Hi everyone,

I came across this company " Ritco Logistics " and found it a good prospect for further analysis.

Incorporated in 2001, Ritco Logistics Limited provides surface logistics services, including transportation of cargo and warehousing services.

The scope of services includes contract logistics, less than truck load (LTL) service and fleet rental services.

The company has pan-India presence through its 29 branches. It has seven warehouses and an in-house fleet of 304 trucks and about 1,000–1,200 attached vehicles to support its operations.

Working Model

The company has an asset-light business model with an in-house fleet of 304 trucks, while about 60–65% of the total requirement is met through fleet hired from the spot market on a daily basis

Important Features

(01) Domestic Leader in Less than Container Load (LCL) Consolidation segment of

Multimodal Logistics

(02) The largest provider of integrated logistics solutions in India for CL.

(03) Only Indian Company with significant presence across all industrial belt in the country…

(04) Amongst very few Indian companies specializing in contract logistics, a business with significant growth opportunities and potential

VALUATION

The company is available at market cap of 66 crores.

Since the company is clocking sales of around 480 crores, i found the valuation attractive.

Taking average net profit of 8 crores, the P/E comes at 8.25.

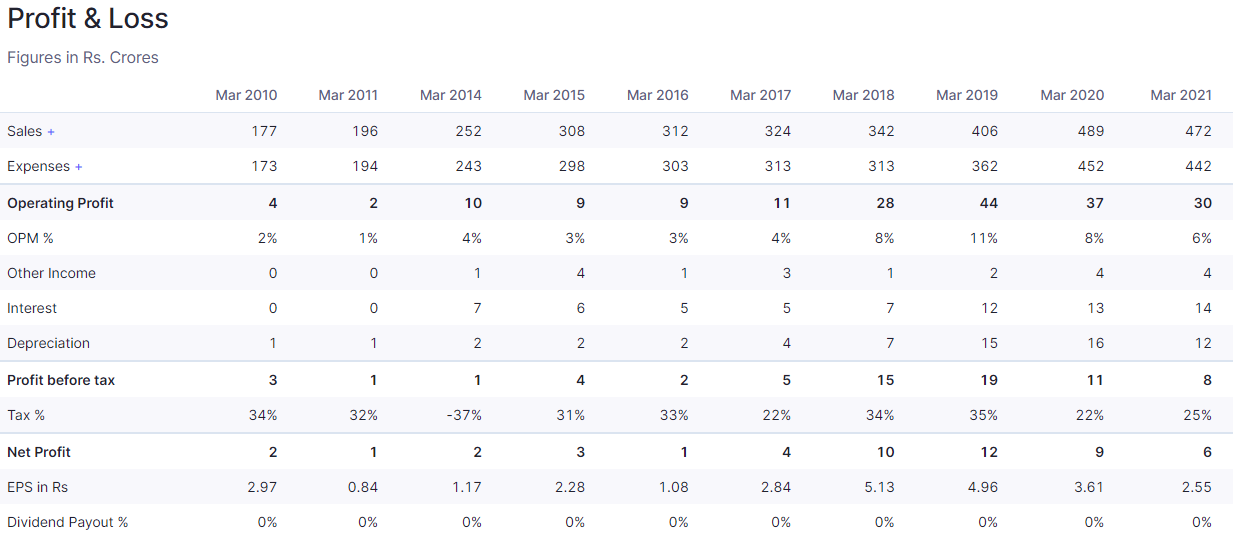

Profit and Loss

The company is aggressively growing its revenue by taking in new clients.

The company has an established customer base comprising reputed players including Gail India Ltd., Brahmaputra Cracker and Polymer Limited, ONGC Petro

Addition Limited, Nestle India Limited, etc.

Operating Margin is around 6 - 8%

Since the company is working on IT infrastructure and ERP systems, the slight improvement of margin is expected.

Rising Fuel cost is one of the problem. Transferring the cost to customers can be trouble due to stiff competition.

Interest Coverage

The yearly interest installment can be easily paid from yearly operation. We can say the survival risk of company is low.

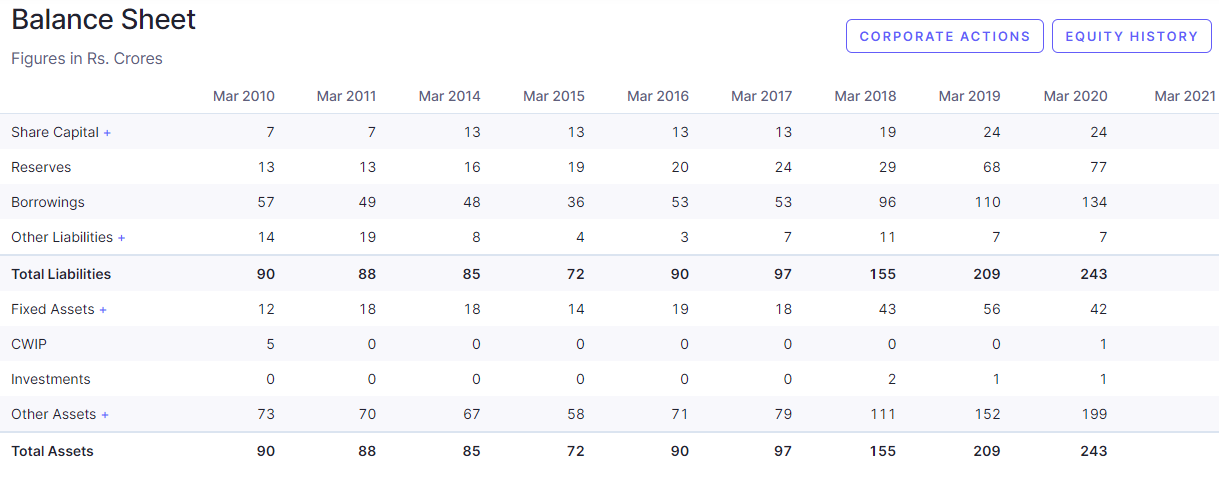

Balance Sheet

Share issue

Recently the company has issued more shares for warehouse development and incorporation of WRP systems.

Debt

Rising debt is one of the issue of company.

Logistics sector is a working capital intensive business and the company has been taking working capital loan for is daily operations.

Debt to equity ratio is 1.32 .

It is slightly on higher side.

Debtor Days

Debtor days has increased to 110 days.

This increase is caused to covid situation which i think is a temporary phenomon.

I think the situation will improve for company in next 2-3 years.

Cash Flow

The company has generated positive FCF for 2021.

All the previous negative cash flow is attributed to high receivables.

Receivables might not be a problem since it has reputed client base which is less likely to default.

Management

The management appears to be good and experienced with more than 25 years of experience.

Recently they have hired CEO from Delhi college of Engineering with good amount of experience in reputed logistics brand.

Positive Points

(01) Reputed client base

The company has an established customer base comprising reputed players including Gail India Ltd., Brahmaputra Cracker and Polymer Limited, ONGC Petro

Addition Limited, Nestle India Limited, etc

(02) Asset Light Model

The company has an asset-light business model with an in-house fleet of 304 trucks, while about 60–65% of the total requirement is met through fleet hired from the spot market on a daily basis

(03) Management Mindset

The management has been taking steps to improve the efficient and productivity of operation throughout the incorporation.

Ritco is further consolidating by increasing its warehouse footprint by 1 million sq.ft. in the next financial year through Built to Suite warehouse infrastructure.

Negative Points

(01) Rising fuel price and spot price of truck fleets destroys profitability.

(02) High receivable is a concern.

(03) Highly competitive and fragmented market – The road logistics sector is highly fragmented with most business being generated by the unorganised segment

Ratings

ICRA Ratings = BBB+

https://www.icra.in/Rationale/ShowRationaleReport/?Id=101007

If anyone has done any kind of research, please share your thoughts on the company.

PS : Not invested. Tracking the company.