manufacturer of acrylic polymers in India (Source: F&S Report) and manufactures over 300 products in the soaps and detergent, paints, inks and coatings, ceramics and tiles, water treatment chemicals and pulp and paper industries. Rossari also manufactures institutional cleaning chemical formulations for hospitality, facility management, airports, corporates, food service, commercial laundry, malls, multiplexes, educational sector, places of worship etc. Company primarily operates in B2B model for our home, personal care and performance products with some direct selling to consumers under private label or on Amazon. HPPC constituted 46.11% and 37.81% of H1-20 and FY19 revenues respectively.

TAM - Rossari has ~10% market share (F&S report) with addressable market in India ~USD 1.6 billion. The personal care ingredients market is divided into active and

inactive ingredients. Company has presence in inactive ingredients with focus on silicone ingredients. This segment is 32% of the inactive ingredients market and 21% of total personal care ingredients market (active and inactive). The addressable market for Company in India personal care ingredients is approximately USD 0.8 billion. (Source: F&S Report). -

Textile specialty chemicals

Rossari Biotech is the largest manufacturer of textile specialty chemicals in India (Source: F&S). Company sells specialty chemicals for the entire value-chain starting from fiber, yarn to fabric, wet processing and garment processing and manufactures/sells ~1,520 products. These chemicals are used to enhance hydrophilic properties, anti-microbial properties, flame retardant properties, fragrance, water repellents and UV absorbing properties of the textiles. Revenue from textile chemicals constituted 44.82% and 52.18% of H1-20 and FY19 revenues respectively. Since textile industry consumes large amount of water and contributes to water pollution, Rossari focuses on providing eco-friendly chemical solutions which either replaces the highly polluting chemicals or reduces environment pollution of existing industrial process.

TAM - TAM Indian textile specialty chemicals is approximately USD 1.2 billion. Global green chemicals market is expected to grow at a CAGR of 10.5% during 2019 to 2023. According to the F&S Report, -

Animal health and nutrition

Rossari diversified into animal health and nutrition and supplies poultry feed supplements and additives, pet grooming and pet treats including for weaning, infants and adult pets. Company mainly sells products through B2B through distributors. Revenue from sale of animal health and nutrition products constituted 9.08% and 10.00% of H1-20 and FY19 revenues respectively.

TAM - TAM in Indian animal health and nutrition products is ~USD 0.14 billion. (Source: F&S Report)

New product pipeline - expanding to newer end markets!

Product and end uses

- Cement and construction chemicals: Specialty additive for cement processing

- Water treatment formulations: Boiler chemicals, Cooling tower chemicals, RO chemical, Waste water treatment

- Specialty formulation for breweries as well as dairies: Hinder bacterial growth, Break molasses, Cleaning sugar syrup

- Sanitizers for electronic gadgets: Mobile-antibacterial sanitizers for screens, Non-alcohol sanitizers

TAM for Construction chemicals market and water treatment formulations market is ~USD 1.1 billion and USD 1.7 billion respectively.

Expansion plans - planning to more than double existing capacity within FY21

Rossari’s existing plant in Silvassa has an installed capacity of 120,000 MTPA. Silvassa facility has flexible manufacturing capabilities for powders, granules and liquids. Silvassa capacity utilization was at 74.19%/93.94%/82.46% in Fiscal 2018/19/20.

New Dahej manufacturing facility has a proposed installed capacity of 132,500 MTPA. The Dahej Manufacturing Facility will also enjoy a proximity to the deep-water, multi-cargo port of Dahej which is a cost and logistical advantage. The proposed facility will be commissioned in Fiscal 2021.

R&D - competitive moat!

Rossari has qualified and experienced in-house R&D team which focuses on the new product development by collaborating with customers and customizes products as per customer expectations. Company has two R&D facilities – one within the Silvassa Manufacturing

Facility and another one in Mumbai (in IIT Mumbai). R&D facilities are recognized by the Department of Scientific and Industrial Research, Government of India and are also certified by a number of organizations including the Global Organic Textile Standards and the American National Standards Institute.

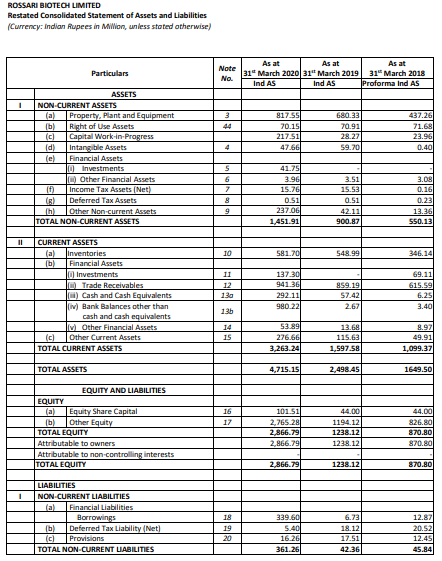

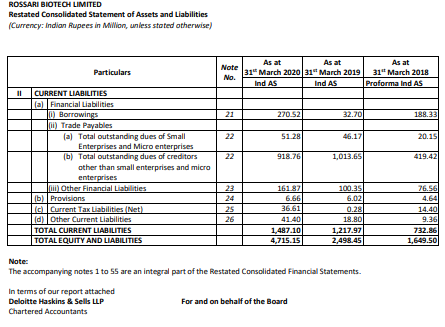

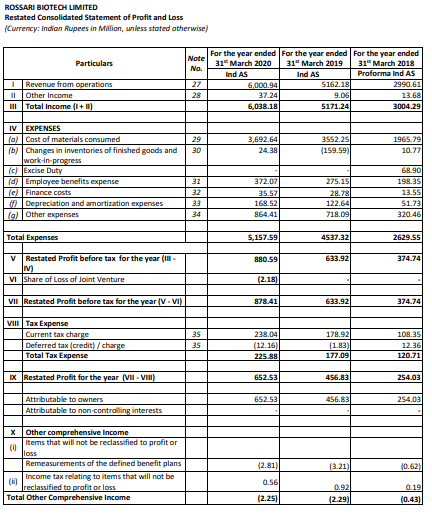

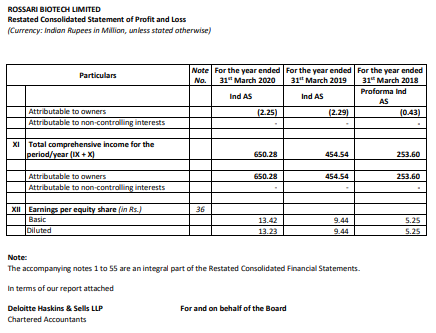

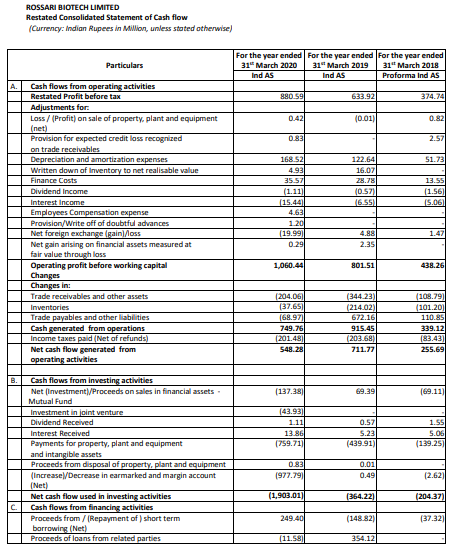

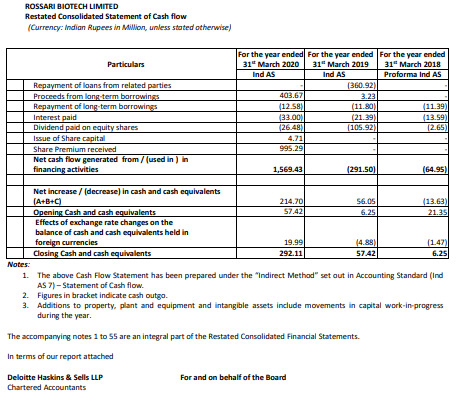

Financials - impressive!

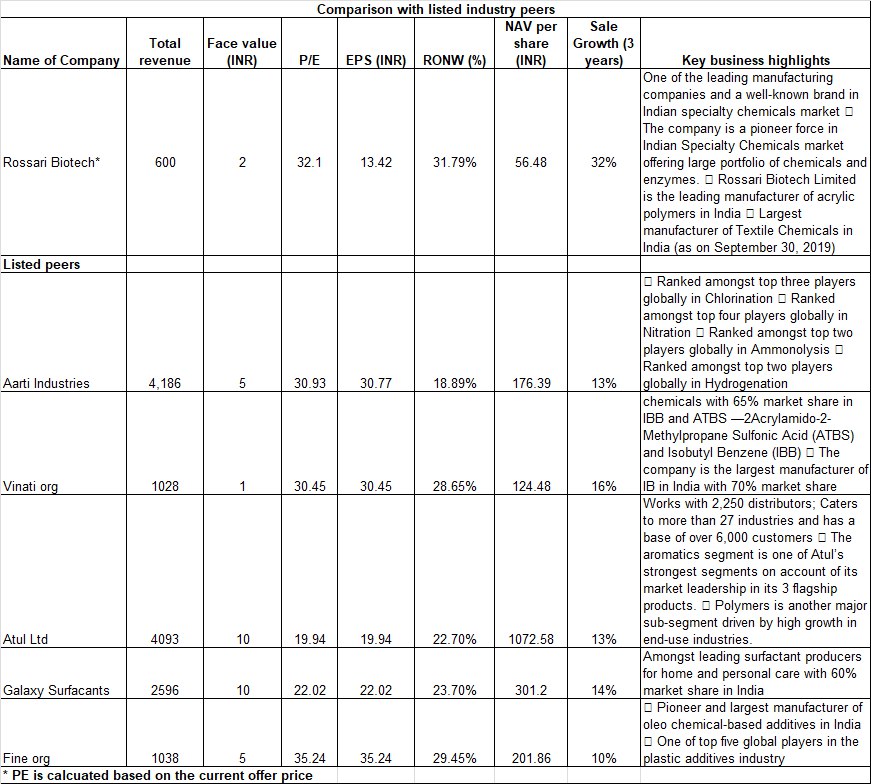

Valuation

IPO is coming at Rs. 423-425 which is slightly higher on PE basis (33.8) vs. peers.

Key risks and Red flags - looking for more on this from respected VP members

- Conflicts of interest may arise out of common business objects shared by our Company and some of our Group Companies and members of the Promoter Group. Certain our Group Companies, namely RBIPL, RMIPL and RSCPL and certain of the members of the Promoter Group, namely Rossari Hydra Chemicals Private Limited and Suisse Silicon Specialties Private Limited, share the common business objects and the constitutional documents of these Group Companies and members of the Promoter Group permit them to operate in the same line of business as us, which may lead to competition with such Group Companies and members of the Promoter Group. We may hence have to compete with such Group Companies and members of the Promoter Group for business, which may impact our business, financial condition and results of operations. The interests of our Group Companies and members of the Promoter Group may also conflict in material aspects with our interests or the interests of our Shareholders. Further, a conflict of interest may occur between our business and the business of such Group Companies and members of the Promoter Group in which our Promoters and Directors are involved with, which could have an adverse effect on our operations.

- Edward Menezes was previously associated with Clariant India Ltd (Red flag? as Clariant India had some corporate governance issue; see video from Candor Investing on Clariant https://youtu.be/xigATYEOfiY).