Moneycontrol said IPO got subscribed about 60%(news posted at around 3pm), Livemint said 35%(around 4 pm) and NDTV said the IPO got subscribed 38%(around 4.30pm).

https://youtu.be/OoTduRBp0a8 This might help.

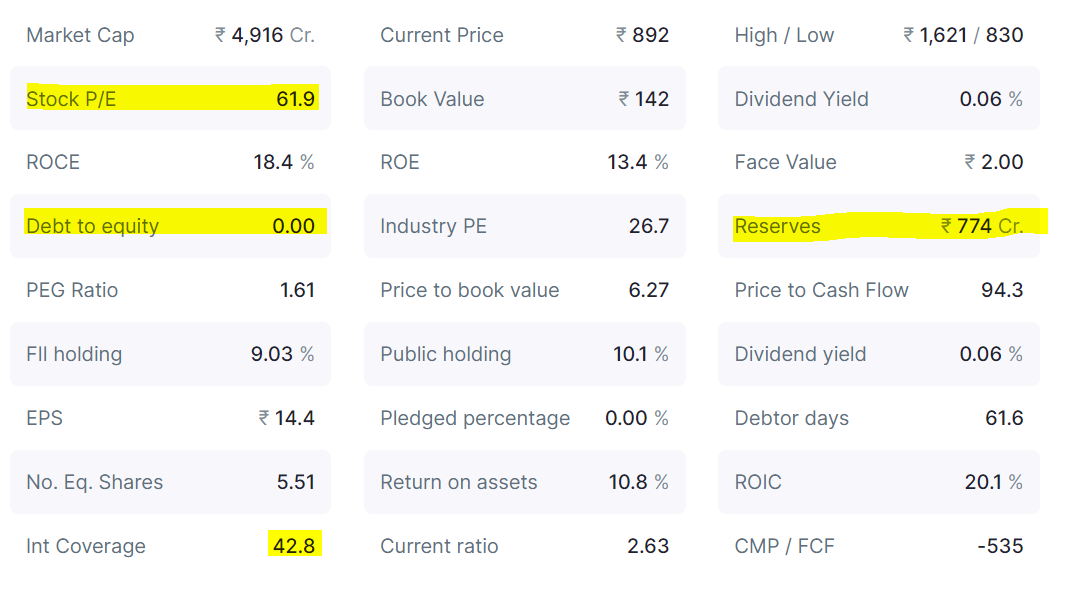

Listing price is 669! If we thought It was expensive earlier the PE is now at nosebleed levels. My current thoughts are to just hold however since I just got 1 lot allotted in the end so it’s a very small part of my PF. I’m very surprised by the response though. 65 percent+ is just crazy. If you ever needed proof that the market is full of froth this listing shows it is.

2 Likes

The total shares alloted were 1Cr something, see the Volumes on NSE, more than 2Cr… People are selling and re-enter at lower level to sell again I guess.

1 Like

Yup. Looks like it could be the reason. Anyway my safety of margin is HUGE now so il just hold. Will buy more if it ever falls around 500/550. Ignoring the knee-jerk to sell and book profit.

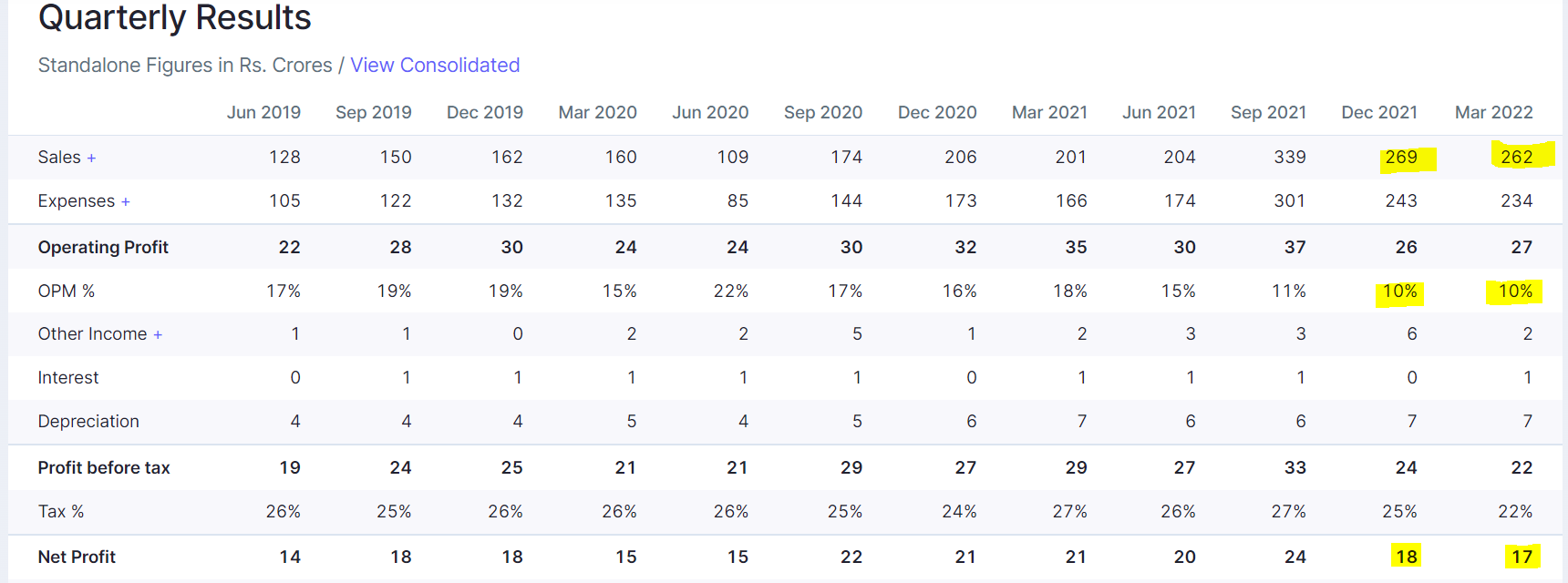

Okay results but not that inspiring given where valuations are.

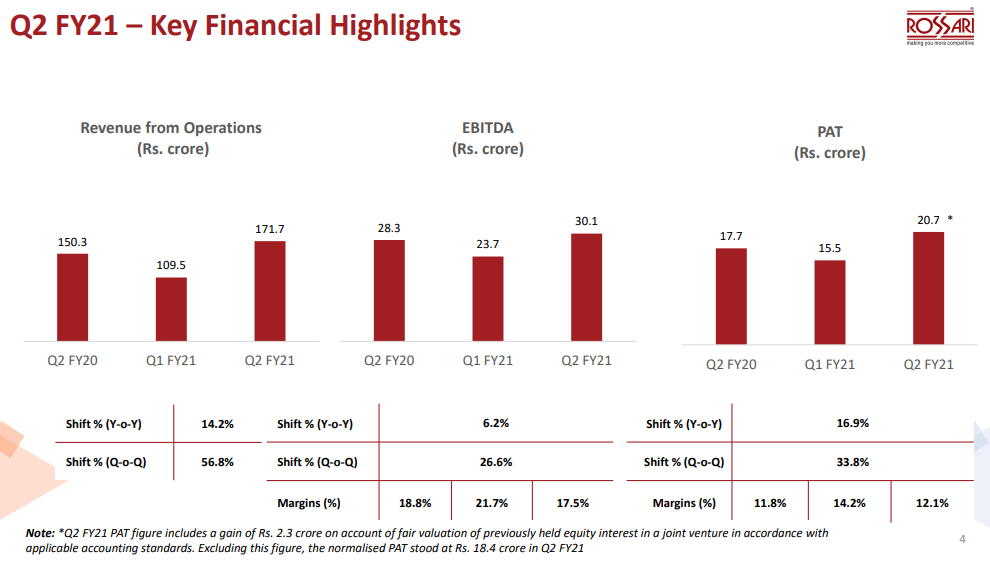

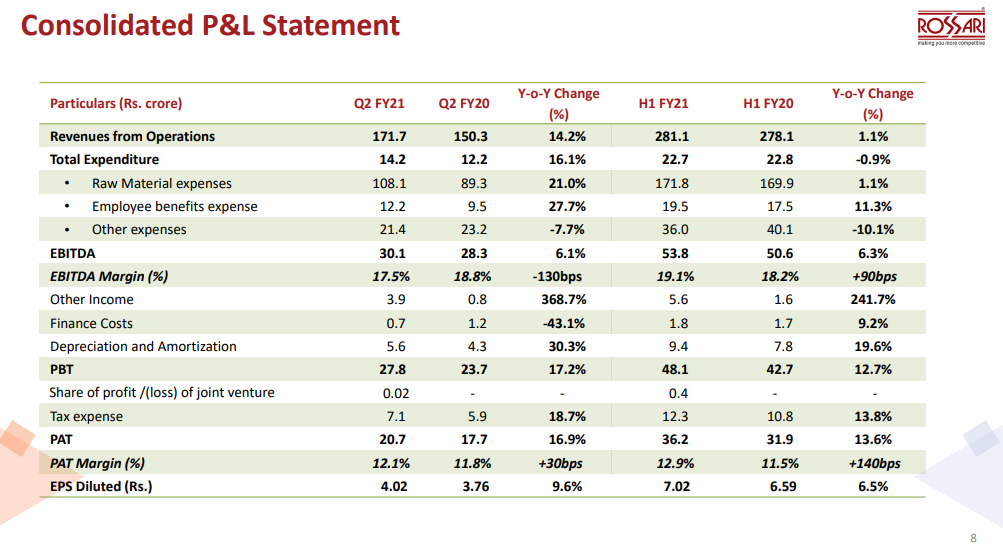

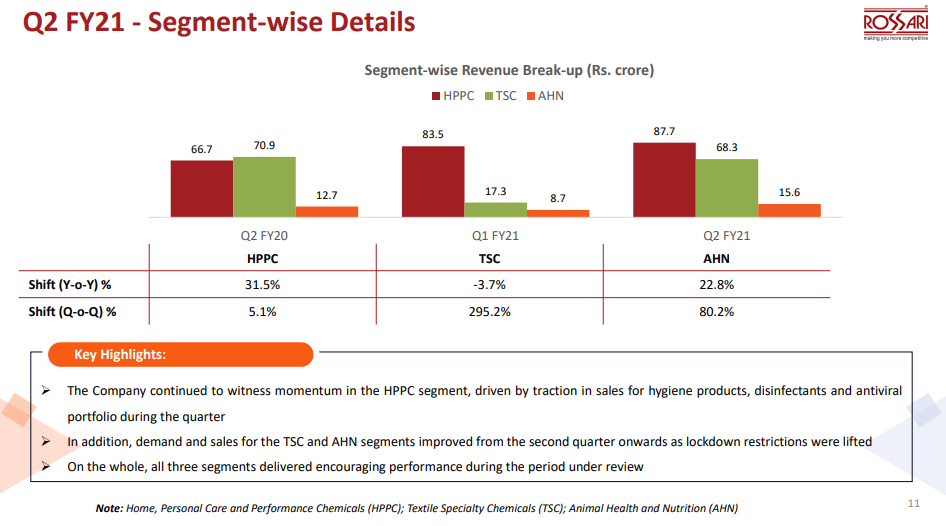

Check out 2Q21 results presentation and release.

2 Likes

Initiating coverage report by Nirmal Bang

1 Like

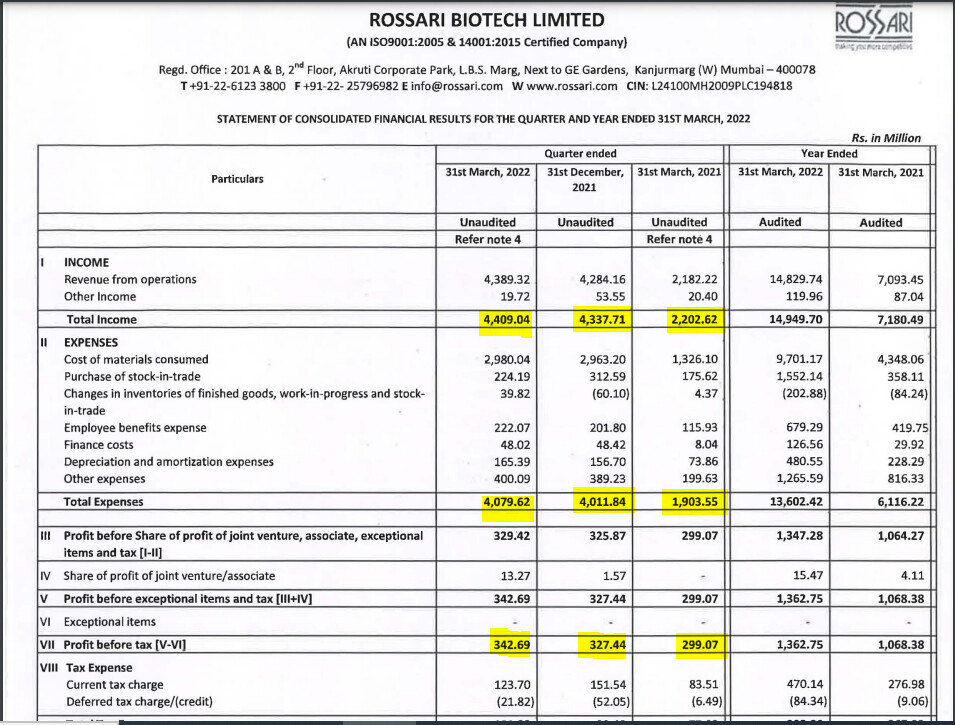

Rossari has reported great set of Q4 numbers (Standalone + Consolidated basis) both on Q-O-Q and Y-O-Y basis. Revenues, Profits and EPS have increased. Declared maiden dividend.

Disclosure: Invested.

1 Like

Today, Rossari has announced an Acquisition of Unitop Chemicals (https://www.unitopchemicals.com/) (UNITOP GROUP on Vimeo) for a consideration of 421 cr, whose FY 19-20 revenues were 280 Cr.

This company is into surfactants, emulsifiers and speciality chemicals and was growing at 20% YOY. The company has also 3 manufacturing units located in India and has a manufacturing capacity of 86,000 MTPA. I looked at their website, their products have diversified end applications. Further as per their website, the company is Market Leader in Non-ionic and Specialty Blended Surfactants and has established reputed Clientele in India & Abroad who are dealing in Non-ionic & Anionic products and blended specialty chemicals. The Company is well equipped with a team of technically and Commercially Qualified Professionals.

The Company is having its own Marketing Network in all major cities of India like Delhi, Kolkata, Chennai, Bangalore, Hyderabad, Cochin, Ahmadabad, Baroda, Jaipur etc. and also for overseas Marketing arrangements in countries like Malaysia, Thailand, Iran, Egypt, Jordan, Kuwait, Oman, Turkey, Germany and Latin American Countries etc.

In the last management con call, they mentioned they are actively looking at 2-3 acquisitions which are EPS accretive from day 1. Waiting for more details as to what it means to Rossari’s numbers in FY 22 and thereafter.

Acquisition.pdf (1.6 MB)

4 Likes

1 Like

Interesting co, scaling fast, aggressive growth plans, attracting good quality senior personnel. Can keep monitoring.

Valuations though at the current juncture are extremely pricey.

Was hearing the promoter in a B&K arranged call and he made an interesting comment, in which he said the co barely made any profits from 2010-2015.

Went back before FY17 and checked their financials.

Last 4 years basically, as the co grew, ebitda & pat margins went on an upswing. There is an argument in saying home & personal care drove this (FY18 18% of sales, FY21 56% of sales), textiles has relatively lower margins which was bulk of the business, and hence last 5 years vs prior 5 years cannot be compared which is fair enough. While the management is confident of sustaining margins at 16-18%, safer to be tad conservative here. They are providing value added solutions on top of intermediates, but still, my sense from transcripts is they don’t have any real pricing power in any of their segments. Margins in an inflationary environment (which can last for many years) can go down, as its playing out right now.

If one looks at the return ratios, they are extremely high, it’s a differentiated business model vs other chemical cos who have higher capex intensity, but the current profitability levels imply nearly ~50% average Pre-tax roce – just very high, I think, for this to be sustainable over a long period of time for a chemical co in which R&D is ~1.5%, and its the bigger foreign players present in the market who drive the constant innovation.

They have doubled their capacity and have utilized ~20-25% of the newly created one in FY21, while guiding for full utilisation in the next 3-4 years. So 20-25% of the additional sales from this expansion are already reflected in the FY21 pnl.

At current prices of 1250, it’s at ~10x trailing EV/S & 15x trailing P/B. One can try baking in different scenarios for the next 2-3 years, just very expensive. Taking a bull case of say 1400cr (peak sales as per management) sales by FY24 (base business, ignoring the recent acqs in YTDFY22), 18% Ebitda, 13% Pat, and still the co at 1250 would be at 5x FY24 EV/S, 28x FY24 EV/Ebitda, 38x FY24 PE!

While last few years ramp up have been tremendous, & the co has aggressive growth plans, to be on the conservative side, I would ideally want to monitor hpcc profitability over a longer period of time to have a better sense of what to expect here.

1 industry point to make is while their chemistries & focus is in inactive, not active chemistries, the global home & personal care space is shifting gradually towards active chemicals.

There are elements to like here, will keep monitoring, but valuations are very sore, even a ~25-30% drop wont interest me.

Very strong growth on sales can contribute to a bull case, esp with the rec acqs, 1HFY22 sales were indeed impressive.

5 Likes

Sir at 894 cmp with recent results, does it bring it to more reasonable valuations?

Highlights from the Rossari Biotech management commentary Operating performance

-

The sequential growth in revenue was aided by the easing of raw material prices and the addition of several customers.

-

Weak performance in its subsidiaries and loss of one major customer in Q3FY23 led to moderate growth YoY. However, the Management was able to recoup sales by adding several new customers.

-

It expects a gradual improvement in margin over the next two years.

-

EBITDA was impacted by certain one-off expenses (INR2.5–3cr) towards the acquisition of Tristar.

-

Weak performance by Tristar and Unitop resulted in an overall pressure on margin and subdued volume offtake.

-

Average capacity utilisation across segments stood ~55% in FY23. ROSSARI has no plans to expand capacity at present.

Home, personal care, and performance chemicals (HPPC) and textile specialty chemicals (TSC)

-

Subdued demand in its subsidiaries —Unitop and Tristar — led to a contraction in consolidated revenue.

-

ROSSARI faced headwinds with one customer. However, it was able to recoup the revenue run-rate from new customers.

-

It added HUL as a customer in the HPPC segment.

-

The company has multiple growth drivers in the HPPC segment. Going forward, revenue is expected to be driven by traction in water treatment chemicals and product additions in detergent and coating chemicals and silicon chemistry.

-

The slowdown in the TSC segment will continue in H1, but demand will improve from H2FY24.

Animal Health and Nutrition (AHN)

-

The YoY growth in this segment was due to healthy demand for its products.

-

The management expects revenue to double over the next two-to-three years as these products are value accretive and offer a higher margin.

-

The company added new products in vitamins and minerals. It will incur a small capex for vitamin premix in FY24.

Capex

- The company is expected to incur a capex of INR40cr-INR50cr in FY24/FY25.

Tristar Intermediates and Unitop Chemicals

-

Volume offtake in both subsidiaries remains subdued.

-

Revenue growth in Tristar was subdued owing to lower demand from Europe and Russia.

-

ROSSARI completed the acquisition of Tristar in Q1FY24, with the buyout of the balance (16%) stake for INR17cr. The entire acquisition was funded through internal accruals.

-

The management expects to complete the acquisition of Unitop in FY24.

-

It is planning to merge Unitop and Tristar by FY24-end to unlock synergies.

Guidance

- The management targets 20% growth over FY23 absolute EBITDA in FY24

(Source:Nuvama Research)

1 Like

Found something interesting but could not understand the logic. Appreciate if any member could help clarify this

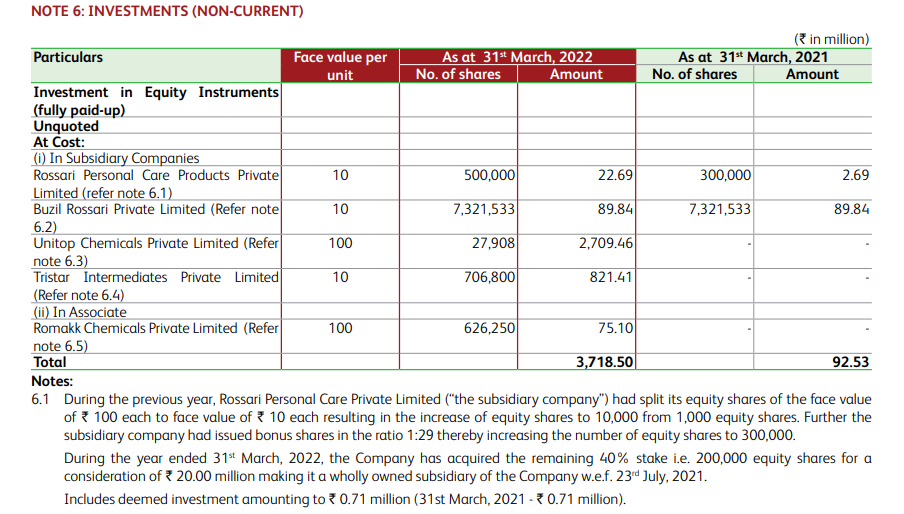

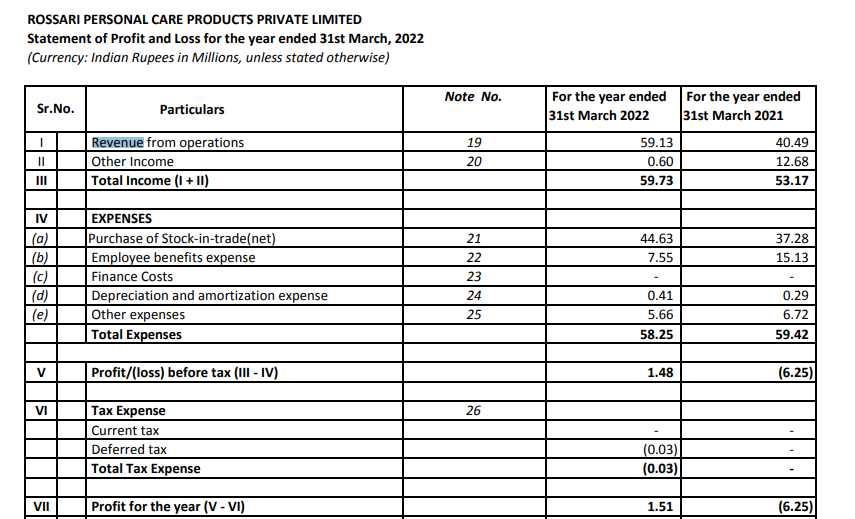

They valued inv. in subsidiary - Rossari Personal Care at 27L (aprox) in FY21, sell 40% stake & buy back the same 40% at much higher value within a year itself & value the company at 2.27Cr?

A 10x jump in valuation.

I looked at revenue numbers for Rossari Personal Care too which were 4Cr in FY21 & 6Cr in FY22 (ref image)

So 10x jump in valuation or routing money?

Understand that 2Crs is small amt. in a 1600Cr rev comapany but am I looking at it correctly or missing something here?

3 Likes

Hello, anyone tracking… Numbers are good all time high revenue , ebidta… stock price all time high 1500+ current price 755… why stock has not cheer up sep numbers… anything missing ?

Although the numbers are good but stock price appears overvalued to me at the moment. 550-650 will be a good range I think to go in big. It may take few years of earning growth & new innovative products to justify the previous all the time high of 1500 price. Let’s see.

Started accumulating slowly between 700-820 levels after I found out that it contract manufactures ENZO liquid detergent for reliance at a very affordable price ![]() compared to SURF and ARIEL. (Buy Enzo Intelomatic Front Load Liquid Detergent 2 L Online at Best Prices in India - JioMart.)

compared to SURF and ARIEL. (Buy Enzo Intelomatic Front Load Liquid Detergent 2 L Online at Best Prices in India - JioMart.)

It is the behavior of the market, and weak hands are stepped out as the trend for chemical in downwards across and headwinds contribute to panic selling, which is a bad combination for stock price. And the price when this hit at 1500 levels is in the period of tailwind time, and the formula for cyclical stock is that you invest in high PE and square off your position at low PE. And in regards to Rossori, it is a sound business with value in fundamentals, and with the recent results, we kind of see how the revenues are ticking upwards, and the commentary for the periodic UNITOP scale starting from Q3 FY24 is the lever for stock uptick, I believe. The stock price eventually scales up as revenue improves, and it is great that price is moving downward and allowing us to accumulate more. Be patient; watch for the near term.

3 Likes

Rossari Biotech Limited Q4 and FY24 Earnings Conference Call Transcript April 30, 2024

-

We are pleased to report another strong quarter for the company, driven by healthy Y-o-Y growth in both revenues and profits. This performance was largely driven by the expansion of our HPPC business.

-

While challenges in our TSC and AHN divisions persisted due to external industry headwinds, we remain optimistic about the recovery of these segments in the upcoming fiscal.

-

We are particularly focused on specialty surfactants, phenoxy series, institutional cleaning, and performance chemicals.

-

Our recent expansion plan at Dahej along with increased its ethoxylation capacity, will allow us to meet growing demand in these key segments.

-

We expanded our customer base for key HPPC products, leading to a robust 18% growth in this division.

-

Our Institutional Cleaning segment has achieved exceptional results during the year, serving major sectors such as airports, railways, hotels, and healthcare that rely on specialized cleaning solutions.

-

We take pride in our growth from an Rs. 700 crore top line to our expected milestone of around Rs. 2,000 crore top line in FY25.

2 Likes